Corrosion Under Insulation (CUI) and Spray-on Insulation (SOI) Coatings Market Size, Asset Integrity Demand, and Thermal Protection Innovation

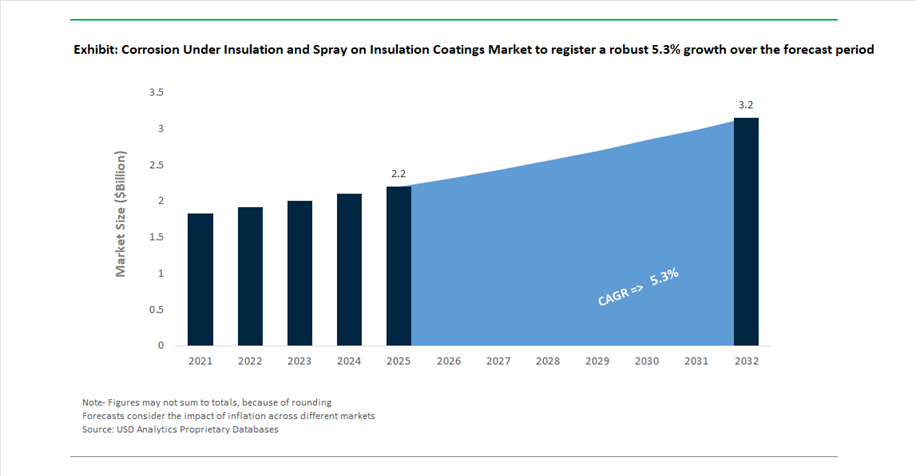

The global corrosion under insulation (CUI) and spray-on insulation (SOI) coatings market was valued at $2.2 billion in 2025 and is projected to grow at a CAGR of 5.3% between 2025 and 2032, reaching $3.2 billion by 2032. This growth is driven by increasing demand across oil & gas, petrochemicals, power generation, marine, and industrial processing sectors, where CUI remains one of the most critical and costly forms of asset degradation.

CUI occurs when moisture becomes trapped beneath insulation systems, leading to hidden corrosion, structural weakening, and unexpected equipment failure. As a result, industries are increasingly transitioning from traditional insulation systems to advanced coating-based solutions that provide both thermal insulation and corrosion protection. Spray-on insulation (SOI) coatings are gaining traction due to their ability to create seamless, monolithic barriers, eliminating joints and gaps where moisture ingress typically occurs.

A key market driver is the growing emphasis on asset lifecycle extension and predictive maintenance, particularly in aging infrastructure such as refineries, pipelines, storage tanks, and offshore platforms. Operators are investing in high-performance coatings that can be applied on hot substrates, resist extreme temperatures, and reduce maintenance downtime, thereby improving operational efficiency and safety.

Technological advancements are significantly enhancing product performance. Innovations in silicone-based hydrophobic coatings, epoxy phenolics, and hybrid polymer systems are enabling improved thermal insulation, water repellency, and chemical resistance. Additionally, the shift toward low-VOC, waterborne, and environmentally compliant coatings is aligning with stricter global regulations, particularly in North America and Europe.

High-Temperature Coating Breakthroughs, Monolithic Insulation Systems, and Integrated Protection Solutions Driving Market Evolution

The CUI and SOI coatings market is evolving through innovation in high-temperature performance, system-level integration, and cost-efficiency improvements. A notable advancement is Sherwin-Williams’ Heat-Flex® CUI coating (December 2025), which received the Materials Performance Corrosion Innovation Award. This technology addresses the closed-loop moisture cycle and can be applied on hot substrates up to 175°C, eliminating the need for equipment shutdown and significantly reducing operational downtime.

