Corrosion Protection Coating Market Size, Infrastructure Longevity Demand, and Advanced Protective Technologies

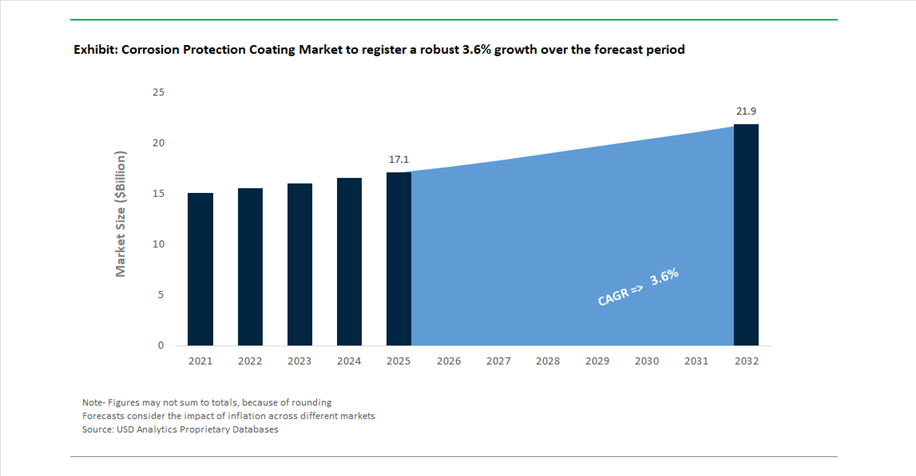

The global corrosion protection coating market was valued at $17.1 billion in 2025 and is projected to grow at a CAGR of 3.6% between 2025 and 2032, reaching $21.9 billion by 2032. This steady growth reflects sustained demand across marine, oil & gas, infrastructure, power generation, automotive, and industrial manufacturing sectors, where corrosion protection coatings are critical for asset longevity, structural integrity, and lifecycle cost reduction.

A primary growth driver is the increasing global focus on infrastructure durability and maintenance, particularly in aging assets such as bridges, pipelines, offshore platforms, and transportation systems. Corrosion-related degradation continues to impose significant economic costs, prompting governments and private operators to invest in high-performance coating systems that provide long-term protection against moisture, salt spray, chemicals, and extreme environmental conditions.

The market is also evolving with the adoption of advanced coating chemistries, including epoxy, polyurethane, zinc-rich primers, and powder coatings, which offer superior resistance and extended service life. Additionally, the transition toward environmentally compliant coatings, such as low-VOC, solvent-free, and high-solids formulations, is gaining momentum in response to stringent regulatory frameworks. Innovations in nanotechnology, smart coatings, and self-healing materials are further enhancing corrosion resistance and reducing maintenance frequency.

Emerging applications in renewable energy and electric vehicles (EVs) are creating new demand for corrosion protection coatings, particularly for battery systems, wind turbines, and solar infrastructure, where exposure to harsh environments necessitates advanced protective solutions.

Strategic Acquisitions, High-Performance Coating Innovation, and Industrial Expansion Driving Market Evolution

The corrosion protection coating market is being reshaped by strategic acquisitions, product innovation, and investments in high-performance technologies. A significant development is RPM International’s acquisition of Kalzip GmbH (April 2026), integrating high-performance aluminum roofing and façade systems into its portfolio. This strengthens RPM’s ability to deliver corrosion-resistant building envelope solutions, particularly for infrastructure and commercial construction projects in Europe and North America.

Innovation in protective coatings is accelerating to address emerging industrial needs. Jotun’s next-generation powder coatings (June 2025) are engineered for EV battery packs and energy storage systems, providing high-level corrosion protection (C5VH/CX classification) alongside thermal management and electrical insulation. Similarly, Kansai Helios’ launch of C5-class thin-film lacquers (March 2026) targets demanding applications in automotive and electrical machinery, offering protection against extreme corrosion and thermal stress.

Strong financial performance and strategic investments are enabling continued innovation. Sherwin-Williams reported record net sales of $23.57 billion in 2025, driven in part by robust demand for protective and marine coatings, and confirmed further investment in innovation programs to strengthen its competitive position. Meanwhile, Axalta’s record EBITDA performance (February 2026) supports ongoing expansion in advanced anti-corrosion systems for automotive and industrial applications.

