Decorative Coatings Market Size, Premium Aesthetic Demand, and Sustainable Paint Innovation

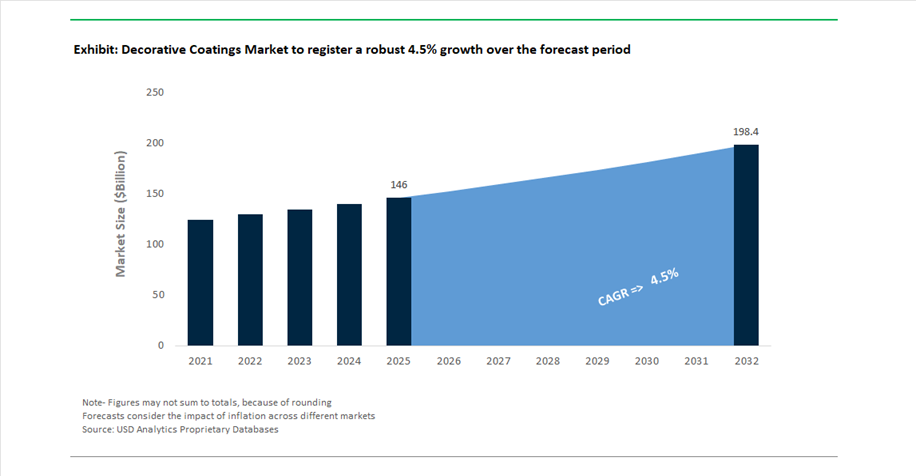

The global decorative coatings market was valued at $146 billion in 2025 and is projected to grow at a CAGR of 4.5% between 2025 and 2032, reaching $198.7 billion by 2032. This growth is driven by strong demand across residential housing, commercial interiors, infrastructure refurbishment, and real estate development, where decorative coatings play a central role in aesthetic enhancement, surface protection, and environmental performance.

A key growth driver is the increasing consumer and developer focus on premium finishes, personalized color palettes, and design-led coatings solutions. The market is witnessing a shift toward high-value decorative paints that offer enhanced durability, stain resistance, washability, and long-lasting color retention, particularly in urban and high-income segments. Additionally, the expansion of repainting cycles and renovation activities in mature markets is sustaining demand for interior and exterior decorative coatings.

Sustainability is becoming a defining factor in product development. Manufacturers are accelerating the adoption of low-VOC, waterborne, and eco-labeled paints, supported by certifications such as Environmental Product Declarations (EPDs) and green building standards. This transition is particularly significant in Europe and Asia-Pacific, where regulatory frameworks and consumer awareness are driving the uptake of environmentally responsible decorative coatings.

Technological advancements are also reshaping the market through the integration of digital color matching systems, AI-assisted design tools, and advanced pigment technologies. These innovations are enabling greater customization, faster product development cycles, and improved application efficiency, enhancing both professional and DIY user experiences.

Color Trend Innovation, Pricing Strategies, and Digital Transformation Shaping Market Dynamics

The decorative coatings market is being actively shaped by design-led innovation, pricing strategies, and digital transformation initiatives. A major trend driver is the launch of 2026 Color of the Year collections, which significantly influence global design preferences. PPG’s “Secret Safari” (October 2025) introduces a nature-inspired yellow-green tone, aligned with its “Parallels” theme, emphasizing botanical aesthetics across residential and commercial spaces. Similarly, Behr’s “Hidden Gem” (July 2025) reflects a shift toward grounded, smoky hues, while AkzoNobel’s “Rhythm of Blues” collection (September 2025) highlights indigo-based palettes that balance calmness with expressive design.

Pricing strategies are also playing a critical role in maintaining profitability amid raw material volatility. In March 2026, Asian Paints implemented a strategic price increase to offset rising input costs linked to crude oil fluctuations and supply chain disruptions. This move underscores the company’s strong pricing power in both urban and rural markets, enabling it to protect margins while sustaining market leadership in India.