Spray-on insulation systems are redefining traditional insulation approaches. PPG’s launch of PITT-THERM® 909 (June 2025) introduces a silicone-based hydrophobic SOI coating capable of achieving up to 250 mil thickness in a single application, outperforming multi-layer conventional systems. Field trials demonstrated improved efficiency and faster installation, while PPG also reported 5% total cost of ownership savings, driven by reduced maintenance and elimination of moisture ingress points.

Performance validation in real-world environments is accelerating adoption. Hempel’s Malaysia case study (April 2025) demonstrated a 50% improvement in energy efficiency compared to traditional insulation systems, highlighting the dual functionality of modern coatings as both thermal barriers and corrosion-resistant layers. Similarly, Jotun’s C5VH-rated powder coatings are being adapted for SOI applications in extreme offshore and coastal environments, providing enhanced corrosion resistance alongside electrical insulation.

Strategic investments and regional innovation hubs are strengthening product development capabilities. Stahl’s reopening of its advanced coatings facility in Ranipet, India (December 2025) includes a dedicated R&D center focused on localized CUI and SOI solutions for the South Asian energy sector. Meanwhile, AkzoNobel’s €1.1 billion capital raise (March 2026) supports ongoing R&D into zero-VOC CUI primers and high-build sprayable thermal coatings, aligning with tightening environmental regulations.

Integrated system solutions are emerging as a key competitive differentiator. RPM International’s acquisition of Kalzip (April 2026) enables the combination of corrosion-resistant coatings with advanced aluminum cladding systems, creating multi-layer protection strategies for large-scale infrastructure. Additionally, Kansai Helios’ C5-class Remisol EB coatings (March 2026) are being leveraged for thin-film CUI protection in high-vibration environments, where traditional insulation systems may fail due to cracking or delamination.

API RP 571 (2024) CUI Risk Reclassification Forcing High-Performance Corrosion Under Insulation Coating Adoption

The CUI coatings market is undergoing a regulatory-led transformation following the 2024 update to API RP 571, which formally elevates corrosion under insulation (CUI) as a critical damage mechanism for carbon steel and low-alloy steel assets in refining and petrochemical environments. The revised framework explicitly identifies the 60°C to 175°C temperature range as the peak CUI risk window, where corrosion kinetics accelerate due to cyclic wet-dry exposure beneath insulation systems.

This reclassification is not theoretical. Integrated field data indicates that approximately 80% of piping leaks in petrochemical facilities are linked to CUI, with nearly 60% of these failures occurring where coating systems have exceeded their 10-year design life. This directly links asset integrity failures to coating degradation, forcing operators to prioritize high-performance CUI-resistant coating systems as the primary mitigation layer rather than relying on insulation alone.

Performance specifications under API-aligned inspection codes (API 510 and API 570) now demand significantly enhanced coating durability. CUI coatings must maintain dielectric strength above 500 V/mil after thermal cycling, ensuring electrical insulation and resistance to localized corrosion pathways. Additionally, coatings are required to pass 2,000+ hours of cyclic condensation testing with rust creepage below 2 mm, aligning laboratory validation with real-world exposure conditions.

Inspection mandates further intensify operational pressure. Facilities using legacy insulation systems must inspect 25% to 33% of insulated piping every five years using visual inspection or non-destructive testing methods. This creates a cost-intensive inspection cycle, incentivizing operators to adopt advanced anti-corrosion coatings that extend inspection intervals and reduce lifecycle maintenance expenditure.

The regulatory shift is driving accelerated adoption of high-build epoxy, phenolic, and advanced multipolymeric coatings engineered for long-term resistance to moisture ingress, thermal stress, and chemical exposure in high-risk temperature zones.

NACE SP0198-2024 Qualification Establishing Spray-On Insulation (SOI) as a Primary CUI Mitigation Technology

The release of NACE SP0198-2024 by AMPP marks a pivotal shift in the CUI and insulation coatings market by formally recognizing Spray-On Insulation (SOI) as a standalone corrosion mitigation system rather than a supplementary solution. This redefinition is supported by stringent qualification criteria that elevate SOI from a thermal insulation material to a dual-function corrosion protection and thermal barrier coating system.

