Digitally Printed Wallpaper Market to Reach $234.1 Billion by 2034 at 22.9% CAGR Driven by 3D Textures, Latex Inks and On-Demand Decor

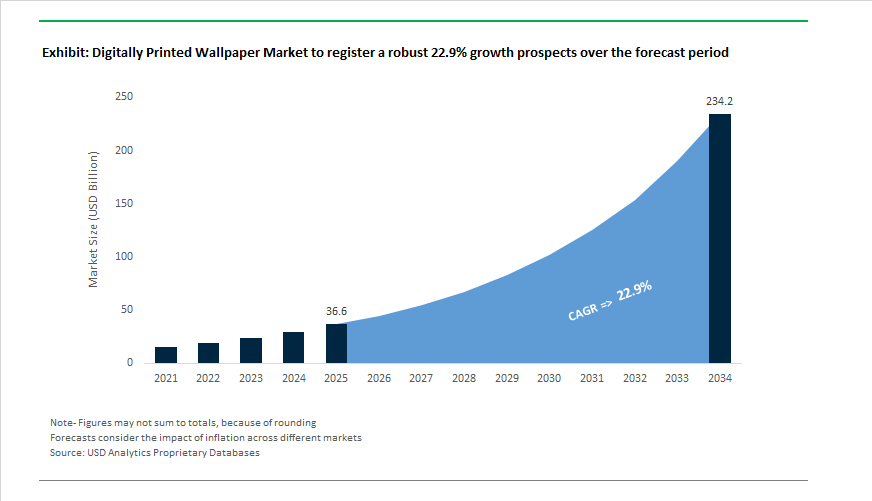

The Digitally Printed Wallpaper Market is projected to expand from $36.6 billion in 2025 to $234.1 billion by 2034, registering an exceptional CAGR of 22.9%. This accelerated growth trajectory is underpinned by rapid adoption of UV-curable inks, latex-based waterborne inks, dye-sublimation textile systems, and advanced pigment technologies tailored for residential, hospitality, healthcare, and commercial interiors. The shift from analog gravure wallpaper printing toward digital inkjet platforms is redefining production economics through short-run customization, print-on-demand wallpaper manufacturing, and sustainable, low-VOC wallcovering solutions.

In March 2024, HP Inc. introduced the HP Latex 630 series, engineered specifically for signage and interior décor applications. The fourth-generation water-based latex inks contain 60% water and emit zero VOCs, addressing stringent indoor air quality requirements in schools and hospitals. The 630W configuration integrates white ink capability, enabling high-opacity printing on colored and textured wallpaper substrates, expanding design flexibility for layered décor applications. In May 2024, Canon India launched the imagePROGRAF GP and PRO series with 7-color and 12-color configurations utilizing LUCIA PRO II pigment inks. These systems deliver enhanced scratch resistance and archival-grade durability, with interior longevity claims approaching 200 years, positioning digital wallpaper murals within the premium residential décor segment.

In July 2024, Xeikon expanded its approved wallpaper media portfolio through collaboration with Kernow Coatings, validating PVC-free and non-woven substrates compliant with fire-safety and environmental standards for high-traffic commercial wallcoverings. During December 2024, the DIMENSE solution, owned by Roland DG, won the BDNY Inspire Award for Best Wallcoverings, accelerating adoption of digitally embossed 3D-textured wallpapers for the 2025–2026 hospitality design cycle. Roland DG’s acquisition of DG DIMENSE through 2024 and 2025 enabled integration of simultaneous color and structural printing in a single pass via the DIMENSE DA-640 platform, transforming wallpaper from flat mural surfaces into tactile architectural finishes such as plaster and woven textile effects.