Sustainability and certification-driven innovation are gaining traction across the market. Nippon Paint Thailand’s achievement of EPD International Certification (January 2026) enhances transparency for its water-based paints, supporting compliance with global green building standards such as LEED and BREEAM. Additionally, Asian Paints’ amalgamation of its polymers subsidiary (March 2026) strengthens vertical integration, improving control over resin and emulsion production, which are critical inputs for eco-friendly paint formulations.

Product innovation is addressing evolving performance and aesthetic requirements. Hempel’s Flat Eggshell finish (October 2025) combines low-sheen aesthetics with high durability, catering to commercial spaces requiring both visual appeal and long-term performance. Meanwhile, Nippon Paint’s Southeast Asia strategy (2024–2026) emphasizes expansion of computer color matching (CCM) networks and AI-assisted color selection tools, enhancing customer engagement and enabling faster decision-making for both professionals and consumers.

EU Ecolabel 2026 Criteria Forcing PFAS-Free Decorative Paint Formulations and Low-Emission Coating Technologies

The decorative coatings industry is entering a compliance-intensive phase following the implementation of Commission Decision (EU) 2025/2607, which fundamentally restructures formulation strategies across the European decorative paints market. The revised EU Ecolabel introduces a complete ban on PFAS substances, requiring manufacturers to demonstrate concentrations below 25 ppb across all raw materials, including surfactants and leveling agents. This eliminates a wide class of performance additives traditionally used to enhance flow, wetting, and stain resistance in premium decorative coatings.

This regulatory shift is compounded by stricter preservative controls. The updated framework mandates a 30% reduction in isothiazolinone-based biocides (MIT/BIT) compared to earlier criteria, directly impacting microbial stability strategies in waterborne paints. Manufacturers are now investing in alternative preservation technologies such as encapsulated biocides and pH-controlled systems to maintain shelf life without exceeding toxicity thresholds.

Titanium dioxide, a core pigment in architectural coatings, is also under enhanced scrutiny. To retain ecolabel certification, coatings containing TiO₂ must comply with dust suppression protocols during manufacturing and provide full life cycle assessment transparency, particularly regarding carbon footprint contributions. This is pushing suppliers toward low-carbon pigment sourcing and energy-efficient dispersion technologies.

Indoor air quality compliance is becoming more stringent with the introduction of SVOC emission limits. Decorative paints must now ensure emissions below 0.1 mg/m³ after 28 days, aligning with high-performance green building standards. Combined with existing VOC caps of 10 g/L for interior matt coatings, this creates a dual constraint environment where both immediate and long-term emissions must be optimized.

China GB 30981.1-2024 Standard Driving High-Purity and Transparent Decorative Paint Formulations

China’s GB 30981.1-2024 standard is redefining safety and performance benchmarks in the decorative coatings market by consolidating previously fragmented regulations into a unified, high-rigor compliance framework. This standard introduces mandatory limits on harmful substances across both wall and floor coatings, eliminating regulatory inconsistencies that previously allowed mid-tier products to bypass stricter controls.

A key advancement is the inclusion of Semi-Volatile Organic Compounds (SVOCs) within regulated emission categories. This aligns China’s domestic standards with global green certification frameworks, requiring manufacturers to control both short-term VOC emissions and long-term indoor air pollutants.

Transparency requirements are also significantly expanded. Decorative coatings must now disclose all biocides used in formulation, including compounds such as MIT and arsenic-based preservatives, directly on technical data sheets. This level of disclosure is transforming procurement decisions, particularly among professional contractors and institutional buyers who prioritize ingredient-level visibility.

The standard further tightens limits on formaldehyde and benzene-series compounds, requiring approximately 30% lower emission levels compared to previous benchmarks. This is driving rapid adoption of ultra-low emission binders, advanced coalescing agents, and solvent-free dispersion systems.

By consolidating seven legacy standards into a simplified regulatory structure, China is effectively eliminating compliance loopholes and accelerating market consolidation. High-performance, low-emission decorative coatings are becoming the baseline requirement for participation in large-scale construction and renovation projects.

Digital Tinting Systems and AI-Based Color Matching Transforming Decorative Paint Retail Economics

The decorative coatings market is undergoing a retail and distribution transformation driven by the adoption of digital tinting systems and AI-powered color matching technologies. The shift from pre-manufactured color inventories to on-demand tinting at the point of sale is redefining inventory management, customer experience, and operational efficiency.

