Coil Coatings Market Size, Pre-Painted Metal Demand, and Energy-Efficient Processing Technologies

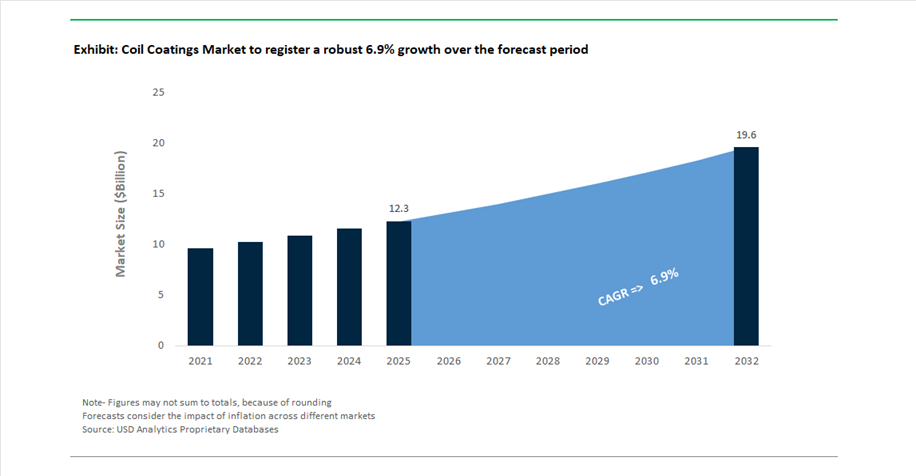

The global coil coatings market was valued at $12.3 billion in 2025 and is projected to grow at a CAGR of 6.9% between 2025 and 2032, reaching $19.6 billion by 2032. This above-average growth reflects strong demand from construction, appliances, transportation, and industrial manufacturing, where coil coatings enable high-throughput, factory-applied finishes on metal substrates such as steel and aluminum.

Coil coatings are integral to pre-painted metal applications, offering advantages such as uniform coating thickness, superior adhesion, corrosion resistance, and enhanced aesthetic consistency. The market is benefiting significantly from rising adoption of metal roofing, wall cladding, and façade systems, particularly in urbanizing regions where durability, low maintenance, and energy efficiency are critical. Additionally, the increasing use of coated metals in white goods and HVAC systems is reinforcing demand for high-performance, scratch-resistant, and chemically stable coatings.

A key transformation underway is the shift toward sustainable and energy-efficient coating processes, particularly in curing technologies. Traditional gas-fired curing systems are being replaced or supplemented by electrified, induction-based, and renewable energy-driven curing solutions, reducing carbon emissions and operational costs. Simultaneously, advancements in resin chemistry, pigments, and additives are enabling coatings with improved solar reflectance, UV stability, and long-term weatherability, supporting green building initiatives and regulatory compliance.

Capacity Expansion, Renewable Curing Technologies, and Bio-Based Resin Innovation Driving Market Evolution

The coil coatings market is undergoing rapid evolution, characterized by capacity expansion, sustainability-focused innovation, and strategic investments in advanced materials and processing technologies. A major development occurred in March 2026, when Sherwin-Williams completed a 60% capacity expansion at its Bowling Green, Kentucky facility, incorporating advanced automation and modern manufacturing systems. This expansion is designed to address rising demand from metal roofing, siding, and OEM manufacturing sectors, while improving lead times and production scalability.

Sustainability-driven process innovation is gaining strong momentum. AkzoNobel’s launch of the IONOMY™ ecosystem (October 2025) represents a significant step toward decarbonizing coil coating operations, enabling manufacturers to transition from gas-fired curing to renewable energy-based and induction curing technologies. By March 2026, the initiative had gained traction through partnerships with equipment providers, highlighting the industry's commitment to reducing energy intensity and carbon footprint in coating lines.

Material innovation is also advancing through strategic collaborations. Beckers Group’s partnership with Anodyne Chemistries (June 2025) focuses on developing bio-based resins and additives using enzymatic processes, directly addressing the need for fossil-free raw materials in coil coatings. Complementing this, Beckers’ new R&D center in Shanghai (October 2025) enhances localized innovation capabilities, enabling the development of region-specific, high-performance coating solutions for Asia’s construction and appliance markets.

