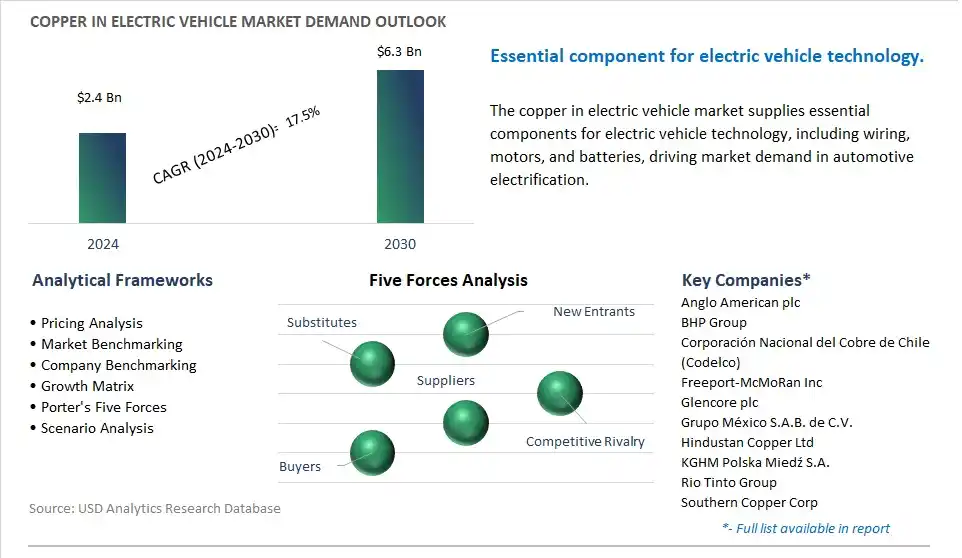

The global Copper In Electric Vehicle Market is poised to register a 17.5% CAGR from $2.4 Billion in 2024 to $6.3 Billion in 2030.

The global Copper In Electric Vehicle Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Vehicle (BEVS, PHEVS, HEVS), By Application (Electric Motors, Batteries, Wiring, Charging Stations, Others).

An Introduction to Global Copper In Electric Vehicle Market in 2024

The future of copper in electric vehicles (EVs) is driven by the rapid electrification of transportation, advancements in battery technology, and the growing demand for energy-efficient and sustainable mobility solutions. Copper plays a vital role in EVs, serving as a key component in electric motors, wiring harnesses, charging infrastructure, and battery systems. Key trends shaping this industry include the development of high-efficiency electric drivetrains and power electronics to maximize energy conversion and minimize copper usage, the optimization of battery chemistries and thermal management systems to enhance performance and durability, and the expansion of EV charging infrastructure to support widespread adoption and convenience. As automakers accelerate the transition to electric mobility and governments implement policies to reduce greenhouse gas emissions, the demand for copper in EVs and associated infrastructure is expected to grow substantially, driving market expansion and innovation.

Copper In Electric Vehicle Market Competitive Landscape

The market report analyses the leading companies in the industry including Anglo American plc, BHP Group, Corporación Nacional del Cobre de Chile (Codelco), Freeport-McMoRan Inc, Glencore plc, Grupo México S.A.B. de C.V., Hindustan Copper Ltd, KGHM Polska Miedź S.A., Rio Tinto Group, Southern Copper Corp.

Copper In Electric Vehicle Market Dynamics

Copper In Electric Vehicle Market Trend: Increasing Adoption of Electric Vehicles (EVs)

One prominent market trend in the copper in electric vehicle (EV) industry is the increasing adoption of electric vehicles worldwide. With growing concerns about climate change, air pollution, and fossil fuel dependency, there is a global push towards sustainable transportation solutions. Electric vehicles, powered by electricity stored in batteries, offer a cleaner and more environmentally friendly alternative to traditional internal combustion engine vehicles. Copper plays a crucial role in electric vehicles, as it is used extensively in wiring, motors, batteries, and charging infrastructure. As governments, automakers, and consumers embrace electric vehicles to reduce emissions and combat climate change, the demand for copper in the EV industry is expected to soar, driving market growth and opportunities for copper suppliers and manufacturers.