Consumer and professional preferences are clearly aligned with customization. Surveys indicate that approximately 70% of homeowners and specifiers prioritize precise color matching, driving demand for systems capable of replicating colors from digital inputs such as photographs, fabrics, and architectural references. This is enabling retailers to deliver highly personalized solutions without maintaining extensive physical stock.

The integration of spectral AI technologies is significantly improving accuracy. Advanced color matching systems now achieve a Delta E (ΔE) value below 0.5, ensuring near-perfect color consistency across batches, which is critical for large commercial projects requiring uniform finishes.

Operational benefits are equally compelling. Digital tinting reduces material waste and obsolescence by 15% to 20%, while also decreasing back-end storage requirements by up to 40%. This allows retailers to optimize floor space, shifting toward higher-margin advisory services and professional-grade product offerings.

This transition represents a structural evolution in the decorative coatings value chain, where data-driven customization replaces mass inventory models, enhancing both profitability and customer satisfaction.

Functional Decorative Coatings Enabling Anti-Viral Protection and Indoor Air Quality Enhancement

The demand for functional decorative coatings is expanding rapidly, particularly in healthcare, education, and high-occupancy commercial environments where surface performance is directly linked to occupant health. Anti-viral and air-purifying paints are emerging as a high-growth segment within the decorative coatings market, driven by increasing awareness of indoor environmental quality.

Advanced photo-catalytic coatings are demonstrating the ability to inactivate 99.9% of viruses and bacteria within two hours of contact, transforming painted surfaces into active antimicrobial barriers. This capability is particularly valuable in hospitals, clinics, and public infrastructure where pathogen transmission risk is elevated.

Air purification functionality is also advancing. Modern decorative coatings incorporate mineral-based scavengers capable of neutralizing up to 75% of airborne formaldehyde over a multi-year period, significantly improving indoor air quality in sealed or energy-efficient buildings.

Additional performance attributes include rapid odor neutralization, with coatings achieving up to 50% reduction in VOC-related odors within 24 hours, enabling faster re-occupancy of treated spaces. This is particularly relevant for schools and commercial offices where downtime must be minimized.

Regulatory alignment is a critical factor in this segment. The market is shifting toward non-leaching antimicrobial technologies that comply with EPA and ECHA standards, ensuring that active agents remain bound within the coating matrix and do not contribute to environmental contamination.

Emulsion Paints Dominate Decorative Coatings Market with 54% Share Driven by Global Wall Paint Demand

Product Type Analysis: Water-Based Emulsion Coatings Lead with Versatility and Interior-Exterior Performance

Emulsion paints account for a dominant 54.0% share of the decorative coatings market in 2025, driven by their universal application across interior walls, ceilings, and exterior masonry surfaces. These water-based coatings, formulated using acrylic, styrene-acrylic, and vinyl acetate ethylene (VAE) binders, represent the bulk of global paint consumption due to the vast surface area of residential and commercial buildings. The segment is bifurcated into interior emulsions, which prioritize low odor, high scrub resistance, and premium matte finishes, and exterior emulsions, which deliver UV resistance, crack-bridging flexibility, and long-term durability (10–25 year warranties). A key innovation trend in 2025 is the rise of waterborne alkyd-acrylic hybrid emulsions, replacing solvent-based enamels by offering high gloss, smooth leveling, and non-yellowing performance. This convergence of performance, sustainability, and application ease reinforces emulsions as the cornerstone of the global decorative coatings market.

DIY Segment Leads Decorative Coatings Market with 54% Share Driven by Home Improvement Trends and Premium Paint Adoption

User Type Analysis: Homeowners Drive Volume Demand with Increasing Preference for Premium Finishes

The DIY (Do-It-Yourself) segment holds a leading 54.0% share of the decorative coatings market in 2025, driven by the massive global base of homeowners and renters engaged in self-applied painting projects. This segment dominates volume due to frequent interior repaint cycles (4–5 years), particularly influenced by ongoing hybrid work and home-centric lifestyles, which increase awareness of aesthetics and maintenance needs. DIY consumers are increasingly trading up to premium paint products, including “paint + primer in one” formulations and scrub-resistant matte finishes, which offer improved durability and ease of application. A critical enabler of this segment is the in-store tinting ecosystem, allowing consumers to customize colors from thousands of shades using advanced color-matching systems. Additionally, marketing strategies such as “Color of the Year” campaigns and curated palettes are driving premium paint sales. These dynamics position the DIY segment as the primary volume engine in the global decorative paints market.