Sector-specific demand is also driving technological advancements. AkzoNobel’s marine coatings contract for a new ferry fleet (March 2026) highlights the growing need for low-drag, anti-corrosive coatings that improve fuel efficiency and support maritime decarbonization. In parallel, PPG’s digital innovations showcased at AIA 2025 enable more precise application of corrosion-resistant coatings on architectural metals, improving durability and reducing material waste in harsh environments.

Supply chain optimization and regional expansion are enhancing market accessibility. Kansai Helios’ new logistics hub in Vienna (operational expansion 2026) improves distribution efficiency across the EMEA region, supporting infrastructure projects requiring high-performance protective coatings. Additionally, AkzoNobel’s €1.1 billion capital raise (March 2026) provides financial flexibility for continued investment in performance coatings R&D, reinforcing its leadership in corrosion protection technologies.

Stringent Pipeline Integrity Regulations Accelerating Adoption of High-Performance Anti-Corrosion Coatings

The corrosion protection coating market is undergoing a structural transformation driven by the enforcement of the PHMSA final rule under 49 CFR 192, which significantly elevates compliance requirements for gas transmission pipeline safety. This regulatory framework mandates proactive and quantifiable coating integrity assessments, fundamentally altering how pipeline operators approach corrosion mitigation strategies. Operators are now required to conduct Direct Current Voltage Gradient (DCVG) or Alternating Current Voltage Gradient (ACVG) inspections on newly installed pipelines exceeding 1,000 feet within six months of commissioning, introducing a strict early-life monitoring regime.

The introduction of clearly defined severe damage thresholds, such as voltage drops exceeding 60% in DCVG or 70 dBµV in ACVG surveys, has standardized failure classification across the industry. This is forcing operators to transition toward high-durability corrosion protection coatings capable of withstanding mechanical stress during installation and long-term environmental exposure. Abrasion Resistant Overcoats (ARO) and Dual-Layer Fusion Bonded Epoxy (FBE) systems are emerging as preferred solutions due to their superior resistance to impact damage, soil stress, and chemical degradation in aggressive environments.

Another critical dimension introduced by the regulation is lifecycle traceability. Pipeline operators must now maintain detailed records of coating inspections, defect identification, and remedial actions for the entire operational lifespan of the asset. This requirement is accelerating the integration of digital asset integrity management systems, creating a “cradle-to-grave” data architecture for corrosion protection coatings. The result is a shift from reactive maintenance toward predictive corrosion management, where coating performance data becomes a core input in risk modeling and infrastructure investment decisions.

EU Industrial Emissions Directive Driving Low-VOC Corrosion Protection Technologies

The European corrosion protection coatings market is being reshaped by the implementation phase of the revised Industrial Emissions Directive (Directive 2024/1785), which introduces stringent VOC emission limits and operational compliance requirements for industrial coating applications. With a mandatory transposition deadline of July 1, 2026, the directive is directly impacting coating manufacturers, applicators, and asset owners across sectors such as oil and gas, power generation, and heavy infrastructure.

A defining feature of the directive is the enforcement of Best Available Techniques Associated Emission Levels (BAT-AELs), which now require facilities to operate at the lower end of permissible emission ranges. This is accelerating the adoption of waterborne epoxy coatings, ultra-high solids coatings exceeding 85% solids content, and solvent-free corrosion protection systems. These technologies not only reduce VOC emissions but also enhance film build efficiency and long-term durability in industrial environments.

The directive also mandates the implementation of Environmental Management Systems (EMS) by 2030, requiring coating facilities to develop structured industrial transformation plans targeting climate neutrality and emission reduction. This is pushing manufacturers to optimize production processes, integrate renewable energy sources, and redesign product portfolios around sustainability-driven performance metrics.

Financial risk exposure has increased significantly under the revised framework, with penalties reaching at least 3% of annual EU turnover for major compliance failures. This has elevated environmental compliance from a regulatory obligation to a core strategic priority, influencing procurement decisions, technology investments, and supplier selection across the corrosion protection coatings value chain.

Graphene-Enhanced Epoxy Coatings Unlocking Next-Generation Marine Corrosion Resistance

Graphene-enhanced epoxy coatings are emerging as a high-value innovation in the corrosion protection coatings market, particularly for maritime applications such as ballast water tanks and offshore steel structures. These advanced coatings leverage the unique barrier properties of graphene to create a “tortuous path” that significantly restricts the diffusion of water, oxygen, and chloride ions through the coating matrix.

