Coating Agents for Synthetic Leather Market Size, Bio-Based Polyurethane Innovation, and Sustainability-Driven Growth

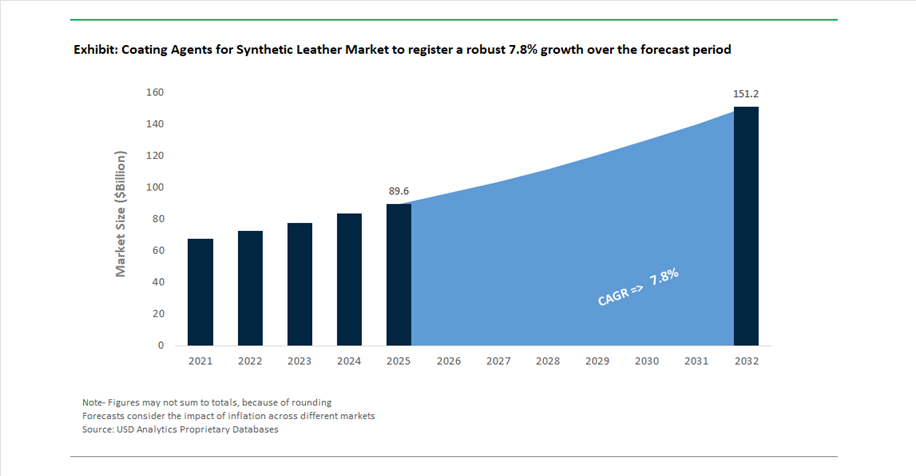

The global coating agents for synthetic leather market was valued at $89.6 billion in 2025 and is projected to expand at a CAGR of 7.8% between 2025 and 2032, reaching $151.6 billion by 2032. This strong growth trajectory is driven by rising demand across automotive interiors, footwear, fashion apparel, furniture upholstery, and sportswear, where synthetic leather coatings provide essential attributes such as flexibility, abrasion resistance, chemical stability, and premium surface aesthetics.

A key structural transformation shaping the market is the shift toward waterborne polyurethane (PU), bio-based resins, and low-VOC coating technologies, replacing traditional solvent-based systems. Increasing regulatory scrutiny on hazardous chemicals, particularly Dimethylformamide (DMF), is accelerating adoption of eco-friendly coating agents that align with global environmental and occupational safety standards. This transition is particularly pronounced in Europe and North America, while Asia-Pacific continues to scale production with a growing emphasis on sustainable exports.

Technological innovation is expanding the functional scope of synthetic leather coatings. Advanced formulations now enable soft-touch finishes, enhanced haptic properties, UV resistance, anti-microbial functionality, and improved recyclability, supporting premiumization trends in automotive and consumer goods sectors. Additionally, the integration of smart materials and responsive surfaces is redefining synthetic leather applications, particularly in next-generation mobility solutions.

The market is also benefiting from increasing penetration of vegan leather alternatives, driven by shifting consumer preferences and corporate sustainability commitments. Brands across automotive and fashion industries are actively transitioning toward animal-free, performance-engineered materials, creating significant demand for high-performance coating agents that replicate the look and feel of genuine leather while offering superior durability and environmental performance.

Strategic Acquisitions, Smart Surface Technologies, and Low-Carbon Coatings Reshaping Competitive Dynamics

The competitive landscape of the coating agents for synthetic leather market is being reshaped by major acquisitions, advanced material innovation, and sustainability-led strategic initiatives. A landmark development occurred in February 2026, when Henkel announced its €2.1 billion acquisition of Stahl Group, a global leader in specialty coatings for flexible materials. This acquisition significantly strengthens Henkel’s position in synthetic leather and performance coatings, leveraging Stahl’s expertise in water-based, environmentally responsible solutions widely used in automotive and fashion applications.

Innovation in smart and functional materials is accelerating rapidly. In March 2026, Covestro, in collaboration with Marquardt and E Ink, unveiled a responsive synthetic leather surface integrating E Ink display technology, enabled by a transparent waterborne PU coating. This breakthrough allows dynamic color-changing functionality in automotive interiors while maintaining durability and tactile quality, highlighting the convergence of electronics and coated materials.