Decorative Coatings Market Competitive Landscape Driven by Low-VOC Innovation, Regional Expansion, and Contractor-Centric Distribution

The decorative coatings market is highly competitive, driven by low-VOC formulations, color innovation, and strong contractor distribution networks. Leading players focus on sustainability, regional expansion, and digital color tools to capture demand across residential, commercial, and renovation segments globally.

Sherwin-Williams Strengthens Decorative Coatings Leadership with Latin America Expansion and Wellness-Focused Innovation

The Sherwin-Williams Company reported $23.57 billion in 2025 sales and projects steady growth into 2026, supported by strong performance in its Paint Stores Group. The integration of Suvinil added $164.5 million in Q4 2025, strengthening its Latin American decorative coatings footprint. Its 2026 Colormix® Forecast introduces ultra-low-VOC acrylic coatings aligned with wellness-centric interior design trends. The company’s 5,000+ store network enables a direct-to-contractor model, ensuring pricing control and supply chain efficiency. Sherwin-Williams continues to generate strong cash flows, returning $2.4 billion to shareholders. Its scale, innovation, and distribution dominance reinforce its leadership in decorative coatings.

AkzoNobel Drives Profitability with Bio-Based Coatings and Strategic Mega-Merger

AkzoNobel N.V. is advancing its position in decorative coatings through a proposed merger with Axalta, creating a $17 billion global coatings leader. Despite a 5% revenue decline in 2025, operating profit surged 27% due to cost optimization under its Industrial Excellence program. The company is investing in bio-attributed resin systems to reduce carbon footprint across architectural coatings. Its €1.1 billion bond issuance supports energy transition and capacity upgrades across global manufacturing sites. AkzoNobel maintains strong market share in EMEA and China through a price-over-volume strategy. Its focus on sustainability and profitability strengthens its competitive edge in decorative coatings.

PPG Repositions Decorative Coatings Portfolio with Digital Color Platforms and Emerging Market Growth

PPG Industries, Inc. has strategically exited its North American architectural coatings business, focusing on high-margin decorative coatings in EMEA and Latin America. The company reported record Q1 2026 adjusted EPS of $1.83, with 3% organic growth in remaining decorative segments. Its 2026 Color of the Year “Secret Safari” integrates with the PPG LINQ™ platform, enabling AI-driven color matching and reducing material waste by 15%. PPG continues to expand in Asia-Pacific, which accounted for over 46% of global decorative coatings demand. Its Colorful Communities initiative strengthens brand visibility in urban development projects. The company’s digital integration and regional strategy enhance its competitive positioning.

Nippon Paint Expands Global Decorative Coatings with Asset Assembler Strategy and Strong APAC Growth

Nippon Paint Holdings (NIPSEA Group) is projecting ¥1.92 trillion in revenue for 2026, driven by its asset assembler M&A model and strong regional execution. The acquisition of AOC strengthens its position in specialty resins and adjacent markets such as ETICS systems. Its NIPSEA segment achieved robust growth, supported by demand in China and Southeast Asia. Nippon Paint’s decentralized structure allows regional brands to operate independently, improving responsiveness and market penetration. The company is targeting a 14.7% operating margin through disciplined execution and acquisitions. Its expansion strategy reinforces its leadership in decorative coatings across Asia-Pacific.

Asian Paints Strengthens Market Leadership with Home Décor Expansion and High ROCE

Asian Paints Limited dominates the Indian decorative coatings market with strong share and financial performance. The company is executing a ₹10,000 crore CAPEX plan to expand manufacturing and backward integration. Its Beautiful Homes retail network is rapidly growing, aiming to contribute up to 10% of total revenue by 2026. Asian Paints’ SmartCare segment has achieved a 25% CAGR, diversifying into waterproofing and construction chemicals. The company maintains a strong balance sheet with high ROCE above 30%, supporting future investments. Its integrated approach strengthens its leadership in decorative coatings and adjacent markets.