Copper In Electric Vehicle Market Driver: Electrification of Transportation Sector

A key driver in the copper in electric vehicle market is the electrification of the transportation sector. Governments around the world are implementing policies and incentives to accelerate the transition to electric vehicles as part of efforts to achieve carbon neutrality and meet climate targets. Automakers are investing heavily in electric vehicle development and production, introducing a wide range of electric models to meet consumer demand and regulatory requirements. Copper's high conductivity, durability, and reliability make it an essential material for electric vehicle components such as motors, inverters, wiring harnesses, and battery systems. The electrification of the transportation sector is driving the demand for copper in electric vehicles, creating opportunities for copper producers to meet the growing needs of the automotive industry.

Copper In Electric Vehicle Market Opportunity: Innovation in Copper-Based Technologies for EVs

One potential opportunity in the copper in electric vehicle market lies in innovation in copper-based technologies for EVs. As electric vehicle technology continues to evolve, there is a need for advanced materials and components that enhance performance, efficiency, and reliability. Copper-based innovations such as high-efficiency motors, lightweight wiring systems, and advanced battery technologies offer opportunities to improve the performance and range of electric vehicles while reducing manufacturing costs and environmental impact. By investing in research and development of copper-based technologies tailored to the specific needs of electric vehicles, manufacturers aim to gain market shares in the market and capitalize on the growing demand for sustainable transportation solutions.

Copper In Electric Vehicle Market Ecosystem

Copper's role in the Electric Vehicle (EV) market spans various stages of the Market Ecosystem. It begins with Copper Mining and Refining, where companies including Freeport-McMoRan Inc. and BHP Group Ltd. extract and refine copper ore into usable forms. Optionally, Copper Mills convert refined copper into semi-finished products. Next, Component Manufacturing involves Wire Harness Manufacturers including Aptiv PLC, and Motor Manufacturers including Nidec Corporation, which rely on copper for electrical wiring and motor windings, respectively. Other Component Manufacturers also utilize copper in various EV parts. Further, in Electric Vehicle Assembly, Automobile Manufacturers including Tesla, Inc. and Volkswagen AG integrate all components, including those containing copper, into functional electric vehicles.

Copper's Market Ecosystem in the EV market underscores its indispensability in powering electric vehicles. From its extraction and refining to its integration into various components, copper facilitates the transmission of electrical currents crucial for EV operation. Companies across the chain, from mining giants including Freeport-McMoRan Inc. to automotive leaders including Tesla, Inc., play vital roles in ensuring a robust supply of copper and its incorporation into EVs, driving innovation and sustainability in the automotive industry.

Copper in Electric Vehicle Market Share Analysis: Battery Electric Vehicles (BEVs) held the dominant revenue share in 2024

The largest segment in the Copper in Electric Vehicle (EV) Market is the "Battery Electric Vehicles (BEVs)" segment. This dominance is driven by BEVs rely solely on electricity stored in onboard battery packs to power electric motors, making them heavily dependent on copper-intensive components for electrical conductivity, energy storage, and power distribution. Copper is a crucial material in the manufacturing of electric vehicle batteries, electric motors, power electronics, and charging infrastructure due to its excellent electrical conductivity, thermal conductivity, and corrosion resistance properties. Additionally, BEVs require larger battery capacities to achieve longer driving ranges and higher performance, leading to increased copper content per vehicle compared to plug-in hybrid electric vehicles (PHEVs) and hybrid electric vehicles (HEVs). In addition, the growing adoption of BEVs worldwide, driven by government incentives, emissions regulations, consumer preferences, and technological advancements, fuels the demand for copper in electric vehicle production. Further, BEVs offer environmental benefits, energy efficiency, and reduced greenhouse gas emissions compared to conventional internal combustion engine vehicles, making them a preferred choice for automakers, policymakers, and consumers alike, further driving the growth of the BEV segment in the Copper in Electric Vehicle Market. As a result, the "Battery Electric Vehicles (BEVs)" segment is the largest segment in the Copper in Electric Vehicle Market due to the significant copper content and widespread adoption of BEVs in the global automotive market.

