Coating Solvent Market Size, Feedstock Volatility, and Transition Toward Sustainable Solvent Systems

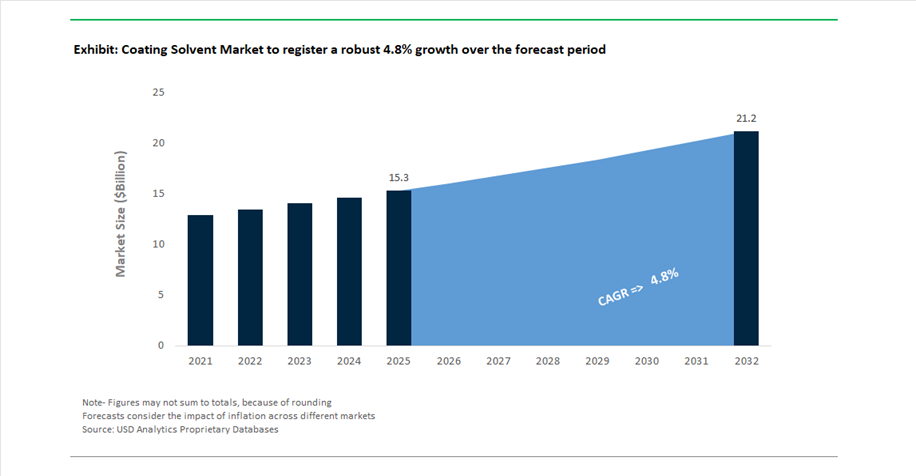

The global coating solvent market was valued at $15.3 billion in 2025 and is projected to grow at a CAGR of 4.8% between 2025 and 2032, reaching $21.2 billion by 2032. This growth is supported by steady demand from paints and coatings, adhesives, automotive refinishing, construction, and industrial manufacturing sectors, where solvents play a critical role in viscosity control, film formation, drying performance, and application efficiency.

The market is currently undergoing a structural shift driven by raw material cost volatility, environmental regulations, and evolving end-user requirements. Conventional solvent systems such as alcohols, esters, ketones, and acetyl intermediates remain dominant; however, increasing regulatory pressure on volatile organic compounds (VOCs) is accelerating the transition toward low-VOC, bio-based, and sustainable solvent alternatives. This shift is particularly pronounced in developed markets, where compliance with stringent environmental standards is reshaping formulation strategies across coatings manufacturers.

Feedstock dynamics are playing a crucial role in shaping pricing and supply patterns. Coating solvents are heavily dependent on petrochemical derivatives, making them sensitive to fluctuations in crude oil prices, energy costs, and supply chain disruptions. As a result, manufacturers are focusing on process optimization, cost control, and diversification of raw material sources, including the integration of recycled and renewable feedstocks.

In parallel, the rise of high-performance coatings and specialty applications is driving demand for tailored solvent systems that offer improved solvency power, evaporation rates, and compatibility with advanced resin chemistries. This is particularly relevant in automotive coatings, industrial maintenance, and high-end architectural applications, where performance consistency and environmental compliance are critical.

Industry Restructuring, Pricing Pressures, and Sustainable Solvent Innovation Defining Market Dynamics

The coating solvent market is witnessing significant transformation through portfolio restructuring, pricing adjustments, and sustainability-focused innovation. A major structural shift is underway with BASF’s agreement (October 2025) to spin off its coatings business into a standalone entity, in partnership with Carlyle and the Qatar Investment Authority, with completion expected in Q2 2026. The appointment of Jens Luehring as CEO in March 2026 signals a strategic refocus on specialized coatings and solvent systems, reshaping supply dynamics for one of the largest consumers of coating solvents globally.

Pricing pressures remain a defining feature of the market. In February 2025, Dow Chemical implemented price increases across its oxygenated solvent portfolio, impacting key products such as propanol, n-butyl acetate, and isopropyl acetate, citing rising raw material costs. Similarly, OQ Chemicals announced parallel price adjustments, reflecting broader industry efforts to maintain margins amid energy price volatility and logistical constraints, particularly in European markets.

