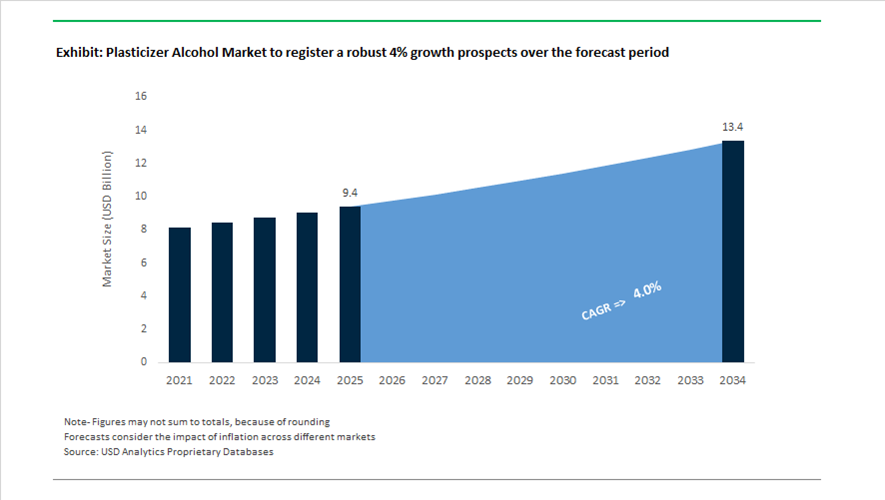

Plasticizer Alcohol Market Size 2025–2034: $9.4 Billion to $13.4 Billion at 4% CAGR Driven by Oxo-Alcohol Localization and Circular Feedstock Integration

The global plasticizer alcohol market is projected to grow from $9.4 billion in 2025 to $13.4 billion by 2034, registering a CAGR of 4%. Plasticizer alcohols—primarily 2-ethylhexanol (2-EH), n-butanol, isobutanol, and isononanol—serve as essential intermediates in the production of phthalate and non-phthalate plasticizers used in PVC flooring, cables, automotive interiors, construction materials, and synthetic leather. Market growth is supported by infrastructure expansion in Asia-Pacific, resilient demand for flexible PVC in energy and construction, and gradual diversification toward higher-performance and bio-based alcohol derivatives. However, pricing remains highly sensitive to propylene feedstock volatility, regional supply-demand imbalances, and energy costs.

Localization of Oxo-alcohol production capacity is reshaping supply chains. In August 2024, BASF and UPC Technology Corporation signed a memorandum of understanding to secure long-term supply of 2-EH and n-butanol for South China’s growing plasticizer sector. This strategy aligns with BASF’s upcoming 2025 startup of its Oxo-alcohol plant at the Zhanjiang Verbund site, which will serve as a regional hub for 2-EH and C4 alcohol production. The Zhanjiang investment reduces import dependency for mainland China and strengthens integration between upstream propylene derivatives and downstream plasticizer manufacturing.

Pricing dynamics intensified across 2025–2026 in the Americas. In February 2025, Eastman implemented a $0.05 per pound off-list increase for 2-ethylhexanol, n-butanol, and n-isobutyl alcohol, citing elevated operating costs and raw material volatility. Additional price adjustments followed in May 2025 and March 2026 for specialty plasticizer derivatives such as TOTM. Similarly, effective February 1, 2026, BASF increased North American prices for Oxo-C4 alcohols, raising n-butanol by $0.07/lb and 2-EH and isobutanol by $0.05/lb due to tightening supply conditions and feedstock pressures. These sequential increases highlight ongoing cost pass-through strategies in a margin-sensitive intermediates market.

Circular feedstock initiatives are gradually influencing long-term positioning. In late 2024, ExxonMobil announced over $200 million in investments to expand advanced recycling capacity at Baytown and Beaumont. By converting plastic waste into virgin-quality chemical intermediates, such initiatives may provide alternative hydrocarbon feedstocks for Oxo-alcohol production, reducing reliance on fossil-based inputs. In 2025, ICL Group demonstrated industrial-scale implementation of Puraloop® recycled precursor technology, signaling future integration of circular intermediates into stabilizer and alcohol derivative value chains.