A key requirement under the updated standard is adhesion integrity. SOI coatings must demonstrate a minimum pull-off adhesion strength of 3.5 MPa (500 psi) on abrasive-blasted steel surfaces, ensuring a seamless bond that eliminates interfacial voids where moisture accumulation typically initiates corrosion.

Thermal performance is equally critical. To qualify under SP0198, SOI systems must maintain a thermal conductivity of ≤0.07 W/m·K at 100°C, confirming their effectiveness as true insulation systems while maintaining protective coating functionality. This dual requirement is redefining material formulation strategies, particularly in polymer-ceramic hybrid coatings.

The introduction of cyclic CUI resistance testing further strengthens qualification rigor. SOI systems must withstand repeated cycles of boiling water immersion followed by dry heat at 150°C without blistering or delamination, simulating extreme operational conditions found in refining and offshore environments.

As of 2026, major EPC contractors are mandating SP0198 Type 3 or Type 4 certification for liquid-applied insulation systems used on complex geometries such as vessels, elbows, and flanges. This is accelerating the replacement of traditional insulation systems with advanced SOI coatings that offer both corrosion protection and thermal efficiency in a single application layer.

High-Temperature CUI Coatings Enabling Extended Asset Life in FCC and Petrochemical Units

The increasing severity of operating conditions in refinery units, particularly Fluid Catalytic Cracking (FCC) units and ethylene crackers, is driving demand for high-temperature corrosion protection coatings capable of withstanding extreme thermal exposure. Traditional epoxy systems are no longer sufficient in these environments, creating a shift toward Inert Multipolymeric Matrix (IMM) coatings and Novolac epoxy systems engineered for elevated temperature stability.

Next-generation high-temperature CUI coatings now demonstrate continuous operating stability in the 400°C to 540°C range, effectively bridging the performance gap between organic coatings and inorganic zinc systems. This enables corrosion protection in previously uncoatable high-temperature zones, expanding the addressable market for advanced coating technologies.

Thermal shock resistance is a critical differentiator. These coatings are engineered to withstand rapid temperature transitions, such as drops from 450°C to ambient conditions during emergency shutdowns, without micro-cracking. This prevents the formation of pathways for moisture ingress, which is a primary trigger for accelerated corrosion under insulation.

From an economic perspective, the adoption of IMM-based coatings significantly enhances maintenance efficiency. Operators report extension of maintenance cycles from approximately 3 years to over 10 years, reducing total cost of ownership by up to 45% when factoring in insulation removal, scaffolding, and downtime costs.

Application efficiency is also improving. Ultra-high solids formulations exceeding 95% solids content enable single-coat applications at thicknesses of 200 to 300 microns, reducing turnaround time during refinery shutdowns and improving project execution timelines.

Fluoropolymer-Based Spray-On Insulation Transforming Offshore Corrosion Protection

Offshore oil and gas platforms and floating production systems are among the most aggressive environments for corrosion, characterized by continuous salt spray, high humidity, and chloride-induced stress corrosion cracking risks. Fluoropolymer-based Spray-On Insulation (SOI) coatings are emerging as a high-performance solution that addresses both corrosion protection and thermal insulation in these conditions.

These advanced SOI systems exhibit near-zero chloride ion permeability, effectively preventing salt-laden moisture from reaching the steel substrate. This is particularly critical for stainless steel piping and topside equipment, where chloride exposure can lead to rapid stress corrosion cracking.

Weight reduction is a significant operational advantage. Replacing traditional insulation systems comprising cladding and mineral wool with high-build SOI coatings can reduce topside weight by up to 15 tons per project, improving structural efficiency and reducing load constraints on offshore platforms.

