Radiation Cured Coatings Market Size, Energy-Efficient Processing, and High-Speed Industrial Demand

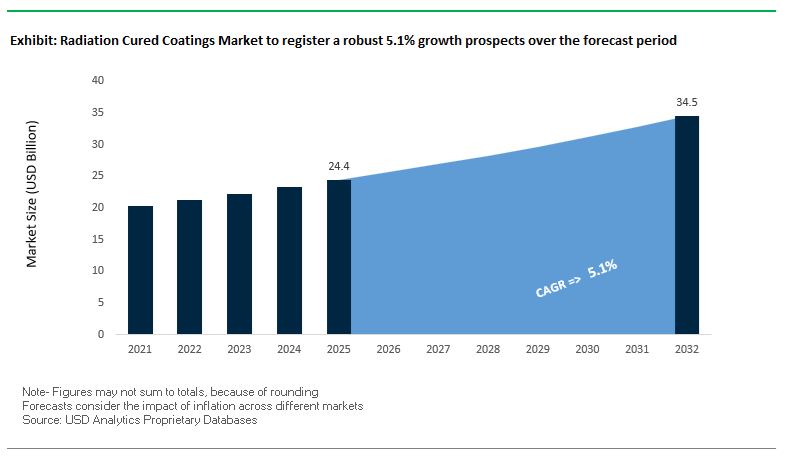

The global Radiation Cured Coatings Market was valued at $24.4 billion in 2025 and is projected to grow at a CAGR of 5.1% through 2032, reaching $34.6 billion by 2032. Growth is driven by increasing demand for high-speed, energy-efficient, and solvent-free coating technologies across automotive, electronics, packaging, wood, and industrial manufacturing sectors.

Radiation cured coatings—primarily UV, LED, and Electron Beam (EB) systems—enable instantaneous curing, reduced energy consumption, and superior surface performance compared to traditional thermal curing. These coatings are widely used in applications requiring high throughput, precision finishes, and minimal environmental impact, such as coil coatings, printed packaging, flooring, and electronics components.

A key structural driver is the increasing need for low-VOC and solvent-free coating solutions, as global regulations tighten around emissions and sustainability. Radiation curing processes eliminate or significantly reduce solvents, making them highly aligned with ESG targets and industrial decarbonization strategies.

In addition, the growth of advanced manufacturing technologies, including additive manufacturing (3D printing), smart coatings, and high-performance automotive finishes, is accelerating the adoption of radiation-cured systems. These applications require rapid curing cycles and precise control over coating properties, which radiation technologies uniquely provide.

Market Analysis: Laser-Based Curing, EB Coil Innovations, and Bio-Attributed UV Systems Driving Market Evolution

Recent developments in the Radiation Cured Coatings Market highlight a strong convergence of next-generation curing technologies, sustainability-driven innovation, and industrial scalability. In April 2026, AkzoNobel introduced laser-based curing technology in collaboration with IPG Photonics, enabling selective, instantaneous curing of powder coatings with significantly reduced energy consumption. This marks a major evolution beyond traditional UV systems toward precision radiation curing.

Electron Beam (EB) curing is gaining traction in heavy industrial applications. The collaboration between Beckers and ArcelorMittal resulted in the first commercial EB coil coating system, enabling 100% solid, solvent-free coatings for steel substrates without the need for thermal drying ovens. This innovation is particularly significant for pre-painted metal manufacturing, where energy savings and process efficiency are critical.

Material innovation is advancing sustainability and performance. Allnex’s waterborne UV Excimer resin (October 2025) combines low-VOC benefits with ultra-matte finishes, targeting premium furniture and flooring markets. Meanwhile, Arkema’s ISCC PLUS certification (January 2026) enables large-scale production of bio-attributed UV/LED curable resins, supporting downstream manufacturers in reducing Scope 3 emissions.

Application flexibility is expanding through field-deployable technologies. Allnex’s Field-Applied UV (FAC) coatings allow on-site curing for flooring and concrete surfaces, delivering instant return-to-service and improved durability in commercial renovation projects.

Advanced functionality is also shaping product development. BASF’s radiation-cured automotive coatings, introduced under its “DRIVING THE PROXY” initiative, enable precise alignment of metallic pigments, critical for achieving next-generation visual effects. Additionally, Arkema’s UV-LED resins for 3D printing (February 2026) support faster production of complex components with enhanced pre-cure stability (“green strength”).

