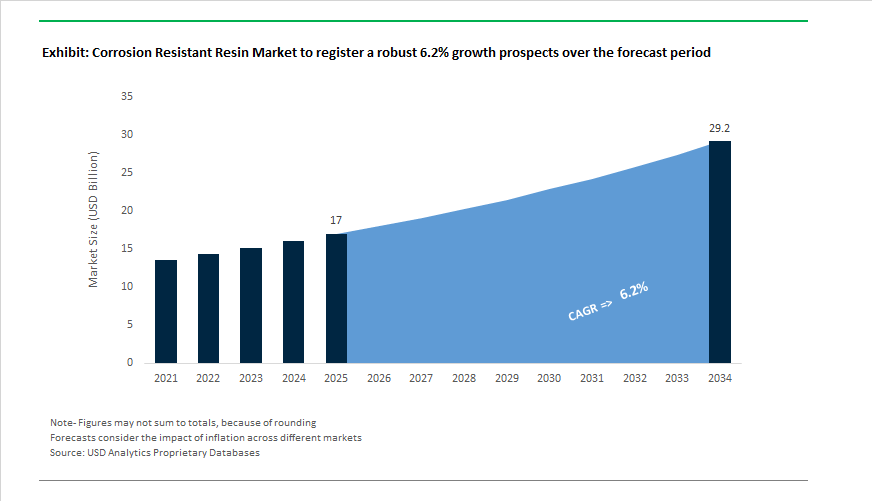

Corrosion Resistant Resin Market Outlook 2025–2034: $17 Billion to $29.2 Billion at 6.2% CAGR Driven by Composite Infrastructure, Marine +LC Resins, and Recyclable Epoxy Systems

The global Corrosion Resistant Resin Market is projected to grow from $17 billion in 2025 to $29.2 billion by 2034, registering a CAGR of 6.2%. Expansion is supported by rising demand for vinyl ester resins, unsaturated polyester resins (UPR), epoxy systems, urethane acrylates, and waterborne protective resin technologies across chemical storage, oil and gas, marine infrastructure, offshore wind, rail interiors, and automotive composite structures. Increasing investment in corrosion-resistant composite materials for harsh chemical environments, saltwater exposure, fire-retardant rail systems, and renewable energy infrastructure is strengthening long-term demand fundamentals. Sustainability mandates, recyclability requirements, and low-VOC resin innovations are reshaping formulation priorities across global composite supply chains.

Strategic consolidation and production expansion accelerated during 2024 and early 2025. In February 2024, AOC commissioned a new high-capacity specialty resin production line in Nanjing, significantly increasing output of Atlac® and Vipel® corrosion-resistant vinyl ester resins to serve Asia-Pacific chemical processing and infrastructure markets. In the same month, Covestro launched high-stability waterborne resins engineered for fast drying, chemical resistance, and low-VOC protective metal coatings. AOC and BÜFA extended their distribution agreement into Sweden in February 2024, improving access to specialty corrosion-resistant resins within the Nordic composite market. In March 2024, Polynt signed a Memorandum of Understanding to acquire Polyprocess, strengthening its gel coat and specialty corrosion-resistant surface technologies portfolio in Europe. In October 2024, Polynt finalized the merger of Reichhold do Brasil into Polynt Composites Brazil, streamlining production of DION® and DISTITRON® corrosion-resistant resins for South America’s oil and gas sector. Late 2024 also saw INEOS Enterprises agree to sell INEOS Composites to KPS Capital Partners for approximately €1.7 billion, a transaction expected to close in H1 2025, involving 17 global manufacturing sites specializing in vinyl ester and UPR corrosion-resistant systems.

Innovation in bio-based and recyclable resin chemistries gained visibility throughout 2024 and 2025. In September 2024, Scott Bader introduced Crestafire® Bio P1-8001 and P1-8003, 100% bio-based fire-retardant resins derived from sugar cane waste, designed to replace phenolic systems in rail applications while maintaining corrosion and fire resistance. In November 2024, AOC launched a UV-resistant SMC resin system for automotive exterior parts engineered to resist degradation from road salts and pollutants, expanding composite adoption in high-exposure environments. In March 2025, Scott Bader unveiled Crestapol® 1240 urethane acrylate resin at JEC World, enabling bulkhead bonding in marine construction without sanding or priming while maintaining saltwater corrosion resistance. In July 2025, LyondellBasell and Polynt announced collaboration on +LC low-carbon marine resins using bio-attributed feedstocks to reduce the carbon footprint of boat hulls and marine infrastructure while preserving osmotic and chemical resistance performance.