Technology upgrades intensified in January 2025 when Canon introduced the high-speed imagePROGRAF TZ-5320 and TX series, incorporating enhanced magenta ink channels for saturated reds and automated roll loading to support 24/7 wallpaper production lines. In April 2025, Mimaki launched ELS and ELH UV-curable inks with GREENGUARD Gold certification, meeting residential and office indoor air emission standards while delivering durability for textured wallcoverings. In May 2025, Mimaki introduced the JV200-160 roll-to-roll printer, targeting entry-level décor entrepreneurs and online wallpaper boutiques with cost-efficient, high-resolution aqueous output.

By August 2025, Durst Group unveiled its Open Software Initiative under the Smart Factory Portfolio, enabling wallpaper manufacturers to integrate UV, Latex, and aqueous printers from multiple vendors into a unified automated workflow. In October 2025, Durst debuted the P5 500 TEX iSUB in North America, leveraging integrated inline fixation and Subliflix dye-sublimation inks for seamless 5-meter textile wallcoverings and acoustic panels.

Market data in Q3 2025 identified Epson as the global leader in inkjet unit volume, reflecting accelerating penetration of PrecisionCore-based systems in print-on-demand wallpaper studios. The convergence of white-ink latex platforms, UV-texture hybrid systems, dye-sub textile wallpaper solutions, expanded substrate validation, and smart factory software integration is fundamentally reshaping the digital wallcoverings ecosystem toward high-margin customization, sustainability compliance, and industrial-scale automation.

Trends and Opportunities Reshaping the Digitally Printed Wallpaper Market

DTC Expansion Enabled by Web-to-Print Automation and AI Personalization

- The rise of Web-to-Print platforms has fundamentally altered distribution dynamics in the digitally printed wallpaper market. Direct-to-consumer sales models now allow homeowners, interior designers, and small contractors to bypass wholesalers and access fully customized wallpapers with zero minimum order quantities. In late 2024 and 2025, Etsy reported that the Home and Living category generated USD 12.6 billion in gross merchandise sales, underscoring strong consumer appetite for personalized décor products. A significant share of this growth is being captured by print-on-demand wall murals that can be produced and shipped within days, eliminating inventory risk for sellers.

- Artificial intelligence is amplifying this shift. By mid-2025, leading digital wallpaper manufacturers had deployed B2B portals with consumer-grade user experiences that integrate AI-powered room visualization and augmented reality previews. These tools allow customers to see custom designs rendered at true scale within their own rooms before purchase. Industry data indicates that such visualization capabilities have lifted online conversion rates by as much as 88 %, transforming wallpaper from a high-consideration purchase into a confident, data-driven decision. For manufacturers, this translates into higher order values, lower return rates, and deeper customer engagement.

Functional Coatings Drive Adoption in Healthcare and High-Traffic Commercial Spaces

- Beyond aesthetics, digitally printed wallpaper is increasingly specified as a functional surface in environments where durability, hygiene, and regulatory compliance are critical. Healthcare and hospitality sectors are leading adopters, driven by heightened awareness of infection control and material performance. Following warnings on antimicrobial resistance highlighted in 2025 reports by the World Health Organization, hospitals and clinics are specifying digitally printed wallpapers with integrated antibacterial and antiviral coatings. These products are engineered to withstand frequent chemical cleaning while maintaining color integrity and surface stability.

- Fire safety and indoor air quality standards are also shaping material selection. Advanced digital print platforms such as the HP Latex 830W, introduced during 2024 and 2025, rely on water-based inks that meet UL GREENGUARD Gold and UL ECOLOGO certifications. These systems enable the production of wallcoverings that comply with Class A fire ratings, a mandatory requirement for hotels, airports, and large commercial refurbishments. As a result, digital wallpaper is increasingly positioned as a compliant architectural finish rather than a decorative afterthought.

Large-Format Seamless Murals for Retail and Hospitality Branding

- Large-format digital printing is unlocking a major growth opportunity in architectural branding. Industrial-scale printers introduced in late 2025, such as the Canon Colorado XL-series, enable seamless mural production at widths exceeding 10 feet with consistent color density and surface uniformity. Using UVgel technology, these platforms deliver high-resolution output without banding, making them suitable for flagship retail stores and experiential hospitality environments.