Sustainability remains a central focus across product development pipelines. At Techtextil 2026, Covestro introduced its latest INSQIN® bio-based polyurethane technologies, incorporating mass-balanced and partially renewable feedstocks to improve recyclability and reduce lifecycle emissions. Similarly, Stahl’s Ympact® product line, rolled out globally in early 2025, utilizes bio-based and recycled carbon content, enabling manufacturers to meet stringent ESG targets without compromising performance.

Supply chain optimization and operational efficiency are also key strategic priorities. Evonik’s restructuring of its North American distribution network (February 2026) aims to enhance technical service capabilities and supply reliability for coating additives, particularly in waterborne and UV-curable systems. In parallel, Huntsman’s $100 million cost-reduction program (January 2026) reflects ongoing competitive pressures in the polyurethane value chain, especially amid oversupply conditions in Asia-Pacific.

Digitalization and lifecycle transparency are gaining prominence in material selection processes. Dow’s Carbon Footprint Ledger, recognized with the 2026 CIO 100 Award, enables manufacturers to track and verify the environmental impact of coating agents, supporting compliance with global sustainability frameworks. Additionally, Covestro’s strategic partnership with XRG (December 2025) and its extended collaboration with Team Sonnenwagen (February 2026) are enhancing R&D capabilities, particularly in UV resistance, weatherability, and high-performance coatings tested under extreme conditions.

EU REACH DMF Restriction Forcing Rapid Transition to Waterborne Polyurethane Systems

The synthetic leather coatings industry is undergoing a decisive chemical transition as the restriction on N,N-Dimethylformamide (DMF) under REACH Annex XVII (Entry 76) enters full enforcement. DMF has historically been a critical solvent in polyurethane-based coating processes, particularly in direct coating and wet-spinning applications. However, its classification as a reproductive toxin has triggered stringent regulatory limits, fundamentally altering formulation strategies.

The compliance threshold is highly restrictive. As of late 2025, DMF concentrations in coating mixtures must not exceed 0.3% by weight, effectively eliminating its use in most commercial applications within the European Economic Area. In addition, facilities operating under limited exemptions must adhere to strict occupational exposure limits of 15 mg/m³, requiring the implementation of closed-loop systems and advanced vapor capture technologies.

This regulatory pressure has accelerated industry-wide reformulation. By early 2026, approximately 85% of premium synthetic leather manufacturers have successfully transitioned to DMF-free systems, primarily utilizing waterborne polyurethane dispersions. This shift is not only addressing compliance but also improving workplace safety, with projected reductions of up to 70% in chemical-related reproductive toxicity risks compared to 2020 levels.

From a strategic standpoint, DMF elimination is redefining supplier qualification criteria, with OEMs and brands increasingly mandating solvent-free or waterborne coating systems as a baseline requirement. This transition is positioning waterborne polyurethane technologies as the dominant standard in synthetic leather coating agents.

China’s GB 30981.2-2025 Driving VOC and Heavy Metal Compliance in Synthetic Leather Coatings

China’s enforcement of GB 30981.2-2025, effective February 1, 2026, is introducing a comprehensive regulatory framework governing volatile organic compounds and hazardous substances in industrial coatings, including those used for synthetic leather. This standard represents a significant tightening of environmental and safety requirements, aligning Chinese manufacturing practices with global benchmarks.

The regulation imposes strict VOC ceilings, requiring waterborne coating systems to maintain VOC levels below 200 g/L to qualify for green manufacturing incentives. This is accelerating the shift away from solvent-borne formulations across domestic production facilities. In parallel, the standard introduces stringent limits on heavy metals, including lead (≤ 90 mg/kg), cadmium (≤ 75 mg/kg), and mercury (≤ 60 mg/kg), ensuring compliance with international safety standards such as EN 71-3.

Consumer safety considerations are also central to the regulation. For synthetic leather products intended for direct human contact, phthalate concentrations must remain below 0.1%, impacting coatings used in apparel, footwear, and upholstery applications. This is driving the adoption of safer plasticizers and non-toxic additive systems.

