Global Coatings Market Size, Industrial Demand Stability, and Technology-Driven Formulation Evolution

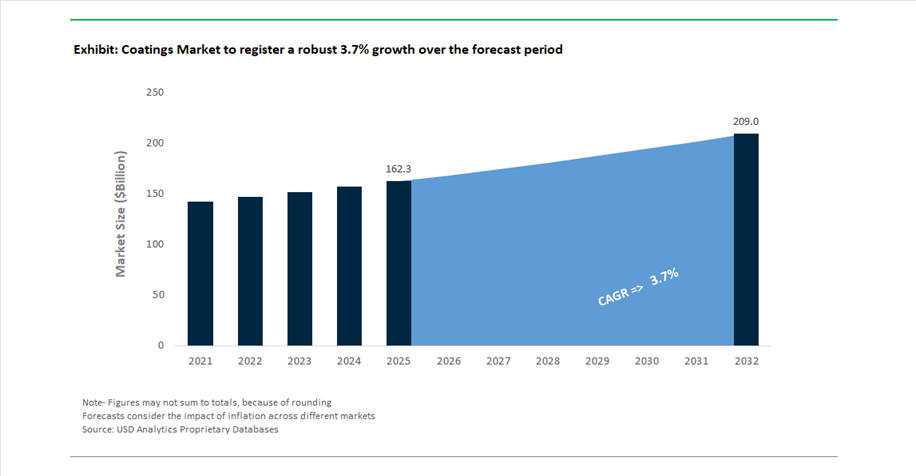

The global coatings market was valued at $162.3 billion in 2025 and is projected to grow at a CAGR of 3.7% between 2025 and 2032, reaching $209.3 billion by 2032. This moderate yet stable growth trajectory reflects the market’s maturity, underpinned by consistent demand across architectural coatings, automotive OEM and refinish, industrial coatings, marine, aerospace, and packaging applications.

Coatings remain a critical component in modern industrial ecosystems, providing surface protection, corrosion resistance, chemical stability, and enhanced aesthetics. The market is currently transitioning toward high-performance, sustainable, and digitally optimized coating systems, driven by tightening environmental regulations and evolving end-user expectations. The shift toward low-VOC, waterborne, powder coatings, and bio-based formulations is accelerating, particularly in developed markets, where compliance with environmental standards is a key differentiator.

A notable transformation is occurring in automotive and industrial coatings, where the integration of advanced resins, nanotechnology, and AI-assisted formulation tools is enabling faster development cycles and improved coating performance. The growing adoption of electric vehicles (EVs) is further influencing coating requirements, demanding lightweight, thermally stable, and high-durability finishes that support next-generation mobility platforms.

In parallel, emerging economies in Asia-Pacific and Latin America are driving volume growth through urbanization, infrastructure development, and rising consumer spending. Investments in local manufacturing capacity, supply chain optimization, and product customization are enabling global players to strengthen their regional footprints and cater to diverse application requirements.

Mega Acquisitions, AI-Driven Coating Innovation, and Regional Expansion Strategies Reshaping Industry Dynamics

The coatings market is undergoing significant transformation through large-scale acquisitions, digital innovation, and strategic regional expansion. One of the most impactful developments is BASF’s agreement (October 2025) to sell its coatings business to Carlyle and the Qatar Investment Authority for €7.7 billion, with closing expected in Q2 2026. The formation of a standalone coatings entity under the leadership of Jens Luehring (announced March 2026) represents a major structural shift, enabling sharper strategic focus on automotive and industrial coatings segments.

Strategic consolidation is further evident in Henkel’s February 2026 agreement to acquire Stahl, strengthening its position in specialty coatings for flexible substrates, particularly in automotive interiors and industrial packaging. Similarly, Kansai Nerolac’s amalgamation with Nerofix (February 2026) reflects consolidation within the Indian coatings market, aimed at improving operational efficiency and leveraging global R&D capabilities to address increasing competition.