- European print service providers have demonstrated that seamless digital murals can replace multiple joined panels, reducing installation time and visual disruption. Hospitality groups are leveraging this capability to create immersive brand narratives within lobbies, corridors, and common areas. Market feedback indicates that such environments increase dwell time and guest engagement, positioning digitally printed wallpaper as a strategic branding asset rather than a passive interior element.

Acceleration of Sustainable, PVC-Free, and Circular Wallpaper Solutions

- Sustainability is becoming a primary purchase criterion in the digitally printed wallpaper market. Under the 2025 EU Green Deal and green building frameworks such as LEED and BREEAM, demand is rising for PVC-free substrates and low-emission wallcoverings. Manufacturers are shifting toward non-woven paper, natural fiber materials such as jute and grasscloth, and bio-based polymer backings, all printed with 100% water-based aqueous inks to ensure superior indoor air quality.

- The on-demand nature of digital printing reinforces circular economy principles. Unlike traditional analog wallpaper production, which relies on large batch runs and warehousing, digital workflows support print-only-what-you-sell models. In 2025, companies including Ricoh and HP announced initiatives to incorporate recycled plastics and ocean-bound resins into printer hardware and consumables. Combined with reduced overproduction, these efforts have the potential to cut global wallpaper manufacturing waste by thousands of tons annually as the industry moves away from inventory-heavy legacy models.

Digitally Printed Wallpaper Market Share and Segmentation Insights

Digitally Printed Wallpaper Market Share by Printing Technology : Inkjet Printing Drives Mass Customization and Photo-Realistic Interiors

Inkjet printing dominates the digitally printed wallpaper market in 2025 with 82% share, cementing its position as the core production technology for custom wall décor and digitally printed wall coverings. Inkjet’s non-contact printing capability enables vibrant color reproduction, seamless pattern repeats, and photo-realistic imagery across vinyl, non-woven, textile, and specialty substrates. This flexibility supports both short-run bespoke wallpaper and large-scale commercial production, making inkjet indispensable for interior designers, hospitality projects, and residential personalization trends. The technology’s compatibility with UV, latex, and water-based inks further strengthens adoption amid rising demand for eco-friendly wallpaper printing and low-VOC interior solutions. In contrast, electrophotography retains only a niche presence, primarily in standardized commercial applications requiring fast turnaround. However, its limited color gamut, narrower substrate compatibility, and visible seam constraints restrict scalability, positioning inkjet printing as the clear growth engine for mass customization, digital décor innovation, and premium architectural surface design.

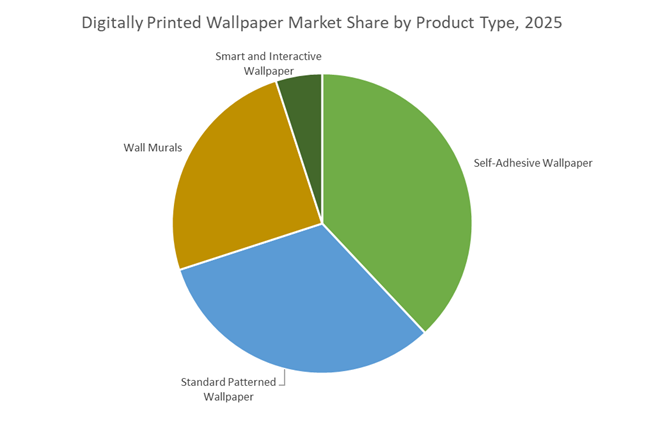

Digitally Printed Wallpaper Market Share by Product Type : Peel-and-Stick Leads as Murals and Smart Walls Gain Momentum

