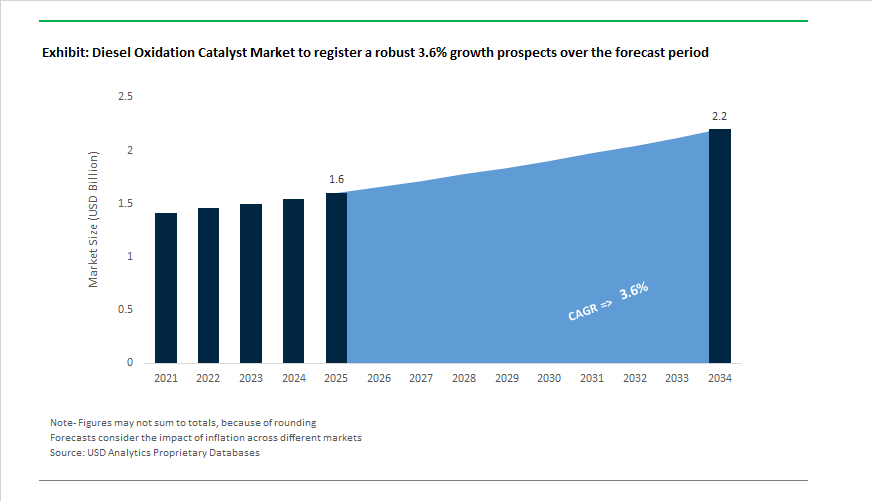

Diesel Oxidation Catalyst Market to Reach $2.2 Billion by 2034 at 3.6% CAGR Driven by Retrofit Mandates and PGM Optimization

The Diesel Oxidation Catalyst (DOC) Market is projected to grow from $1.6 billion in 2025 to $2.2 billion by 2034, expanding at a CAGR of 3.6%. Growth is supported by tightening emission regulations, retrofit demand for stationary diesel engines, and ongoing optimization of platinum group metal (PGM) loading in automotive aftertreatment systems. DOC systems remain a core component in diesel emission control architectures, enabling the oxidation of carbon monoxide (CO), unburned hydrocarbons (HC), and soluble organic fractions before downstream diesel particulate filters (DPFs) and selective catalytic reduction (SCR) units. Regulatory enforcement between 2024 and 2028 has strengthened compliance requirements for both on-road and non-road diesel engines, sustaining baseline demand despite accelerating electrification in passenger vehicles.

Regulatory catalysts intensified in 2024, when the U.S. EPA finalized a mandate requiring industrial and stationary diesel plants to reduce carbon monoxide emissions by 35% by 2028. This directive immediately stimulated retrofit orders for large-scale DOC systems across power generation, oilfield services, and construction fleets during 2025 and into 2026. In July 2024, Umicore Shokubai Japan received Nissan’s Global Innovation Award for a catalyst coating breakthrough that reduces platinum, palladium, and rhodium loading while maintaining high oxidation efficiency. Lower PGM intensity is strategically critical as precious metal price volatility continues to pressure OEM margins. In December 2024, Clariant introduced its EcoTox oxidation catalysts tailored for biogas and renewable diesel applications, demonstrating a 15% conversion efficiency improvement in German pilot installations. This development reflects the shift toward low-carbon fuels that present unique impurity profiles requiring enhanced oxidation stability.

Industry consolidation accelerated in 2025 and early 2026. In May 2025, Honeywell signed a definitive agreement to acquire Johnson Matthey’s Catalyst Technologies business, with completion expected in the first half of 2026. The transaction integrates advanced catalyst intellectual property into Honeywell’s energy transition portfolio while allowing Johnson Matthey to focus on PGM services. In September 2025, Technip Energies agreed to acquire Ecovyst’s advanced materials and catalysts business for $556 million, strengthening vertical integration between process engineering and emission-control catalyst supply. Electrified aftertreatment solutions gained traction as Vitesco Technologies scaled its EMICAT electric-heated catalysts in 2025, enabling rapid light-off performance for 48-volt hybrid diesel vans during cold-start cycles. Recycling capacity also expanded in February 2025, when Elemental Econrg opened a 130-ton PGM recovery facility in Maharashtra, India, targeting platinum and palladium extraction from spent DOCs and DPFs. Technological innovation continued in December 2025, with BASF launching its X3D 3D-printed catalyst technology and constructing a Ludwigshafen production unit scheduled for 2026 startup, improving reactor flow dynamics and reducing pressure drop. BASF further announced a Global Digital Hub in Hyderabad in Q1 2026 to accelerate AI-driven catalyst formulation modeling. Meanwhile, FORVIA advanced 60% of its EU-FORWARD restructuring by October 2025, reinforcing competitiveness in DOC and SCR housing systems amid sustained internal combustion engine demand. Concurrently, ICL Group’s pivot toward zinc-bromine flow batteries in November 2025 signals selective capital reallocation within the broader catalytic materials ecosystem, though stationary and hybrid diesel platforms continue to anchor medium-term DOC demand.