Offshore wind and circular composite mandates are driving structural shifts toward recyclability and EU expansion. In March 2024, Swancor signed a Letter of Intent with Siemens Gamesa to supply EzCiclo recyclable thermosetting epoxy resins for offshore wind turbine blades starting in 2026, enabling up to 95% material recovery at end of life. During 2025, Swancor established a Netherlands subsidiary to serve as a European technical hub, supporting HYVER and EzCiclo resin integration into maritime and wind energy supply chains ahead of 2026 sustainability mandates. These developments highlight accelerating demand for corrosion-resistant vinyl ester resins, epoxy composites, urethane acrylates, gel coats, and bio-attributed polymer systems across marine, wind energy, automotive, rail, and chemical storage infrastructure segments.

Trends and Opportunities in the Global Corrosion Resistant Resin Market

Shift Toward High-Performance Novolac and Specialty Resin Chemistries

- Operators handling severe chemical service conditions are increasingly bypassing standard vinyl ester resins in favor of Novolac and Bisphenol-F based systems that offer superior thermal stability and acid resistance. By late 2025, Novolac-type epoxy vinyl esters such as the Derakane™ 470 series had become the preferred choice for flue gas desulfurization units and chimney liners, where prolonged exposure to sulfuric and hydrochloric acids combined with elevated temperatures causes conventional resins to soften and lose mechanical strength. These Novolac systems maintain high strength retention in environments that historically required high-nickel alloys, creating a cost-effective alternative for corrosion-critical infrastructure.

- Bisphenol-F epoxy resins are gaining parallel momentum, particularly in marine and subsea applications. Their lower viscosity enables higher filler loading and improved fiber wet-out in fiber reinforced polymer composites, which is critical for storage tanks and process vessels operating in high-humidity and tropical corridors. Enhanced moisture resistance directly improves long-term structural integrity, reducing the frequency of repairs and extending inspection intervals. As offshore operators prioritize durability under cyclic loading and moisture ingress, Bisphenol-F chemistries are increasingly specified for next-generation corrosion resistant composite structures.

Acceleration of Sustainable and Circular Resin Formulations

- Sustainability mandates and Scope 3 emissions reporting are driving resin producers toward bio-based feedstocks and recyclable chemistries without compromising corrosion resistance. In October 2025, Braskem showcased updated life cycle assessment data for its I’m green™ bio-based polyethylene resins derived from sugarcane ethanol. These materials demonstrated carbon footprints ranging from −2.01 to −2.27 kgCO2e per kilogram of resin, positioning them as negative carbon footprint solutions for industrial and healthcare packaging applications requiring chemical resistance.

- At the same time, resin formulators are integrating biodegradable bio-inhibitors into corrosion resistant systems. Developments presented at the European Coatings Show 2025 highlighted formulations incorporating up to 95% biodegradable microbial polysaccharides and plant-derived extracts. These green resins are achieving inhibition efficiencies comparable to chromate-based systems in chloride-rich environments while complying with REACH Annex XVII restrictions. For end users, this trend reduces regulatory risk and hazardous material handling costs while supporting circular economy objectives.

Resin Demand Expansion Driven by CCUS and Flue Gas Treatment Systems

- The global rollout of post-combustion carbon capture and flue gas treatment infrastructure is creating a specialized demand for corrosion resistant resins capable of withstanding aggressive amine-based solvents. Monoethanolamine and methyldiethanolamine systems are highly corrosive to carbon steel, particularly during solvent regeneration cycles at temperatures between 100 and 150 degrees Celsius. This has driven increased adoption of FRP ducting, absorbers, and scrubbers based on brominated vinyl ester resins such as Derakane™ 510N, which combine fire retardancy with resistance to hot, acidic, moisture-laden flue gases.