Supply chain optimization and regional production shifts are also evident. Celanese Corporation idled its Frankfurt VAM facility in 2025 and is prioritizing production along the U.S. Gulf Coast, leveraging cost advantages to mitigate weak European demand. Meanwhile, Shell’s strategic review of its chemicals division (February 2026) indicates a potential retreat from low-margin segments, while retaining high-value solvent and detergent alcohol businesses, highlighting a broader industry trend toward portfolio rationalization and profitability optimization.

Sustainability and circularity are becoming central to long-term competitiveness. Celanese’s Eco-CC solvent line (February 2026) utilizes bio-based and mass-balance feedstocks, offering lower-carbon alternatives for coatings and adhesives manufacturers. Similarly, Solvay’s transformation strategy includes a 29% reduction in Scope 1 and 2 emissions, alongside a pivot toward greener solvent production technologies. Eastman’s Kingsport methanolysis facility, which achieved 2.5x growth in recycled content output in 2025, represents a critical advancement in chemical recycling for solvent production, enabling the development of circular solvent systems.

Operational efficiency and cost optimization remain key strategic priorities. LyondellBasell’s $1.3 billion cash improvement target by 2026 and ExxonMobil’s $15.1 billion structural cost savings since 2019 underscore the industry’s focus on maintaining profitability amid fluctuating demand and margin pressures. These initiatives are complemented by investments in advanced refining and feedstock upgrading technologies, ensuring a stable supply of high-quality intermediates for solvent manufacturing.

EU REACH and US TSCA Enforcement on NMP Driving Industry-Wide Solvent Substitution

The coating solvent industry is undergoing a structural transition as regulatory enforcement intensifies around N-Methyl-2-Pyrrolidone (NMP), a widely used high-performance solvent in coatings and electronics applications. With the closure of final derogation windows in the European Union by May 2024 and full enforcement realized in 2026, NMP is now effectively restricted across most industrial use cases under REACH. Parallel regulatory developments in the United States under the Toxic Substances Control Act are further reinforcing this shift.

The compliance framework is highly stringent. Under REACH, industrial users must adhere to Derived No Effect Levels of 14.4 mg/m³ for inhalation and 4.8 mg/kg/day for dermal exposure, effectively mandating closed-loop processing systems for any residual usage. In the U.S., the EPA’s upcoming Section 6 risk management rule is expected to significantly restrict or eliminate NMP in consumer-facing and certain industrial solvent applications, impacting over 12,000 regulated facilities.

This regulatory pressure has accelerated substitution at scale. By 2026, approximately 85% of premium wire coating manufacturers in Europe have transitioned away from NMP, adopting alternatives such as Dimethyl Sulfoxide and advanced water-reducible resin systems. However, compliance costs remain a concern, with facilities maintaining NMP usage reporting a 15% to 20% increase in operational overhead due to monitoring, containment, and safety infrastructure requirements.

This global regulatory convergence is driving a fundamental shift toward safer, low-toxicity solvent systems, positioning NMP-free formulations as the emerging industry standard.

China’s GB 30981.2-2025 Enforcing Ultra-Low VOC and Aromatic Content Limits

China’s implementation of GB 30981.2-2025 marks a significant escalation in environmental regulation within the coating solvent sector. Effective June 1, 2026, this standard introduces the most stringent VOC and hazardous substance limits in the country’s industrial coatings history, reshaping solvent formulation strategies across domestic and export-oriented manufacturers.

The regulation mandates VOC ceilings below 200 g/L for industrial coating systems, effectively forcing a transition toward waterborne and high-solids formulations. Additionally, the standard imposes strict limits on aromatic hydrocarbon content, capping total benzene, toluene, ethylbenzene, and xylene (BTEX) concentrations at ≤ 0.1%. This requirement is eliminating a wide range of conventional hydrocarbon solvent blends from the Chinese market.

Compliance enforcement is rigorous. Following the June 2026 deadline, coating solvents lacking documented certification are being excluded from high-volume industries such as automotive manufacturing and consumer electronics assembly. This is creating a strong incentive for manufacturers to invest in compliant solvent systems and obtain environmental labeling certifications.

The regulatory shift is also driving innovation. Over 30% of China-based solvent suppliers have redirected research and development efforts toward water-reducible coalescents and green-certified additives, reflecting a broader industry transition toward sustainable solvent technologies.