Product innovation and design trends are influencing market differentiation. PPG’s Color Now 2026 launch (January 2026) emphasizes architectural metal coatings with enhanced solar reflectance and durability, aligning with energy-efficient building requirements. Similarly, Kansai Paint’s “GOING THROUGH” global color concept (April 2026) introduces advanced finishes with improved gloss, depth, and translucency, catering to premium architectural and appliance applications.

Financial performance and strategic capital allocation are reinforcing industry expansion. Axalta’s record EBITDA performance in 2025, driven by growth in its industrial coatings segment, highlights the resilience of the coil coatings business despite macroeconomic challenges. Meanwhile, Nippon Paint’s ¥30 billion share buyback (February 2026) supports ongoing investments in coil coating capacity expansion across Southeast Asia and India, targeting the fast-growing building materials sector.

Leadership and operational transformation are further enabling long-term competitiveness. Beckers Group’s appointment of Dr. Susanne Goldammer as COO (June 2025) underscores its focus on streamlining global manufacturing operations and achieving Net Zero targets by 2050, particularly addressing the energy-intensive nature of coil coating production.

Regulatory Push Toward Energy-Efficient Building Envelopes

The coil coatings segment is increasingly shaped by building decarbonization mandates, with the EU Energy Performance of Buildings Directive (EPBD) 2024 acting as a central regulatory driver. As Member States approach the May 2026 transposition deadline, the directive is accelerating the adoption of high-performance “cool roof” systems in both new construction and retrofit applications.

A key technical requirement emerging from EPBD implementation is the Solar Reflectance Index (SRI) threshold of 75 or higher for coated metal roofing. This has catalyzed demand for advanced infrared-reflective pigments capable of reflecting up to 90% of solar radiation. The direct impact is substantial: coated metal roofs can reduce surface temperatures by as much as 30°C, translating into 15%–20% reductions in building cooling energy demand—a critical lever in achieving zero-emission building (ZEB) targets.

In parallel, the “solar-ready” mandate is redefining durability expectations. Coil coatings are now required to support a minimum 25-year service life, ensuring compatibility with photovoltaic systems that are increasingly integrated into roofing structures. This has elevated the importance of long-term weatherability, UV resistance, and adhesion stability under cyclic thermal loads.

The EPBD-driven renovation wave further amplifies this trend. With a target to upgrade the EU’s least energy-efficient building stock, coil coating manufacturers are developing over-paintable PVDF and SMP systems that enable retrofitting without full roof replacement. This regulatory environment is effectively transforming coil coatings from a protective layer into a functional energy-efficiency component within the building envelope.

Low-Cure Technologies Reshaping Manufacturing Economics

In the United States, policy-driven innovation is centered on reducing the embodied energy of construction materials, with the Department of Energy (DOE) promoting low-cure coil coating technologies through its Building Technologies Office. The transition from traditional high-temperature curing processes to low-cure chemistries is redefining both operational efficiency and carbon intensity in coil coating production.

Modern low-cure formulations achieve full cross-linking at peak metal temperatures (PMT) of 180°C to 200°C, compared to legacy systems requiring temperatures above 240°C. This reduction has a direct impact on energy consumption, enabling manufacturers to lower oven energy use by nearly 20% or alternatively increase line speeds by 10%–15% without additional capital investment.

The implications extend beyond factory efficiency into lifecycle carbon accounting. Under the Federal Buy Clean Initiative, Environmental Product Declarations (EPDs) are becoming mandatory for construction materials. Low-cure coatings offer a measurable advantage by reducing Global Warming Potential (GWP) by approximately 12% per square foot, positioning them as a premium, compliance-aligned solution in public infrastructure projects.

Additionally, the shift toward high-solids and waterborne systems is enabling VOC emissions to fall below 0.15 kg/L, meeting stringent regional air quality standards. This convergence of energy efficiency and emissions control is not incremental—it represents a process-level transformation that aligns manufacturing economics with sustainability metrics.

Integration of Solar Generation into Coated Metal Systems

A major structural opportunity in the coil coatings market lies in the emergence of Building-Integrated Photovoltaics (BIPV), where coated metal substrates serve as both structural and energy-generating components. This evolution moves beyond traditional “add-on” solar panels toward fully integrated roofing systems that combine durability with electricity generation.

Technologically, this is enabled by the compatibility of pre-coated steel and aluminum with thin-film photovoltaic materials such as CIGS (Copper Indium Gallium Selenide). These flexible solar cells can be directly laminated or deposited onto coil-coated substrates, creating a dual-function material that reduces installation complexity and structural load.