Trends and Opportunities in the Global Diesel Oxidation Catalyst (DOC) Market

Cold-Start Optimization and Fast-SCR NO₂ Management Under Euro 7

- Tightened Euro 7 emission standards are forcing DOCs to deliver rapid light-off and precise NO₂ generation under sub-200°C exhaust conditions. Regulatory targets such as a 35% NOx reduction for light commercial vehicles and tailpipe limits approaching 0.02 g/km are redefining DOC design priorities. Peer-reviewed research published in August 2025 confirms that maintaining a DOC-controlled NO₂ to NOx ratio close to 0.5 enables Fast-SCR reactions that proceed up to ten times faster than conventional SCR pathways at low temperatures. This chemistry is critical during urban driving cycles where exhaust heat is insufficient for traditional catalyst activation.

- To address delayed catalyst activation, OEMs and tier-one suppliers are integrating electrically heated catalysts directly upstream or within the DOC substrate. Technical evaluations released in December 2025 show that pulsed electrical heating strategies can improve carbon monoxide conversion by 34% and total hydrocarbon oxidation by 31% during cold-start events. By reducing light-off time from minutes to seconds, DOC-EHC integration ensures that the full aftertreatment chain reaches operational efficiency almost immediately after ignition, a requirement for compliance in real-driving emissions testing.

Enhanced Resistance to Poisoning from Biodiesel and Low-Ash Lubricants

- The rapid global adoption of renewable diesel and biodiesel blends above B20 is introducing new durability challenges for DOC systems. Alkali metals, phosphorus, calcium, and zinc originating from bio-feedstocks and CK-4 engine oils accelerate catalyst deactivation and raise light-off temperatures. Findings presented at the 2024 SAE World Congress demonstrate that while B20 behaves similarly to ultra-low sulfur diesel, B100 can increase DOC light-off temperatures by up to 100°C due to higher boiling fractions and altered exhaust composition.

- As a result, catalyst developers are moving toward zone-coated washcoat architectures that spatially separate poison-trapping layers from precious metal group active sites. High-surface-area aluminas and modified ceria-zirconia systems are being deployed to immobilize calcium, zinc, and potassium before they reach platinum and palladium domains. Durability testing published in September 2025 indicates that conventional DOCs can lose up to 46% of CO conversion efficiency within 60,000 kilometers on biodiesel-powered engines. This has accelerated the shift toward silver-based formulations and ceria-zirconia promoted catalysts that retain activity under chemically aggressive exhaust environments.

Hybrid Diesel-Electric Powertrains and Non-Road Stage V Expansion

- Hybrid diesel-electric architectures and stricter off-road emission frameworks are creating a new operating envelope for DOCs characterized by frequent thermal cycling and prolonged low-temperature exposure. Engine-off intervals in hybrids allow catalyst temperatures to fall below light-off thresholds, undermining passive regeneration strategies. In response, system integrators such as Forvia and Tenneco are commercializing compact aftertreatment modules that combine DOC and DPF functions within a single substrate. This configuration lowers thermal mass and preserves exothermic heat generation during transient operation.

- Parallel momentum is building in the non-road segment. The California Air Resources Board is advancing Tier 5 standards aimed at further reducing NOx and particulate emissions from construction, mining, and agricultural equipment. This regulatory leap is driving demand for Stage V-compliant DOCs capable of sustaining up to 95% hydrocarbon and CO conversion efficiency under intermittent duty cycles and high-sulfur fuel exposure common in emerging markets. Advanced PGM alloying strategies are becoming a key differentiator in this segment.