Regulatory and safety considerations are influencing innovation in packaging. Industry developments highlighted at RadTech 2025 focus on low-migration UV-LED systems, ensuring compliance with food safety regulations by minimizing chemical transfer from coatings to packaged products.

Ecosystem-level initiatives are also accelerating adoption. AkzoNobel’s IONOMY™ platform (October 2025) provides a collaborative framework to transition coil coating manufacturers from energy-intensive thermal curing to radiation-based systems, reinforcing the industry’s shift toward efficient, low-carbon production methods.

Market Trend: Electron Beam Curing Adoption Accelerating Under EU MDR and FDA QMSR Compliance for Medical Devices

The radiation cured coatings market is witnessing accelerated adoption of electron beam curing technologies in medical device manufacturing, driven by tightening regulatory frameworks and biocompatibility requirements. The transition deadlines under EU MDR 2017/745 for high-risk devices and the 2026 enforcement of updated quality management standards by the U.S. Food and Drug Administration are compelling manufacturers to shift toward coating processes that ensure both performance and compliance.

Electron beam curing is gaining preference due to its ability to achieve exceptionally high polymerization efficiency. Medical-grade acrylate systems cured via EB demonstrate conversion rates exceeding 99.5%, significantly reducing residual monomer content and enabling compliance with extractable and leachable limits under ISO 10993-18 biocompatibility standards. This is critical for applications such as catheters, implants, and diagnostic devices where material purity directly impacts patient safety.

The regulatory transition timeline is also driving capital investment. With the December 31, 2027 deadline for certifying legacy Class III and IIb devices under MDR, medical device manufacturers are upgrading coating infrastructure to align with future-ready technologies. Industry data indicates a 25% to 30% increase in EB curing line installations as facilities replace heat-intensive curing methods that are incompatible with emerging biopolymer substrates.

A key operational advantage is the dual-functionality of EB curing. The process acts as both a coating cure mechanism and a sterilization step, eliminating the need for separate sterilization cycles. This reduces total processing time for coated medical components by approximately 60%, improving throughput and enabling manufacturers to meet the accelerated supply chain demands imposed by modern regulatory frameworks.

Market Trend: UV-LED Curing Systems Transforming Automotive Interior Coatings in China’s EV Ecosystem

The adoption of UV-LED curing technologies is expanding rapidly within the automotive coatings segment, particularly in China’s electric vehicle manufacturing ecosystem. Regulatory drivers such as cabin VOC emission limits and battery safety standards are pushing OEMs toward low-energy, low-temperature coating processes for interior components.

UV-LED curing systems operating at wavelengths around 395 nm provide a significant thermal advantage over traditional mercury arc lamps. These systems operate at temperatures 30°C to 50°C lower, which is critical for preventing deformation of thin-wall plastic components used in lightweight EV interiors. As vehicle manufacturers reduce material thickness by approximately 15% to achieve weight reduction targets, maintaining dimensional stability during coating becomes a key requirement.

Energy efficiency is another major driver. Under China’s decarbonization objectives, UV-LED curing systems demonstrate energy savings of 70% to 80% compared to conventional thermal curing ovens. This aligns with broader industrial energy reduction targets and reduces operating costs in high-volume automotive coating lines.

Production speed improvements further enhance adoption. UV-LED cured anti-fingerprint coatings applied to touch displays and center consoles achieve full hardness in under two seconds. This rapid curing capability supports high-throughput manufacturing environments, particularly as China targets annual EV production volumes exceeding 10 million units. The combination of speed, efficiency, and compliance is positioning UV-LED curing as a standard technology in next-generation automotive interior coatings.

Market Opportunity: EB-Cured Silicone Release Coatings Enabling Scalable Production of Lithium-Ion Battery Separators

The rapid expansion of lithium-ion battery manufacturing is creating a significant opportunity for electron beam cured silicone release coatings in separator film production. These coatings are critical in enabling high-speed processing and maintaining the structural integrity of ultra-thin battery components.

Electron beam curing offers a distinct advantage in substrate preservation. Silicone release coatings can be applied to biaxially-oriented polypropylene separator films as thin as 12 microns without inducing thermal shrinkage, which is commonly observed in conventional oven-based curing processes. Preventing shrinkage is essential for maintaining alignment and performance in battery cells.