Bio-Based Solvents Emerging as Key Enablers of Low-Carbon Coating Formulations

The push for sustainable construction and green building certifications such as LEED v5 is creating a strong growth trajectory for bio-based coating solvents. Derived from renewable feedstocks including corn, citrus, and soy, these solvents are increasingly replacing traditional petroleum-based aromatics and ketones in architectural and industrial coatings.

Environmental performance is a primary advantage. Bio-based solvents such as ethyl lactate demonstrate Global Warming Potential reductions of 40% to 60% compared to conventional solvents like MEK or MIBK. Additionally, these materials are typically classified as Hazardous Air Pollutant-free, allowing manufacturers to avoid the regulatory burden associated with Title V air permits.

Market adoption is accelerating. In 2026, demand for bio-based solvents is rising sharply in zero-VOC and low-VOC coating systems, particularly in interior architectural applications where indoor air quality standards are becoming more stringent. Technological advancements have also improved performance parity. Modern lactate ester blends now achieve Hansen Solubility Parameter profiles that enable direct substitution for traditional solvents in alkyd and epoxy systems without compromising drying time or finish quality.

High-Purity DMSO Unlocking New Opportunities in Lithium-Ion Battery Manufacturing

The rapid expansion of the electric vehicle ecosystem is creating a specialized, high-value opportunity for advanced coating solvents in lithium-ion battery production. As manufacturers move away from NMP in electrode processing, high-purity Dimethyl Sulfoxide is emerging as a preferred alternative for dissolving PVDF binders in cathode slurry formulations.

Performance requirements in this segment are exceptionally stringent. Battery-grade DMSO must achieve purity levels of at least 99.99%, with metal ion contamination maintained at sub-part-per-billion levels to ensure battery stability and long-term cycle performance. These specifications place DMSO among the highest-value solvents in the industry.

Operational benefits further support adoption. Compared to NMP, DMSO offers a lower toxicity profile and more manageable vapor handling requirements, enabling gigafactories to reduce the complexity and cost of solvent recovery systems. This contributes to improved process efficiency and lower environmental impact.

The economic implications are significant. Electronics-grade DMSO commands a price premium of five to eight times that of industrial-grade solvent, reflecting the complexity of purification processes and the critical role it plays in high-performance battery manufacturing. In response to growing demand, major chemical producers are investing in dedicated purification capacity across North America and Europe to support a rapidly expanding market expected to exceed $600 million by late 2026.

Architectural Coatings Drive 36% of Coating Solvent Market with Massive Global Paint Consumption

Application Area Analysis: Coalescing Solvents Power Waterborne Paint Performance at Scale

Architectural coatings account for a dominant 36.0% share of the coating solvent market in 2025, driven by the sheer global volume of decorative paints used across residential and commercial construction. Despite the shift toward waterborne acrylic and latex paints, solvents remain essential in the form of coalescing agents (3–8% formulation content) such as Texanol, glycol ethers, and low-VOC alternatives like Dowanol and Optifilm enhancers. These solvents enable proper film formation, adhesion, and durability, preventing defects such as powdery or weak coatings. The segment reflects a unique “low VOC per liter but high total volume” paradox, as architectural coatings consume massive solvent volumes due to global production exceeding 40 billion liters annually. Additionally, ongoing regulatory pressures from EPA AIM rules, SCAQMD standards, and EU directives are accelerating innovation in bio-based and zero-VOC coalescents, reinforcing architectural coatings as the largest contributor to the global coating solvents market.

Solvent-Borne Systems Dominate with 54% Share Driven by Industrial Performance and Harsh Environment Applications

Technology Compatibility Analysis: High-Solids Solvent Systems Lead in Marine, Automotive, and Industrial Coatings

Solvent-borne systems hold a leading 54.0% share of the coating solvent market in 2025, underscoring their continued importance in high-performance industrial coatings applications. These systems remain indispensable in sectors such as marine and offshore coatings, automotive OEM and refinish coatings, packaging, and heavy-duty infrastructure, where coatings must perform under extreme conditions including low temperatures, high humidity, and aggressive chemical exposure. Modern solvent-borne coatings are primarily high-solids (60–85%) or ultra-high-solids formulations, significantly reducing VOC emissions while maintaining application advantages such as fast drying, superior flow, and strong adhesion. Technologies including reactive diluents and exempt solvents like acetone and PCBTF further enhance compliance with environmental regulations. Their ability to deliver consistent coating performance, rapid curing, and durability in demanding environments ensures solvent-borne systems remain dominant in the global industrial coatings solvent market.