Methane and Hydrogen Oxidation for Alternative Fuel Engines

- The expansion of natural gas and hydrogen-assisted combustion is opening a premium niche for oxidation catalysts beyond conventional diesel applications. Methane slip from lean-burn CNG and LNG engines represents a significant climate challenge, as unoxidized methane has a global warming potential far exceeding that of CO2. Through July 2025, the ARPA-E AMPLIFY program has allocated more than $3.2 million to the development of hydrothermally stable methane oxidation catalysts targeting 99.5% methane conversion efficiency under lean conditions.

- Simultaneously, hydrogen-diesel dual-fuel engines are gaining attention as transitional decarbonization solutions. Technical papers presented by SAE International in September 2025 show that hydrogen enrichment can reduce CO2 and NOx emissions by over 55% and 60% respectively. However, these systems introduce new challenges, including unburned hydrogen slip and altered particulate profiles that can rise by up to 77% at high hydrogen substitution rates. This is creating demand for next-generation DOCs capable of managing hydrogen oxidation while maintaining control over ultrafine particulate formation, positioning advanced oxidation catalysts as critical enablers of multi-fuel heavy-duty platforms.

Diesel Oxidation Catalyst (DOC) Market Share and Segmentation Insights

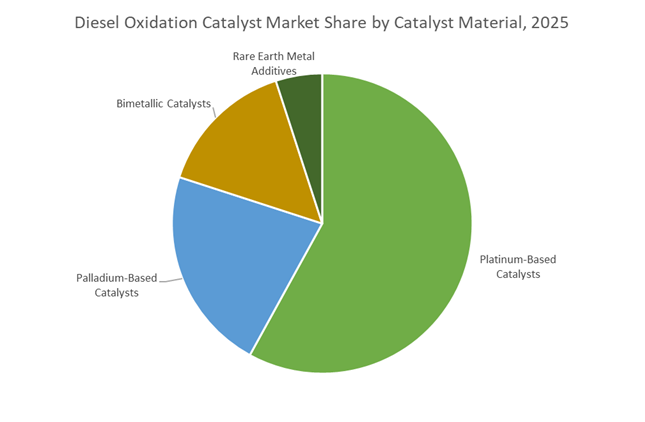

Market Share by Catalyst Material : Platinum Systems Lead as Bimetallic Formulations Optimize Cost and Performance

Platinum-based catalysts command 58% of the global DOC market in 2025, reflecting platinum’s superior low-temperature activity for carbon monoxide (CO) and hydrocarbon (HC) oxidation, which is critical during cold-start operation in diesel engines. Its durability and resistance to sulfur poisoning make platinum the benchmark material for compliance with Euro VI, China VI, and upcoming EPA 2027 emission standards. Palladium-based catalysts are gaining traction as OEMs pursue partial platinum substitution to manage precious metal costs, particularly in applications with controlled sulfur levels. Bimetallic platinum–palladium systems represent a fast-adopted compromise, delivering balanced light-off performance, thermal stability, and cost efficiency in modern exhaust aftertreatment architectures. Rare earth metal additives, primarily cerium and zirconium oxides, account for a smaller share by value but play a critical enabling role by providing oxygen storage capacity and enhancing catalyst durability, supporting long-term DOC performance under high-temperature diesel operating conditions.

Market Share by Application : On-Road Vehicles Dominate as Off-Road Regulations Tighten

On-road vehicles account for 65% of DOC demand, driven by mandatory installation across heavy-duty trucks, buses, and light commercial vehicles to meet stringent global emission regulations. DOCs are foundational to diesel aftertreatment systems, enabling passive diesel particulate filter (DPF) regeneration while reducing CO and unburned hydrocarbons. Off-road equipment represents a rapidly expanding segment as Tier 4 Final and Stage V standards extend DOC adoption into construction machinery, agricultural tractors, mining equipment, locomotives, and marine engines. Industrial and power generation applications form a steady niche, covering stationary diesel generators and backup power systems where air quality permitting increasingly requires oxidation catalysts. Growth across all segments is reinforced by tightening regional emissions legislation, fleet modernization, and rising demand for integrated DOC–DPF–SCR exhaust systems to achieve compliance while maintaining fuel efficiency.

Competitive Landscape of the Diesel Oxidation Catalyst (DOC) Market

The Diesel Oxidation Catalyst market is dominated by vertically integrated emission-control leaders and system integrators supplying advanced DOC solutions for heavy-duty trucks, off-highway equipment, mining engines, and BS-VI / Euro VI compliant vehicles, driven by tightening global emission regulations and circular PGM recovery models.