The commercial implications are significant. Manufacturers that fail to achieve certification under GB 30981.2-2025 are increasingly excluded from major automotive and fashion supply chains, both domestically and internationally. As a result, compliance is becoming a critical determinant of market access, reinforcing the transition toward low-VOC, non-toxic coating technologies.

Waterborne PU Coatings Enabling Premium Automotive “Vegan Leather” Interiors

The automotive industry, particularly within the electric vehicle segment, is creating a high-value opportunity for advanced waterborne polyurethane coating agents designed for synthetic leather interiors. As OEMs move toward “vegan leather” alternatives, coating performance must replicate the tactile qualities and durability of traditional Nappa leather while meeting stringent environmental standards.

Modern waterborne polyurethane dispersions are achieving performance parity with solvent-based systems. Advanced formulations now deliver Bally Flex test results exceeding 100,000 cycles at -20°C, ensuring durability under extreme conditions. At the same time, these coatings significantly reduce volatile emissions, lowering interior fogging levels by up to 90%. This is a critical parameter for improving in-cabin air quality and achieving high consumer satisfaction scores.

Energy efficiency is another key advantage. Low-temperature curing systems, operating at 80°C to 100°C, reduce energy consumption in production by approximately 20%, enhancing the sustainability profile of automotive manufacturing processes. Additionally, these coatings increasingly integrate multifunctional additives, including UV stabilizers and anti-soiling agents, reducing the need for secondary finishing treatments.

Bio-Based Polyol Coating Agents Driving Sustainable Innovation in Footwear and Apparel

The fashion and footwear industries are creating strong demand for bio-based coating agents that align with circular economy objectives and carbon reduction targets. Bio-based polyols derived from renewable feedstocks such as castor oil, soybean oil, and agricultural waste are emerging as a key innovation in synthetic leather coatings.

These materials offer significant environmental benefits. Leading bio-based polyurethane coatings now achieve biogenic carbon content levels between 40% and 65%, as verified through standardized testing methodologies. This transition reduces the global warming potential of synthetic leather products by approximately 35%, supporting sustainability goals across the fashion supply chain.

Market adoption is accelerating rapidly. By early 2026, approximately 25% of major global footwear brands have implemented mandates requiring at least 30% bio-based content in synthetic leather coatings. This is driving increased investment in renewable raw material sourcing and bio-based polymer development.

Importantly, performance limitations associated with bio-based materials are being overcome. Advanced formulations now demonstrate hydrolysis resistance of up to 10 years in accelerated aging tests, exceeding the durability benchmarks previously associated with plant-derived resins. This ensures that sustainability improvements do not come at the expense of product longevity or quality.

Water-Borne PUD Coatings Lead Synthetic Leather Market with 44% Share Driven by VOC Compliance and Premium Performance

Technology Analysis: Polyurethane Dispersions (PUDs) Dominate with Breathability and Automotive-Grade Properties

Water-borne coatings, particularly polyurethane dispersions (PUDs), hold a leading 44.0% share of the coating agents for synthetic leather market in 2025, driven by stringent VOC regulations and the shift toward eco-friendly manufacturing. These coatings form flexible, durable films through water evaporation and polymer coalescence, delivering superior soft-touch feel, breathability (high moisture vapor transmission - MVTR), and low odor performance. Unlike solvent-borne systems, water-borne PUDs enable microporous structures, allowing moisture escape—critical for automotive seating, footwear, and upholstery applications. The rapid transition is largely fueled by China’s regulatory crackdown on solvent-based (DMF) coatings, as the country accounts for over 70% of global synthetic leather production. Additionally, advancements in crosslinked PUD chemistry now provide high abrasion resistance, chemical durability, and UV stability, achieving full performance parity with solvent-based alternatives, reinforcing dominance in the synthetic leather coatings market.