Recent technical advancements demonstrate that functionalized graphene nanofillers can achieve corrosion resistance efficiencies exceeding 99% in chloride-rich environments, outperforming conventional epoxy coatings. This level of protection is particularly critical in ballast water tanks, where continuous exposure to saline water and microbial activity accelerates corrosion processes.

In addition to barrier performance, graphene-based systems enhance interfacial adhesion between the coating and substrate. Reduced Graphene Oxide (rGO) derivatives have shown significant improvements in delamination resistance, maintaining structural integrity after more than 2,000 hours of immersion in synthetic seawater. This directly translates into longer service intervals and reduced maintenance frequency for marine assets.

The economic implications are substantial. By extending the time-to-first-maintenance from approximately 15 years to over 20 years, these coatings reduce dry-docking frequency and associated operational downtime. Furthermore, the superior barrier efficiency allows for thinner coating applications, reducing overall coating weight by around 10% on large vessels, contributing to fuel efficiency and emission reduction.

Polysiloxane Hybrid Coatings Advancing Offshore Wind Corrosion Protection

The rapid expansion of offshore wind energy infrastructure is creating a specialized demand for high-performance corrosion protection coatings capable of withstanding extreme environmental conditions. Polysiloxane hybrid coatings are emerging as a preferred solution due to their ability to combine durability, UV resistance, and application efficiency in harsh marine environments.

One of the most significant advantages of polysiloxane coatings is their high-build capability, enabling full ISO 12944 C5-M protection in a two-coat system. This eliminates the need for traditional three-coat systems that include a separate polyurethane topcoat, reducing application time by approximately 30% and lowering labor costs for offshore installations.

Performance metrics further reinforce their suitability for offshore applications. These coatings maintain gloss retention above 85% after 3,000 hours of QUV exposure, demonstrating superior resistance to UV degradation compared to conventional polyurethane systems. Their thermal stability across a wide temperature range from -40°C to +120°C ensures consistent performance under fluctuating marine conditions.

Field data indicates that polysiloxane systems significantly reduce under-film blistering and corrosion propagation, with salt spray resistance exceeding 15,000 hours in accelerated testing environments. This enhances asset reliability and reduces maintenance frequency for offshore wind towers, where access and repair costs are inherently high.

Epoxy Coatings Dominate Corrosion Protection Market with 44% Share Driven by Superior Barrier Performance and Industrial Reliability

Resin Type Analysis: High-Performance Epoxy Coatings Lead with Cross-Link Density and Chemical Resistance

Epoxy coatings command a dominant 44.0% share of the corrosion protection coatings market in 2025, driven by their unmatched ability to deliver adhesion, chemical resistance, and low moisture vapor transmission rates (MVTR) in aggressive environments. Their densely cross-linked thermoset structure, formed through reactions between epoxy resins and curing agents such as amines or polyamides, creates a highly durable barrier against water ingress, corrosion, and chemical attack. Epoxies are the foundational layer in multi-coat protective systems (zinc-rich primer + epoxy intermediate + polyurethane topcoat) used across marine, oil & gas, and infrastructure applications. The segment includes diverse technologies such as polyamide epoxies for surface-tolerant maintenance, novolac epoxies for high-temperature chemical resistance, and 100% solids solvent-free epoxies for confined spaces. Their versatility across both factory-applied (FBE coatings) and field-applied systems reinforces epoxy’s leadership in the global corrosion protection coatings market.

Infrastructure Sector Leads Corrosion Protection Market with 27% Share Driven by Global Asset Maintenance and Public Investment

End-Use Industry Analysis: Bridge Coatings and Water Infrastructure Drive High-Volume Demand

The infrastructure sector accounts for a leading 27.0% share of the corrosion protection coatings market in 2025, driven by the extensive global network of bridges, highways, tunnels, ports, and water systems requiring ongoing maintenance and protection. Atmospheric and splash-zone corrosion in C3–C5 environments (per ISO 12944) necessitates high-performance coating systems, typically consisting of zinc-rich epoxy primers, epoxy build coats, and polyurethane topcoats. A major growth driver is increased public investment through initiatives such as the U.S. Infrastructure Investment and Jobs Act (IIJA), the EU Green Deal, and China’s Belt and Road Initiative, all of which are accelerating large-scale refurbishment projects. Additionally, the growing adoption of overcoating strategies—applying advanced epoxy systems over existing coatings to avoid costly lead paint removal—is significantly boosting demand. These factors position infrastructure as the primary growth engine in the global corrosion protection coatings market.