Self-adhesive wallpaper captures the largest share at 38%, emerging as the fastest-growing product category in the digitally printed wallpaper market. Driven by DIY home décor trends, rental-friendly interiors, and demand for removable wall coverings, peel-and-stick formats benefit directly from digital printing’s ability to deliver short-run custom designs with minimal waste. Standard patterned wallpaper continues to hold a strong position in residential and commercial interiors, revitalized by digital workflows that eliminate inventory constraints while enabling expansive pattern libraries and color variations. Wall murals represent a substantial segment, leveraging large-format inkjet printing to deliver custom-sized, continuous visuals for feature walls in hospitality, retail, and corporate spaces. Meanwhile, smart and interactive wallpaper remains an early-stage niche, integrating conductive inks, LEDs, and sensors for responsive architectural surfaces. Though small today, this segment signals future convergence between interior design technology and digitally printed smart environments.

Competitive Landscape of the Digitally Printed Wallpaper Market

The Digitally Printed Wallpaper Market in 2026 is shaped by rapid adoption of print-on-demand wallcoverings, VOC-free digital inks, AR-based visualization, and customized murals across residential and contract interiors. Leading players are competing on speed-to-design, sustainable substrates, bespoke production, and digital POD infrastructure, addressing strong demand from hospitality, DIY renovation, healthcare, and architect-led commercial projects.

A.S. Création Tapeten AG accelerates fast-fashion digital wallcoverings across Europe

A.S. Création Tapeten AG holds a top-3 global position in digitally printed wallpapers with roughly 6% market share, driven by its fast-fashion production model and deep digital integration. In late 2025, the company launched DESIGNDROP, an automated B2B portal enabling architects to upload vector artwork and receive digital proofs within 24 hours. Its Metropolitan Stories range leverages digital printing to replicate hyper-realistic textures such as concrete, rusted metal, and reclaimed wood. Strategically, A.S. Création is transitioning toward water-based, VOC-free inks to align with 2026 EU Green Deal indoor air quality standards. Its in-house Architects Paper digital center focuses exclusively on premium customized contract projects for hotels and offices.

Graham & Brown builds a digital-first DTC wallpaper ecosystem with AR visualization

Graham & Brown has reinvented itself as a digital-native, direct-to-consumer wallpaper brand, with nearly 100% of new launches now produced digitally, dramatically reducing print-run waste and carbon emissions. For 2026, the company unveiled Divine Damson and Eternal Weave as its Color and Design of the Year, showcasing intricate embroidery effects only achievable through digital printing. A key innovation is its AR-enabled mobile app, allowing customers to preview bespoke murals in real room dimensions before purchase. The brand’s storytelling strength is highlighted by the 2026 Eternal City mural, using hand-painted digital scans inspired by Jaipur architecture to deliver exceptional color depth and personalization at scale.

Bersham Group dominates North American POD wallpapers with Brewster and York

Following the Brewster Home Fashions and York Wallcoverings merger, The Bersham Group commands the North American residential segment through a robust print-on-demand supply chain anchored by a massive Randolph, Massachusetts warehouse, supported by facilities in the UK and China for 48-hour digital POD delivery. Its FloorPops and WallPops lines now include digitally printed peel-and-stick vinyl, targeting the booming renter-friendly DIY market in 2026. York Wallcoverings operates the widest printing technology mix in the US, spanning surface, gravure, and wide-format digital presses. Strategically, Bersham is digitally remastering York’s historic archive dating back to 1895 into large-scale contemporary murals.

Grandeco Wallfashion expands mural-led growth with eco digital collections

Grandeco Wallfashion Group is a key force in the digital mural sub-segment, serving youth-driven and contemporary residential demand across more than 80 countries. Its 2025–2026 Mural Young Edition XL introduced oversized digitally printed panels designed for simple “one-roll-one-wall” installation. In 2026, Grandeco partnered with Roomblush to launch ecological digital wallcoverings using non-woven substrates and sustainable inks for nurseries. A core differentiator is its Atmosphere Collection Integration, where murals are color-matched to solid wallpapers for seamless accent-wall design. Grandeco products also meet ASTM E84 Type I fire ratings, establishing the company as a benchmark for digital durability and safety.