Production scalability is a key factor driving adoption. EB curing lines are capable of operating at speeds of up to 1,000 meters per minute, nearly doubling the throughput of solvent-based thermal coating systems. This capability is critical as global battery demand continues to exceed existing manufacturing capacity, particularly in electric vehicle and energy storage applications.

The use of nitrogen-inerted curing environments further enhances coating performance. By reducing oxygen levels below 200 ppm, EB curing ensures complete cross-linking of silicone systems and eliminates the risk of migratory silicone contamination in active battery materials. This level of process control is essential for maintaining battery efficiency, safety, and lifecycle performance.

Market Opportunity: Far-UVC Excimer Technology Unlocking High-Speed, Sanitized Coating for Beverage and Aerosol Packaging

Emerging deep-UV curing technologies, particularly 222 nm Far-UVC excimer lamps, are creating new opportunities in the metal packaging coatings segment. These systems combine rapid curing capabilities with surface sanitization, addressing both production efficiency and hygiene requirements in food-grade packaging.

Far-UVC excimer systems enable internal lacquer coatings on aluminum cans to be cured at line speeds exceeding 2,500 cans per minute. This high-speed capability is essential for meeting the throughput demands of modern beverage and aerosol packaging facilities. At the same time, the technology delivers a 5-log reduction in surface pathogens, eliminating the need for additional chemical sterilization steps.

Space efficiency is a major advantage in manufacturing facility design. Replacing traditional gas-fired thermal ovens, which can span up to 30 meters, with compact UV-LED or excimer modules reduces the coating line footprint by approximately 90%. This allows manufacturers to establish smaller, decentralized production units, supporting trends such as urban micro-canning and localized supply chains.

Environmental performance further strengthens the value proposition. Advanced 222 nm systems are engineered to operate without generating ozone, removing the need for complex exhaust and air scrubbing systems typically required in UV curing operations. This simplifies plant infrastructure while ensuring compliance with environmental and occupational safety standards in food packaging environments.

Radiation Cured Coatings Market Share and Segmentation Insights: Oligomer Dominance and OEM-Driven Supply Chain Dynamics

By Formulation Component: Oligomers Lead as Core Performance Drivers in UV/EB Coatings

The oligomers segment dominated the radiation cured coatings market with a 45.8% share in 2025, owing to its critical role in defining the core performance characteristics of UV-cured and electron beam (EB) coatings. Oligomers such as epoxy acrylates, polyurethane acrylates, polyester acrylates, and silicone acrylates serve as the backbone of coating formulations, directly influencing hardness, flexibility, chemical resistance, adhesion, and weatherability. These properties are essential across high-performance applications including wood coatings, automotive clearcoats, electronics protection, and metal packaging. Additionally, oligomers account for a significant 40–70% of total formulation weight, making them the largest contributor to raw material consumption in radiation-cured systems. Their ability to deliver low-VOC, fast-curing, and high-durability coatings aligns with growing demand for sustainable and high-efficiency coating technologies, reinforcing oligomers’ leadership in the global radiation cured coatings market.

By Sales Channel: OEM Coating Manufacturers Dominate with High-Volume Procurement and Custom Formulation Needs

The OEM (coating manufacturers) segment held a leading 52.4% share of the radiation cured coatings market in 2025, reflecting the concentration of demand among large-scale UV/EB coating producers. These manufacturers require highly customized formulations, blending oligomers, monomers, photoinitiators, and specialty additives to meet specific performance requirements for applications such as wood flooring finishes, automotive coatings, electronics, and printing inks. Direct sourcing from leading chemical companies like Arkema, Allnex, Covestro, and BASF enables OEMs to secure consistent raw material quality, tailored chemistry, and innovation support. Furthermore, OEMs represent the largest consumers of radiation-cured raw materials, necessitating bulk procurement contracts, stable supply chains, and technical collaboration to optimize formulation performance. This strong integration between raw material suppliers and coating manufacturers ensures product consistency, scalability, and regulatory compliance, solidifying OEM dominance in the global radiation cured coatings market.