Coating Solvent Market Competitive Landscape Driven by Oxygenated Solvents, Low-VOC Systems, and Sustainable Feedstocks

The coating solvent market is moderately consolidated, driven by oxygenated solvents, glycol ethers, and low-odor hydrocarbon solvents. Key players are focusing on low-VOC solvent systems, renewable feedstocks, and carbon footprint reduction to meet stringent environmental regulations across architectural, automotive, and industrial coatings applications.

BASF leads coating solvent innovation with Verbund integration and oxygenated solvent portfolio

BASF SE dominates the coating solvent market through its Industrial Solutions segment, supported by €59.7 billion in 2025 sales. The company has sharpened its focus on high-margin solvents following the divestment of its decorative paints business. Its leadership in oxygenated solvents such as n-butanol, isobutanol, and butyl acetate supports advanced coating formulations. Verbund integration enables a 29% reduction in Scope 1 and 2 emissions, improving sustainability across production. Increased R&D investment drives development of next-generation solvent systems for advanced pigments and coatings. Product strategy focuses on green solvents, integration efficiency, and high-performance formulations.

Dow strengthens solvent market position with glycol ethers and carbon footprint tracking innovation

Dow Inc. is a major player in coating solvents, supported by $40 billion in net sales and a strong Performance Materials segment. Its DOWANOL glycol ethers and UCAR ester solvents are widely used for controlled evaporation and high resin compatibility. The company is executing cost optimization strategies while maintaining product innovation. Its Carbon Footprint Ledger enables real-time tracking of emissions, supporting ESG compliance for customers. Streamlined asset operations improve efficiency amid global market challenges. Product development focuses on sustainable solvents, process optimization, and digital transparency.

Eastman advances specialty solvent leadership with circular economy integration and high-clarity solutions

Eastman Chemical Company is a leader in specialty coating solvents, particularly esters and ketones for high-performance applications. The company generated strong cash flow in 2025 while maintaining pricing power in specialty solvents. Its methanolysis technology supports circular economy goals by increasing recycled content in solvent production. Eastman’s solvents are critical for high-clarity finishes in electronics and aerospace coatings. Cost-reduction initiatives enhance competitiveness against global suppliers. Product innovation focuses on sustainable solvents, high-purity formulations, and specialty applications.

Shell Chemicals drives growth with GTL solvents and low-odor hydrocarbon solutions

Shell Chemicals is a key supplier in the coating solvent market, focusing on gas-to-liquids (GTL) solvent technology. GTL solvents offer high purity, low odor, and zero sulfur content, making them ideal for indoor coatings and sensitive applications. The ShellSol product line enables compliance with stringent European environmental standards. Expansion into infrastructure-driven markets supports demand for heavy-duty coating solvents. The company leverages global energy integration to maintain supply reliability. Product strategy focuses on low-odor solvents, regulatory compliance, and infrastructure applications.

Solvay accelerates sustainable solvent innovation with renewable oxygenated solvents and cost optimization

Solvay is a leader in sustainable coating solvents, particularly oxygenated solvents derived from renewable sources. The company achieved a 29% reduction in CO2 emissions ahead of its 2030 targets, strengthening its ESG positioning. Its Coatis business unit focuses on eco-friendly solvents for architectural coatings in Europe and Latin America. Cost optimization initiatives aim to improve profitability amid market contraction. Strong EBITDA margins highlight operational resilience. Product development focuses on renewable solvents, sustainability, and regional market expansion.

ExxonMobil drives solvent market with low-odor hydrocarbons and feedstock integration advantages

ExxonMobil Chemical plays a significant role in the coating solvent market through its hydrocarbon solvent portfolio. Its Isopar and Exxsol products are widely used in low-odor coating formulations. The company is shifting toward specialty chemicals to capture higher margins in a competitive market. Expansion of upstream petrochemical capacity supports cost-efficient solvent production. Operational efficiency improvements enhance profitability during industry downturns. Product strategy focuses on hydrocarbon solvents, feedstock integration, and performance-driven formulations.