Koroseal leads contract-grade digital wallcoverings for healthcare and hospitality

Koroseal Interior Products specializes in high-traffic commercial digital wallcoverings, supplying hospitality, corporate, and healthcare interiors with antimicrobial and protective wall systems. In 2026, Koroseal partnered with digital ink innovators to introduce 3D Sol-Gel inks, creating embossed textures without mechanical rollers. Its Digital Lab enables designers to customize everything from substrate selection (vinyl, wood veneer, silk) to pattern scale, supporting fully bespoke interiors. Growth in 2026 is centered on the healthcare sector, where digitally printed biophilic nature scenes are increasingly used to improve patient recovery environments. Koroseal’s strength lies in contract-grade performance combined with designer-level personalization.

United States: D2C Personalization, DIY Economics, and Substrate Transition

The United States digitally printed wallpaper market in 2025–2026 is being reshaped by direct-to-consumer personalization and cost-conscious renovation behavior. Print-on-demand platforms expanded North American fulfillment in 2025 with AI-driven room visualization that renders murals in true scale and lighting, cutting return rates by an estimated 18%. This shift materially improves unit economics for short-run production and favors digital inkjet over analog gravure. Technology suppliers reinforced sustainability credentials as HP Inc. completed the rollout of Eco-Carton ink cartridges across its high-volume latex fleet in late 2025, reducing plastic usage by roughly 80% and aligning with hospitality sector LEED requirements.

Demand is increasingly DIY-led. U.S. housing data indicate that 73% of millennials identify as DIY enthusiasts, accelerating adoption of removable peel-and-stick formats. Major retailers such as Home Depot and Lowe’s doubled their digital mural assortments ahead of the 2026 spring season. With installation labor averaging $567 per room in 2025, manufacturers introduced smart-seam alignment markers to simplify hanging for non-professionals. Regulatory pressure is reinforcing material innovation. Updated 2026 indoor air quality standards from the U.S. EPA are pushing rapid substitution toward PVC-free non-woven and paper substrates that eliminate phthalates and heavy metals traditionally associated with vinyl.

China: Subsidized Capacity, Speed-to-Market, and Clustered Upgrading

China is consolidating its role as a global hub for short-run and customized wallpaper exports through policy-backed digitization. The National Data Administration’s Digital China 2025 Action Plan introduced targeted subsidies for SMEs adopting high-definition digital presses, compressing payback cycles and accelerating capacity additions. Technology launches at China Print 2025 underscored the pace of innovation. HP Indigo demonstrated AI-powered color management on the Indigo 120K HD and 18K HD platforms, achieving 99% accuracy in reproducing complex textures and gradients that are critical for premium wallpaper aesthetics.

Throughput gains are shortening lead times. Komori introduced a 29-inch sheetfed UV inkjet press in June 2025 delivering 6,000 sheets per hour, enabling medium-lot custom jobs to move from weeks to days. Industrial upgrading under the Made in China 2025 framework has further concentrated capabilities. Local governments in Fujian and Jiangsu established Smart Printing Clusters offering tax incentives for Variable Data Printing, which supports serialized and limited-edition designs. This cluster strategy is improving consistency, lowering scrap rates, and enhancing China’s competitiveness in export-oriented digital wallpaper.

Germany: Automation, Green Compliance, and Premium Customization

Germany’s digitally printed wallpaper market is defined by automation and regulatory alignment that favor premium, high-margin customization. At Heimtextil 2025, Canon partnered with Fotoba to showcase the UVgel Wallpaper Factory, a modular line that converts jumbo rolls into finished wallpaper without manual intervention. The solution targets a 15% uplift in operational uptime and materially reduces labor dependency, a key constraint for European converters.