Corrosion Protection Coatings Market Competitive Landscape Driven by Marine Coatings, Energy Infrastructure, and High-Performance Anti-Corrosive Technologies

The corrosion protection coatings market is highly competitive, driven by demand from offshore energy, infrastructure, marine, and industrial sectors. Key players focus on high-performance anticorrosive coatings, low-VOC formulations, and digital monitoring systems to enhance asset durability, lifecycle performance, and sustainability.

AkzoNobel Strengthens Global Anticorrosive Leadership with EV and Marine Coatings Expansion

AkzoNobel N.V., through its International® brand, is reinforcing its leadership in corrosion protection coatings with a proposed merger with Axalta, forming a $17 billion coatings powerhouse. The company achieved a 27% operating profit increase in 2025 and raised €1.1 billion in 2026 to fund decarbonization initiatives. Its Interpon powder coatings under the “Rhythm of Blues” collection deliver advanced corrosion resistance for EV battery enclosures and charging infrastructure. AkzoNobel remains a dominant force in marine anticorrosive coatings, widely specified for container ships and offshore wind structures. Portfolio optimization through divestments supports its focus on high-margin performance coatings. Its innovation and scale strengthen its position in industrial corrosion protection.

PPG Expands Protective Coatings with Digital Twin Monitoring and Energy Infrastructure Solutions

PPG Industries, Inc. continues to lead in protective and marine coatings, supported by $15.9 billion in 2025 revenue and strong organic growth in infrastructure and offshore energy sectors. Its integrated coatings suite for data centers combines corrosion protection with heat-reflective performance, improving energy efficiency. The adaptation of SOLARON BLUE PROTECTION™ technology enhances UV stability and reduces application time by 20% for structural steel coatings. PPG LINQ™ enables digital twin monitoring of coating performance, tracking corrosion and film thickness in real time. The company is positioning itself as a key supplier for hydrogen storage and carbon capture systems. Its innovation and digital integration reinforce leadership in advanced corrosion protection coatings.

Sherwin-Williams Enhances Infrastructure Coatings with High-Performance Polysiloxane Systems

The Sherwin-Williams Company is expanding its presence in corrosion protection coatings through its Protective and Marine segment, supported by strong financial performance and steady growth outlook for 2026. Its Dura-Plate® and Sher-Loxane® systems have been deployed in large-scale infrastructure projects, including water treatment facilities. The Corothane® I GalvaPac 1K primer remains a benchmark for one-coat corrosion protection in harsh coastal environments. Sherwin-Williams leverages its extensive distribution network to provide just-in-time delivery, reducing contractor downtime by 15%. Integration of Suvinil and BASF assets enhances its global industrial coatings portfolio. Its focus on durability and supply chain efficiency strengthens its market position.

Hempel Advances Long-Life Corrosion Protection with Low-VOC Zinc-Rich Primers

Hempel A/S is driving innovation in corrosion protection coatings with its Avantguard® 750 Pro primer, offering 76% solids volume and ultra-low VOC content for high-corrosion environments. Its coatings provide protection for over 35 years, significantly reducing lifecycle emissions for infrastructure such as bridges and offshore wind farms. The company is targeting 50% of revenue from sustainable solutions by 2026. Hempel secured major contracts for offshore wind projects, supplying high-build epoxy coatings designed for extreme conditions. Its Hempaguard® hull coatings contribute to significant CO2 reductions through improved vessel efficiency. The company’s sustainability focus and technical performance strengthen its leadership in corrosion protection.

Jotun Expands High-Temperature and EV Coatings with Strong Marine Market Presence

Jotun A/S is a key player in corrosion protection coatings, dominating the tank coating market with its Tankguard range used in 30% of global chemical tankers. Its EV battery coating solutions provide both electrical insulation and high-level corrosion resistance for high-voltage systems. The upgraded Jotatemp coatings withstand temperatures up to 650°C, addressing corrosion under insulation challenges in refineries. Jotun’s Hull Performance Solutions contribute to fuel efficiency and maritime decarbonization. The company maintains strong manufacturing presence in Asia, supporting major shipbuilding hubs. Its diversified portfolio strengthens its competitive position across marine and industrial coatings.