Regional expansion remains a key growth lever. Sherwin-Williams’ integration of the Suvinil brand (completed in late 2025) significantly enhances its presence in South America’s architectural coatings segment, contributing $164.5 million in Q4 2025 net sales. Meanwhile, Nippon Paint’s expansion of its Design-to-Factory (D2F) system in China (February 2026) is transforming supply chain responsiveness, with 70% of orders in Shanghai now processed through D2F, reducing lead times and improving customer service efficiency.

Technological innovation is increasingly centered on digitalization and sustainability. In February 2026, PPG Industries launched its AI-designed DELTRON® NXT Premium Glamour Speed Clearcoat, demonstrating how artificial intelligence can optimize formulation processes and enhance productivity in automotive refinish applications. Additionally, Axalta’s multi-year partnership with BMW Group (operational through 2026) integrates its Fast Cure Low Energy (FCLE) systems, enabling significant reductions in energy consumption and CO₂ emissions during coating processes.

Product innovation is also influencing market differentiation. Axalta’s introduction of “Solar Boost” as its 2026 Automotive Color of the Year (October 2025) highlights the growing importance of advanced layering and high-clarity clearcoat technologies to achieve complex, dynamic finishes for EV platforms.

EPA TSCA PFAS Reporting Rule Creating Unprecedented Data Transparency and Liability Exposure

The global coatings industry is entering a new compliance era as the U.S. Environmental Protection Agency enforces the TSCA Section 8(a)(7) PFAS reporting mandate. This regulation introduces a comprehensive “look-back” requirement, compelling manufacturers and importers to disclose detailed data on PFAS substances used since 2011. The scope extends beyond fluoropolymer resins to include surfactants, dispersants, and leveling agents embedded across coating formulations.

The regulatory breadth is substantial. The rule covers at least 1,462 PFAS compounds, requiring disclosure of production volumes, chemical identities, byproducts, and disposal practices over a 15-year period. The reporting window, opening in late 2026 with deadlines extending into early 2027, is forcing companies to undertake extensive historical audits of their chemical usage.

The removal of de minimis exemptions—particularly for imported articles—represents a critical escalation. Small and mid-sized coating importers are expected to face a compliance burden increase exceeding 40%, as even trace PFAS content must now be reported. This is driving a significant reallocation of resources, with companies dedicating approximately 15% of their compliance budgets to retroactive chemical traceability and documentation.

From a strategic perspective, this mandate is accelerating the transition toward PFAS-free formulations. The risk of penalties associated with inaccurate reporting, combined with increasing customer demand for transparency, is pushing manufacturers to eliminate fluorinated chemistries wherever feasible. This regulatory shift is transforming PFAS from a performance enabler into a liability factor, fundamentally reshaping formulation strategies across the coatings industry.

EU Industrial Emissions Directive Revision Forcing Structural Shift to Low-VOC Technologies

In Europe, the revised Industrial Emissions Directive (Directive 2024/1785) is driving a parallel transformation, focusing on reducing industrial emissions and enforcing stricter environmental performance standards for coating operations. With a transposition deadline of July 1, 2026, this directive is introducing binding requirements that significantly tighten allowable emission ranges.

A key development is the shift from indicative to mandatory Best Available Techniques emission limits. Coating manufacturers must now operate at the lower end of these limits, effectively mandating the adoption of waterborne, powder, or high-solids coating systems. This is eliminating flexibility in compliance strategies and accelerating capital investment in new production technologies.

The directive also introduces mandatory Environmental Management Systems for all large-scale coating installations. By 2030, facilities must implement certified systems such as ISO 14001 or EMAS, supported by detailed transformation plans outlining pathways to climate neutrality by 2050. This requirement is embedding sustainability into core operational frameworks rather than treating it as an optional initiative.

Digital transparency is another critical component. Under the Industrial Emissions Portal Regulation, facilities must report emissions data electronically, enabling near real-time public access to VOC and hazardous air pollutant data. This level of visibility is increasing reputational risk and incentivizing proactive emission reduction strategies.

Polysiloxane Coatings Advancing Infrastructure Durability and Lifecycle Efficiency

The global focus on infrastructure resilience is creating a strong growth opportunity for polysiloxane coatings, particularly in applications such as bridges, offshore structures, and marine assets. These hybrid inorganic-organic systems are increasingly replacing traditional three-coat polyurethane systems due to their superior durability and application efficiency.