Producers are also shifting toward higher-performance niches. In February 2026, Evonik announced expansion of its hydroxyl-terminated polybutadiene (HTPB) infrastructure, reflecting broader industry interest in specialty alcohol derivatives offering enhanced durability and UV resistance compared to commodity plasticizers. Evonik’s adoption of a dynamic dividend policy in 2026 also underscores cautious capital allocation amid challenging macroeconomic conditions for chemical intermediates.

Key Trends and High-Value Opportunities in the Plasticizer Alcohol Market

Structural Pivot to Non-Phthalate and Sustainable Plasticizer Alcohol Capacity

The plasticizer alcohol market is undergoing a structural realignment as regulatory pressure accelerates the shift away from legacy phthalates toward non-phthalate alternatives such as Dioctyl Terephthalate (DOTP), Diisononyl Cyclohexane Dicarboxylate (DINCH), and other terephthalate-based systems. This transition has materially altered demand patterns for key alcohols, particularly 2-Ethylhexanol (2-EH) and Isononyl Alcohol (INA), which now serve as critical feedstocks for “safe” plasticizer formulations compliant with EU REACH, U.S. TSCA, and emerging Asian chemical safety frameworks.

Capital investment is increasingly concentrated in large, integrated production complexes capable of flexibly allocating output between conventional oxo-alcohols and higher-value specialty grades. A defining milestone occurred in August 2024, when BASF signed a Memorandum of Understanding with UPC Technology Corporation to supply 2-Ethylhexanol and N-Butanol from its Zhanjiang Verbund site in China. Scheduled to come online in 2025, this facility directly targets surging South China demand for phthalate-free PVC compounds, particularly in wire and cable insulation, flooring, and synthetic leather. The strategic value of such Verbund-scale assets lies in their ability to stabilize regional supply while meeting increasingly stringent purity and sustainability specifications.

In parallel, sustainability credentials have moved from marketing differentiators to procurement requirements. By late 2024, leading plasticizer alcohol producers began institutionalizing Biomass Balance (BMB) offerings under ISCC PLUS certification. Through mass-balance integration of renewable feedstocks, suppliers can deliver alcohols with significantly lower carbon footprints without requiring downstream processors to modify established PVC compounding workflows. This approach has gained traction among multinational flooring and automotive OEMs seeking Scope 3 emission reductions while preserving cost competitiveness.

Diversification into High-Performance Synthetic Intermediates Beyond PVC

While PVC plasticizers remain the largest outlet for plasticizer alcohols, market resilience in 2025 is increasingly underpinned by diversification into non-PVC chemical intermediates. The consumption of 2-Ethylhexanol and isononyl alcohol in lubricants, surfactants, acrylates, and specialty esters has emerged as a stabilizing force, reducing producer exposure to the cyclical nature of construction and real estate markets.

Industry data from early 2025 indicates that demand for 2-EH as a precursor for synthetic lubricants and high-performance surfactants has accelerated, driven by growth in automotive fluids, industrial detergents, and low-foaming cleaning formulations. Applications such as 2-EH nitrate and 2-EH-based acrylates are expanding faster than traditional plasticizer demand, supported by stricter efficiency and performance requirements in both consumer and industrial formulations.

Specialty adhesives and sealants represent another structurally important demand vector. The transition toward lightweight vehicle architectures and multi-material assemblies has increased reliance on alcohol-derived ester plasticizers that deliver superior flexibility, vibration damping, and adhesion. In 2025, these applications have elevated certain plasticizer alcohols from commodity inputs to performance-critical intermediates, particularly in automotive, electronics, and construction sealant systems where long-term durability is non-negotiable.

Circular Economy Enablement Through Chemical Recycling of PET into Plasticizers

One of the most compelling sustainability-driven opportunities in the plasticizer alcohol market is the chemical recycling of Polyethylene Terephthalate (PET) waste into high-purity plasticizers. This open-loop recycling pathway utilizes 2-Ethylhexanol to convert post-consumer PET into Dioctyl Terephthalate, creating a circular, drop-in plasticizer solution for flexible PVC applications.

A comprehensive study published in September 2025 evaluated this process at scale and reported a greenhouse gas emission profile of minus 0.88 tonnes of CO₂-equivalent per tonne of PET processed. This negative emissions outcome positions PET-to-DOTP conversion as a materially superior alternative to incineration or virgin terephthalate synthesis. As regulatory scrutiny on plastic waste intensifies, this route offers a rare convergence of environmental benefit and economic viability.

