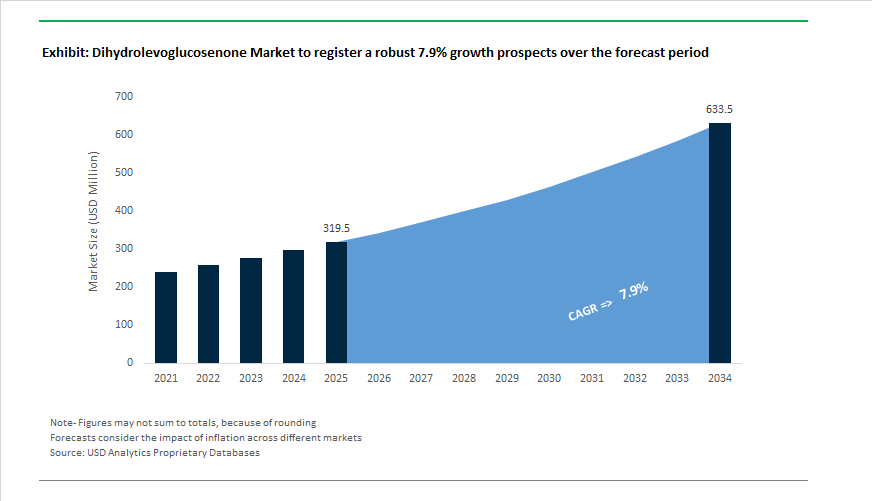

Dihydrolevoglucosenone Market to Reach $633.4 Million by 2034 at 7.9% CAGR Amid Bio-Based Solvent Disruption and Hydrogen Carrier Breakthroughs

The Dihydrolevoglucosenone Market is projected to expand from $319.5 Million in 2025 to $633.4 Million by 2034, registering a CAGR of 7.9%. Market growth is anchored in accelerating demand for bio-based solvents, sustainable chemical intermediates, liquid organic hydrogen carriers (LOHCs), and green chemistry platforms designed to replace petroleum-derived solvents such as DMF and NMP. Dihydrolevoglucosenone, commercially branded as Cyrene™, remains central to the decarbonization of medicinal chemistry, pharmaceutical manufacturing, CO2 capture systems, and advanced materials processing.

In July 2023 through 2024, Circa Group AS applied for patents covering its FuraTech:1 and FuraTech:2 solvent systems. These levoglucosenone-derived formulations demonstrated superior CO2 absorption efficiency and reduced desorption energy demand compared to conventional amine-based capture solvents, strengthening the role of biomass-derived cyclic ketones in Carbon Capture and Storage infrastructure. In Q1 2024, Circa signed a regional market development agreement with IXOM Operations Pty Ltd to expand Cyrene™ distribution across Australia and New Zealand, establishing an ANZ commercial footprint.

In April 2024, Circa finalized a strategic OEM agreement with Merck to supply and distribute Cyrene™ globally. The agreement leveraged Merck’s laboratory and pharmaceutical distribution channels to accelerate adoption among researchers seeking safer, bio-based dipolar aprotic solvents. In May 2024, Circa reported that construction of its flagship ReSolute plant in France was 50% complete, with core industrial equipment already delivered on-site. The facility was engineered to scale output from 50 tonnes per annum to 1,200 tonnes per annum, transitioning production from pilot volumes to industrial scale. During 2024, Circa also formalized a hydrogenation technology partnership with EKATO Group to optimize levoglucosenone conversion processes and ensure high-purity Dihydrolevoglucosenone output.

Despite these advances, a significant inflection occurred in October 2024, when Circa Group AS filed for bankruptcy after failing to secure sufficient equity funding amid shifting investor sentiment toward biomanufacturing ventures. Although the holding entity entered insolvency, late 2024 and 2025 efforts focused on preserving high-value assets, including the ReSolute plant infrastructure, engineering permits in France, the Cyrene™ trademark, and the patented FuraCell process. These assets remain potential acquisition targets for larger chemical producers seeking entry into renewable solvent production platforms.