Masco (Behr) Focuses on R&R Market with One-Coat Technologies and Sustainable Manufacturing

Masco Corporation’s Behr Paint generated $7.6 billion in 2025 sales, with nearly 90% of revenue driven by the repair and remodel segment. Its BEHR DYNASTY® line leads in DIY and pro-sumer markets, supported by an exclusive partnership with The Home Depot. The introduction of “Smoky Jade” with high-hide pigments enables one-coat application, reducing labor costs for contractors. The company is targeting margin expansion in 2026 through operational efficiency improvements. Sustainability initiatives include increased recycled packaging and a transition to renewable energy in manufacturing. Masco’s focus on value-driven coatings and R&R demand strengthens its competitive position.

India Decorative Coatings Market: Capacity Shock and Urbanization Driving Structural Transformation

India is the most dynamic market for decorative coatings, undergoing a major structural shift due to capacity expansion and urban demand. The launch of Birla Opus (Grasim Industries, 2025) added 1,332 million liters of capacity, increasing national production by ~40% and intensifying competition in premium residential and commercial segments.

Government-driven housing demand is a major catalyst. The PMAY-U 2.0 program is channeling billions into affordable housing, boosting demand for durable exterior emulsions (5–7 year lifecycle). Infrastructure initiatives such as the Amrit Bharat Station Scheme (1,300+ stations) are driving demand for anti-carbonation and high-traffic coatings. Additionally, regulatory pressure is accelerating sustainability, with waterborne coatings exceeding 75% share in Tier-1 cities and strict Zero-Liquid-Discharge (ZLD) mandates enforcing cleaner production. Smart city investments (~$130 billion) are also driving adoption of photocatalytic self-cleaning coatings in polluted urban zones.

China Decorative Coatings Market: Green Standards and Repainting Economy Driving High-Value Shift

China’s decorative coatings market is transitioning from volume to value-driven growth, despite a slowdown in new construction. The implementation of GB 30981.1-2025 (effective 2026) is phasing out high-VOC solvent coatings in favor of ultra-low VOC waterborne systems.

A key structural shift is the “repainting economy”, with leading companies allocating up to 70% of marketing budgets toward maintenance and refurbishment in Tier 1–3 cities. Regulatory updates under GB 4806.10-2025 are expanding approved materials while enforcing strict safety thresholds. Additionally, China’s push toward Building-Integrated Photovoltaics (BIPV) is driving demand for transparent conductive coatings in commercial facades. Expansion of high-purity NMP capacity (+35% in 2025) is further supporting advanced resin systems for high-performance coatings.

United States Decorative Coatings Market: Federal Stimulus and AI Customization Driving Premiumization

The United States market is evolving through federal funding and digital transformation. Investments under the Infrastructure Investment and Jobs Act (IIJA) are driving adoption of cool-roof coatings in public infrastructure to mitigate urban heat islands.

Technological innovation is a major differentiator. The deployment of AI-enabled color-matching kiosks (15,000+ locations) allows contractors to achieve 99.9% accuracy in custom shades, transforming project workflows. Regulatory shifts under TSCA are accelerating a 22% increase in bio-based solvent adoption, while the semiconductor boom is creating niche demand for ESD and chemical-resistant coatings in cleanrooms. Additionally, antimicrobial coatings are now specified in ~85% of new healthcare and education projects, reinforcing premiumization trends.

Germany Decorative Coatings Market: Anti-Greenwashing Regulation and Bio-Circular Innovation Leading Sustainability

Germany remains the global benchmark for sustainable decorative coatings, driven by strict environmental policies and transparency requirements. The Anti-Greenwashing Bill (2025) mandates third-party verification of all sustainability claims, eliminating unverified “eco-friendly” labeling.

The industry has achieved a ~90% phase-out of PFAS-based surfactants, while scaling mass-balance bio-resins that reduce CO₂ emissions by up to 50%. Germany is also pioneering Digital Product Passports (DPP), enabling full lifecycle traceability of coatings. Technological advancements such as IR and UV-LED curing systems are reducing energy consumption by ~22%, while R&D into hydrogen infrastructure coatings is opening new application areas.