- Beyond point-source capture, direct air capture technologies are opening a new resin-driven opportunity. A 2025 study conducted by Northwestern University highlighted the role of ion-exchange resins in moisture-swing DAC systems. These resins use negatively charged functional groups to capture carbon dioxide at low humidity and release it at higher humidity, offering potential energy savings of more than 40% compared with thermal-swing capture methods. As DAC projects scale, demand for chemically stable, regenerable resin systems is expected to grow sharply.

Ultra-Pure and Low-Leachable Resins for Semiconductor and Pharmaceutical Manufacturing

- Precision manufacturing environments are creating high-value opportunities for corrosion resistant resins engineered for ultra-low contamination and emissions. In semiconductor fabrication, ion exchange resins are now being specified for sub-3 nanometer wafer processes. Specialty grades developed by Mitsubishi Chemical are certified to meet SEMI F63 guidelines, maintaining ultra-pure water resistivity at 18.2 megaohm-centimeters and total organic carbon levels below 1.0 parts per billion. These performance thresholds are critical for preventing optical defects such as lens hazing in advanced immersion lithography.

- In the pharmaceutical sector, the implementation of USP <665> guidance has intensified scrutiny of plastic and resin components used in high-potency active pharmaceutical ingredient manufacturing. Producers are increasingly adopting low-leachable and low-extractable resin systems to mitigate the risk of process equipment-related leachables migrating into drug substances. This shift is elevating demand for clean, corrosion resistant resins that ensure regulatory compliance, product purity, and long-term equipment reliability in highly regulated production environments.

Corrosion Resistant Resin Market Share and Segmentation Insights

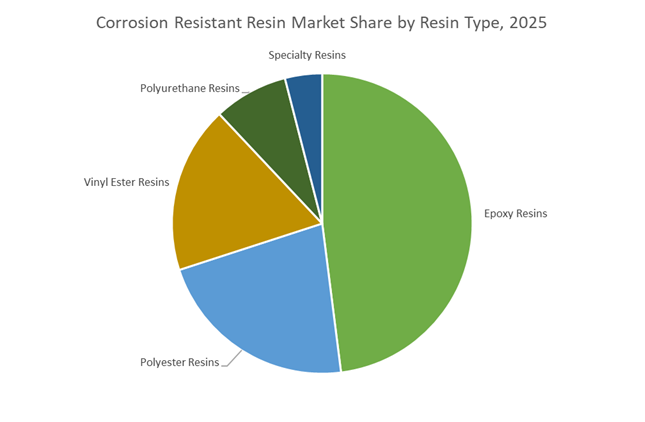

Resin Type Landscape: Epoxy Resins Lead Structural Protection While Vinyl Esters Serve High-Temperature Niches

Epoxy resins account for 48% of the corrosion resistant resin market in 2025, supported by superior adhesion, mechanical strength, and broad chemical resistance that make them the preferred matrix for fiberglass-reinforced plastic (FRP) tanks, linings, and piping systems in aggressive chemical environments. Their ability to bond strongly to steel and composite substrates underpins widespread use in chemical plants and oilfield infrastructure. Polyester resins maintain a significant share as a cost-effective alternative, delivering adequate corrosion resistance for construction, marine, and general industrial applications where budget constraints influence material selection. Vinyl ester resins occupy a critical performance segment, combining epoxy-like chemical resistance with polyester processing ease, enabling reliable service in high-temperature acidic conditions such as flue gas desulfurization units and pulp mill bleach plants. Polyurethane resins contribute abrasion and impact resistance in mining and material handling, while specialty resins including fluoropolymers and benzoxazines address extreme temperature and purity requirements.

End-Use Industry Distribution: Chemical Processing Anchors Demand as Energy and Infrastructure Expand Composite Adoption

Chemical processing represents 35% of corrosion resistant resin consumption, driven by extensive use in storage tanks, reactors, scrubbers, and piping handling corrosive acids, caustics, and solvents where material failure carries severe safety risks. Oil and gas follows closely, deploying glass-reinforced epoxy and vinyl ester systems in downhole tubing, offshore platforms, and pipelines exposed to H2S, CO2, and high-salinity produced water, increasingly replacing carbon steel in corrosive service. Infrastructure and construction applications focus on bridges, water treatment facilities, and corrosion-resistant rebar, leveraging FRP composites to extend asset life. Marine environments drive demand for lightweight, maintenance-free hulls and offshore structures. Power generation relies on vinyl ester and epoxy resins in cooling towers and scrubbers, while automotive and transportation represent an emerging segment adopting corrosion resistant composites for weight reduction and durability.