China Coating Solvent Market: VOC Control Overhaul and High-Purity Innovation Driving Transformation

China’s coating solvent market is undergoing a major structural shift toward high-purity and low-emission formulations, driven by stringent environmental and safety regulations. The implementation of GB 4806.10-2025 (effective September 2026) has expanded permitted materials for food-contact coatings, requiring ultra-clean solvents with undetectable primary aromatic amines (PAAs).

At the same time, the Ministry of Ecology and Environment is enforcing a comprehensive VOC reduction strategy, accelerating the transition toward zero-VOC and waterborne alternatives, especially in industrial clusters like the Pearl River Delta. Growth in EV battery production is driving a 35% expansion in high-purity NMP capacity, while semiconductor demand is pushing development of ultra-low-metal solvents (<10 ppt impurities). Additionally, new circular economy regulations mandate 65% solvent recovery by 2027, reinforcing China’s leadership in sustainable and high-tech solvent systems.

United States Coating Solvent Market: Functional Coating Demand and Bio-Based Solvent Scaling Driving Growth

The United States market is evolving toward high-performance and environmentally compliant solvent systems, supported by federal investments and regulatory pressure. The CHIPS Act is driving strong demand for electronics-grade solvents used in semiconductor fabrication and cleanroom environments.

Infrastructure projects under the IIJA are boosting consumption of HTHP-stable solvent blends for corrosion-resistant coatings. Regulatory actions under TSCA Section 6 are phasing out hazardous solvents like methylene chloride, leading to a 22% increase in oxygenated solvent adoption. Innovation is also focused on sustainability, with companies scaling bio-based solvents such as lactate esters and glycerol derivatives for eco-labeled coatings. Additionally, the shift toward lightweight automotive materials is increasing demand for non-aggressive solvents compatible with composites, reinforcing the U.S. position in advanced solvent technologies.

Germany Coating Solvent Market: Green Chemistry and REACH 2.0 Compliance Driving Innovation

Germany remains the global benchmark for sustainable solvent innovation, driven by strict regulatory frameworks and advanced material science. The transition toward PFAS-free and isocyanate-free solvent systems is accelerating under REACH 2.0 compliance requirements.

A key breakthrough is the commercialization of lignin-based bio-circular solvents, providing renewable alternatives to petrochemical-derived aromatics. Germany is also pioneering Digital Product Passports (DPP) for solvents, enabling full traceability of carbon intensity and chemical composition. Growth in hydrogen infrastructure is driving demand for chemically inert solvent systems, while the MedTech sector is increasing adoption of zero-residue specialty solvents for implant coatings. Additionally, the integration of electric IR-curing systems is reducing energy consumption by 20%, influencing solvent evaporation dynamics and formulation strategies.

India Coating Solvent Market: Petrochemical Expansion and Bio-Refinery Growth Driving Demand

India is rapidly transitioning into a specialty solvent production hub, supported by large-scale infrastructure and petrochemical investments. The commissioning of the Paradip PX/PTA plant (2025) is strengthening domestic feedstock supply, reducing import dependency by 15%.

Bio-based solvent innovation is a major growth driver, with companies expanding sugarcane-derived ethanol and acetate production, targeting a 65.7% share of bio-based solvents in decorative coatings. Infrastructure projects under the PM Gati Shakti plan are boosting demand for industrial solvents in protective coatings, while the automotive refinish sector is driving consumption of fast-evaporating hydrocarbon blends. Additionally, new VOC regulations are accelerating the shift toward high-solid solvent systems, positioning India as a high-growth market for sustainable and performance-driven solvents.

Japan Coating Solvent Market: Semiconductor Precision and Nanotechnology Driving Advanced Applications

Japan’s coating solvent market is defined by extreme precision and high-purity requirements, particularly in semiconductor and automotive applications. The development of ultra-high-purity PGMEA (<1 ppb impurities) is critical for next-generation 2nm chip manufacturing.