Personnel protection is another critical benefit. Fluoropolymer SOI coatings can reduce the surface temperature of pipes operating at 180°C to approximately 60°C with a coating thickness of just 5 to 8 mm, ensuring compliance with occupational safety standards while maintaining thermal efficiency.

The elimination of the annular gap between insulation and substrate represents a fundamental shift in CUI mitigation strategy. By bonding directly to the steel surface, SOI coatings remove the primary zone where moisture accumulates, with field audits indicating over 95% reduction in CUI occurrence rates compared to conventional insulation systems.

CUI Coatings Dominate Market with 62% Share Driven by Critical Asset Protection in Oil & Gas and Process Industries

Product Category Analysis: High-Performance CUI Coatings Lead with Advanced Epoxy and Polysiloxane Technologies

Corrosion Under Insulation (CUI) coatings account for a dominant 62.0% share of the CUI and spray-on insulation coatings market in 2025, driven by the urgent need to mitigate one of the most dangerous and costly corrosion mechanisms in industries such as oil & gas, petrochemicals, and power generation. CUI occurs when moisture becomes trapped beneath insulation, creating a highly corrosive environment that can lead to catastrophic equipment failure, leaks, fires, and regulatory penalties. To combat this, advanced coatings such as epoxy novolac, epoxy phenolic, polysiloxane, and thermal spray aluminum (TSA) are widely adopted due to their ability to withstand thermal cycling, moisture ingress, and chemical exposure. These coatings are tested under stringent standards like ISO 19277 and NACE TM0404, ensuring durability and long-term protection. The shift toward proactive asset integrity management and predictive maintenance strategies is further accelerating demand, solidifying CUI coatings as a critical segment in the global industrial protective coatings market.

Medium Temperature Range (100°C–300°C) Leads with 52% Share Driven by High CUI Risk in Industrial Systems

Temperature Performance Analysis: Epoxy Novolac Systems Dominate Critical Operating Range Applications

The medium temperature range (100°C–300°C) accounts for 52.0% of the CUI coatings market in 2025, as this range represents the highest risk zone for corrosion under insulation in carbon steel and stainless steel equipment. Within this temperature window, moisture is not fully evaporated, creating a persistent hot, humid environment that accelerates corrosion rates up to 0.5–1.0 mm per year, potentially leading to pipe failure within a decade. This temperature range is prevalent across industrial steam systems, refineries, power plants, district heating networks, and food processing facilities, driving widespread coating demand. The dominant technologies in this segment are epoxy novolac and epoxy phenolic coatings, applied at high film thicknesses (250–400 microns) to provide robust barrier protection against chloride ingress and thermal cycling. Additionally, specialized formulations are required for stainless steel applications to prevent stress corrosion cracking, reinforcing the importance of advanced coatings in this high-risk segment of the CUI coatings market.

Corrosion Under Insulation and Spray-on Insulation Coatings Market Competitive Landscape Driven by High-Heat Protection, Aerogel Insulation, and Lifecycle Durability

The corrosion under insulation (CUI) and spray-on insulation coatings market is driven by demand for high-temperature coatings, asset lifecycle extension, and energy efficiency. Key players compete through aerogel-based insulation, high-build coatings, and digital monitoring solutions across oil & gas, power, and industrial infrastructure sectors.

AkzoNobel Leads Aerogel-Based CUI Coatings with Passive Cooling and High-Speed Application

AkzoNobel N.V., through its International® brand, is advancing CUI coatings with its aerogel-based “Sunscreen” system, combining thermal insulation with radiative cooling for passive heat management. The company reported €10.15 billion in 2025 revenue, supported by €200 million in cost savings from its Industrial Excellence program. Its Intertherm® series remains a benchmark for high-temperature corrosion protection, now optimized for faster spray-on application, reducing turnaround time by 20%. AkzoNobel’s leadership in Personnel Protection Insulation coatings eliminates the need for traditional cladding, directly addressing root causes of CUI. The company raised €1.1 billion in 2026 to accelerate investments in sustainable insulation technologies. Its innovation and scale reinforce its dominance in high-performance CUI coatings.

