Diisononyl Phthalate Market to Reach $8 Billion by 2034 at 4.5% CAGR Amid PVC Infrastructure Growth and Non-Phthalate Transition Pressure

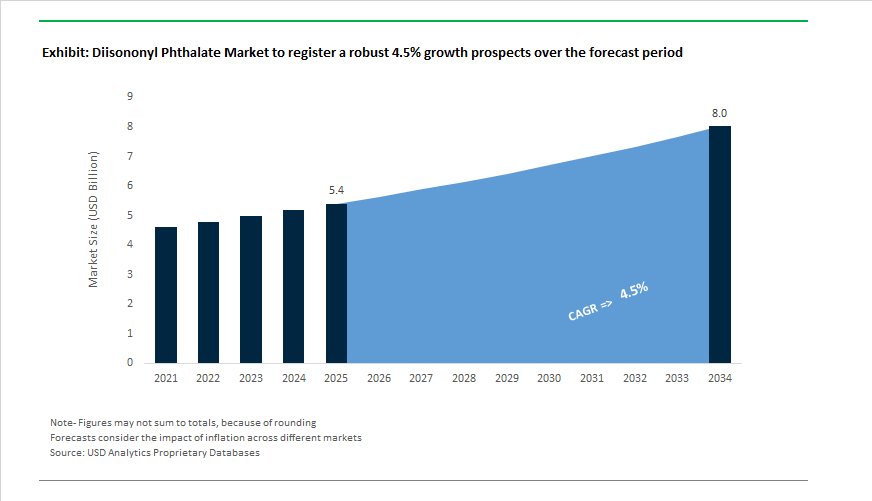

The Diisononyl Phthalate (DINP) Market is projected to expand from $5.4 billion in 2025 to $8 billion by 2034, registering a CAGR of 4.5%. Growth is anchored in sustained demand for flexible PVC in wire and cable, luxury vinyl tile flooring, automotive interiors, roofing membranes, and EV charging infrastructure. DINP remains one of the most widely used high-molecular-weight phthalate plasticizers due to its low volatility, cold-temperature flexibility, and cost efficiency. However, the market is simultaneously navigating regulatory scrutiny, non-phthalate substitution, tariff pressures, and portfolio rationalizations among global intermediates producers.

Between 2024 and 2025, ExxonMobil reinforced its leadership in the DINP segment with the launch of Jayflex™ 218, engineered for high-performance PVC applications in wire and cable and resilient flooring. The product focuses on reduced volatility, enhanced durability, and superior low-temperature performance, targeting automotive under-hood components and construction materials exposed to extreme climates. In April 2025, Nan Ya Plastics completed its flexible PVC sheeting expansion in Texas, supplying high-end automotive interiors and luxury vinyl tile markets across North America. In June 2025, Evonik expanded its plasticizer production capacity in Asia-Pacific, strengthening supply reliability for manufacturers in China and India where infrastructure and consumer goods production continue to scale.

Regulatory and competitive shifts intensified during 2024–2025. UPC Technology reported that its hydrogenated non-phthalate plasticizer DINCH captured more than 70% of Taiwan’s market share by late 2024, signaling accelerated substitution trends. In May 2025, new U.S. tariffs introduced a 10% levy on Chinese PVC resins and a 15% tariff on certain Middle Eastern petrochemical feedstocks, increasing production costs for North American DINP manufacturers and triggering price adjustments across the plasticizer value chain. In late 2025, LG Chem signed an MOU with EL Electric to co-develop flame-retardant PVC charging cables for EV infrastructure, reinforcing DINP’s role in delivering heat resistance and mechanical flexibility for high-voltage applications. Meanwhile, ICL Group announced a strategic pivot toward zinc-bromine flow battery technology in November 2025, redirecting R&D resources toward energy storage and signaling long-term diversification away from traditional phthalate-linked auxiliary segments.