Innovation is also expanding into EV and advanced coatings. Solvents capable of supporting thermally conductive coatings for battery systems are gaining traction, while hydrophobic nanocoating solvents are enhancing durability in public infrastructure. Japan is also advancing supercritical CO₂ solvent technologies for extracting high-purity resins used in aerospace coatings. Automated, IoT-enabled blending systems are further optimizing solvent performance in real-time, reinforcing Japan’s leadership in high-tech solvent innovation.

Brazil Coating Solvent Market: Biofuel Integration and Industrial Growth Driving Regional Expansion

Brazil is leveraging its renewable energy leadership to expand its bio-based coating solvent market. The “Fuel of the Future” law is driving demand for biofuel-resistant solvents used in coatings for ethanol storage and transportation infrastructure.

Agricultural growth is also a key driver, increasing demand for solvent-based coatings for seed protection and agrochemicals. Industrial coatings are projected to reach $2.96 billion by 2033, supported by acrylic and epoxy solvent demand. Investments in green energy and industrial modernization are accelerating adoption of low-carbon solvent systems, while offshore oil exploration is driving demand for high-performance aromatic solvents for subsea coatings. These factors position Brazil as a major regional player.

South Korea Coating Solvent Market: Semiconductor and Display Innovation Driving High-Purity Demand

South Korea’s coating solvent market is driven by its global leadership in semiconductors, displays, and EV manufacturing. The expansion of semiconductor equipment investment—projected at $29.2 billion by 2026—is fueling demand for ultra-clean electronic-grade solvents.

The market is also shaped by advanced applications. The production of flexible OLED displays requires solvents compatible with delicate polymer substrates, while EV manufacturing is increasing demand for precision solvents with tightly controlled evaporation rates. Additionally, innovations in EUV lithography maintenance solvents and automated spray systems are enhancing efficiency and quality in high-tech manufacturing. These developments position South Korea as a leader in high-performance coating solvent technologies.

Coating Solvent Market Report Scope

Coating Solvent Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.3 Billion

|

|

Market Size (2032)

|

$21.2 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Chemistry (Oxygenated Solvents, Alcohols, Ketones, Esters, Glycols and Glycol Ethers, Hydrocarbon Solvents, Aliphatic Solvents, Aromatic Solvents, Specialty Solvents, Bio-based Solvents), By Source of Feedstock (Petroleum-Derived, Bio-derived, Recycled Solvents, Fast and Slow-Evaporating Grades), By Application Area (Architectural Coatings, Automotive OEM and Refinish, General Industrial, Marine and Aerospace, Packaging and Printing Inks), By Technology Compatibility (Solvent-borne Systems, Water-borne Co-solvents, Reactive and UV-curable Systems)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, The Dow Chemical Company, Exxon Mobil Corporation, Shell plc, Eastman Chemical Company, LyondellBasell Industries Holdings B.V., INEOS Group, SABIC, Chevron Phillips Chemical Company, Honeywell International Inc., Arkema S.A., Celanese Corporation, Solvay S.A., Mitsubishi Chemical Group Corporation, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coating Solvent Market Segmentation

By Product Chemistry

- Oxygenated Solvents

- Alcohols

- Ketones

- Esters

- Glycols and Glycol Ethers

- Hydrocarbon Solvents

- Aliphatic Solvents

- Aromatic Solvents

- Specialty Solvents

- Bio-based Solvents

By Source of Feedstock

- Petroleum-Derived

- Bio-derived

- Recycled Solvents

- Fast and Slow-Evaporating Grades

By Application Area

- Architectural Coatings

- Automotive OEM and Refinish

- General Industrial

- Marine and Aerospace

- Packaging and Printing Inks

By Technology Compatibility

- Solvent-borne Systems

- Water-borne Co-solvents

- Reactive and UV-curable Systems

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Coating Solvent Market

- BASF SE

- The Dow Chemical Company

- Exxon Mobil Corporation

- Shell plc

- Eastman Chemical Company

- LyondellBasell Industries Holdings B.V.

- INEOS Group

- SABIC (Saudi Basic Industries Corporation)

- Chevron Phillips Chemical Company

- Honeywell International Inc.

- Arkema S.A.

- Celanese Corporation

- Solvay S.A.

- Mitsubishi Chemical Group Corporation

- Huntsman Corporation

*- List not Exhaustive