RPM International Strengthens Industrial Corrosion Solutions with Carboline Portfolio

RPM International Inc., through its Carboline division, is expanding its footprint in corrosion protection coatings with strong financial growth and strategic acquisitions. The Carbozinc® series is widely used in nuclear power plants, offering superior cathodic protection in extreme environments. The acquisition of Kalzip enhances its integrated solutions for building envelopes and protective coatings. RPM’s MAP 2025 program has delivered significant cost savings through supply chain optimization and AI-driven procurement. Its coatings are designed for high-performance industrial applications, including energy and infrastructure sectors. The company’s focus on efficiency and advanced materials strengthens its role in corrosion protection markets.

United States Corrosion Protection Coatings Market: Infrastructure Reshoring and Nanotechnology Driving Leadership

The United States is a global leader in corrosion protection coatings, driven by infrastructure modernization and advanced material innovation. Under the Infrastructure Investment and Jobs Act (IIJA), over $40 billion has been allocated to bridge rehabilitation, mandating the use of inorganic zinc primers and high-performance epoxy systems designed for 50-year service life.

Innovation is a major differentiator. The introduction of nano-silica and ceramic nanoparticle coatings has improved abrasion resistance by up to 40%, particularly for coastal infrastructure. The expansion of semiconductor fabs under the CHIPS Act is also driving demand for ultra-high-purity dielectric corrosion coatings in cleanroom environments. Regulatory shifts under TSCA have accelerated adoption of waterborne and bio-based anti-corrosion resins (+22% YoY). Additionally, offshore wind expansion (30+ GW pipeline) is increasing demand for NORSOK-compliant coatings, while sensor-integrated smart coatings are enabling real-time corrosion monitoring in critical assets like pipelines.

China Corrosion Protection Coatings Market: ZM Steel Dominance and Green Transition Driving Scale

China remains the largest market globally, combining scale with a rapid shift toward sustainable and high-performance coatings. The implementation of GB 4806.10-2026 is tightening environmental compliance, accelerating adoption of zero-emission powder coating systems.

Technological leadership is evident in materials innovation. China dominates global exports of Zinc-Magnesium-Aluminum (ZM) coated steel, offering up to 3× higher corrosion resistance than traditional galvanization—critical for solar and infrastructure applications. Additionally, graphene-enhanced anti-corrosion coatings in marine vessels are reducing drag by 3–5%, improving efficiency. Large-scale urban renewal programs (~$50 billion in the Greater Bay Area) are driving adoption of self-healing polyurethane coatings, while expansion of high-purity NMP production supports advanced PVDF-based systems. Growth in hydrogen infrastructure is also increasing demand for HDPE internal linings to prevent embrittlement.

India Corrosion Protection Coatings Market: PLI Incentives and Energy Expansion Driving High Growth

India is emerging as a major growth hub for corrosion protection coatings, supported by strong policy incentives and rapid infrastructure expansion. Under the PLI Scheme 2.0 for Specialty Steel, over $1.43 billion is being invested to boost domestic production of galvanized (PPGI) and Galvalume (PPGL) coated steel.

Energy and transportation sectors are key drivers. The expansion of the Vande Bharat train fleet (400+ units by 2026) is increasing demand for fire-resistant and anti-graffiti coatings, while the construction of 12,000 km of new gas pipelines is driving adoption of 3-layer polyethylene (3LPE) and fusion-bonded epoxy (FBE) coatings. Coastal infrastructure mandates are also pushing adoption of C5-M marine-grade coatings, particularly silicon-modified polyesters. Additionally, the rapid deployment of solar parks is fueling 30% YoY growth in demand for UV-stable, salt-resistant coatings, positioning India as a high-growth market.

Germany Corrosion Protection Coatings Market: Hydrogen Infrastructure and Circular Chemistry Driving Sustainability

Germany remains the benchmark for sustainable and high-performance corrosion coatings, driven by strict environmental regulations and energy transition initiatives. The industry has achieved a ~90% phase-out of PFAS-based additives, aligning with REACH 2.0 compliance.

Innovation is centered on decarbonization and advanced infrastructure. The construction of a 9,700 km National Hydrogen Core Grid is driving demand for permeation-resistant internal coatings to prevent hydrogen embrittlement. Germany is also scaling bio-circular resins, reducing CO₂ emissions by up to 50%, and implementing Digital Product Passports (DPP) for full lifecycle traceability. Offshore wind expansion and automotive sector innovations—such as low-temperature curing e-coats (−25% energy use)—further reinforce Germany’s leadership in sustainable corrosion protection technologies.