Technology validation accelerated in 2025. Published research identified Dihydrolevoglucosenone as a viable Liquid Organic Hydrogen Carrier, capable of chemically storing hydrogen under ambient conditions and releasing it upon controlled heating. This LOHC capability positions biomass-derived solvents within hydrogen economy logistics, allowing compatibility with existing fuel distribution infrastructure. Additional studies in 2025 demonstrated that microwave-assisted reactions using Cyrene™ reduced acylal synthesis time from days to minutes, achieving a 70-fold molar efficiency improvement compared to conventional toxic solvent systems.

By early 2026, case studies released by the Royal Society of Chemistry confirmed commercial uptake of Cyrene™ and its sister solvent Ecomeo in medicinal chemistry libraries, replacing lipophilic fossil-derived solvents in pharmaceutical discovery workflows. The Circa Renewable Chemistry Institute, led by Professor James Clark, continued through 2024 and beyond to validate levoglucosenone-derived chemical platforms as cost-competitive, scalable alternatives for next-generation green pharmaceutical synthesis and sustainable industrial solvent systems.

Trends and Opportunities Defining the Dihydrolevoglucosenone (Cyrene™) Market

Regulatory Substitution for NMP and DMF in Pharmaceutical and Polymer Synthesis

- Regulatory pressure is the single most powerful driver of Cyrene adoption. With N-methyl-2-pyrrolidone (NMP) and dimethylformamide (DMF) facing authorization and restriction under EU REACH, pharmaceutical and fine chemical producers are prioritizing non-reprotoxic, biodegradable alternatives that do not compromise reaction efficiency. Toxicological validation completed during 2024–2025 confirms that dihydrolevoglucosenone is fully biodegradable within 14 to 28 days and exhibits an LD50 exceeding 2,000 mg/kg, positioning it as practically non-toxic for industrial use.

- This profile has moved Cyrene from pilot trials into mainstream API synthesis. In early 2025, Merck KGaA confirmed the integration of Cyrene into selected pharmaceutical manufacturing routes, citing regulatory resilience and long-term cost stability. In amide bond formation, which underpins a large share of API production, Cyrene has delivered reaction yields comparable to or higher than DMF while enabling solvent recovery through aqueous work-up and distillation. Industrial data indicates that this switch can reduce organic solvent waste streams by up to 25 %, strengthening Cyrene’s value proposition in GMP-compliant facilities where waste handling costs and audit exposure are rising.

Ultra-High-Purity Grades for Energy Storage and Electronics Processing

- Beyond pharmaceuticals, demand is accelerating for ultra-high-purity Cyrene grades tailored for energy storage and electronics manufacturing. One of Cyrene’s most commercially relevant properties is its ability to disperse conductive nanomaterials without surfactants. Advanced manufacturing trials completed in late 2024 demonstrated stable, surfactant-free dispersions of multi-walled carbon nanotubes, enabling supercapacitor electrodes with lower internal resistance and improved charge transport. This eliminates surfactant residues that typically degrade electrochemical performance over repeated cycles.

- In lithium-ion battery recycling, Cyrene is emerging as a green process solvent for cathode material recovery. Government-supported research in 2025 showed that treating spent PVDF-coated NMC811 electrodes with Cyrene at approximately 100 degrees Celsius allows high-yield separation of active metals from aluminum current collectors. This process supports closed-loop battery recycling initiatives in Europe and North America, where policy frameworks increasingly require material recovery rates that conventional solvent systems struggle to achieve without toxic byproducts.

Valorization of Chitin and Chitosan Through Bio-Solvent Processing

- Cyrene’s solvency for chitin is opening a structurally new opportunity linked to waste valorization. Chitin, the second most abundant natural polymer after cellulose, has historically required aggressive acid or alkali treatments to process, limiting its commercial scalability. Research published in August 2025 confirmed that Cyrene-based systems can dissolve alpha-chitin under comparatively mild conditions, enabling the spinning of high-strength chitosan fibers for biomedical applications such as biodegradable wound dressings and controlled drug delivery matrices.

- From a commercial perspective, this application creates a double-bio pathway where both the solvent and the polymer originate from renewable feedstocks. Packaging and biomedical material developers are actively exploring chitin-based films processed with Cyrene that biodegrade approximately 30% faster than PLA. This aligns with regulatory and brand-driven pressure to replace single-use plastics, particularly in food-contact and medical packaging segments.