Critical to this application are specialized coil coatings that provide both dielectric insulation and long-term adhesion. Advanced primer systems now achieve dielectric breakdown voltages exceeding 1,000V while maintaining structural integrity under prolonged damp-heat conditions (85°C/85% RH). This ensures electrical safety and durability in real-world operating environments.

From an economic perspective, BIPV systems are approaching grid parity, with payback periods estimated at 7 to 10 years. This makes them increasingly attractive to industrial real estate investors and commercial developers seeking to align with sustainability mandates while generating on-site energy. The integration of aesthetics—through matte and textured finishes—further enhances adoption by addressing architectural design constraints.

High-Performance Direct-to-Metal Systems for Complex Architectures

The demand for complex architectural geometries is driving the adoption of Direct-to-Metal (DTM) coil coatings, which eliminate the need for multi-layer coating systems while maintaining high-performance characteristics. This represents a shift toward process simplification without compromising durability or aesthetics.

DTM systems are engineered to withstand extreme forming processes, including 0-T to 1-T bend tests, enabling their use in perforated facades, composite panels, and other advanced architectural elements. This level of formability is essential for modern designs that prioritize fluid shapes and intricate detailing.

From a manufacturing perspective, eliminating the primer layer reduces total coating thickness by approximately 25%, resulting in lower material consumption and faster production cycles. Despite this reduction, DTM coatings maintain robust corrosion resistance, exceeding 1,500 hours in salt spray testing, ensuring long-term durability in harsh environments.

Aesthetic performance has also advanced significantly. High-gloss, metallic, and iridescent finishes—previously achievable only through multi-coat systems—are now possible with single-layer DTM coatings. This is particularly relevant in premium commercial and retail construction, where visual differentiation is a key design requirement.

Field performance metrics further reinforce their value. Reduced edge-creep corrosion—by approximately 30% compared to traditional systems—minimizes maintenance requirements and extends asset life, making DTM coatings a high-margin, performance-driven solution for next-generation architectural applications.

Solvent-Borne Coil Coatings Lead Market with 46% Share Driven by High-Speed Line Efficiency and PVDF Performance

Technology Analysis: High-Solids Solvent Systems Dominate Coil Coating with Rapid Cure and Premium Finish Quality

Solvent-borne coatings dominate the coil coatings market with a 46.0% share in 2025, primarily due to their unmatched ability to perform under ultra-high-speed coil coating line conditions (150–250 meters per minute). These coatings—based on polyester, polyurethane, and PVDF (polyvinylidene fluoride) resins—enable rapid solvent flash-off and curing within 20–40 seconds, ensuring consistent, defect-free finishes across continuous metal strips. Their superior rheology allows precise film thickness control (±1 micron), critical for pre-painted steel and aluminum used in construction and appliances. A key value driver is PVDF-based solvent-borne coatings, which deliver 30–50 year durability, UV resistance, and corrosion protection, making them the premium choice for architectural metal panels. Additionally, advancements in high-solids formulations and solvent recovery systems (>98% capture efficiency) ensure compliance with VOC regulations, reinforcing solvent-borne dominance in the global coil coatings market.

Building & Construction Sector Dominates Coil Coatings Market with 54% Share Driven by Metal Roofing and Infrastructure Demand

End-Use Sector Analysis: Pre-Painted Metal Panels Fuel Growth in Modern Construction Applications

The building and construction sector accounts for a dominant 54.0% share of the coil coatings market in 2025, driven by the widespread adoption of pre-painted metal roofing, wall panels, and structural components in residential, commercial, and industrial construction. Coil-coated materials such as Galvalume® steel and aluminum panels are preferred for their durability, lightweight properties, corrosion resistance, and rapid installation capabilities. Key growth drivers include the surge in mega-warehouses, data centers, and logistics hubs, where metal panels provide cost-effective and scalable building solutions. Additionally, increasing adoption of cool roof technologies with solar-reflective pigments (SRP) is enhancing energy efficiency by reducing surface temperatures and lowering cooling costs by 10–25%. The segment is also benefiting from demand for resilient construction materials capable of withstanding extreme weather conditions. These factors firmly establish construction as the primary growth engine in the global coil coatings market.