Saudi Arabia Corrosion Protection Coatings Market: Vision 2030 and Extreme-Climate Applications Driving Demand

Saudi Arabia’s market is defined by megaprojects and harsh environmental conditions, requiring high-performance coatings. Projects like NEOM and The Line mandate high-reflectivity anti-corrosion coatings to manage thermal expansion in extreme desert temperatures.

Oil & gas investments are a major driver. Saudi Aramco’s refinery expansion is creating strong demand for heavy-duty epoxy and intumescent coatings, while desalination plant growth is increasing use of glass-flake reinforced polyester coatings. Government incentives under the IKTVA program are encouraging local production, and new IAQ regulations are accelerating adoption of waterborne protective systems. Additionally, defense sector localization is driving demand for chemical agent resistant coatings (CARC), reinforcing Saudi Arabia’s position in high-performance coatings.

Brazil Corrosion Protection Coatings Market: Offshore Dominance and Bio-Based Innovation Driving Growth

Brazil is a global leader in deepwater corrosion protection coatings, driven by its dominance in offshore oil production. Investments of $30 billion in FPSO projects (2026 pipeline) are driving demand for NORSOK-certified high-build epoxy coatings.

The expansion of pre-salt oil fields (depths >2,000 meters) is increasing demand for seawater-resistant subsea coatings, while infrastructure PPP programs (~$14 billion) are boosting adoption of zinc-rich primers and maritime coatings. Brazil is also advancing sustainability through bio-based polyurethane coatings derived from castor oil, leveraging its agricultural strength. Additionally, updated building codes mandating liquid-applied waterproofing systems are expanding applications in commercial construction, positioning Brazil as a key regional market.

South Korea Corrosion Protection Coatings Market: Shipbuilding Leadership and EV Innovation Driving Advanced Applications

South Korea is a global leader in high-performance corrosion coatings, leveraging its strengths in shipbuilding and electronics. Its dominance in LNG carrier construction is driving demand for cryogenic-resistant coatings for storage tanks and marine structures.

Innovation is also strong in EV and smart infrastructure. The development of fire-retardant and anti-corrosive silicone coatings for EV battery systems is a major focus, while government-backed “K-Sensor” initiatives are advancing self-healing coatings for smart bridges. Expansion of aviation MRO hubs is increasing demand for chrome-free aerospace primers, and the adoption of UV-LED curing technologies is reducing production cycles by ~20%. Additionally, the push toward decarbonized shipping is driving demand for low-friction anti-fouling coatings, reinforcing South Korea’s leadership in advanced coating technologies.

Corrosion Protection Coating Market Report Scope

Corrosion Protection Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.1 Billion

|

|

Market Size (2032)

|

$21.9 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Resin (Epoxy, Polyurethane (PU), Zinc-Rich Primers, Alkyd, Acrylic, Chlorinated Rubber, Specialty and Advanced Chemistries), By Technology (Solvent-borne, Water-borne, Powder-based), By Protection Mechanism (Barrier Coatings, Sacrificial, Inhibitive Coatings, Diffusion), By End-Use Industry (Oil and Gas, Marine, Infrastructure, Power Generation, Water Treatment, Petrochemical and Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Jotun A/S, Hempel A/S, RPM International Inc., Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., BASF SE, Sika AG, Chugoku Marine Paints, Ltd., Tnemec Company, Inc., The Dow Chemical Company, Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrosion Protection Coating Market Segmentation

By Resin

- Epoxy

- Polyurethane (PU)

- Zinc-Rich Primers

- Alkyd

- Acrylic

- Chlorinated Rubber

- Specialty and Advanced Chemistries

By Technology

- Solvent-borne

- Water-borne

- Powder-based

By Protection Mechanism

- Barrier Coatings

- Sacrificial

- Inhibitive Coatings

- Diffusion

By End-Use Industry

- Oil and Gas

- Marine

- Infrastructure

- Power Generation

- Water Treatment

- Petrochemical and Manufacturing

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Corrosion Protection Coating Market

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- Jotun A/S

- Hempel A/S

- RPM International Inc.

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- Sika AG

- Chugoku Marine Paints, Ltd.

- Tnemec Company, Inc.

- The Dow Chemical Company

- Wacker Chemie AG

*- List not Exhaustive