PPG Expands Digital CUI Monitoring and High-Build Thermal Coatings for Energy Infrastructure

PPG Industries, Inc. is strengthening its position in CUI coatings with integrated solutions combining corrosion protection and thermal insulation for high-demand sectors such as data centers and oil & gas. Its HI-TEMP 1027HD coating delivers high-build protection of up to 12 mils in a single application, enhancing durability in extreme environments. The company reported $15.9 billion in 2025 sales, with strong growth in industrial coatings driven by high-temperature applications. PPG LINQ™ now incorporates CUI risk modeling, enabling predictive maintenance through digital twin technology. Its focus on advanced coatings and digital integration supports improved asset reliability. PPG’s innovation strategy aligns with evolving industrial insulation and corrosion protection needs.

Sherwin-Williams Dominates Thermal Insulative Coatings with Heat-Flex® High-Performance Systems

The Sherwin-Williams Company leads in spray-on insulation coatings through its Heat-Flex® portfolio, particularly Heat-Flex® 7000, which replaces traditional insulation across a wide temperature range from cryogenic to high heat. The company enhanced its formulations with micaceous iron oxide reinforcements to improve durability under thermal cycling and transport conditions. Its Bowling Green facility expansion doubled production capacity to meet rising demand in North America. Sherwin-Williams is targeting CX-rated extreme corrosion environments with advanced Heat-Flex® systems, ensuring superior long-term protection. Its integrated supply chain and technical expertise support large-scale industrial applications. The company’s focus on durability and performance strengthens its leadership in CUI mitigation coatings.

Hempel Advances Sustainable CUI Coatings with Long-Life Zinc Technology and Service Integration

Hempel A/S is positioning itself as a sustainability leader in CUI coatings, offering solutions that extend asset life beyond 35 years and reduce Scope 3 emissions. Its Versiline® CUI series combines high solids content with low VOC emissions, delivering strong resistance to thermal shock. The company deployed over 450 technical experts globally to conduct CUI condition surveys, transitioning toward a service-oriented model. Its Avantguard® technology enhances sub-insulation corrosion protection, offering double the durability of conventional coatings. Hempel’s focus on lifecycle performance and sustainability supports energy infrastructure projects. Its integrated service approach strengthens its competitive positioning.

Jotun Expands High-Performance CUI Coatings with EV and Offshore Energy Applications

Jotun A/S is advancing CUI coatings through innovations targeting both EV battery systems and offshore energy infrastructure. Its next-generation powder coatings provide combined thermal management and corrosion protection for high-voltage battery packs, preventing thermal runaway. The company secured key contracts in floating wind projects, supplying coatings for subsea and splash-zone applications. Jotun’s HPS 2.0 technology contributes to carbon reduction and is being adapted for industrial insulation efficiency. Its vertically integrated resin capabilities enable production of coatings meeting C5VH and CX standards for extreme environments. Strong presence in marine and industrial markets reinforces its global competitiveness. Jotun’s innovation supports high-performance insulation and corrosion protection solutions.

Carboline Strengthens Extreme-Temperature Coatings with Integrated Spray-On Insulation Systems

Carboline, part of RPM International Inc., leads in extreme-performance CUI coatings with its Thermaline series, capable of operating from cryogenic conditions up to 649°C. The company expanded its global industrial service centers to provide rapid technical support for critical infrastructure applications. Its Thermaline 450 EP epoxy-phenolic coating offers superior chemical resistance for pressurized vessels and wash-down environments. Carboline integrates spray-on insulation systems with fireproofing solutions, delivering single-source protection for refineries and offshore platforms. Backed by RPM’s strong financial performance, the company continues to invest in advanced coating technologies. Its focus on extreme durability and integrated solutions enhances its leadership in CUI coatings.