Coil Coatings Market Competitive Landscape Driven by Sustainable Chemistry, High-Performance Coatings, and Infrastructure Demand

The coil coatings market is highly competitive, led by global players focusing on high-durability coatings, sustainable formulations, and advanced PVDF and polyester technologies. Growth is driven by infrastructure projects, green building standards, and demand for pre-painted steel and aluminum in construction, automotive, and appliance applications.

AkzoNobel Leads Premium Coil Coatings with High-SRI Architectural Innovations

AkzoNobel N.V. holds the largest global share in premium coil coatings, driven by strong demand for architectural facades and high-performance roofing systems. Its CERAM-A-STAR® 1050 innovation enhances solar reflectance index (SRI), addressing urban heat island mitigation, a critical factor in 2026 infrastructure and green building projects. The company has expanded its integrated supply chain across Asia-Pacific and the Middle East, targeting large-scale giga-projects requiring localized coil coating solutions. AkzoNobel’s leadership in sustainable coatings is reinforced through low-VOC, water-based, and high-solids polyester technologies. Its Industrial Excellence roadmap aims to sustain EBITDA margins between 14% and 15% through operational optimization. The company’s advanced R&D capabilities and regional expansion strengthen its dominance in high-durability coil coatings.

PPG Expands PVDF Coil Coatings Leadership with Digital and AI-Driven Solutions

PPG Industries, Inc. reported $15.9 billion in 2025 net sales, with its Industrial Coatings segment gaining share in coil coatings and automotive OEM applications. Its PPG DURANAR® MX PVDF coating delivers superior color retention, chalk resistance, and long-term durability for high-rise commercial buildings. The integration of the PPG LINQ™ digital ecosystem enhances coil coating processes through automated color matching, reducing material waste by up to 15%. PPG’s focus on AI-designed coatings accelerates product development cycles for specialized coil finishes. The company maintains strong positioning in aerospace and transportation coil coatings, offering lightweight and chemically resistant primers. Its technical expertise and digital integration reinforce leadership in high-performance fluoropolymer coatings.

Sherwin-Williams Strengthens Coil Coatings Supply Chain with Capacity Expansion

The Sherwin-Williams Company significantly expanded its Bowling Green, Kentucky facility in March 2026, doubling capacity to meet rising demand in roofing and OEM coil coating markets. Its PolyPREMIER™ polyester and WeatherXL™ silicone-modified polyester coatings are widely adopted in North American siding applications due to fast turnaround times and high durability. The company’s direct-to-customer model ensures strong engagement with roll formers and architectural specifiers, enhancing service efficiency. Advanced automation and increased batch production capabilities strengthen supply chain resilience across global operations. Sherwin-Williams’ PVDF and SMP coating technologies meet stringent environmental and weathering performance standards. Its strategic investments support growing demand for high-performance pre-painted metal coatings in construction and industrial sectors.

Beckers Drives Volume Leadership with Low-Carbon and Bio-Based Coil Coatings

Beckers Group is the global leader in coil coatings by volume, operating across 23 locations in 17 countries and serving customers in over 60 markets. The company achieved a major sustainability milestone by scaling Near-Infrared curing technology, reducing coating line carbon emissions by up to 50%. Beckers holds a robust share in the building and construction segment, driven by high-performance topcoats for steel and aluminum cladding. Its bio-based coil coatings, derived from agricultural waste resins, target the premium green building segment in Europe. The company’s focus on high-solids formulations eliminates the need for thermal oxidizers, improving energy efficiency. Beckers’ “Positive Impact” strategy positions it strongly in sustainable and circular coil coatings solutions.

Nippon Paint Expands Coil Coatings in Asia with Smart Surfaces and R&M Focus

Nippon Paint Holdings (NIPSEA Group) continues to expand through its asset assembler strategy and strengthening its coil coatings portfolio through acquisitions such as AOC. The company has shifted focus toward the renovation and maintenance coil coatings market in Asia, which now accounts for 70% of its regional sales amid slowing new construction. Nippon Paint dominates automotive coil coatings in Japan and China, supplying high-performance coatings for EV battery enclosures and structural components. Its smart surface innovations integrate antimicrobial and anti-fingerprint properties into pre-painted steel for appliances. The company is improving financial stability, targeting a Net Debt/EBITDA ratio of ~2.0x by 2026. Its regional leadership and product innovation support growth in high-spec coil coatings applications.