Automotive Sector Leads Synthetic Leather Coatings Market with 36% Share Driven by Vegan Leather and Premium Interior Demand

End-Use Industry Analysis: Automotive Interiors Drive High-Volume and High-Value Coating Adoption

The automotive segment accounts for 36.0% of the synthetic leather coating agents market in 2025, driven by the widespread adoption of PU-based “vegan leather” in vehicle interiors. Synthetic leather is extensively used in seating, door panels, dashboards, steering wheels, and headliners, offering advantages such as lightweight construction (20–30% lighter than genuine leather), design flexibility, and cost efficiency. Mass-market vehicles increasingly adopt synthetic leather as standard, boosting volume demand, while luxury OEMs focus on premium soft-touch finishes, sustainable materials, and advanced coating technologies. Water-borne PUD coatings are preferred due to their low VOC emissions, anti-fogging properties, and resistance to UV exposure, heat (120°C+), chemicals, and abrasion, ensuring long-term durability. Additionally, the growing trend toward bio-based and recycled materials in automotive interiors aligns with sustainability goals, further accelerating demand in the global synthetic leather coatings market.

Coating Agents for Synthetic Leather Market Competitive Landscape Driven by Polyurethane Dispersions, Silicone Coatings, and Sustainable Vegan Leather Technologies

The coating agents for synthetic leather market is driven by polyurethane dispersions (PUDs), silicone-based coatings, and bio-based formulations. Leading players are focusing on low-VOC coatings, smart surfaces, and high-performance vegan leather finishes to meet demand across automotive interiors, footwear, fashion, and flexible electronics applications.

Stahl strengthens synthetic leather coatings leadership through bio-based PUDs and automotive upholstery systems

Stahl Holdings is a pure-play leader in coating agents for synthetic leather, focusing exclusively on specialty coatings following its 2026 restructuring. The acquisition by Henkel for $2.5 billion strengthens its position in industrial coatings and surface treatments. Its Stay Clean technology is widely adopted in automotive interiors, preventing dye transfer and improving durability of light-colored synthetic leather. The company leads in renewable carbon content with bio-attributed polyurethane dispersions aligned with sustainability goals. Integrated primer-to-finish systems enable strong penetration in OEM automotive and premium upholstery markets. Product strategy focuses on high-performance coatings, sustainability, and automotive-grade applications.

Covestro drives innovation with waterborne PU coatings and smart surface technologies for EV interiors

Covestro is a global leader in high-performance polymer coatings, with €12.9 billion in revenue and a strong global manufacturing footprint. Its INSQIN waterborne PU technology enables transparent coatings for smart surfaces, supporting EV dashboards and display-integrated interiors. The company is advancing TPU-based solutions such as Desmopan AIR and FLY for cushioning and lightweight coating applications. Platilon TPU films bridge synthetic leather coatings with flexible electronics and wearable technology. Covestro is committed to climate neutrality by 2035 through bio-based and mass-balanced raw materials. Product innovation focuses on waterborne coatings, smart materials, and sustainable polymers.

Dow expands synthetic leather coatings with silicone-based systems and low-VOC compliance

Dow Inc. is a key player in silicone-based coating agents, delivering superior weatherability and soft-touch finishes for synthetic leather applications. Its DOWSIL coatings provide high abrasion resistance and easy-clean properties, particularly in bags and accessories markets. The company is investing in high-solids and low-VOC coating systems to comply with REACH and Prop 65 regulations. Strong regional supply chains ensure stability amid global trade volatility. Vertical integration into feedstocks supports cost efficiency and supply reliability. Product development focuses on silicone coatings, durability, and regulatory compliance.

Evonik enhances coating performance with advanced additives for gloss control and defect prevention

Evonik Industries is a leading supplier of coating additives for synthetic leather, with strong performance from its Custom Solutions segment generating €5.4 billion in 2025. Its TEGO additives improve surface energy, enabling smooth coatings and eliminating defects such as orange peel. The company supplies matting agents and crosslinkers that control gloss levels and chemical resistance in vegan leather products. Expansion of distribution networks in North America strengthens supply security and technical support. Digital formulation tools accelerate product development cycles. Product strategy focuses on coating additives, surface optimization, and high-quality finishes.