Competitive Landscape of the Corrosion Resistant Resin Market

The Corrosion Resistant Resin Market is defined by vinyl ester innovation, low-VOC formulations, and long-life composite systems for chemical processing, marine, energy, and infrastructure applications, with leading players competing on durability, sustainability, and vertically integrated supply chains.

AOC drives styrene-free vinyl ester adoption for long-life industrial assets

AOC holds a strong global position following the successful integration of AOC and Aliancys portfolios, offering benchmark Daron® and Atlac® vinyl ester resins for FGD units and chemical storage tanks. In late 2025, the company expanded manufacturing across Asia-Pacific to serve China’s fast-growing semiconductor and chemical processing sectors. Its 2026 Eco-Line™ launch introduced styrene-free vinyl esters that retain traditional mechanical performance while significantly lowering VOC emissions. AOC’s strategy centers on “Sustainability Through Longevity,” engineering corrosion resistant resin systems that extend industrial pipe service life beyond 50 years. This lifecycle-driven approach reduces total carbon footprint while reinforcing AOC’s leadership in chemical-resistant composites.

INEOS Composites strengthens marine and green hydrogen resin platforms

INEOS Composites, part of the INEOS Group, anchors its corrosion resistant resin leadership with the globally recognized Derakane™ portfolio. Its Derakane™ Signia™ epoxy vinyl ester improves shop-floor conditions through reduced styrene emissions and superior surface bonding. The company dominates marine and offshore wind, supplying resins for over 60% of premium FRP hull builds worldwide. In February 2026, INEOS unveiled a bio-attributed vinyl ester produced via mass-balance renewable feedstocks, targeting emerging green hydrogen infrastructure. Backed by INEOS’ vertical integration in styrene and epoxy precursors, the company benefits from unmatched supply chain stability and cost control in high-performance corrosion resistant resin manufacturing.

Ashland advances predictive resin engineering for specialty industrial coatings

Ashland has repositioned itself as a pure-play specialty materials provider, reporting over $2.1 billion in 2024 revenue with increasing emphasis on high-margin industrial coatings. Its Technical Service Labs deliver predictive modeling that helps engineers select corrosion resistant resins based on chemical exposure and operating temperature. During 2025–2026, Ashland introduced Klucel™ MS, a specialized thickener and anti-sagging additive for zinc-rich marine primers. The company is also scaling its Intelligent Color and Protection division, integrating resins with pigment systems for automotive and transportation markets. Ashland’s strength lies in application-driven R&D, supporting highly customized resin solutions for chemically aggressive environments.

Polynt-Reichhold leverages vertical integration for low-carbon marine resins

Polynt-Reichhold operates as one of the world’s largest specialty resin producers, generating approximately €2.16 billion in 2024 revenue with 36 plants globally. Its DION® vinyl ester systems are widely deployed in chlor-alkali and mineral extraction facilities where chemical resistance is critical. In July 2025, Polynt-Reichhold partnered with LyondellBasell to develop low-carbon (+LC) marine resins, addressing tightening environmental standards. A core differentiator is deep integration in organic anhydrides, delivering cost advantages across polyester and vinyl ester production. This vertically integrated model enables competitive pricing while supporting next-generation corrosion resistant resin platforms for infrastructure and marine composites.

Scott Bader accelerates recyclable composite resins for rail and marine

Scott Bader brings a unique employee-owned model to the corrosion resistant resin market, focusing on structural composites and adhesives. In early 2026, it expanded Southern European reach through a distribution partnership with Sandtech for its Crystic® VE vinyl ester resins and gelcoats. These systems are engineered for rail and marine applications where fire retardancy and corrosion resistance must coexist. The company also demonstrated corrosion-resistant materials for large-scale additive manufacturing at Formnext 2025, enabling 3D-printed chemical tank components. Guided by “The Scott Bader Way,” the firm is targeting 100% recyclable or bio-derived resin carriers by 2032.