BASF Coatings Enhances Integrated Coil Solutions with Advanced Pigments and Partnerships

BASF SE’s Coatings division is transitioning into a standalone entity, strengthening its focus on high-performance coil coatings and integrated surface solutions. The company introduced the “Driving the Proxy” collection, featuring advanced interference pigments such as Tesseract Blue and Phygital Magnetar for automotive and industrial coil applications. BASF leads in surface treatment and e-coat integration, delivering system-based solutions that combine corrosion protection with aesthetic performance. Its partnership with the Audi Revolut F1 Team highlights the capabilities of Glasurit 100 Line waterborne coatings in lightweight and efficient applications. BASF’s vertical integration into specialty resins and additives ensures consistent quality and supply chain reliability. Its chemical-to-coating approach enhances performance and innovation in advanced coil coatings systems.

China Coil Coatings Market: ZM Steel Leadership and Intelligent Manufacturing Driving Global Scale

China continues to dominate the coil coatings market, driven by its leadership in Zinc-Magnesium-Aluminum (ZM) coated steel, which offers up to three times the corrosion resistance of conventional galvanization—critical for solar infrastructure. The country’s massive photovoltaic expansion is fueling demand for PVDF-coated aluminum coils used in inverter housings and floating solar systems.

Regulatory and technological shifts are accelerating transformation. The revised GB 4806.10-2025 standard is expanding approved materials for food-grade coatings, requiring reformulation of appliance coatings. Additionally, strict air quality mandates now require 95%+ solvent recovery, pushing adoption of waterborne and high-solid systems. AI-driven facilities like Allnex’s Jiaxing Mega-Site are enabling high-speed production of UV-curable resins, reinforcing China’s leadership in both scale and advanced manufacturing.

United States Coil Coatings Market: Infrastructure Modernization and EB/UV Technologies Driving Efficiency

The United States coil coatings market is evolving through federal infrastructure investment and advanced curing technologies. Under the Infrastructure Investment and Jobs Act (IIJA), over $40 billion is allocated to bridge rehabilitation, boosting demand for duplex coil-coated systems on high-performance steel.

A major innovation trend is the adoption of Electron Beam (EB) and UV curing, which enables instant curing with zero thickness loss, improving efficiency and sustainability. The CHIPS Act is also driving demand for chemical-resistant and anti-static coated steel in cleanroom environments. Residential remodeling trends are increasing use of cool-roof coil coatings, reducing solar heat gain by up to 25%, while regulatory shifts under TSCA are accelerating the adoption of oxygenated solvent systems.

India Coil Coatings Market: PLI Stimulus and Infrastructure Growth Fueling Rapid Expansion

India is rapidly transforming into a global hub for specialty coil coatings, supported by strong policy incentives and industrial expansion. Under PLI Scheme 1.2, investments of ₹11,887 crore ($1.43 billion) are driving production of PPGI and PPGL steel for automotive and appliance sectors.

Major projects such as the JSW–POSCO Odisha JV (6 MTPA) are boosting high-grade coated steel output. Infrastructure initiatives—including Smart Cities funding ($19.67 billion) and Vande Bharat train expansion—are driving demand for fire-resistant and silicon-modified polyester (SMP) coatings. Growth in appliance exports is further increasing demand for antimicrobial and stain-resistant coated sheets, while domestic production of waterborne PU dispersions is supporting sustainability goals.

Germany Coil Coatings Market: Green Steel and Circular Economy Driving Sustainability Leadership

Germany remains the benchmark for sustainable coil coatings, driven by decarbonization and circular economy initiatives. The green steel market (~$33 billion in 2024) is rapidly expanding, supported by hydrogen-based direct reduction technologies.

Innovation is centered on sustainability and traceability. The commercialization of bio-circular resins is reducing CO₂ emissions by up to 50%, while proactive compliance with REACH 2.0 is accelerating the shift toward PFAS-free coatings. Germany is also pioneering Digital Product Passports (DPP), enabling full lifecycle tracking of coated materials. Additionally, the adoption of electric IR-curing systems is reducing energy consumption by up to 25%, reinforcing Germany’s leadership in eco-friendly coil coatings.

Japan Coil Coatings Market: Nanotechnology and Urban Redevelopment Driving Advanced Applications

Japan’s coil coatings market is defined by precision engineering and smart coating technologies, particularly in urban infrastructure. Large-scale redevelopment projects such as Roppongi 5-chome are driving demand for high-durability PVDF and SMP coatings for architectural facades.