Sustainability mandates are accelerating ink and substrate shifts. Producers such as A.S. Création Tapeten AG transitioned 40% of digital lines to water-based and bio-derived inks in late 2025, aligning with EU Green Deal objectives and upcoming 2026 French Mineral Oil and PPWR rules. Consumer preferences reinforce this trajectory. A 2025 homeowner survey showed 60% favor customized designs, supporting the growth of boutique e-commerce printers in Berlin and Munich that deploy Xeikon 3500 series presses for seamless, endless-pattern murals with rapid turnaround.

United Kingdom: Hospitality-Led Demand and Interactive Surfaces

In the United Kingdom, digitally printed wallpaper demand is anchored in hospitality modernization and functional differentiation. Boutique hotels invested more than £120 million in refurbishments during 2025, increasingly selecting digital wallpaper for brand storytelling. UV coatings and digital embossing are being used to emulate premium fabrics at lower installed cost and faster timelines, making digital wallpaper a strategic alternative to traditional wallcoverings in hotels and serviced apartments.

Material selection is shifting decisively toward non-woven substrates. UK trade data point to record non-woven volumes in 2026 due to breathability advantages that mitigate mold risks in older housing stock, a decisive factor for suppliers like Graham & Brown. Retail innovation is extending beyond décor. UK brands are embedding dynamic QR codes and NFC chips into digitally printed walls, enabling interactive retail experiences where consumers unlock AR content or product videos directly from the surface. This convergence of media and interiors is creating a new value layer for digital wallpaper producers.

Comparative Snapshot: Digitally Printed Wallpaper Market by Country

Digitally Printed Wallpaper Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Technology or Policy Catalyst

|

Market Impact

|

|

United States

|

DIY renovation and D2C

|

AI visualization, PVC-free rules

|

Rapid growth in peel-and-stick and non-woven

|

|

China

|

Export-oriented customization

|

Digital China subsidies, VDP clusters

|

Faster lead times and scale in short runs

|

|

Germany

|

Premium automation

|

UVgel factories, EU Green Deal

|

High-margin customized production

|

|

United Kingdom

|

Hospitality and interactivity

|

Non-woven adoption, NFC integration

|

Functional and experiential wallpaper

|

Digitally Printed Wallpaper Market Report Scope

Digitally Printed Wallpaper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$36.6 Billion

|

|

Market Size (2034)

|

$234.1 Billion

|

|

Market Growth Rate

|

22.9%

|

|

Segments

|

By Printing Technology (Inkjet Printing, Electrophotography), By Substrate Type (Non-Woven Materials, Vinyl, Paper, Fabric and Textile), By End-Use Sector (Residential, Commercial, Hospitality), By Product Type (Wall Murals, Standard Patterned Wallpaper, Self-Adhesive Wallpaper, Smart and Interactive Wallpaper)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

HP Inc., Canon Inc., Xeikon, Roland DG Corporation, A.S. Création Tapeten AG, Graham & Brown, Seiko Epson Corporation, Mimaki Engineering Co., Ltd., Ricoh Company, Ltd., York Wallcoverings, Brewster Home Fashions, Muraspec Wallcoverings, Durst Group AG, Kornit Digital Ltd., Grandeco Wallfashion Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Digitally Printed Wallpaper Market Segmentation

By Printing Technology

- Inkjet Printing

- Electrophotography

By Substrate Type

- Non-Woven Materials

- Vinyl

- Paper

- Fabric and Textile

By End-Use Sector

- Residential

- Commercial

- Hospitality

By Product Type

- Wall Murals

- Standard Patterned Wallpaper

- Self-Adhesive Wallpaper

- Smart and Interactive Wallpaper

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Digitally Printed Wallpaper Industry

- HP Inc.

- Canon Inc.

- Xeikon

- Roland DG Corporation

- A.S. Création Tapeten AG

- Graham & Brown

- Seiko Epson Corporation

- Mimaki Engineering Co., Ltd.

- Ricoh Company, Ltd.

- York Wallcoverings

- Brewster Home Fashions

- Muraspec Wallcoverings

- Durst Group AG

- Kornit Digital Ltd.

- Grandeco Wallfashion Group

*- List not Exhaustive