Cyrene as a Platform Chemical for Sustainable Specialty Monomers

- Cyrene’s ketone and acetal functionalities extend its value beyond solvent use into monomer and intermediate synthesis. In 2025, the Circa Renewable Chemistry Institute announced progress on Cyrene derivatives such as 5-monohydroxycyrene, designed as chiral building blocks for polyimides and polyesters. These bio-derived monomers exhibit elevated glass transition temperatures and improved mechanical strength, meeting the performance requirements of aerospace electronics and advanced semiconductor substrates.

- Polymer synthesis studies using Cyrene-based intermediates have produced well-defined branched architectures with molecular weights ranging from 700 to 28,000 g/mol and high end-group fidelity. Such control over polymer structure is particularly attractive for next-generation lithography resists and specialty coatings, where rheological precision directly influences yield and pattern fidelity. As semiconductor manufacturers push toward smaller nodes and tighter tolerances, demand for bio-based yet performance-equivalent monomers positions Cyrene as a strategic enabler rather than a niche green alternative.

Dihydrolevoglucosenone (Cyrene) Market Share and Segmentation Insights

Dihydrolevoglucosenone (Cyrene) Market Share by Application : Bio-Based Solvents Lead as Pharma and Green Chemistry Accelerate Adoption

Solvents and extractive media dominate the Dihydrolevoglucosenone (Cyrene) market in 2025, accounting for 58% of total demand, driven by Cyrene’s performance as a bio-based dipolar aprotic solvent and a direct substitute for regulated chemicals such as NMP, DMF, and DMAc. Adoption is accelerating across polymer dissolution, graphene dispersion, and natural product extraction, supported by tightening environmental regulations and corporate sustainability targets. Chemical intermediates represent a significant segment, leveraging Cyrene’s reactive ketone functionality for synthesizing specialty chemicals, chiral compounds, and pharmaceutical intermediates within green manufacturing workflows. Pharmaceutical synthesis is the fastest-growing application, where Cyrene enables API production and peptide chemistry while supporting solvent replacement programs. Cleaning and degreasing remains a niche, focused on electronics and precision cleaning. Agrochemicals currently hold a minor share, limited by cost sensitivity, with uptake concentrated in premium formulations and R&D-driven applications.

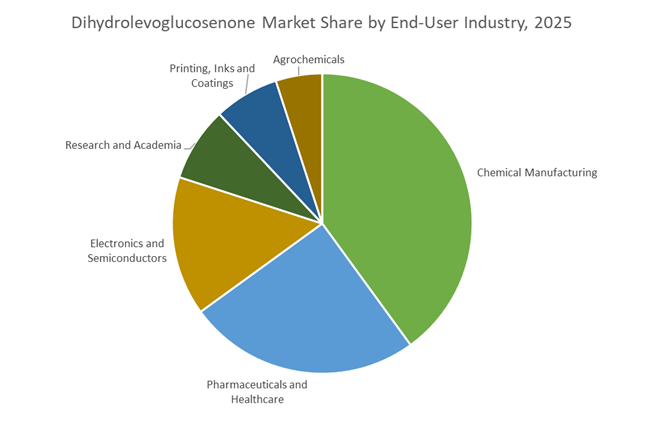

Dihydrolevoglucosenone (Cyrene) Market Share by End-User Industry : Chemical Manufacturing Anchors Demand While Pharma and Electronics Expand

Chemical manufacturing leads Cyrene consumption with 40% market share, positioning the solvent as a core enabler of sustainable chemical processing, specialty materials production, and regulatory-compliant manufacturing. Producers increasingly deploy Cyrene as a process solvent, reaction medium, and intermediate to meet ESG targets while maintaining performance parity with traditional dipolar aprotic solvents. Pharmaceuticals and healthcare form a rapidly expanding segment, driven by Cyrene’s role in API synthesis, formulation development, and NMP/DMF replacement strategies under green chemistry initiatives. Electronics and semiconductors are emerging growth engines, using ultra-high-purity Cyrene for precision cleaning, photoresist stripping, and electronic materials processing. Research and academia account for a notable share, with Cyrene widely adopted as a benchmark green solvent. Printing, inks, and coatings remain niche, while agrochemicals continue to see limited but strategic adoption in high-value and experimental formulations.