Johnson Matthey leads heavy-duty DOC innovation with ActivDPF™ and PGM circularity

Johnson Matthey remains the benchmark player in diesel oxidation catalysts, holding an estimated 25–30% global heavy-duty DOC market share in 2026. Following divestment of non-core health and battery units, JM sharpened its focus on Catalyst Technologies and PGM Services to accelerate margin-led growth. Its 2026 launch of ActivDPF™, integrating advanced DOC coatings with self-regenerating particulate filtration, targets stationary engines and off-road mining fleets. A core competitive edge lies in JM’s unrivaled platinum group metals recycling, insulating OEMs from platinum and palladium price volatility. This vertical PGM integration, combined with deep autocat heritage, positions Johnson Matthey as the global pioneer in low-temperature light-off DOC systems.

BASF ECMS strengthens circular DOC supply for BS-VI and cold-start emission control

BASF Environmental Catalyst and Metal Solutions operates a powerful full-loop DOC model, combining catalyst manufacturing with precious metal recovery. During 2025–2026, BASF scaled its Verdium digital platform, enabling OEMs to track carbon reductions achieved through recycled PGMs. Expansion of its Chennai facility in late 2025 reinforced BASF’s leadership in India’s fast-growing BS-VI heavy-duty diesel segment. Its DOC formulations are engineered for low-temperature light-off, addressing cold-start emissions in stop-start hybrid diesel platforms. BASF’s strategic focus on circularity allows recovery of up to 90% of precious metals from spent catalysts, lowering total ownership cost while supporting decarbonization goals across North America and Europe.

Umicore pioneers low-PGM DOC architectures with FlexMetal nanostructures

Umicore stands apart as the only 2026 DOC supplier offering a true closed-loop ecosystem, spanning catalyst design, substrate precursor production, and advanced PGM refining. Its FlexMetal DOC platform, launched in 2026, achieves equivalent oxidation efficiency with 15% lower precious metal loading, directly improving OEM economics. Umicore’s DOCs are optimized for precise NO-to-NO₂ conversion, maximizing downstream SCR efficiency for near-zero tailpipe emissions. Operating 16 plants across 13 countries with 9 technology centers, Umicore supports global vehicle platforms from Volvo to Mercedes-Benz. This materials-science-driven approach makes Umicore a cornerstone of the clean mobility DOC market.

Tenneco delivers integrated clean-air DOC systems for retrofit and OEM platforms

Tenneco’s Clean Air division differentiates through complete aftertreatment system integration, supplying not just DOC bricks but full thermal-managed assemblies. After acquisition by Apollo Global, Tenneco India secured a major 2026 Japanese OEM contract for SUV platforms, while expanding retrofit DOC programs for municipal buses and commercial trucks meeting Low Emission Zone mandates. Its Southeast Asia operations now act as an export hub for high-spec DOC systems serving the Middle East. A key advantage lies in Tenneco’s thermal management expertise, embedding insulation and heating elements to guarantee catalyst activation in extreme cold climates, strengthening its leadership in fleet modernization projects.

Corning anchors the DOC substrate market with ultra-thin ceramic honeycombs

Corning provides the critical ceramic backbone of the Diesel Oxidation Catalyst through its Celcor® cordierite and silicon carbide substrates, delivering high cell density and massive catalytic surface area. In 2026, Corning intensified investments in EPA Tier 4 Final off-highway engines, supplying construction and agricultural equipment OEMs. Its latest ultra-thin wall substrates reduce exhaust backpressure, directly improving fuel efficiency and engine output. The global automotive DOC carrier market, led by Corning, is projected to reach approximately USD 800 million by end-2026, underlining Corning’s strategic role as the material science foundation of next-generation diesel emission systems.

Cummins Emission Solutions integrates DOCs into compact Single Module™ platforms

Cummins Emission Solutions leverages direct engine integration to deliver DOCs precisely tuned to combustion dynamics. Its 2025–2026 Single Module™ aftertreatment system combines DOC, DPF, and SCR into a unit 40% lighter and 60% smaller, simplifying OEM packaging. These DOCs feature embedded IoT sensors for real-time catalyst health and soot monitoring, supporting predictive maintenance. Under Cummins’ Destination Zero strategy, DOC platforms also act as transitional technologies for hydrogen-combustion and hybrid-diesel engines. This deep digital and mechanical integration gives Cummins a unique advantage in ultra-low emission powertrain architectures.