Resonac pioneers hybrid epoxy systems for electronics and EV infrastructure

Formerly Showa Denko, Resonac integrates chemical and electronics expertise to lead high-purity epoxy resin development for semiconductors and advanced infrastructure. In 2026, the company launched a Hybrid Phenoxy-Epoxy resin combining thermoplastic toughness with thermoset chemical resistance, aimed at EV battery enclosures. Resonac holds a strong footprint across Asia-Pacific, supplying corrosion resistant resins for bridge rehabilitation and high-speed rail pylons in salt-heavy coastal zones. Its Co-Creation strategy leverages Japan-based innovation centers to develop customized blends with OEMs, supporting aerospace composites and next-generation electronics where ultra-clean, chemically robust resin systems are mandatory.

United States: Re-shoring Momentum and Defense-Grade Resin Innovation

The United States corrosion resistant resin industry in 2025 is being reshaped by strategic re-shoring, defense procurement, and accelerated low-VOC reformulation. Olin Corporation reinforced its strategic positioning as the last integrated epoxy resin supplier in Europe while expanding formulated corrosion-resistant resin solutions across North America. This dual strategy directly addresses competitive pressure from high-volume Asian imports while strengthening domestic supply resilience for infrastructure, coatings, and composites. Defense and aviation applications remain a critical demand pillar. The U.S. Department of Defense increased 2025 procurement of advanced vinyl ester resins for naval composites and coastal fuel storage tanks, explicitly prioritizing zero-PFAS additive systems to align with evolving environmental and operational safety standards.

Innovation intensity has also increased at the molecular design level. In early 2025, Hexion Inc. inaugurated its Global R&D Center in the Columbus region, deploying AI-enabled platforms to accelerate discovery of self-healing resin chemistries capable of withstanding highly acidic and corrosive environments. Regulatory pressure is reinforcing formulation change. The U.S. Environmental Protection Agency Clean Air Act updates effective 2026 have driven a rapid shift toward high-solids and water-borne corrosion resistant resins, resulting in a material reduction in solvent intensity across U.S. manufacturing plants. Capital inflows are further reshaping the landscape. KPS Capital Partners finalized its acquisition of INEOS Composites in H1 2025, signaling strong investor confidence in U.S.-based resin innovation for wind energy and transportation. Sustainability-led applications are also expanding, with Scott Bader advancing Crestafire Bio resins for rail flooring that combine recycled PET content with stringent fire, smoke, toxicity, and corrosion resistance performance.

India: Policy-Backed Localization and FRP Demand from Process Industries

India’s corrosion resistant resin industry is entering a structurally important expansion phase, driven by industrial policy alignment, specialty steel integration, and chemical process infrastructure growth. Under the Production Linked Incentive Scheme for Specialty Steel, active through 2026, the government has incentivized localized production of high-performance epoxy and polyester resins used in corrosion protection of advanced alloys. This policy linkage is reducing dependency on imported resin systems while strengthening domestic value chains for infrastructure, energy, and heavy engineering. Cost competitiveness has been further enhanced by the Ministry of Steel’s continuation of Basic Customs Duty exemptions on critical alloying inputs such as molybdenum and ferro-nickel until March 31, 2026, directly lowering production costs for resin-coated metallurgical assets.

Manufacturing scale-up is already visible. In 2025, AOC India expanded capacity at its Pune operations to support rising demand for corrosion-resistant fiberglass reinforced plastics in chemical processing zones, wastewater treatment facilities, and industrial storage systems. Sustainability frameworks are also influencing material selection. The Ministry of Steel’s 2025 Green Steel Roadmap has standardized the use of bio-based resin coatings for structural assets in coastal and high-humidity industrial corridors, positioning corrosion resistant resins as enablers of both durability and decarbonization.

China: High-Speed Rail, Offshore Wind, and Trade Protection

China continues to deploy corrosion resistant resins at scale across transportation and renewable energy infrastructure, while reinforcing domestic manufacturing through trade policy. Under the Ministry of Industry and Information Technology 2025–2026 industrial plan, advanced vinyl ester and epoxy resins have been prioritized for next-generation high-speed rail fleets to mitigate aerodynamic corrosion caused by sustained high-velocity operation. This application requires resin systems with exceptional chemical resistance, fatigue durability, and long-term adhesion under thermal cycling.