Competitive Landscape of the Radiation Cured Coatings Market

PPG Leads Market with Advanced Testing Infrastructure and High-Efficiency Radiation Systems

PPG Industries, Inc. is the technological vanguard of the radiation cured coatings market, leveraging its strong R&D and customer-centric validation capabilities. In 2026, the company installed an advanced testing line in France capable of replicating UV (LED, excimer), IR, and electron beam curing conditions, enabling precise customer application development. Its radiation-cured coatings can reduce carbon emissions by up to 65% compared to thermal curing, especially when formulated as 100% solids. PPG has also pioneered laser-curing pilot lines, bridging the gap between traditional UV curing and localized high-speed coating repair.

AkzoNobel Expands Market Leadership with UV-PUD and Low-Energy Curing Innovations

AkzoNobel N.V. is a major player in the radiation cured coatings market, focusing on productivity and sustainability. Its UV-curable polyurethane dispersion (UV-PUD) coatings enable visible-light-responsive curing, allowing uniform coating of complex 3D geometries in consumer electronics. The company is also investing heavily in low-bake and fast-cure technologies, reducing manufacturing cycle times by up to 40%. Its ongoing merger with Axalta further strengthens its global position in high-performance coatings and advanced curing systems.

BASF Strengthens Market with Integrated Resin Supply and Advanced UV-Cured Systems

BASF SE plays a critical role in the radiation cured coatings market, supplying both oligomers and finished systems through its integrated Verbund model. Its latest innovations include UV-cured automotive coatings that deliver liquid-metal visual effects using advanced pigment technologies. The company has expanded production capacity for radiation-curable oligomers in China, supporting growth in the electronics and automotive sectors. BASF’s formulations incorporate up to 30% bio-attributed content, aligning with sustainability goals and reinforcing its leadership in advanced coating materials.

allnex Leads Resin Innovation with High-Performance UV and EB-Curable Systems

allnex is a specialist leader in the radiation cured coatings market, focusing on high-performance resin platforms. Its UCECOAT® 7690 UV-PUD offers exceptional durability and adhesion across multiple substrates, particularly in green building applications. The company’s EBECRYL® series enhances abrasion and stain resistance for industrial wood and flooring applications. allnex is also a leader in electron beam curing technologies, enabling instantaneous curing without heat distortion, making it ideal for thin-film packaging.

Axalta Drives Efficiency with UV-Curable Automotive Coatings and Rapid Repair Technologies

Axalta Coating Systems is a key player in the radiation cured coatings market, particularly in automotive and mobility applications. Its Lumeera™ 3250 system integrates low-bake and UV-curing technologies, reducing energy consumption in automotive paint shops by up to 20%. The company has also introduced UV-curable refinish primers that enable rapid repair cycles in under 10 minutes, significantly improving productivity in body shops. Axalta’s strong partnerships with global automotive OEMs reinforce its leadership in high-performance radiation-cured coatings.

Arkema Enables Market Growth with Bio-Based Acrylates and UV-LED Resin Technologies

Arkema Group is a critical enabler in the radiation cured coatings market, supplying high-performance acrylates through its Sartomer® business line. The company has expanded its production capacity in China by 35% to meet rising demand in electronics, packaging, and 3D printing. Its Sarbio® range offers bio-based acrylates with over 80% renewable carbon content, supporting sustainability initiatives. Arkema is also transitioning toward UV-LED curing systems, reducing energy consumption by up to 50% compared to traditional mercury lamp technologies. Its strong vertical integration positions it as a leader in next-generation photopolymer solutions.

China’s Dominance in Radiation Cured Coatings Driven by Green Conversion and High-Volume Manufacturing

China continues to lead the global radiation cured coatings market through its aggressive transition from solvent-based coatings to UV-LED curing technologies and waterborne UV formulations. Under the “Blue Sky Defense War” 2025 regulatory updates, the implementation of VOC emission taxes has significantly strengthened the cost competitiveness of UV/EB curable coatings, particularly in industrial wood and plastic applications. This regulatory push has accelerated widespread industrial adoption, positioning China as a key hub for sustainable coatings innovation.

Technological advancements such as UV-curable dual-cure systems are transforming coating applications for complex 3D geometries, especially in automotive interiors, where eliminating shadow zone defects is critical. China’s rapid adoption of dielectric UV coatings in EV battery components, including enclosures and busbars, underscores its leadership in electric mobility applications. Investment momentum remains strong, highlighted by the inauguration of a 15,000-metric-ton UV resin production facility in 2025 aimed at supporting 5G hardware demand. Additionally, innovations in bio-based UV resins with up to 45% renewable content and expansion of UV-LED curing infrastructure for fiber optics further reinforce China’s strategic dominance in high-growth segments.