Investment momentum supports this opportunity. In Europe alone, planned capital expenditure in chemical recycling infrastructure is projected to rise from €2.6 billion in 2025 to approximately €8 billion by 2030. This expansion directly underpins future demand for plasticizer alcohols as enabling reagents in circular material flows, aligning with the EU Green Deal and the Circular Plastics Alliance objective of integrating 10 million tonnes of recycled plastics into European products.

Scaling 2-Ethylhexyl Acrylate for Advanced Coatings and Impact Modifiers

The downstream expansion of 2-Ethylhexyl Acrylate (2-EHA) represents a structurally durable growth opportunity for plasticizer alcohol producers. 2-EHA is a key co-monomer in high-performance acrylic polymers used in weather-resistant coatings, pressure-sensitive adhesives, and impact modifiers for rigid and flexible PVC.

In November 2025, Dow Chemical announced an expansion of its 2-EHA production capacity to address double-digit demand growth from global adhesives and coatings markets. Concurrently, BASF introduced new generations of sustainable acrylic polymers incorporating 2-EHA to improve flexibility, UV resistance, and durability in architectural coatings. These developments reflect the growing strategic importance of 2-EHA as construction, infrastructure, and renovation activity rebounds across emerging economies.

Regulatory pressure on Volatile Organic Compounds continues to accelerate the transition toward waterborne coatings systems. Within these formulations, 2-EHA plays a critical role in film formation, adhesion, and low-temperature performance. As urbanization intensifies in India and Southeast Asia, demand for waterborne, low-VOC coatings is expected to remain structurally strong through 2032, anchoring long-term consumption of plasticizer alcohol-derived acrylates.

Plasticizer Alcohol Market Share and Segmentation Insights

2-Ethylhexanol Leads Plasticizer Alcohol Production in Global Plasticizer Manufacturing

2-Ethylhexanol accounted for 42.80% of the Plasticizer Alcohol Market by alcohol type in 2025, reflecting its central role as the primary feedstock for high-volume plasticizer production. This alcohol is widely used in the manufacture of di-2-ethylhexyl phthalate and di-2-ethylhexyl terephthalate plasticizers applied in flexible PVC products across construction, automotive, and consumer goods industries. The large-scale global production of plasticizers continues to sustain strong demand for 2-ethylhexanol as a key chemical intermediate. In 2025, the transition from phthalate plasticizers to terephthalate-based plasticizers such as DOTP is influencing demand patterns, with 2-ethylhexanol increasingly used in non-phthalate plasticizer manufacturing as regulatory restrictions reshape plasticizer markets in developed economies.

Phthalate Plasticizers Segment Drives Plasticizer Alcohol Consumption in Flexible PVC Manufacturing

Phthalate plasticizers represented 48.60% of the Plasticizer Alcohol Market by application in 2025, reflecting their widespread use in flexible PVC formulations used in cables, flooring materials, films, and synthetic leather products. These plasticizers provide flexibility, durability, and processability in polymer materials used across infrastructure, packaging, and industrial applications. Despite regulatory pressure in certain regions, phthalate plasticizers continue to dominate global consumption due to their performance and cost advantages. In 2025, regional divergence in phthalate plasticizer regulations is shaping global demand patterns, with growth in Asia and Latin America offsetting declines in regulated markets where non-phthalate alternatives are gaining share.

Plasticizer Alcohol Market Competitive Landscape

The global plasticizer alcohol market is transitioning toward high molecular weight (HMW) alcohols such as INA and 2-PH, supported by non-phthalate plasticizer demand and large-scale Oxo-alcohol integration. Competitive dynamics are shaped by Verbund investments, circular feedstocks, and regulatory-driven shifts toward low-VOC, REACH-compliant solutions.