Renewable energy is a parallel growth engine. In mid-2025, INEOS Composites expanded localized resin production in China to supply offshore wind turbine blades, integrating bio-derived intermediates in line with national carbon neutrality objectives for 2060. Trade measures are shaping competitive dynamics. On January 2, 2025, Chinese authorities updated anti-dumping duties on select European and American resin precursors to protect domestic manufacturers such as Swancor, reinforcing local capacity development. These policies collectively position China as both a large-scale consumer and increasingly self-reliant producer of corrosion resistant resin systems.

Germany: Labor-Saving Resin Systems and Certified Bio-Circular Chemistry

Germany’s corrosion resistant resin industry is distinguished by advanced composite research, labor-efficiency gains, and rigorous sustainability certification. At JEC World 2025 in Paris, German-led research collaborations involving BASF SE and allnex unveiled a new generation of urethane acrylate resins that eliminate the need for surface sanding and priming. These systems reduce application labor requirements by roughly 20% while maintaining high corrosion protection performance, a critical advantage in Europe’s cost-sensitive industrial fabrication environment.

Traceability and circularity are becoming decisive procurement criteria. In late 2025, Hexion VAD B.V. and Polynt S.p.A. achieved ISCC PLUS certification across multiple European sites. This certification validates the use of bio-circular feedstocks in corrosion resistant resin production, supporting automotive, wind energy, and infrastructure customers seeking verified low-carbon material pathways. Germany’s emphasis on certified sustainability and application efficiency continues to set technical benchmarks for the broader European market.

Comparative Snapshot: Country-Level Strategic Direction in the Corrosion Resistant Resin Industry

Corrosion Resistant Resin Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Core Application Focus

|

Direction of Resin Innovation

|

|

United States

|

Re-shoring and defense procurement

|

EVs, naval composites, rail

|

PFAS-free, AI-designed, low-VOC resins

|

|

India

|

Industrial policy and FRP adoption

|

Chemical processing, steel

|

Localized, bio-based, cost-efficient systems

|

|

China

|

Infrastructure scale and trade protection

|

HSR, offshore wind

|

High-durability, bio-integrated composites

|

|

Germany

|

Labor efficiency and certification

|

Automotive, wind, infrastructure

|

Primer-free, ISCC-certified bio-circular resins

|

Corrosion Resistant Resin Market Report Scope

Corrosion Resistant Resin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17 Billion

|

|

Market Size (2034)

|

$29.2 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Resin Type (Epoxy Resins, Vinyl Ester Resins, Polyester Resins, Polyurethane Resins, Specialty Resins), By Technology (Solvent-Borne, Water-Borne, High-Solids and 100 Percent Solids, UV-Curable Resins), By Application Method (Composites, Coatings, Structural Adhesives and Putties), By End-Use Industry (Chemical Processing, Oil and Gas, Marine, Power Generation, Infrastructure and Construction, Automotive and Transportation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Olin Corporation, INEOS Composites, Hexion Inc., AOC Aliancys, Polynt-Reichhold Group, Ashland Global Holdings Inc., Huntsman International LLC, BASF SE, Scott Bader Company Ltd., Sino Polymer Co. Ltd., Swancor Holding Co. Ltd., Grasim Industries Limited, Allnex GmbH, Nan Ya Plastics Corporation, Resonac Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrosion Resistant Resin Market Segmentation

By Resin Type

- Epoxy Resins

- Vinyl Ester Resins

- Polyester Resins

- Polyurethane Resins

- Specialty Resins

By Technology

- Solvent-Borne

- Water-Borne

- High-Solids and 100% Solids

- UV-Curable Resins

By Application Method

- Composites

- Coatings

- Structural Adhesives and Putties

By End-Use Industry

- Chemical Processing

- Oil and Gas

- Marine

- Power Generation

- Infrastructure and Construction

- Automotive and Transportation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Corrosion Resistant Resin Industry

- Olin Corporation

- INEOS Composites

- Hexion Inc.

- AOC Aliancys

- Polynt-Reichhold Group

- Ashland Global Holdings Inc.

- Huntsman International LLC

- BASF SE

- Scott Bader Company Ltd.

- Sino Polymer Co. Ltd.

- Swancor Holding Co. Ltd.

- Grasim Industries Limited

- Allnex GmbH

- Nan Ya Plastics Corporation

- Resonac Corporation

*- List not Exhaustive