Strategic restructuring became a defining theme entering 2026. In January 2026, Dow elevated its Cash Improvement Plan target to $1.3 billion, reviewing its intermediates and derivatives footprint to improve margins in oversupplied chemical markets. Reliance Industries implemented rapid pricing revisions in early 2026 to stabilize domestic DINP supply amid volatile imported feedstock costs, reinforcing India’s infrastructure-driven demand cycle. In February 2026, Evonik introduced its Tailor Made efficiency program to streamline global operations and preserve competitiveness in commoditized plasticizer segments. At Plastindia 2026 in February 2026, BASF showcased advanced durability solutions for plastics exposed to solar radiation and extreme environmental conditions. While emphasizing its Hexamoll® DINCH non-phthalate portfolio, BASF remains an important participant in the high-purity DINP value chain, reflecting the industry’s dual-track strategy of maintaining phthalate performance applications while accelerating sustainable plasticizer alternatives.

Trends and Opportunities Shaping the Diisononyl Phthalate (DINP) Market

Accelerated Regulatory Phase-Out in Consumer Products and Childcare

- Regulatory enforcement is now the dominant force compressing DINP demand in consumer-facing segments. The classification of DINP as a Category 1B reprotoxicant has moved from risk assessment into active enforcement across major economies. In the United States, the implementation of California Proposition 65 short-form warning revisions from January 1, 2025 has materially altered retailer behavior. DINP-containing products must now explicitly name the chemical on warning labels, rather than relying on generic toxicity language. This shift has proven commercially disruptive, as national retailers increasingly avoid stocking products that carry toxin-specific labeling, accelerating reformulation toward non-phthalate plasticizers.

- In Europe, enforcement of REACH Annex XVII Entry 52 has intensified throughout 2025. Market surveillance data indicates a sharp increase in inspections targeting imported vinyl toys and childcare articles. Compliance failures have translated into a 65% year-on-year rise in recalls during the first half of 2025, particularly for low-cost imports exceeding the 0.1% DINP threshold in mouthable products. This has effectively removed DINP from the toy and childcare value chain in the EU, reinforcing a managed exit rather than a gradual substitution.

Sustained Utility in Heavy Infrastructure and Grid Modernization

- In contrast to consumer markets, DINP demand remains structurally supported in infrastructure-driven applications. According to projections from the International Energy Agency, global investment in electricity grids is approaching USD 400 billion as countries expand renewable generation, interconnectors, and energy storage. This capital deployment is directly supporting demand for DINP-plasticized PVC in high-performance cable insulation and jacketing, particularly for subsea, underground, and outdoor transmission lines where moisture resistance and low-temperature flexibility are critical.

- DINP also maintains a strong position in automotive and industrial coatings. Technical documentation released in 2025 by Evonik and ExxonMobil confirms that DINP-based plastisols continue to outperform bio-based alternatives in long-term salt spray and oil exposure tests. This performance is increasingly relevant as electric vehicles gain weight due to battery systems, placing higher mechanical and corrosion-resistance demands on underbody coatings. In these applications, DINP’s low volatility and resistance to extraction provide measurable lifecycle advantages.

High-Performance, Low-Migration Formulations for Medical Devices

- Although DINP is excluded from blood-contact medical devices, regulatory guidance is opening selective opportunities in non-invasive healthcare applications. In January 2025, the U.S. Food and Drug Administration Center for Biologics Evaluation and Research issued draft guidance encouraging evaluation of non-DEHP materials, rather than blanket exclusion of all phthalates. This has created a niche for ultra-pure DINP grades in applications such as oxygen delivery tubing, respiratory masks, and examination gloves, where clarity, flexibility, and kink resistance are essential.

- Manufacturers are also developing low-VOC DINP formulations for hospital flooring and wall coverings. These products are engineered to minimize off-gassing while preserving abrasion resistance and chemical durability in high-traffic healthcare environments. Such formulations support compliance with LEED v4.1 indoor air quality criteria, positioning DINP as a transitional solution where alternative plasticizers cannot yet deliver equivalent durability.

Feedstock Role in Circular Transition via Hydrogenation to DINCH

- An increasingly strategic opportunity for DINP lies upstream rather than downstream. Integrated producers are repositioning DINP as a feedstock for the production of non-phthalate plasticizers through catalytic hydrogenation. BASF has expanded capacity for Hexamoll® DINCH, which is derived directly from DINP using established C9 alcohol supply chains. This pathway allows producers to leverage existing assets while meeting fast-growing demand for DINCH in food contact materials, toys, and sensitive consumer applications, particularly in Asia-Pacific markets.