Competitive Landscape of the Dihydrolevoglucosenone Market

The Dihydrolevoglucosenone (Cyrene™) Market in 2026 is defined by rapid commercialization of bio-based aprotic solvents, strong regulatory tailwinds against DMF and NMP, and accelerating adoption across green chemistry, pharmaceuticals, electronics, coatings, and battery recycling. Market leadership is shaped by proprietary biomass conversion technologies, industrial-scale capacity buildouts, and downstream integration into sustainable polymers and formulations.

Circa Group pioneers industrial-scale Cyrene production through Furacell technology

Circa Group AS is the undisputed market creator and primary producer of Dihydrolevoglucosenone (Cyrene™), enabled by its proprietary Furacell™ single-step conversion process from levoglucosenone (LGO). In 2026, Circa commissioned its flagship ReSolute biorefinery in France, the world’s first industrial-scale Cyrene plant, targeting 1,200 tpa capacity. The company’s strategic roadmap aims for 80,000 tpa global capacity by 2030 via new European and Asian biorefineries. Early-2026 partnerships with Valmet and VTT further optimized low-carbon pyrolysis, delivering a near-zero carbon footprint. Circa’s core advantage remains its direct biomass-to-solvent pathway, offering the most cost-efficient route to renewable dipolar aprotic solvents for coatings, pharma synthesis, and advanced materials.

Merck KGaA accelerates pharmaceutical adoption of Cyrene as DMF and NMP replacement

Merck KGaA, operating through MilliporeSigma, is the primary global distributor of laboratory-grade Cyrene, driving adoption across pharmaceutical R&D and academic chemistry. Through its expanded Design for Sustainability program (2025–2026), Merck has replaced DMF and NMP with Cyrene in over 1,000 validated reaction protocols, accelerating market credibility. The company focuses on high-impact reactions such as Sonogashira cross-couplings and amide couplings, where Cyrene consistently demonstrates superior performance versus fossil-based solvents. Merck’s strength lies in ACS and HPLC-certified purity grades, providing the technical trust demanded by medicinal chemistry teams worldwide. Its positioning firmly anchors Cyrene within green solvent systems, sustainable synthesis workflows, and regulatory-compliant pharmaceutical development.

TCI strengthens Asia’s electronics-grade Cyrene supply for graphene and conductive inks

Tokyo Chemical Industry (TCI) serves as a key Asia-Pacific supplier of high-purity (>99%) dihydrolevoglucosenone, targeting electronics, specialty chemicals, and sustainable synthesis applications. Cyrene is increasingly used in liquid-phase exfoliation (LPE) of graphite, enabling production of high-quality graphene for conductive inks and flexible semiconductor coatings. In 2026, TCI intensified its focus on Japan’s electronics manufacturing hubs, positioning Cyrene as a non-toxic processing solvent for advanced materials. Leveraging a catalog exceeding 30,000 reagents, TCI bundles Cyrene with complementary bio-based building blocks for integrated “Total Green Synthesis” kits. Early-2026 expansion of its green chemistry portfolio also introduced Cyrene-derived fragments supporting next-generation sustainable drug discovery pipelines.

Solvay integrates Cyrene into circular polymers and battery recycling systems

Solvay S.A. is advancing downstream integration of dihydrolevoglucosenone across polymer circularity, agrochemicals, and industrial cleaning. The company is deploying Cyrene as a sustainable processing solvent for lithium-ion battery recycling and bio-polymer production, supporting Europe’s circular economy targets. In agrochemical formulations, Cyrene enables biodegradable pesticides and herbicides with significantly reduced environmental toxicity. Solvay’s deep integration across solvents and intermediates allows it to offer Cyrene-blended industrial solutions balancing performance and cost. In late 2025, Solvay increased R&D investment in its Actizone™ and specialty coatings platforms, aligning bio-based carriers with 2026 European Green Deal compliance, reinforcing its position in sustainable coatings and advanced materials.