Lubrizol advances synthetic leather coatings with polyurethane dispersions and UV-curable technologies

Lubrizol Corporation is a major innovator in polyurethane-based coating agents, particularly through its Sancure dispersions for automotive and furniture applications. Its Aptalon hybrid technology combines polyamide strength with PU flexibility, supporting high-performance footwear coatings. The company is investing in UV-curable coatings to reduce energy consumption and improve manufacturing efficiency. Strategic supply chain diversification enhances resilience against market volatility. Lubrizol’s co-development approach with global brands ensures customized solutions for performance-driven applications. Product development focuses on PU coatings, UV curing, and high-durability synthetic leather finishes.

China Coating Agents for Synthetic Leather Market: Waterborne Transition and Bio-Based PU Innovation Driving Scale

China continues to dominate the coating agents for synthetic leather market, supported by its massive manufacturing ecosystem and rapid transition toward green chemistry. Advanced facilities such as Allnex’s Jiaxing plant are accelerating production of UV-curable and waterborne polyurethane (PU) resins, tailored for high-durability synthetic leather applications.

Environmental regulations have driven a 45% increase in adoption of DMF-free PU coating agents, particularly in Fujian and Zhejiang. The booming New Energy Vehicle (NEV) sector is a major demand driver, with silicone-based coatings used in fire-retardant battery curtains and premium vegan interiors. Additionally, strong R&D investment in Shanghai is advancing nanotechnology-enabled topcoats with enhanced scratch and hydrolysis resistance. Government-backed initiatives promoting bio-based polyols from agricultural waste are further reducing carbon footprints, reinforcing China’s leadership in sustainable synthetic leather coatings.

United States Coating Agents for Synthetic Leather Market: High-Performance Automotive and Defense Applications Driving Innovation

The United States market is characterized by strong demand for high-performance coating agents, particularly in automotive, semiconductor, and defense applications. The CHIPS Act is boosting demand for ESD (electrostatic discharge) coating agents used in cleanroom-grade synthetic leather for semiconductor facilities.

Automotive OEMs are increasingly specifying polycarbonate-based PU coatings to ensure long-term durability (up to 10-year hydrolysis resistance) in EV interiors. Sustainability trends are also shaping the market, with growing adoption of bio-attributed PU coatings containing over 50% renewable content. Defense applications remain critical, with updated military standards favoring fluorinated coating agents for chemical and biological resistance. Additionally, EPA regulations are accelerating the transition toward high-solid, powder, and solvent-free coating systems, while footwear brands are investing in fully recyclable TPU coatings to support circular economy initiatives.

Germany Coating Agents for Synthetic Leather Market: REACH Compliance and Bio-Based Resin Leadership Driving Sustainability

Germany leads the global market in eco-compliant coating agent innovation, driven by strict REACH regulations and circular economy principles. The industry is rapidly transitioning toward PFAS-free and phthalate-free coating agents, ensuring compliance with evolving European safety standards.

A key innovation is the commercialization of lignin-based coating agents, providing renewable alternatives to petroleum-derived chemicals. German manufacturers are also pioneering LED-UV curing technologies, reducing energy consumption by over 20% while minimizing thermal stress on substrates. Growth in healthcare and aerospace sectors is driving demand for antimicrobial silver-ion coatings and smoke-toxicant-free (FST) coating agents for cabin interiors. Additionally, the integration of Digital Product Passports (DPP) enables real-time lifecycle tracking, reinforcing Germany’s leadership in sustainable synthetic leather coatings.

India Coating Agents for Synthetic Leather Market: PLI-Driven Growth and Footwear Expansion Fueling Demand

India is rapidly emerging as a global hub for synthetic leather coating agents, supported by strong government incentives and expanding industrial applications. Under the PLI Scheme (Round III), investments of ₹6,708 crore ($805 million) are being directed toward high-value technical textiles and coating technologies.

The footwear industry is a major growth driver, with mega clusters in Tamil Nadu and Haryana driving a 20% annual increase in demand for hydrolysis-resistant PU coatings. Infrastructure and transportation sectors are also contributing, particularly through the expansion of Vande Bharat trains, which require fire-retardant coated materials. Domestic companies are scaling production of waterborne PU dispersions (PUDs) to reduce import dependency. Additionally, rising demand for bio-based coatings derived from cork and pineapple is supporting India’s entry into sustainable fashion markets, positioning the country as a key growth engine.