- At the same time, mass-balance certification is reshaping DINP’s sustainability profile. In mid-2025, Evonik highlighted DINP grades produced under ISCC PLUS frameworks, enabling carbon footprint reductions of up to 70% through renewable and circular feedstock allocation. This positions DINP as a bridge chemistry for industrial sectors that require phthalate-level performance but are under pressure to demonstrate measurable decarbonization progress.

Diisononyl Phthalate (DINP) Market Share and Segmentation Insights

DINP Market Share by Product Type : Industrial Grade Leads While Sustainable DINP Gains Momentum

Industrial grade DINP dominates the global diisononyl phthalate market in 2025 with 72% share, driven by its widespread use as a primary PVC plasticizer in flooring, wire insulation, coated fabrics, and general-purpose vinyl compounds. Its strong balance of flexibility, permanence, processability, and cost efficiency positions industrial grade DINP as the preferred choice for high-volume construction and consumer applications. High purity DINP serves sensitive markets such as medical devices, food-contact materials, and children’s products, where low impurity levels and regulatory compliance are critical for migration control and safety certification. Meanwhile, sustainable DINP, produced from bio-based or recycled feedstocks, represents a small but rapidly expanding segment. Growth is fueled by circular economy initiatives and ESG commitments, particularly across Europe and North America. Manufacturers are accelerating development of renewable-content DINP to meet demand from environmentally conscious brands seeking compliant, low-carbon plasticizer solutions.

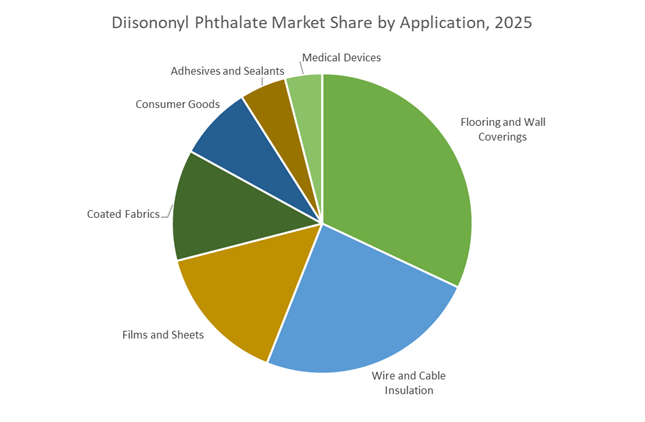

DINP Market Share by Application : Flooring and Wire Insulation Drive High-Volume PVC Demand

Flooring and wall coverings lead DINP consumption with 32% market share, supported by strong demand for luxury vinyl tiles, sheet flooring, and decorative wall panels requiring durability, stain resistance, and long-term flexibility. Wire and cable insulation represents another major segment, using DINP to enhance flame resistance and electrical performance in building wiring, automotive harnesses, and appliance cords. Films and sheets follow closely, covering agricultural films, protective sheeting, and stationery where clarity and flexibility are essential. Coated fabrics for automotive interiors, upholstery, tarpaulins, and protective apparel rely on DINP for weatherability and mechanical strength. Consumer goods such as hoses, footwear, and sporting products maintain steady uptake. Adhesives and sealants form a niche, while medical devices remain a specialized but high-value segment, utilizing high-purity DINP in tubing and fluid containers, although regulatory pressure is accelerating evaluation of non-phthalate alternatives.

Competitive Landscape of the Diisononyl Phthalate (DINP) Market

The Diisononyl Phthalate Market in 2026 is shaped by vertical integration, feedstock security, and accelerating demand from PVC flooring, automotive wiring, construction membranes, and solar infrastructure. Market leaders are strengthening their positions through oxo-alcohol backward integration, circular plasticizer technologies, and region-specific expansion strategies across APAC, Europe, and North America.