Operational efficiency gains are significant. Polysiloxane-epoxy systems can be applied as a two-coat system, eliminating the need for a separate polyurethane topcoat. This reduces application labor costs by approximately 30% while simplifying project timelines. In addition, these coatings demonstrate exceptional weathering performance, retaining more than 90% of their initial gloss after 2,000 hours of accelerated UV exposure, compared to 60% to 70% for conventional polyurethane systems.

Environmental compliance further enhances their value. With VOC levels typically below 100 g/L, polysiloxane coatings meet stringent regulatory requirements in regions such as California and the European Union. This “future-proof” characteristic makes them particularly attractive for long-term infrastructure projects subject to evolving environmental standards.

Durability improvements are equally compelling. Polysiloxane coatings offer approximately 20% greater resistance to acid rain and industrial pollutants, extending maintenance intervals and reducing lifecycle costs. As governments and private investors prioritize asset longevity, these coatings are emerging as a preferred solution for high-value infrastructure protection.

Intumescent Coatings Unlocking Fire-Safe Expansion of Mass Timber Construction

The rapid adoption of mass timber construction, particularly cross-laminated timber, is creating a specialized opportunity for intumescent fire-resistive coatings. These coatings enable timber structures to meet stringent fire safety standards while preserving the natural aesthetic of wood, supporting the growing demand for sustainable and biophilic building designs.

Performance capabilities have advanced significantly. Modern thin-film intumescent coatings achieve fire resistance ratings of R60 to R90, allowing mass timber buildings to compete with steel and concrete structures in mid-rise construction. Upon exposure to heat, these coatings expand by 20 to 100 times their original thickness, forming a protective char layer that insulates the underlying wood and slows combustion.

Aesthetic considerations are also driving adoption. More than 55% of intumescent coatings for timber applications are now formulated as transparent or clear systems, enabling architects to maintain the visual appeal of exposed wood surfaces. This aligns with contemporary design trends that emphasize natural materials and occupant well-being.

Recent formulation improvements have addressed historical limitations related to moisture sensitivity. Advanced waterborne intumescent coatings now exhibit enhanced resistance to leaching in high-humidity environments, ensuring long-term performance without compromising fire protection.

Acrylic Resins Lead Global Coatings Market with 31.5% Share Driven by Versatility and Waterborne Dominance

Resin Chemistry Analysis: Acrylic Coatings Power Architectural, Automotive, and Industrial Applications

Acrylic resins command a leading 31.5% share of the global coatings market in 2025, driven by their unmatched versatility across architectural coatings, automotive finishes, and industrial applications. Waterborne acrylic emulsions dominate the segment, accounting for over 80% of architectural paints globally, offering superior UV resistance, flexibility, and durability for both interior and exterior surfaces. These coatings range from low-cost styrene acrylics used in interior wall paints to premium 100% acrylic formulations delivering 10–15 year exterior performance warranties. Beyond architectural use, acrylic coatings are widely adopted in automotive refinish systems, direct-to-metal (DTM) coatings, and coil coatings, providing excellent weatherability, corrosion resistance, and gloss retention. Additionally, the growing shift toward waterborne and bio-based acrylic monomers supports sustainability goals and VOC compliance, reinforcing acrylic’s position as the backbone of the global paints and coatings industry.

Standard Protective & Decorative Coatings Dominate with 68% Share Driven by High-Volume Paint Applications

Functional Property Analysis: Decorative Paints and Industrial Finishes Drive Market Volume

Standard protective and decorative coatings hold a dominant 68.0% share of the coatings market in 2025, representing the core function of coatings—aesthetic enhancement combined with basic protection against UV exposure, moisture, and wear. This segment includes architectural paints, automotive basecoat-clearcoat systems, industrial product finishes, and wood coatings, making it the largest contributor by both volume and value. Demand is driven by global construction activity, automotive production, and consumer goods manufacturing, with coatings formulated for cost efficiency and large-scale application. The segment is heavily reliant on waterborne acrylics, alkyds, and polyester resins, along with high-volume pigments such as titanium dioxide (TiO₂) for opacity and brightness. A key 2025 trend is premiumization, with rising demand for scrubbable matte finishes, paint-and-primer combinations, and antimicrobial coatings, enhancing durability and functionality. These factors solidify this segment as the foundation of the global decorative and protective coatings market.