Copper in Electric Vehicle Market Share Analysis: Batteries is the fastest growing market segment over the forecast period to 2030

The fastest-growing segment in the Copper in Electric Vehicle (EV) Market is the "Batteries" segment. This trend is driven by batteries are essential components of electric vehicles, providing energy storage for powering electric motors and enabling vehicle propulsion. Lithium-ion batteries, the most common type used in EVs, rely on copper for various components, including current collectors, busbars, and interconnects, due to its high electrical conductivity, low resistance, and excellent thermal conductivity. Additionally, as battery technology continues to advance, there is a trend toward higher energy density and longer driving ranges, leading to increased demand for larger battery capacities and higher copper content per battery pack. In addition, the growing adoption of electric vehicles worldwide, driven by environmental regulations, government incentives, and consumer preferences, fuels the demand for batteries and, consequently, copper in electric vehicle production. Further, advancements in battery manufacturing processes, electrode materials, and cell designs aim to optimize performance, efficiency, and reliability, further driving the need for copper in battery applications. As a result, the "Batteries" segment is the fastest-growing segment in the Copper in Electric Vehicle Market, propelled by the increasing demand for electric vehicles, the critical role of batteries in vehicle electrification, and the rising copper content per battery pack to meet performance and range requirements.

Copper in Electric Vehicle Charging Infrastructure Market Share Analysis: Level 2 Charge Ports held the dominant revenue share in 2024

The largest segment in the Copper in Electric Vehicle Charging Infrastructure Market is the "Level 2 Charge Ports" segment. This dominance is driven by Level 2 charging ports are widely used in both residential and commercial settings due to their versatility, affordability, and faster charging speeds compared to Level 1 charging ports. Level 2 charging ports operate at higher power levels, ranging from 3.3 kW to 22 kW, allowing for quicker charging times compared to the standard household outlets used for Level 1 charging. Additionally, Level 2 charging infrastructure is compatible with a wide range of electric vehicles, including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs), making them suitable for various applications, from home charging stations to public charging networks. In addition, the growing adoption of electric vehicles worldwide, driven by government incentives, emissions regulations, and consumer preferences, fuels the demand for Level 2 charging infrastructure to support the expanding EV market. Further, Level 2 charging ports offer the convenience of faster charging without the high installation costs associated with Level 3 DC fast chargers, making them an attractive option for residential installations, workplace charging, retail locations, and public parking facilities. As a result, the "Level 2 Charge Ports" segment is the largest segment in the Copper in Electric Vehicle Charging Infrastructure Market due to its widespread use, compatibility, affordability, and versatility in supporting electric vehicle charging needs for residential and commercial applications.

Copper in Electric Vehicle Charging Infrastructure Market Share Analysis: Commercial Charging Station is the fastest growing market segment over the forecast period to 2030