European Union (Germany & Belgium): Euro 7 as a Structural Reset for DOC Engineering

The European Union is entering a decisive redesign cycle for diesel oxidation catalysts as Regulation (EU) 2024/1257 moves from policy to execution. With Euro 7 compliance for new M1 and N1 vehicle types mandated from November 29, 2026, catalyst suppliers across Germany and Belgium are prioritizing cold-start efficiency as a primary engineering constraint. The regulatory emphasis on reducing emissions in the first seconds after ignition is pushing DOC substrate architectures toward lower thermal mass, higher oxygen storage efficiency, and optimized precious metal dispersion. This shift has direct implications for palladium utilization strategies, washcoat formulation, and monolith geometry across European OEM supply chains.

A second and more structural change under Euro 7 is the durability mandate. For the first time, diesel oxidation catalysts must maintain functional performance for up to 200,000 kilometers or ten years. This requirement is reshaping cost curves and procurement decisions, as OEMs increasingly favor catalysts with higher upfront material quality to reduce lifetime compliance risk. In early 2025, Umicore confirmed it is scaling complex catalyst systems designed to withstand long-term thermal aging and sulfur exposure, particularly for mixed urban and highway duty cycles. At the corporate level, portfolio concentration is accelerating. In May 2025, Johnson Matthey announced the sale of its Catalyst Technologies business to Honeywell, enabling Johnson Matthey to redeploy capital exclusively into automotive clean air catalysts and PGM services. Parallel to road transport, Europe is also signaling future DOC demand in non-automotive applications. The December 2025 launch of the world’s first dynamic green ammonia plant by Topsoe, Vestas, and Skovgaard Energy highlights how sustainable chemical precursors may influence next-generation industrial and maritime oxidation catalyst systems.

United States: Flex-Module Integration and Regulatory Asymmetry

In the United States, the diesel oxidation catalyst market is being shaped by a combination of tightening heavy-duty standards and a more fluid light-duty regulatory environment. The EPA’s finalized Greenhouse Gas Emissions Standards for Heavy-Duty Vehicles Phase 3 will apply to model years 2027–2032, prompting OEMs to accelerate aftertreatment innovation as early as 2025. A defining response has been the development of compact, modular exhaust systems where DOCs are co-designed with diesel particulate filters to reduce packaging space while maintaining oxidation efficiency. These Flex Module architectures are particularly critical for vocational trucks and off-highway equipment, where under-bonnet space is constrained.

Technological signaling from OEMs underscores this shift. At Agritechnica 2025, Cummins Inc. showcased its 4.5 Structural Engine with an integrated Flex Module™ aftertreatment system, featuring a DOC optimized for passive regeneration and low-maintenance agricultural use. In the light-duty segment, the full enforcement of Tier 3 Bin 30 targets by early 2025 has increased demand for DOCs with ultra-fast light-off characteristics, pushing suppliers toward thinner substrates and advanced PGM anchoring technologies. At the policy level, regulatory asymmetry is emerging. While certain greenhouse gas standards are under reconsideration, the EPA continues strict enforcement against aftermarket defeat devices under the Clean Air Act. This has preserved the integrity of the catalyst replacement and retrofit market, sustaining steady baseline demand for certified diesel oxidation catalysts despite broader regulatory uncertainty.

India: BS7 Preparation and Industrial Emissions Convergence

India’s diesel oxidation catalyst landscape is entering a transition phase as policymakers prepare for Bharat Stage 7 emission norms targeted for implementation in 2026–27. The proposed BS7 framework introduces On-Board Monitoring for real-time tracking of NOx, ammonia, and particulate matter, significantly raising the functional expectations placed on DOCs in both passenger and commercial vehicles. Unlike previous step changes, BS7 places stronger emphasis on in-use performance rather than laboratory compliance alone, increasing the value of oxidation catalysts with stable conversion efficiency across diverse fuel qualities and operating conditions.

Beyond transport, industrial demand is becoming an increasingly important driver. In October 2025, the Ministry of Environment, Forest and Climate Change notified emission intensity reduction targets under the Carbon Credit Trading Scheme, requiring up to a 40% reduction for 2025–26 across energy-intensive sectors. This policy has expanded the role of oxidation catalysts in refineries and petrochemical plants, where they are deployed for VOC and CO abatement. Public sector refiners such as Indian Oil Corporation Limited and Bharat Petroleum Corporation Limited have initiated large-scale green transformation programs in 2025, upgrading secondary processing units with advanced catalyst recovery and emissions control systems. As a result, India’s DOC market is increasingly characterized by convergence between automotive and industrial oxidation catalyst demand, improving scale economics for domestic suppliers.