Vietnam Decorative Coatings Market: FDI, Green Certification, and Housing Expansion Driving High Growth

Vietnam is emerging as a high-growth market for decorative coatings, supported by FDI inflows and large-scale housing development. Government targets to build 100,000 social housing units (2025–2026) are driving demand for weather-resistant exterior coatings.

Sustainability is a key trend. Regulations such as QCVN 19:2024/BTNMT are enforcing strict VOC limits, while over 400 projects (~10 million m²) have achieved LEED or Green Mark certification, mandating low-emission coatings. Hospitality and tourism investments—such as large resort developments—are driving demand for premium finishes, while waterborne coatings already dominate with ~78% market share. These factors position Vietnam as a major emerging hub.

Brazil Decorative Coatings Market: Industrial Expansion and Agribusiness Synergy Driving Demand

Brazil’s decorative coatings market is supported by strong industrial investment and housing demand. WEG’s R$70 million (2025) investment is expanding liquid paint production capacity by 70%, strengthening regional supply chains.

Agriculture is a major indirect driver. Record harvests have increased demand for ZM-coated steel in grain storage infrastructure, boosting protective and decorative coating consumption. Government housing programs such as Minha Casa Minha Vida continue to drive high-volume demand for decorative emulsions, while new building codes mandate liquid-applied PU waterproofing systems for commercial rooftops. Additionally, Brazil is advancing bio-based polyurethane coatings derived from castor oil, reinforcing its sustainability positioning.

Japan Decorative Coatings Market: Disaster-Resistant Formulations and Healthcare Innovation Driving Niche Leadership

Japan’s decorative coatings market is shaped by seismic resilience and aging population needs, leading to highly specialized innovations. Reconstruction following the 2024 Noto earthquake (80,000+ homes) has driven demand for flexible, crack-bridging coatings.

Regulatory updates now mandate elastic coatings for commercial buildings in seismic zones, ensuring structural durability. Innovation is also strong in healthcare applications, with zwitterionic polymer coatings preventing bacterial adhesion in hospitals. Additionally, Japan is a pioneer in photocatalytic self-cleaning coatings, widely used in high-rise buildings. Government subsidies have shifted demand toward retrofitting (≈65% of market volume), reinforcing Japan’s focus on upgrading existing infrastructure.

Decorative Coatings Market Report Scope

Decorative Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$146 Billion

|

|

Market Size (2032)

|

$198.7 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Resin Type (Acrylic, Alkyd, Vinyl, Polyurethane, Epoxy, Polyester, Others), By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, UV-Cured Coatings), By Product Type (Emulsions, Enamels, Primers and Undercoats, Wood Coatings, Specialty Coatings), By Coating (Interior Coatings, Exterior Coatings), By End-Use Sector (Residential, Non-Residential), By User Type (Professional, DIY), By Color and Aesthetic Type (White, Colored, Special Effects)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Kansai Paint Co., Ltd., Jotun A/S, RPM International Inc., Masco Corporation, Berger Paints India Limited, Hempel A/S, Benjamin Moore & Co., DAW SE, Tikkurila Oyj, Diamond Vogel

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Decorative Coatings Market Segmentation

By Resin Type

- Acrylic

- Alkyd

- Vinyl

- Polyurethane

- Epoxy

- Polyester

- Others

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- UV-Cured Coatings

By Product Type

- Emulsions

- Enamels

- Primers and Undercoats

- Wood Coatings

- Specialty Coatings

By Coating

- Interior Coatings

- Exterior Coatings

- Facades

- Roofs

- Fences and Railings

By End-Use Sector

- Residential

- Non-Residential

By User Type

By Color and Aesthetic Type

- White

- Colored

- Special Effects

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Decorative Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Jotun A/S

- RPM International Inc.

- Masco Corporation

- Berger Paints India Limited

- Hempel A/S

- Benjamin Moore & Co.

- DAW SE

- Tikkurila Oyj

- Diamond Vogel

*- List not Exhaustive