Shandong Luba expands industrial-grade Cyrene supply for China’s coatings sector

Shandong Luba Chemical has emerged as a high-volume APAC supplier of industrial-grade dihydrolevoglucosenone, holding an estimated 12–15% regional bio-solvent share under China’s Green Chemical Hub initiatives. The company upgraded its catalytic hydrogenation infrastructure in 2025, improving yield and purity of bio-based intermediates derived from waste cellulose. Proximity to the world’s largest paper and pulp feedstock base provides structural cost advantages. In 2026, Shandong Luba pivoted aggressively toward the paint and coatings market, supplying bulk Cyrene as a non-mutagenic solvent for heavy-duty machinery finishes. Its strategy centers on volume-driven penetration of industrial coatings while supporting China’s broader transition toward renewable solvent systems.

France: Industrial Scale-Up Anchored in Circular Biorefining

France has emerged as the global industrial anchor for dihydrolevoglucosenone through the commissioning trajectory of the ReSolute™ plant in Eastern France. In late 2025, Circa Group advanced the facility toward mechanical completion, targeting 1,200 tonnes per annum of DLG output. This scale represents a decisive shift from demonstration volumes to true commercial supply, directly addressing European demand for bio-based replacements to NMP and DMF in coatings, electronics, and advanced materials. Strategically, the project repurposes a former coal-fired power station under the Grand Est regional industrial transition plan, positioning DLG as a flagship example of coal-to-chemical transformation supported by EU Horizon 2020 funding exceeding €11.8 million as of early 2025.

Beyond volume expansion, France’s competitive advantage lies in feedstock and process integration. The ReSolute™ site operates as a circular biorefinery using locally sourced, non-food sawdust biomass, delivering a reported carbon footprint up to 80% lower than fossil-derived polar aprotic solvents. Parallel R&D efforts with the Circa Renewable Chemistry Institute are extending the value chain into levoglucosenone derivatives, with pilot-scale programs targeting ultra-high-purity grades for aerospace and defense applications. This combination of scale, sustainability, and derivative optionality positions France as the reference manufacturing base for DLG in Europe.

United States: Regulatory Clearance and High-Value Application Adoption

In the United States, the commercialization trajectory for dihydrolevoglucosenone is tightly linked to regulatory validation and application-driven economics. As of Q3 2025, DLG remains in the final stages of TSCA review, a critical prerequisite for its widespread adoption as Cyrene™ in U.S. semiconductor, electronics cleaning, and advanced manufacturing workflows. In parallel, DLG has been recognized within Critical Chemicals Alliance frameworks, underscoring its strategic relevance in reducing U.S. dependence on imported polar aprotic solvents.

Application pull is already visible in specialty segments. During 2025, U.S.-based ink formulators reported up to a 30% reduction in manufacturing costs for graphene inks when substituting NMP with DLG, while simultaneously improving conductivity and dispersion stability in flexible electronics. In agrochemicals, alignment with the EPA’s 2026 safer chemicals workplan has encouraged early integration of DLG into green-label liquid pesticide formulations, where its low volatility and absence of reproductive toxicity offer a regulatory and performance advantage. Collectively, these use cases demonstrate that U.S. demand is being shaped less by bulk solvent substitution and more by high-margin, performance-critical applications.

Germany: Distribution Depth and REACH-Led Industrialization

Germany’s role in the dihydrolevoglucosenone market is defined by regulatory leadership and downstream industrial penetration. In 2025, OQEMA Group expanded its DACH-region distribution footprint to include specialized logistics for DLG, directly targeting German automotive and lithium-ion battery manufacturers seeking NMP-free cathode coating processes. This distribution-layer investment is accelerating qualification cycles for DLG in high-volume industrial environments.

Regulatory alignment further reinforces adoption. German stakeholders have led efforts toward REACH Annex IX registration for DLG, enabling its use above 100 tonnes per year in polymer processing, membrane manufacturing, and advanced composites. On the innovation front, Merck KGaA disclosed in late 2024–2025 that LGO derivatives are being incorporated into sustainable API synthesis routes. These bio-based pathways are delivering competitive cost structures relative to petroleum-derived intermediates, highlighting Germany’s role in translating green chemistry into economically viable pharmaceutical production.