BASF drives DINP leadership through Verbund integration and circular plasticizer innovation

BASF SE remains a dominant force in the global DINP plasticizer market, leveraging its world-scale Verbund sites for unmatched cost stability and supply reliability. At Plastindia 2026, BASF highlighted its transition toward the VALERAS® portfolio, integrating DINP with circular economy additives to extend PVC durability in infrastructure and renewable energy applications. A recent oxo-technology licensing agreement with NZRCC strengthens BASF’s internal production of isononyl alcohol (INA), a critical DINP intermediate. Its deep vertical integration, including in-house 2-EHA and INA production in Germany and Malaysia, shields margins from 2026 raw material volatility. BASF is also scaling high-performance stabilizers that work alongside DINP to push product lifecycles beyond 30 years in cables, solar backsheets, and construction plastics.

ExxonMobil expands Jayflex DINP share across automotive electrical and industrial PVC

ExxonMobil Corporation leads the North American DINP market, capitalizing on rising domestic demand and trade tariffs that limited low-cost Asian imports in early 2026. Its flagship Jayflex™ DINP is widely recognized for low volatility and superior thermal stability, making it the benchmark plasticizer for wire and cable insulation. ExxonMobil dominates the automotive electrical segment, where DINP supports complex wiring harnesses required for accelerating EV production. The company’s “Portfolio Resilience” strategy prioritizes long-service-life applications such as roofing membranes, resilient flooring, and industrial PVC, targeting predictable multi-decade performance. Backed by strong feedstock integration and logistics across the US Gulf Coast, ExxonMobil continues to gain share in high-durability plasticizer markets.

Evonik positions VESTINOL 9 DINP for premium applications and circular plastics

Evonik Industries AG differentiates itself as a specialty DINP supplier, emphasizing high-purity grades and circular economy technologies across Europe. Through its Evonik Tailor Made efficiency program (2025–2026), the company streamlined operations at its Marl chemical park to stay competitive against lower-cost DOTP alternatives. Evonik’s VESTINOL® 9 DINP is optimized for sensitive coated fabrics and synthetic leather applications requiring consistent softness and migration resistance. In 2026, Evonik showcased breakthrough hydrolysis technology at the Circular Valley Convention, enabling recovery of raw materials from plasticized foams. Navigating a challenging 15% US tariff environment, Evonik redirected exports toward EMEA and South America, where its quality-to-cost positioning remains strongest.

LG Chem accelerates APAC DINP growth through AI-driven sustainability strategy

LG Chem Ltd. is the Asia-Pacific market leader, rapidly expanding DINP exports into Southeast Asia’s construction hubs, including Singapore and Indonesia. Under its 2026 “Winning Tech” strategy, LG Chem is deploying AI transformation across R&D to develop next-generation eco-efficient plasticizers aligned with evolving REACH and RoHS standards. The company is a major supplier to the consumer electronics sector, where DINP’s insulation performance supports miniaturized 5G hardware and device components. LG Chem’s core advantage lies in exceptional R&D agility, allowing rapid reformulation of phthalate portfolios to meet regulatory shifts. Its technology-driven sustainability roadmap positions the company strongly across APAC infrastructure, electronics, and flexible PVC markets.

UPC Group anchors global DINP volumes through scale and phthalic anhydride integration

UPC Group operates as one of the world’s largest independent DINP producers, serving as a critical volume supplier to the global merchant market. With extensive manufacturing in Mainland China, UPC supports the world’s largest PVC-consuming base with cost-competitive DINP for vinyl flooring and wallcoverings. Deep integration into the phthalic anhydride value chain ensures reliable feedstock access, reinforcing UPC’s role as a preferred partner for high-volume processors. During 2025–2026, approximately 40% of UPC’s production transitioned toward safer, regulation-ready formulations to anticipate stricter global compliance. Its defining strength remains scale and reliability, frequently acting as the backup supplier when vertically integrated majors face operational disruptions.

United States: Risk Management Enforcement and Circular Plasticizer Transition

The United States diisononyl phthalate landscape entered a structurally different phase following the January 2025 Final Risk Evaluation under TSCA. The U.S. Environmental Protection Agency has moved DINP into mandatory risk management, with targeted federal directives focused on spray-applied uses and industrial floor coverings. By 2026, manufacturers and downstream processors are required to implement enhanced vapor recovery systems and upgraded personal protective equipment protocols. This regulatory tightening is reshaping operational practices across compounding and conversion facilities, increasing compliance-related capital expenditure while favoring larger, well-capitalized producers with established EHS frameworks.