Vietnam Coating Agents for Synthetic Leather Market: Footwear Manufacturing Dominance and Automation Driving Efficiency

Vietnam has established itself as a global leader in synthetic leather coating applications, particularly within the footwear industry. Significant foreign direct investment (FDI) from South Korean and Taiwanese firms is driving the establishment of automated coating agent mixing and application facilities.

The market is evolving toward advanced technologies. Trends highlighted at IFLE-Vietnam 2026 include 3D-printable coating agents and solvent-free finishing chemicals, reflecting a shift toward high-value innovation. The integration of robotic spray coating systems is increasing demand for low-viscosity, high-consistency coating agents, improving efficiency and product quality. Additionally, trade agreements such as EVFTA are pushing manufacturers to adopt EU-compliant non-toxic coatings, while biomass-powered curing systems are reducing carbon emissions. These developments position Vietnam as a critical hub in the global synthetic leather supply chain.

Brazil Coating Agents for Synthetic Leather Market: Biofuel Resistance and Agribusiness Applications Driving Growth

Brazil’s market is uniquely shaped by its agribusiness and energy sectors. The “Fuel of the Future” law is driving demand for biofuel-resistant coating agents, particularly for protective gear used in fuel handling and storage.

Agricultural expansion is also a key driver, increasing demand for UV-stabilized and chemical-resistant coatings for protective clothing and storage materials. Government-backed initiatives under the National Circular Economy Strategy ($9 billion allocation) are promoting the use of bio-attributed PU coatings on recycled polyester substrates. Additionally, growth in offshore oil exploration is boosting demand for saltwater-resistant coating agents for maritime applications. The rise of plant-based coatings derived from soybean and castor oil is further strengthening Brazil’s position in sustainable synthetic leather coatings.

Coating Agents for Synthetic Leather Market Report Scope

Coating Agents for Synthetic Leather Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$89.6 Billion

|

|

Market Size (2032)

|

$151.6 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Resin (Polyurethane (PU), Polyvinyl Chloride (PVC), Acrylic Resins, Silicone Coatings, Rubber and Specialty Elastomers), By Technology (Water-borne (PUDs), Solvent-borne, Solvent-free, UV-Cured and Radiation Curable, Powder Coatings), By Functional Category (Base-Coat Agents, Top-Coat Agents, Cross-linking Agents, Bio-based Coating Agents), By End-Use Industry (Automotive, Footwear, Furniture and Domestic Upholstery, Textile and Fashion, Electronics and Accessories)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Stahl Holdings B.V., BASF SE, Covestro AG, LANXESS AG, Evonik Industries AG, The Dow Chemical Company, Wacker Chemie AG, Huntsman Corporation, Shin-Etsu Chemical Co., Ltd., Elkem ASA, Lubrizol Corporation, DIC Corporation, CHT Group, Arkema S.A., Zschimmer & Schwarz

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coating Agents for Synthetic Leather Market Segmentation

By Resin

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylic Resins

- Silicone Coatings

- Rubber and Specialty Elastomers

By Technology

- Water-borne (PUDs)

- Solvent-borne

- Solvent-free

- UV-Cured and Radiation Curable

- Powder Coatings

By Functional Category

- Base-Coat Agents

- Top-Coat Agents

- Cross-linking Agents

- Bio-based Coating Agents

By End-Use Industry

- Automotive

- Footwear

- Furniture and Domestic Upholstery

- Textile and Fashion

- Electronics and Accessories

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Coating Agents for Synthetic Leather Market

- Stahl Holdings B.V.

- BASF SE

- Covestro AG

- LANXESS AG

- Evonik Industries AG

- The Dow Chemical Company

- Wacker Chemie AG

- Huntsman Corporation

- Shin-Etsu Chemical Co., Ltd.

- Elkem ASA

- Lubrizol Corporation

- DIC Corporation

- CHT Group

- Arkema S.A.

- Zschimmer & Schwarz

*- List not Exhaustive