United States: Advanced EB Curing and Reshoring Trends Transforming High-Performance Coatings

The United States is emerging as a critical innovation hub in the radiation cured coatings industry, driven by reshoring initiatives and advanced Electron Beam (EB) curing technologies. Regulatory developments such as the EPA’s 2026 PFAS-free mandates are accelerating the transition toward PFAS-free UV coatings, particularly in architectural and medical applications, thereby reshaping product development strategies across the market.

The US is witnessing strong growth in EB curing for flexible packaging, enabling the production of high-barrier food packaging with zero photoinitiator migration—essential for FDA compliance. In aerospace, the standardization of UV-curable primers and topcoats is significantly reducing maintenance time and energy consumption in MRO operations. Government-backed investments, including DOE funding, are supporting R&D in UV coatings for offshore wind turbine blades, enhancing durability in extreme environments. Additionally, the rising adoption of UV-LED wood coatings in reshored furniture manufacturing and innovations such as anti-reflective UV coatings for solar glass are strengthening the US position in sustainable and high-efficiency coating solutions.

Germany’s Industry 4.0 Leadership Driving Smart UV Curing and Functional Coatings Innovation

Germany stands at the forefront of the European radiation cured coatings market, leveraging its Industry 4.0 capabilities to integrate AI-driven UV-LED curing systems. These smart systems dynamically adjust curing parameters based on coating thickness and production speed, achieving significant energy efficiency improvements. Regulatory alignment with the EU Energy Performance of Buildings Directive (EPBD) is fueling demand for UV-cured low-emissivity (Low-E) coatings, particularly in architectural glass applications.

Sustainability initiatives are a major growth driver, with the introduction of carbon-neutral UV-curable monomers targeting premium automotive OEMs. Germany also leads in specialized applications, including antimicrobial UV coatings for public transport and healthcare infrastructure, incorporating advanced silver-ion technologies. Expansion of urethane acrylate production capacity reflects rising demand for optical coatings, while innovations in UV-curable 3D printing resins are bridging the gap between prototyping and industrial-scale manufacturing.

India’s Rapid Expansion as a High-Growth Market for UV Curable Coatings in Electronics and Packaging

India is experiencing exponential growth in the radiation cured coatings market, driven by government-backed initiatives and rising industrialization. The Production Linked Incentive (PLI) scheme for electronics manufacturing is significantly boosting demand for UV-curable solder masks and conformal coatings, positioning India as a global electronics manufacturing hub.

Infrastructure development, including smart cities and high-speed rail, is driving demand for UV-curable architectural metal coatings, while the shift toward UV pre-finished coil coatings in the white goods sector is modernizing domestic appliance manufacturing. Leading companies such as Asian Paints are investing in UV-LED curing laboratories to localize production capabilities. The booming e-commerce sector is also accelerating demand for UV-curable inks and packaging coatings, while regulatory updates like BIS 2025 are promoting low-VOC, environmentally friendly coating technologies, further strengthening market adoption.

South Korea’s Leadership in Semiconductor-Grade UV Coatings and Advanced Display Technologies

South Korea remains a global powerhouse in high-precision radiation cured coatings, particularly in semiconductor and display applications. The development of photo-curable polyimide coatings is enabling the next generation of foldable and flexible OLED displays, ensuring durability and flexibility without material degradation.

Major investments by industry leaders such as LG Chem and SK Group are advancing UV-curable materials for solid-state batteries, including electrolytes and separators. South Korea’s dominance in UV-curable photoresists is critical for semiconductor lithography at advanced nodes. Regulatory updates under K-REACH 2025 are pushing manufacturers toward safer, low-migration photoinitiators, enhancing product sustainability. Innovations such as anti-fingerprint UV coatings for smartphones and expansion of waterborne UV dispersions for automotive refinishing further reinforce South Korea’s position in high-value applications.