China: Policy-Driven Substitution and Electronics Pull

China’s engagement with dihydrolevoglucosenone is being shaped by policy directives that prioritize specialty chemicals over incremental refining capacity. Under the 2025–2026 petrochemical stabilization plan issued by the Ministry of Industry and Information Technology, technical transformation and higher-value chemical outputs are explicitly encouraged, creating policy space for bio-based solvents like DLG. In response, research clusters in Jiangsu are exploring catalytic hydrogenation routes to produce DLG from locally available cellulosic waste, aligning self-sufficiency goals with decarbonization objectives.

Regulatory pressure from downstream industries is accelerating adoption. Updated national standards for VOC emissions in electronics manufacturing released in December 2025 have positioned DLG as a low-toxicity alternative for photoresist stripping and flux removal in HDI PCB production. This electronics-driven demand is particularly relevant given China’s scale in semiconductor packaging and consumer electronics assembly, suggesting that DLG uptake will be concentrated in precision cleaning rather than commodity solvent markets.

Australia: Technology Origin and Feedstock Export Strategy

Australia occupies a structurally distinct position as both the technology origin point and a future feedstock supplier for the global dihydrolevoglucosenone market. The FC5 plant in Tasmania continues to function as the primary R&D hub for the Furacell™ thermochemical process. In 2025, the facility achieved a notable improvement in levoglucosenone selectivity, reducing byproduct waste by 12%, a gain that directly improves downstream DLG economics at scale.

From a trade perspective, Australian agencies are leveraging abundant, sustainably managed forestry resources to position the country as a preferred exporter of cellulose-derived precursors into the Asia-Pacific region. This strategy supports emerging DLG production hubs in China and potentially Southeast Asia, anchoring Australia’s role upstream in the global value chain rather than as a large-volume solvent consumer.

Snapshot Summary: Dihydrolevoglucosenone Market by Country

Dihydrolevoglucosenone Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Development Lever

|

Industrial Impact

|

|

France

|

Commercial scale-up

|

Circular biorefinery, EU funding

|

Anchor production base for Europe

|

|

United States

|

Regulatory clearance

|

TSCA approval, specialty adoption

|

High-margin electronics and agro uses

|

|

Germany

|

Downstream penetration

|

REACH leadership, distribution

|

Industrial-scale substitution for NMP

|

|

China

|

Policy-driven transition

|

Electronics VOC standards

|

Precision cleaning demand growth

|

|

Australia

|

Technology and feedstock

|

Process IP, forestry exports

|

Upstream value chain positioning

|

Dihydrolevoglucosenone Market Report Scope

Dihydrolevoglucosenone Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$319.5 Million

|

|

Market Size (2034)

|

$633.4 Million

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Application (Solvents and Extractive Media, Pharmaceutical Synthesis, Chemical Intermediates, Cleaning and Degreasing, Agrochemicals), By Purity Grade (Industrial Grade, High Purity Grade), By End-User Industry (Pharmaceuticals and Healthcare, Electronics and Semiconductors, Chemical Manufacturing, Agrochemicals, Printing, Inks and Coatings, Research and Academia)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Circa Group AS, Merck KGaA, Tokyo Chemical Industry Co., Ltd., OQEMA Group, Carl Roth GmbH & Co. KG, Scientific Design Company, Inc., Thermo Fisher Scientific Inc., Solvay S.A., Haihang Industry Co., Ltd., Shandong Luba Chemical Co., Ltd., China Petroleum & Chemical Corporation, Vertec Biosolvents Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dihydrolevoglucosenone Market Segmentation

By Application

- Solvents and Extractive Media

- Pharmaceutical Synthesis

- Chemical Intermediates

- Cleaning and Degreasing

- Agrochemicals

By Purity Grade

- Industrial Grade

- High Purity Grade

By End-User Industry

- Pharmaceuticals and Healthcare

- Electronics and Semiconductors

- Chemical Manufacturing

- Agrochemicals

- Printing, Inks and Coatings

- Research and Academia

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dihydrolevoglucosenone Industry

- Circa Group AS

- Merck KGaA

- Tokyo Chemical Industry Co., Ltd.

- OQEMA Group

- Carl Roth GmbH & Co. KG

- Scientific Design Company, Inc.

- Thermo Fisher Scientific Inc.

- Solvay S.A.

- Haihang Industry Co., Ltd.

- Shandong Luba Chemical Co., Ltd.

- China Petroleum & Chemical Corporation

- Vertec Biosolvents Inc.

*- List not Exhaustive