Coatings Industry Competitive Landscape Driven by Advanced Materials, Sustainability, and Digital Integration

The global coatings industry is dominated by large-scale players leveraging advanced materials science, sustainability-driven formulations, and digital coating technologies. Competitive intensity is shaped by pricing strategies, innovation in automotive and aerospace coatings, and expansion into high-performance, low-VOC, and energy-efficient coating solutions.

Sherwin-Williams Strengthens Protective Coatings Leadership with Cash-Driven Expansion

The Sherwin-Williams Company maintains its position as a global coatings leader, reporting $23.57 billion in 2025 net sales with continued low-to-mid single-digit growth projected for 2026. Its Protective and Marine coatings segment delivered high-single-digit growth, supported by an extensive network of over 5,000 company-operated stores, reinforcing distribution dominance. Strong operating cash flow of $3.45 billion enabled $2.4 billion in shareholder returns while funding expansion in packaging coatings and automotive refinish solutions. The company’s introduction of self-healing clearcoats using thermal-reactive polymers enhances durability and surface performance in automotive applications. Sherwin-Williams continues to focus on high-performance industrial coatings, leveraging scale, distribution efficiency, and product innovation. Its strategy integrates financial strength with portfolio diversification across protective, marine, and refinish coatings markets.

PPG Industries Drives Growth Through Aerospace Coatings and Digital Paint Ecosystems

PPG Industries, Inc. reported a record Q1 2026 adjusted EPS of $1.83, supported by strong demand in aerospace coatings and Latin American architectural coatings. The acquisition of Ozark Materials in April 2026 strengthens its presence in pavement markings and traffic safety coatings across North America. The company implemented price increases of up to 20% to offset rising raw material and logistics costs while maintaining consistent organic sales growth. Its SOLARON BLUE PROTECTION™ clearcoat technology enhances UV resistance in aerospace transparencies without compromising optical clarity. PPG’s LINQ™ digital ecosystem optimizes paint mixing processes, reducing material waste by up to 15% and improving operational efficiency. The company’s integrated approach combines pricing discipline, digitalization, and innovation in high-performance coatings. This positions PPG as a leader in smart coatings and sustainable manufacturing solutions.

AkzoNobel Enhances Profitability Through Strategic Divestment and Performance Coatings Focus

AkzoNobel N.V. achieved €10.16 billion in 2025 revenue while increasing operating profit by 27% to €1.164 billion, driven by its price-over-volume strategy and stringent cost control measures. The divestment of its India business generated €922 million, strengthening capital allocation toward core performance coatings markets. Its Industrial Excellence Program targets €980 million in cost savings through 2026, supporting a 14.2% adjusted EBITDA margin. The proposed merger with Axalta Coating Systems aims to create a scaled technical pure-play entity in advanced coatings by late 2026. AkzoNobel’s Aerodur coating systems deliver thin-film technology that reduces aircraft weight and improves fuel efficiency, reinforcing its aerospace coatings leadership. The company continues to prioritize margin expansion, operational efficiency, and high-performance industrial coatings innovation. Its strategic transformation aligns with long-term value creation in specialty coatings markets.

Axalta Advances EV and Digital Coatings with Award-Winning EcoNextJet™ Technology

Axalta Coating Systems achieved record 2025 net sales of $5.12 billion and an industry-leading 22.0% adjusted EBITDA margin, highlighting strong operational performance. The company earned three Gold Edison Awards in 2026 for innovations including EcoNextJet™, Alesta® e-PRO FG Black, and TintMaster AI. Its EcoNextJet™ system enables digital, drop-on-demand automotive painting, eliminating masking waste and enabling mass customization for OEMs. The Alesta® e-PRO FG Black powder coating offers fire resistance up to 1200°C, addressing critical safety requirements in electric vehicle battery systems. Axalta’s TintMaster AI platform improves Right-First-Time production accuracy by up to 29%, enhancing manufacturing efficiency. Strategic collaborations with Dürr and Xaar accelerate the adoption of digital coatings technologies across automotive production lines. The company’s focus on EV coatings, AI-driven manufacturing, and sustainability strengthens its competitive positioning.