Japan’s Precision Engineering Excellence in EB Cross-Linking and Specialty UV Coatings

Japan is a global leader in niche, high-performance segments of the radiation cured coatings market, particularly through its expertise in Electron Beam (EB) cross-linking technologies. These technologies are critical for high-temperature resistant wire and cable insulation used in aerospace and electric vehicle applications.

The country has strong demand for UV-curable hardcoats in automotive applications, ensuring long-term durability and UV resistance. Investments in clean-room EB coating facilities are enabling innovations in smart food packaging with oxygen-scavenging properties. Japanese firms are also pioneering dual-cure bio-resins that leverage natural sunlight for secondary curing, enhancing sustainability in infrastructure projects. Breakthrough innovations such as self-healing UV coatings for electronics and strict compliance with food safety regulations are further driving adoption of advanced curing technologies.

Vietnam Emerging as a Strategic Manufacturing Hub for UV Cured Coatings in Southeast Asia

Vietnam is rapidly gaining traction in the radiation cured coatings market as a key manufacturing destination amid global supply chain shifts. The influx of electronics OEMs has increased demand for UV conformal coatings for PCB assembly, strengthening Vietnam’s role in electronics manufacturing.

Significant investments, including a $30 million UV-LED coating cluster in Dong Nai, are boosting production capacity for export-oriented furniture and metal coatings. Government incentives such as tax benefits for adopting energy-efficient UV-LED curing systems are accelerating industrial transformation. Vietnam is also witnessing rapid growth in UV coatings for bicycle and e-bike frames, alongside expansion in high-speed UV labeling for beverages and pharmaceuticals. Technological advancements such as low-viscosity UV primers are enabling efficient coating of porous substrates, further enhancing production efficiency and quality.

Radiation Cured Coatings Market Report Scope

Radiation Cured Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.4 Billion

|

|

Market Size (2032)

|

$34.6 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Curing (Ultraviolet, Electron Beam, Dual-Cure Systems), By Resin (Acrylates, Epoxies, Polyesters, Urethane, Silicones, Bio-based Resins), By Formulation Component (Oligomers, Monomers, Photoinitiators, Additives and Pigments), By Substrate (Wood, Plastic, Paper and Board, Metal, Glass and Ceramics, Composites), By End-Use Industry (Packaging and Graphic Arts, Electronics and Semiconductor, Automotive and Transportation, Wood and Furniture, Industrial and General Manufacturing, Healthcare and Medical Devices, Energy), By Functional Property (Scratch and Abrasion Resistance, High-Gloss, Chemical and Solvent Resistance, UV Protection, Specialty), By Sales Channel (OEM, Printing and Converting Services, Specialty Chemical and Equipment Distributors, On-Site)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., Arkema S.A., Covestro AG, Allnex Netherlands B.V., Evonik Industries AG, Axalta Coating Systems Ltd., DIC Corporation, Nippon Paint Holdings Co., Ltd., Dymax Corporation, IGM Resins B.V., Rahn AG, Toyo Ink SC Holdings Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Radiation Cured Coatings Market Segmentation

By Curing

- Ultraviolet

- Electron Beam

- Dual-Cure Systems

By Resin

- Acrylates

- Epoxies

- Polyesters

- Urethane

- Silicones

- Bio-based Resins

By Formulation Component

- Oligomers

- Monomers

- Photoinitiators

- Additives and Pigments

By Substrate

- Wood

- Plastic

- Paper and Board

- Metal

- Glass and Ceramics

- Composites

By End-Use Industry

- Packaging and Graphic Arts

- Electronics and Semiconductor

- Automotive and Transportation

- Wood and Furniture

- Industrial and General Manufacturing

- Healthcare and Medical Devices

- Energy

By Functional Property

- Scratch and Abrasion Resistance

- High-Gloss

- Chemical and Solvent Resistance

- UV Protection

- Specialty

By Sales Channel

- OEM

- Printing and Converting Services

- Specialty Chemical and Equipment Distributors

- On-Site

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Radiation Cured Coatings Industry

- BASF SE

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Akzo Nobel N.V.

- Arkema S.A.

- Covestro AG

- Allnex Netherlands B.V.

- Evonik Industries AG

- Axalta Coating Systems Ltd.

- DIC Corporation

- Nippon Paint Holdings Co., Ltd.

- Dymax Corporation

- IGM Resins B.V.

- Rahn AG

- Toyo Ink SC Holdings Co., Ltd.

*- List not Exhaustive