The fastest-growing segment in the Copper in Electric Vehicle Charging Infrastructure Market is the "Commercial Charging Station" segment. This trend is driven by the increasing adoption of electric vehicles (EVs) worldwide is driving the demand for public charging infrastructure to support the growing EV market. Commercial charging stations play a crucial role in providing convenient and accessible charging solutions for EV owners who do not have access to private charging facilities or need to charge their vehicles while away from home. Additionally, commercial charging stations are essential for promoting EV adoption in urban areas, commercial districts, workplaces, retail locations, and public spaces, where EV drivers require reliable and fast-charging options to meet their daily commuting and travel needs. In addition, government incentives, regulations, and initiatives aimed at promoting electric vehicle adoption and reducing greenhouse gas emissions encourage investments in public charging infrastructure, including commercial charging stations. Further, advancements in charging technology, such as Level 3 DC fast chargers, high-power charging networks, and smart charging solutions, further drive the growth of commercial charging stations by improving charging speeds, efficiency, and user experience. As a result, the "Commercial Charging Station" segment is the fastest-growing segment in the Copper in Electric Vehicle Charging Infrastructure Market, propelled by the increasing demand for public charging solutions, the expansion of the EV market, and the role of commercial charging stations in supporting EV adoption, urban mobility, and sustainability initiatives.

Copper In Electric Vehicle Market Report Scope-

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

Copper In Electric Vehicle Market Companies Profiled

Anglo American plc

BHP Group

Corporación Nacional del Cobre de Chile (Codelco)

Freeport-McMoRan Inc

Glencore plc

Grupo México S.A.B. de C.V.

Hindustan Copper Ltd

KGHM Polska Miedź S.A.

Rio Tinto Group

Southern Copper Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Copper In Electric Vehicle Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Copper In Electric Vehicle Market Size Outlook, $ Million, 2021 to 2030

3.2 Copper In Electric Vehicle Market Outlook by Type, $ Million, 2021 to 2030

3.3 Copper In Electric Vehicle Market Outlook by Product, $ Million, 2021 to 2030

3.4 Copper In Electric Vehicle Market Outlook by Application, $ Million, 2021 to 2030

3.5 Copper In Electric Vehicle Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Copper In Electric Vehicle Industry

4.2 Key Market Trends in Copper In Electric Vehicle Industry

4.3 Potential Opportunities in Copper In Electric Vehicle Industry

4.4 Key Challenges in Copper In Electric Vehicle Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Copper In Electric Vehicle Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Copper In Electric Vehicle Market Outlook by Segments

7.1 Copper In Electric Vehicle Market Outlook by Segments, $ Million, 2021- 2030

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

8 North America Copper In Electric Vehicle Market Analysis and Outlook To 2030

8.1 Introduction to North America Copper In Electric Vehicle Markets in 2024

8.2 North America Copper In Electric Vehicle Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Copper In Electric Vehicle Market size Outlook by Segments, 2021-2030

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

9 Europe Copper In Electric Vehicle Market Analysis and Outlook To 2030

9.1 Introduction to Europe Copper In Electric Vehicle Markets in 2024

9.2 Europe Copper In Electric Vehicle Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Copper In Electric Vehicle Market Size Outlook by Segments, 2021-2030

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

10 Asia Pacific Copper In Electric Vehicle Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Copper In Electric Vehicle Markets in 2024

10.2 Asia Pacific Copper In Electric Vehicle Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Copper In Electric Vehicle Market size Outlook by Segments, 2021-2030

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

11 South America Copper In Electric Vehicle Market Analysis and Outlook To 2030

11.1 Introduction to South America Copper In Electric Vehicle Markets in 2024

11.2 South America Copper In Electric Vehicle Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Copper In Electric Vehicle Market size Outlook by Segments, 2021-2030

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

12 Middle East and Africa Copper In Electric Vehicle Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Copper In Electric Vehicle Markets in 2024

12.2 Middle East and Africa Copper In Electric Vehicle Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Copper In Electric Vehicle Market size Outlook by Segments, 2021-2030

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Anglo American plc

BHP Group

Corporación Nacional del Cobre de Chile (Codelco)

Freeport-McMoRan Inc

Glencore plc

Grupo México S.A.B. de C.V.

Hindustan Copper Ltd

KGHM Polska Miedź S.A.

Rio Tinto Group

Southern Copper Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Vehicle

BEVS

PHEVS

HEVS

By Application

Electric Motors

Batteries

Wiring

Charging Stations

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)