Cost pressures have reinforced this structural shift. In January 2025, leading suppliers such as ExxonMobil Chemical and BASF implemented price increases in the range of $0.03–$0.05 per pound across North American DINP grades, reflecting volatility in isononyl alcohol feedstocks and elevated Gulf Coast logistics costs. At the same time, innovation is being used as a strategic hedge. BASF’s February 2025 launch of Ccycled® DINP grades introduced biomass-balanced and circular feedstock pathways using pyrolysis oil derived from mixed plastic waste, enabling up to a 50% reduction in product carbon footprint. Demand fundamentals remain resilient in automotive interiors and infrastructure wiring. With the average North American vehicle now incorporating roughly 426 pounds of plastics, OEMs are increasing DINP procurement for vibration-tolerant EV cabin components, while Infrastructure Investment and Jobs Act funding is driving strong pull for DINP-plasticized wire and cable insulation in nationwide 5G rollouts. However, competitive pressure is intensifying as suppliers such as Dow accelerate the commercialization of phthalate-free plasticizers for medical and other high-sensitivity applications.

China: Feedstock Self-Sufficiency and Urban Infrastructure Pull

China’s DINP market is being reshaped by a combination of feedstock localization policies and large-scale urban renewal demand. The 2025 Catalogue of Encouraged Industries for Foreign Investment issued by the National Development and Reform Commission and the Ministry of Commerce explicitly promotes foreign participation in advanced plasticizer manufacturing and high-purity petrochemical intermediates, particularly in central and western provinces. This policy direction is already translating into tangible capacity development. A notable example is BASF’s oxo-technology licensing agreement with Ningbo Refining and Chemical Co. Ltd, finalized in late 2024 to early 2025, which significantly strengthens domestic isononyl alcohol availability and reduces China’s dependence on imported DINP precursors.

On the demand side, the market is supported by infrastructure-driven consumption. China’s New Urbanization guidelines for 2025–2026 emphasize large-scale replacement of aging residential plumbing and electrical systems, creating a government-backed preference for long-chain phthalates such as DINP in pipes, cables, and flexible construction materials. This structural demand is reinforced by progress at the SABIC Fujian petrochemical complex, a $6.4 billion project entering final mechanical completion in 2026, which will supply world-scale ethylene and derivative plasticizer units to serve flexible PVC demand in the Greater Bay Area. Sustainability is emerging as a parallel theme. In August 2025, BASF and UPC Technology Corp. signed an MoU to co-develop lower-carbon plasticizer alcohols and deploy emission-reduction technologies across Asian manufacturing sites. At the same time, updates to China’s Export Control Catalogue in November 2025 have increased compliance complexity for high-performance chemical intermediates, forcing DINP producers to strengthen documentation and traceability to maintain access to European and North American automotive supply chains.

Germany and the European Union: Specialty Positioning Under Regulatory Tightening

In Germany, the diisononyl phthalate market is undergoing consolidation and repositioning rather than outright expansion. Facing persistently high energy costs and a reported decline in overall chemical production in 2025, domestic producers are shifting away from commodity DINP grades toward specialty and high-purity variants used in medical-grade PVC and precision automotive components. This move aligns with tightening EU regulatory expectations, particularly Regulation (EU) 2024/2865, which introduces new physical and digital labeling requirements for hazardous chemicals from July 2026. German manufacturers are already investing in dual-format labeling systems to ensure full traceability and Digital Product Passport readiness across the EU supply chain.

Circularity and substitution dynamics are also influencing strategy. In September 2025, Evonik launched its Next Markets Program, including pilot projects to convert polyolefin-based mixed waste into pyrolysis oils suitable for sustainable plasticizer production. These initiatives support DINP’s continued relevance in applications where PFAS-based additives are being phased out under expanding EU restrictions. Additionally, announced increases in German defense and national infrastructure spending for 2026 are expected to revive domestic demand for high-performance DINP in military-grade tents, protective coatings, and specialized wiring. Collectively, the German market is evolving toward lower-volume but higher-value DINP consumption, underpinned by compliance leadership and circular feedstock experimentation.