Nippon Paint Expands Specialty Coatings Portfolio with Green Transformation Focus

Nippon Paint Holdings (NIPSEA Group) continues its expansion through the $2.3 billion acquisition of AOC, strengthening its presence in specialty chemical formulations and high-margin coatings segments. The company is trending toward ¥1.6 trillion in revenue for 2026, driven by its asset assembler model and strong market share in Japan and China. Despite construction challenges in China, Nippon has shifted focus to the renovation and maintenance segment, which now contributes 70% of regional decorative coatings sales. Its development of biocide-free antimicrobial coatings addresses post-pandemic hygiene requirements in healthcare and public infrastructure. The company is advancing waterborne coatings and low-VOC technologies under its Green Transformation strategy to meet stringent environmental regulations. Nippon Paint’s geographic diversification and sustainability-driven innovation support long-term growth in decorative and industrial coatings markets. Its portfolio reflects increasing demand for eco-friendly and functional coatings solutions.

BASF Coatings Strengthens eMobility and Sustainability with Strategic Restructuring

BASF SE’s Coatings division is undergoing a strategic transformation, with plans to operate as a standalone entity following a transaction with Carlyle, positioning it for focused growth in advanced coatings markets. The inauguration of its Lean Lab in France in March 2026 enhances R&D capabilities in eMobility coatings and sustainable industrial applications. BASF’s Eco Impact Assessment tool, certified by TÜV Rheinland, enables accurate carbon footprint measurement for automotive body shops, supporting sustainability compliance. Its partnership with Volvo Car UK strengthens its automotive refinish coatings presence through premium brands Glasurit and R-M. BASF continues to lead in automotive OEM coatings, integrating materials science with aesthetic design and protective performance. The company’s focus on sustainability, digital tools, and high-performance coatings reinforces its competitive advantage in next-generation mobility solutions.

India Coatings Market: Consolidation, Policy Tailwinds, and Automotive Surge Driving High Growth

India’s coatings market is undergoing a structural transformation driven by major consolidation, fiscal stimulus, and manufacturing expansion. A defining moment was JSW Paints’ acquisition of a 60.76% stake in AkzoNobel India (2025), which reshaped the competitive landscape and elevated JSW to a leading position in industrial and decorative coatings.

Policy support is playing a major role. The GST reduction on cement and tiles (2025) has triggered a housing boom, indirectly boosting demand for architectural paints. Simultaneously, GST cuts on small automobiles have driven a surge in vehicle sales, significantly increasing demand for OEM coatings and refinish systems. Long-term partnerships—such as the extended PPG–Asian Paints joint venture (2026–2041)—are strengthening supply chains across automotive, marine, and powder coatings segments. Environmental regulations are also accelerating the transition toward waterborne coating systems, particularly in industrial clusters.

China Coatings Market: Dual Carbon Strategy and Advanced Resin Ecosystem Driving Global Scale

China remains the global leader in coatings volume while rapidly transitioning toward high-performance and low-carbon solutions. The revised GB 4806.10-2026 standard has expanded approved materials for food-contact coatings, increasing demand for high-purity, low-migration solvent systems.

The country is also strengthening its position in advanced manufacturing. Expansion of high-purity NMP capacity (+35% in 2025) supports EV battery coatings, while facilities like Allnex’s Jiaxing “Mega-Site” are producing UV-curable and waterborne resins using AI-driven systems. Growth in renewable energy is driving demand for ZM-coated steel in solar installations, and offshore wind projects are increasing the need for heavy-duty marine coatings. These developments reinforce China’s leadership in both scale and next-generation coating technologies.

United States Coatings Market: Infrastructure Modernization and Cleanroom Demand Driving High-Value Growth

The United States coatings market is evolving toward high-value, performance-driven applications, supported by federal funding and reshoring initiatives. Under the Infrastructure Investment and Jobs Act (IIJA), over $40 billion is being directed toward bridge rehabilitation, driving demand for advanced duplex coating systems on high-performance steel.