Saudi Arabia CUI & Spray-on Insulation Coatings Market: Mega Energy Projects and Smart Coatings Driving Global Leadership

Saudi Arabia is the global epicenter for corrosion under insulation (CUI) and spray-on insulation (SOI) coatings, driven by massive oil & gas investments under Vision 2030. The Jafurah unconventional gas field expansion (> $10 billion) is a major catalyst, requiring high-temperature-resistant CUI coatings for extensive pipeline infrastructure.

Technological innovation is accelerating rapidly. Saudi Aramco is piloting IoT-enabled intelligent coatings with embedded sensors to monitor moisture ingress and real-time corrosion beneath insulation—marking a shift toward predictive maintenance. Large-scale projects like the Tanajib Gas Plant (2025) are driving demand for silicone-based SOI coatings with superior thermal stability in desert climates. Additionally, the expansion of desalination plants along the Red Sea is boosting adoption of glass-flake reinforced CUI primers for high-salinity environments, while IKTVA incentives are encouraging local R&D in extreme-heat coating systems.

United States CUI & Spray-on Insulation Coatings Market: Regulatory Push and Hydrogen Infrastructure Driving Growth

The United States market is evolving through regulatory enforcement and infrastructure modernization. New EPA mandates for methane emissions reporting are accelerating the replacement of traditional insulation with spray-applied coatings that enable easier leak detection, particularly in oil & gas operations.

Federal investments under the Bipartisan Infrastructure Law (BIL) are also driving demand for cryogenic-resistant CUI coatings in emerging hydrogen hubs. Innovation is focused on sustainability, with the introduction of USDA-certified bio-based insulation coatings for green building retrofits. Updated ASTM G189-24 standards are standardizing performance benchmarking, while workforce training programs are addressing skill shortages in maintenance and repair. Offshore expansion in the Gulf of Mexico is further increasing demand for C5-M marine-grade epoxy systems, reinforcing the U.S. as a high-value innovation market.

China CUI & Spray-on Insulation Coatings Market: Green Standards and Hydrogen Expansion Driving Scale

China is rapidly transitioning toward eco-friendly and high-performance CUI coatings, driven by strict environmental regulations and energy transition goals. The upcoming GB 30981.1-2025 standard (effective 2026) is forcing a shift toward waterborne CUI primers, reducing VOC emissions across industrial applications.

Growth is strongly tied to energy infrastructure. Expansion of hydrogen storage facilities is driving demand for permeation-resistant internal linings, while mega-refinery projects such as Zhejiang Petrochemical are adopting nanoceramic SOI coatings that reduce thermal energy loss by ~15%. Urban redevelopment programs are also integrating solar-reflective coatings for insulated roofing systems. Additionally, China’s expansion of high-purity NMP capacity supports advanced PVDF-based coatings, reinforcing its global scale advantage.

India CUI & Spray-on Insulation Coatings Market: Infrastructure Boom and PLI Incentives Driving High Growth

India is emerging as a key growth hub for CUI and insulation coatings, supported by strong policy incentives and industrial expansion. The extension of the PLI Scheme 2.0 to specialty chemicals is targeting a 20% reduction in import dependence for advanced anticorrosive and thermal insulation resins.

Major infrastructure projects are driving demand. The HPCL Rajasthan Refinery (HRRL) alone is deploying over 2 million sq. meters of spray-applied insulation coatings for pipeline thermal management. Under the $1.4 trillion National Infrastructure Pipeline (NIP), new gas terminals are specifying fusion-bonded epoxy (FBE) and CUI-resistant coatings as standard. Additionally, expansion of Vande Bharat trains is increasing demand for FST-compliant insulation coatings, while renewable energy projects are driving adoption of ultra-high-temperature silicone coatings (up to 600°C). Emerging innovations such as self-healing coatings with micro-encapsulated inhibitors further highlight India’s growing technological capabilities.