India: Localization Incentives and Construction-Led Volume Growth

India’s DINP market is primarily being driven by policy-led localization and large-scale infrastructure development. By June 2025, the Production Linked Incentive scheme had realized investments exceeding ₹1.88 lakh crore, with chemicals and petrochemicals among the core beneficiary sectors. New incentives are explicitly targeting the domestic manufacture of DINP and DIDP to reduce reliance on imports from East Asia. This policy support is coinciding with strong downstream demand from construction and urban development programs. The Housing for All and Smart Cities initiatives have significantly increased consumption of PVC-based flooring, wall coverings, and flexible building materials, much of which relies on DINP plasticization for durability and processability.

Industrial stability is reinforcing this demand base. Growth in India’s Index of Eight Core Industries during late 2025 has supported steady consumption of DINP in wire and cable manufacturing, a segment that accounts for a substantial share of regional plasticizer use. Looking ahead, regulatory standardization will play a larger role. The Ministry of Chemicals and Fertilizers is preparing to introduce mandatory BIS certification for imported plasticizers by mid-2026, a move designed to harmonize quality standards across consumer goods, toys, and construction materials. This is expected to favor compliant domestic producers while raising entry barriers for lower-quality imports.

Snapshot Summary: Diisononyl Phthalate Market by Country

Diisononyl Phthalate (DNP) Market County Level Snapshot

|

Region

|

Strategic Focus

|

Policy or Industry Driver

|

Market Implication

|

|

United States

|

Risk management and circular feedstocks

|

TSCA mandates, Infrastructure Act

|

Higher compliance costs, resilient automotive and cable demand

|

|

China

|

Feedstock self-sufficiency

|

Oxo-technology licensing, urban renewal

|

Strong domestic DINP production and construction-led consumption

|

|

Germany / EU

|

Specialty repositioning

|

REACH 2.0, PFAS restrictions

|

Shift toward high-purity DINP and circular plasticizers

|

|

India

|

Localization and infrastructure

|

PLI scheme, Smart Cities

|

Volume growth in construction and cables, reduced import reliance

|

Diisononyl Phthalate (DNP) Market Report Scope

Diisononyl Phthalate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.4 Billion

|

|

Market Size (2034)

|

$8 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Product Type (Industrial Grade, High Purity Grade, Sustainable Grade), By Formulation Type (Liquid Plasticizers, Masterbatch Compounds), By Application (Flooring and Wall Coverings, Wire and Cable Insulation, Films and Sheets, Coated Fabrics, Consumer Goods, Medical Devices, Adhesives and Sealants), By End-User Industry (Building and Construction, Automotive and Transportation, Electrical and Electronics, Healthcare and Pharmaceuticals, Textiles and Apparel, Packaging and Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exxon Mobil Corporation, BASF SE, Evonik Industries AG, UPC Technology Corporation, Nan Ya Plastics Corporation, LG Chem Ltd., Mitsubishi Chemical Group Corporation, KLJ Group, Aekyung Chemical Co., Ltd., Azelis Group NV, Hallstar Company, Polynt S.p.A., Valtris Specialty Chemicals, LANXESS AG, GP Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diisononyl Phthalate Market Segmentation

By Product Type

- Industrial Grade

- High Purity Grade

- Sustainable Grade

By Formulation Type

- Liquid Plasticizers

- Masterbatch Compounds

By Application

- Flooring and Wall Coverings

- Wire and Cable Insulation

- Films and Sheets

- Coated Fabrics

- Consumer Goods

- Medical Devices

- Adhesives and Sealants

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Electrical and Electronics

- Healthcare and Pharmaceuticals

- Textiles and Apparel

- Packaging and Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diisononyl Phthalate Industry

- Exxon Mobil Corporation

- BASF SE

- Evonik Industries AG

- UPC Technology Corporation

- Nan Ya Plastics Corporation

- LG Chem Ltd.

- Mitsubishi Chemical Group Corporation

- KLJ Group

- Aekyung Chemical Co., Ltd.

- Azelis Group NV

- Hallstar Company

- Polynt S.p.A.

- Valtris Specialty Chemicals

- LANXESS AG

- GP Group

*- List not Exhaustive