The CHIPS Act is another major growth driver, creating a “cleanroom boom” that is increasing demand for ultra-high-purity chemical-resistant coatings in semiconductor facilities. Regulatory changes under TSCA are phasing out hazardous solvents, leading to a 22% increase in oxygenated solvent adoption. Additionally, renewable energy projects are boosting use of self-cleaning hydrophobic coatings, while the aging vehicle fleet is sustaining strong demand for premium automotive refinish coatings.

Germany Coatings Market: Bio-Circular Innovation and Hydrogen Infrastructure Driving Sustainability Leadership

Germany continues to lead in sustainable coatings innovation, driven by circular economy principles and strict regulatory compliance. The commercialization of bio-circular resins is reducing CO₂ emissions by up to 50%, while proactive phase-out of PFAS is positioning German manufacturers as global leaders in toxin-free coatings.

Innovation is closely tied to energy transition initiatives. Significant R&D is focused on permeation-resistant coatings for hydrogen pipelines, supporting the national hydrogen grid. Germany is also pioneering Digital Product Passports (DPP) for coatings, ensuring full lifecycle traceability. Additionally, advancements in smart coatings with self-healing and leak-indicating properties are enhancing industrial automation, while energy-efficient curing technologies (IR and UV-LED) are reducing operational energy consumption by ~22%.

Japan Coatings Market: Nanotechnology Precision and Geriatric-Focused Innovation Driving Advanced Applications

Japan’s coatings market is defined by high-precision engineering and advanced nanotechnology, with strong focus on healthcare and electronics. The development of ultra-high-purity solvents (PGMEA <1 ppb impurities) is critical for next-generation semiconductor manufacturing.

Innovation is also expanding into healthcare and EV applications. Japan is advancing bio-cellulose coatings for aesthetic medical treatments, as well as thermally conductive coatings for EV battery systems to improve heat dissipation. Regulatory reforms under the PMDA are easing approval pathways for coated medical devices, while self-cleaning nanocoatings are being widely adopted in public infrastructure. Additionally, maritime industries are adopting non-toxic silicone-based antifouling coatings to meet international environmental standards.

Brazil Coatings Market: Biofuel Integration and Infrastructure Investments Driving Regional Growth

Brazil’s coatings market is shaped by its dual strength in agribusiness and energy sectors. The “Fuel of the Future” law (2024) is driving demand for biofuel-resistant coatings in storage tanks and pipelines, particularly with higher ethanol and biodiesel blends.

Agricultural expansion is also fueling demand, with a 15% increase in zinc-aluminum coated steel usage for grain storage and logistics. Government housing programs such as Minha Casa Minha Vida are boosting demand for waterborne architectural coatings, while infrastructure concessions worth $14 billion are driving consumption of heavy-duty protective coatings. Offshore oil exploration is further increasing demand for seawater-resistant coatings, positioning Brazil as a key regional market with strong growth potential.

Coatings Market Report Scope

Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$162.3 Billion

|

|

Market Size (2032)

|

$209.3 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Radiation Curable, High-Solids), By Resin Chemistry (Acrylic, Polyurethane (PU), Epoxy, Alkyd, Polyester, Specialty Resins), By End-Use Sector (Architectural and Decorative, Industrial and Protective, Automotive and Transportation, Specialty Sectors), By Functional Property (Standard Protective and Decorative, Smart Coatings, Thermal Management, Anti-Corrosive)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., Asian Paints Limited, Jotun A/S, Hempel A/S, Masco Corporation, Berger Paints India Limited, Sika AG, Beckers Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coatings Market Segmentation

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Radiation Curable

- High-Solids

By Resin Chemistry

- Acrylic

- Polyurethane (PU)

- Epoxy

- Alkyd

- Polyester

- Specialty Resins

By End-Use Sector

- Architectural and Decorative

- Industrial and Protective

- Automotive and Transportation

- Specialty Sectors

By Functional Property

- Standard Protective and Decorative

- Smart Coatings

- Thermal Management

- Anti-Corrosive

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- Jotun A/S

- Hempel A/S

- Masco Corporation

- Berger Paints India Limited

- Sika AG

- Beckers Group

*- List not Exhaustive