Germany CUI & Spray-on Insulation Coatings Market: Hydrogen Infrastructure and Circular Chemistry Driving Sustainability

Germany remains the global benchmark for sustainable CUI coatings, driven by its energy transition and strict regulatory framework. The construction of the 9,700 km National Hydrogen Core Grid is a major demand driver, requiring permeation-resistant coatings to prevent hydrogen embrittlement in insulated pipelines.

Regulatory leadership is a key differentiator. Under REACH 2.0, Germany has already achieved a ~90% phase-out of PFAS-based additives, while Digital Product Passports (DPP) ensure full lifecycle transparency for coating materials. Innovation is also advancing through mass-balance bio-resins, reducing CO₂ intensity by ~40%. Additionally, offshore wind expansion is increasing demand for C5-H high-durability epoxy systems, reinforcing Germany’s leadership in eco-compliant, high-performance coatings.

Norway CUI & Spray-on Insulation Coatings Market: Offshore Exploration and Subsea Innovation Driving Advanced Applications

Norway is a leader in subsea and offshore CUI coating technologies, driven by strong exploration activity on the Norwegian Continental Shelf (NCS). With 21 new discoveries in 2025, demand is rising for high-build epoxy-phenolic coatings for insulated wellheads and pipelines.

Innovation is focused on reducing weight and improving efficiency. Projects like Omega Alfa are deploying aerogel-based insulation coatings, achieving up to 30% reduction in insulation bulk. Updated NORSOK M-501 standards are tightening performance requirements for thermal cycling resistance, ensuring durability in extreme conditions. Additionally, subsea pipeline rehabilitation is driving adoption of underwater-curable epoxy coatings, while carbon capture initiatives like Northern Lights are creating demand for CO₂-resistant coatings in insulated transport systems.

Corrosion Under Insulation and Spray on Insulation Coatings Market Report Scope

Corrosion Under Insulation and Spray on Insulation Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2032)

|

$3.2 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product Category (Corrosion Under Insulation (CUI) Coatings, Spray-on Insulation (SOI) Coatings), By Resin Chemistry (Epoxy, Polyurethane (PU), Silicone, Inorganic Zinc-Rich, Specialty Hybrids), By Technology (Solvent-borne Coatings, Water-borne Paint, Powder Coatings), By Temperature Range Performance (Low Temperature (<100°C), Medium Temperature (100°C–300°C), High Temperature (>300°C)), By End-Use Industry (Oil and Gas and Petrochemical, Energy and Power Generation, Marine, Industrial Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Jotun A/S, Hempel A/S, Carboline Company, Kansai Paint Co., Ltd., Mascoat, The Dow Chemical Company, Nippon Paint Holdings Co., Ltd., BASF SE, Seal For Life Industries, Temp-Coat Brand Products, LLC, Tnemec Company, Inc., Superior Products International II, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

CUI and SOI Coatings Market Segmentation

By Product Category

- Corrosion Under Insulation (CUI) Coatings

- Spray-on Insulation (SOI) Coatings

By Resin Chemistry

- Epoxy

- Polyurethane (PU)

- Silicone

- Inorganic Zinc-Rich

- Specialty Hybrids

By Technology

- Solvent-borne Coatings

- Water-borne Paint

- Powder Coatings

By Temperature Range Performance

- Low Temperature (<100°C)

- Medium Temperature (100°C–300°C)

- High Temperature (>300°C)

By End-Use Industry

- Oil and Gas and Petrochemical

- Energy and Power Generation

- Marine

- Industrial Manufacturing

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Corrosion Under Insulation and Spray on Insulation Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Jotun A/S

- Hempel A/S

- Carboline Company

- Kansai Paint Co., Ltd.

- Mascoat

- The Dow Chemical Company

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- Seal For Life Industries

- Temp-Coat Brand Products, LLC

- Tnemec Company, Inc.

- Superior Products International II, Inc.

*- List not Exhaustive