Technological innovation is strong in multifunctional coatings. Japan is pioneering photocatalytic self-cleaning coatings, reducing maintenance costs for high-rise buildings. Additionally, thermally conductive coatings for EV battery enclosures are improving heat dissipation, while aluminum coil coatings are gaining traction due to recyclability and lightweight advantages. Government initiatives promoting Zero Energy Buildings (ZEB) are further boosting demand for high-reflectivity coatings.

South Korea Coil Coatings Market: High-Tech Mobility and Graphene Innovation Driving Performance

South Korea is a leader in high-performance coil coatings, particularly in automotive, shipbuilding, and electronics applications. Its dominance in LNG carrier construction is driving demand for heavy-duty coated steel capable of withstanding cryogenic conditions.

Innovation is focused on advanced materials and automation. The development of graphene-enhanced coil coatings is improving heat dissipation and extending service life of metal roofing by up to 30%. Additionally, signal-transparent coatings are enabling integration of radar systems in autonomous vehicles, while automated spray systems in Hyundai-Kia supply chains are ensuring precise color consistency. Government mandates to reduce industrial energy consumption are also accelerating adoption of cool-running ceramic coatings.

Brazil Coil Coatings Market: Agribusiness Demand and Biofuel Integration Driving Regional Growth

Brazil’s coil coatings market is driven by its strong agribusiness and renewable energy sectors. The expansion of ArcelorMittal’s galvanizing capacity is supporting demand for coated steel in automotive and appliance applications.

Agricultural growth is a major driver, with a 15% increase in demand for zinc-aluminum coated steel used in grain storage silos. The “Fuel of the Future” law is also increasing demand for biofuel-resistant coatings in storage tanks and pipelines. Investments of $19.5 billion in industrial modernization are boosting adoption of low-carbon coatings for wind and solar infrastructure. Additionally, offshore oil exploration is driving demand for seawater-resistant epoxy coatings, positioning Brazil as a key regional market.

Coil Coatings Market Report Scope

Coil Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.3 Billion

|

|

Market Size (2032)

|

$19.6 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Resin Chemistry (Polyester, Siliconized Modified Polyester (SMP), Polyvinylidene Fluoride, Polyurethane (PU), Plastisols (PVC), Epoxy, Acrylic), By Technology (Solvent-borne, Water-borne, Powder Coil Coatings, Radiation Curable), By Substrate Compatibility (Steel Coils, Aluminum Coils), By End-Use Sector (Building and Construction, Industrial and Domestic Appliances, Automotive and Transportation, Infrastructure and Energy, Furniture and Interiors), By Functional Specification (High-Reflectivity, Antimicrobial and Food-Grade, Anti-Corrosive, Textured and Metallic Finishes)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., PPG Industries, Inc., Sherwin-Williams Company, Beckers Group, Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun Group, Hempel A/S, KCC Corporation, Asian Paints Limited, Yung Chi Paint & Varnish Mfg. Co., Ltd., JSW Paints, Teknos Group Oy, Henkel AG & Co. KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coil Coatings Market Segmentation

By Resin Chemistry

- Polyester

- Siliconized Modified Polyester (SMP)

- Polyvinylidene Fluoride

- Polyurethane (PU)

- Plastisols (PVC)

- Epoxy

- Acrylic

By Technology

- Solvent-borne

- Water-borne

- Powder Coil Coatings

- Radiation Curable

By Substrate Compatibility

- Steel Coils

- Aluminum Coils

By End-Use Sector

- Building and Construction

- Industrial and Domestic Appliances

- Automotive and Transportation

- Infrastructure and Energy

- Furniture and Interiors

By Functional Specification

- High-Reflectivity

- Antimicrobial and Food-Grade

- Anti-Corrosive

- Textured and Metallic Finishes

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Coil Coatings Market

- AkzoNobel N.V.

- PPG Industries, Inc.

- Sherwin-Williams Company

- Beckers Group

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun Group

- Hempel A/S

- KCC Corporation

- Asian Paints Limited

- Yung Chi Paint & Varnish Mfg. Co., Ltd.

- JSW Paints

- Teknos Group Oy

- Henkel AG & Co. KGaA

*- List not Exhaustive