China: China 7 Drafting and Heavy-Duty Recovery

China’s diesel oxidation catalyst market is entering its next regulatory cycle following the nationwide implementation of China VIb. In late 2025, the Ministry of Ecology and Environment began drafting China 7 standards, which are widely expected to align closely with Euro 7. Early policy signals point to a strong focus on cold-start emissions, particularly in urban driving conditions, elevating the importance of high-palladium-loaded DOCs with rapid activation profiles. This anticipated shift is already influencing R&D priorities among domestic and international catalyst suppliers operating in China.

Market fundamentals are also improving. In 2025, Umicore indicated expectations of approximately 10% growth in China’s heavy-duty diesel truck segment through 2028, driven by logistics recovery and fleet modernization. This rebound is supporting renewed investment in more complex aftertreatment systems combining DOCs with SCR and DPF technologies. On the manufacturing side, environmental compliance is tightening beyond tailpipe emissions. The release of mandatory standards GB 30981.1-2025 by the State Administration for Market Regulation in May 2025 limits harmful substances in industrial coatings, indirectly increasing compliance costs for catalyst housing and coating facilities. As a result, China’s DOC industry is evolving toward higher regulatory sophistication, with emissions control extending across both product performance and manufacturing footprint.

Comparative Overview: Diesel Oxidation Catalyst Market by Region

Diesel Oxidation Catalyst Market Country Level Snapshot

|

Region

|

Primary Regulatory Trigger

|

Core Market Response

|

Structural Implication

|

|

EU (Germany, Belgium)

|

Euro 7 durability and cold-start limits

|

High-stability, low thermal mass DOCs

|

Higher material quality, longer lifecycle focus

|

|

United States

|

EPA Phase 3 heavy-duty standards

|

Modular DOC-DPF integration

|

Compact systems, aftermarket stability

|

|

India

|

BS7 and industrial emission targets

|

OBM-compatible and industrial DOCs

|

Convergence of auto and refinery demand

|

|

China

|

China 7 preparation

|

High-palladium, fast light-off DOCs

|

Complex aftertreatment adoption

|

Diesel Oxidation Catalyst (DOC) Market Report Scope

Diesel Oxidation Catalyst Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$2.2 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Catalyst Material (Platinum-Based Catalysts, Palladium-Based Catalysts, Bimetallic Catalysts, Rare Earth Metal Additives), By Substrate Material (Ceramic Substrates, Metallic Substrates, Flow-Through Monoliths), By Application (On-Road Vehicles, Off-Road Equipment, Industrial and Power Applications), By Sales Channel (Original Equipment Manufacturers, Aftermarket), By Functionality (Carbon Monoxide and Hydrocarbon Oxidation, Particulate Matter Reduction, Nitrogen Dioxide Management)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Johnson Matthey Plc, Umicore SA, BASF SE, Corning Incorporated, NGK Insulators, Ltd., Cummins Inc., Faurecia SE, Tenneco Inc., Heraeus Holding GmbH, Bosal International, Eberspächer Group, Katcon Global, CDTI Advanced Materials, SinterCast AB, Clariant AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diesel Oxidation Catalyst Market Segmentation

By Catalyst Material

- Platinum-Based Catalysts

- Palladium-Based Catalysts

- Bimetallic Catalysts

- Rare Earth Metal Additives

By Substrate Material

- Ceramic Substrates

- Metallic Substrates

- Flow-Through Monoliths

By Application

- On-Road Vehicles

- Off-Road Equipment

- Industrial and Power Applications

By Sales Channel

- Original Equipment Manufacturers

- Aftermarket

By Functionality

- Carbon Monoxide and Hydrocarbon Oxidation

- Particulate Matter Reduction

- Nitrogen Dioxide Management

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diesel Oxidation Catalyst Industry

- Johnson Matthey Plc

- Umicore SA

- BASF SE

- Corning Incorporated

- NGK Insulators, Ltd.

- Cummins Inc.

- Faurecia SE

- Tenneco Inc.

- Heraeus Holding GmbH

- Bosal International

- Eberspächer Group

- Katcon Global

- CDTI Advanced Materials

- SinterCast AB

- Clariant AG

*- List not Exhaustive