BASF Scales Low-Carbon Oxo-Alcohol Production with Zhanjiang Verbund Integration

BASF SE is expanding its leadership in plasticizer alcohols through its €10 billion Zhanjiang Verbund project, positioning it as a major supply hub in Asia. The new Oxo-alcohol plant, scheduled for 2025–2026 startup, will supply 2-Ethylhexanol (2-EH) and N-Butanol under a strategic MoU with UPC Technology. The company is integrating Biomass Balance (BMB) certified alcohols to reduce Scope 3 emissions for downstream PVC applications. Its portfolio includes 2-EH, N-Butanol, and 2-Propylheptanol (2-PH), widely used in high-performance, weather-resistant PVC. The Verbund system ensures feedstock efficiency and cost optimization through integrated production. Strategy focuses on low-carbon manufacturing, regional supply security, and high-performance plasticizer intermediates.

Eastman Expands Non-Phthalate Plasticizer Portfolio with Integrated Oxo-Alcohol Supply

Eastman Chemical Company is prioritizing specialty plasticizers and circular economy feedstocks, supported by its Oxo-alcohol integration. The company reported $8.8 billion in revenue in 2025, driven by its Additives & Functional Products segment. Price increases of $0.05/lb in March 2026 reflect rising feedstock and logistics costs. Eastman 168™ (DOTP), based on high-purity 2-EH, is positioned as a benchmark for medical, childcare, and sensitive applications. Expansion of Oxo-alcohol derivative production in Texas strengthens captive supply and reduces exposure to market volatility. Strategy emphasizes non-phthalate plasticizers, feedstock integration, and high-value specialty applications.

Evonik Leads Isononyl Alcohol Innovation for High-Performance and Low-Migration Plasticizers

Evonik Industries AG is a key player in high molecular weight alcohols, particularly isononyl alcohol (INA) used in DINP and DINCH plasticizers. The company reaffirmed a 2026 EBITDA outlook of €1.7–2.0 billion, supported by strong performance in additives and performance materials. Its vertical integration from butene dimerization to INA production ensures consistent high purity and supply reliability. ELATUR® CH plasticizer technology, based on INA, targets low-migration applications such as food contact materials. Product development focuses on C10+ alcohols for automotive, construction, and specialty PVC applications. Strategy centers on high-performance alcohols, regulatory compliance, and specialty plasticizer innovation.

LG Chem Expands High-Value PVC and Plasticizer Alcohol Integration for EV and Sustainable Applications

LG Chem is strengthening its plasticizer alcohol position through integration with high-performance PVC and sustainable materials. The company maintains significant 2-EH production capacity in South Korea, supporting both internal PVC production and external markets. Collaboration with EL Electric enables development of flame-retardant EV charging cables requiring advanced plasticizer systems for enhanced flexibility. Sustainability initiatives include Zero Waste to Landfill (ZWTL) Platinum certification across key facilities. The Nexula™ platform introduces advanced materials leveraging branched-chain alcohol chemistry. Strategy focuses on eco-friendly materials, EV-ready applications, and integrated polymer-alcohol value chains.

ExxonMobil Strengthens High-Carbon Alcohol Portfolio with Integrated Oxo Supply and Advanced Catalysis

ExxonMobil Product Solutions is a major producer of high-carbon alcohols through its Exxal™ portfolio (C8–C13). These branched alcohols are critical for low-volatility plasticizers used in automotive wiring and industrial applications. Its isononyl alcohol (INA) supports production of Jayflex™ DINP, benefiting from regulatory shifts away from low-molecular-weight phthalates. The company operates highly integrated Oxo-alcohol supply chains in Baton Rouge and Rotterdam, ensuring global supply security. Investments in advanced hydroformylation catalysts improve production efficiency and reduce energy intensity. Strategy emphasizes scale, integration, and high-performance plasticizer alcohol supply.

OQ Chemicals Expands Global Oxo-Intermediates Supply with Integrated Value Chain and Digital Logistics

OQ Chemicals (formerly Oxea) operates as a key supplier of Oxo-alcohol intermediates for global plasticizer production. The company maintains large-scale facilities in Germany and the United States, focusing on merchant markets for 2-EH and N-Butanol. Integration with parent company OQ ensures competitive feedstock sourcing and pricing stability. Its 2-EH is widely used in 2-ethylhexyl acrylate production, supporting demand in adhesives and water-borne coatings. Digital logistics initiatives introduced in 2025 improve supply chain efficiency across Latin America and Asia. Strategy focuses on high-purity intermediates, global supply reliability, and downstream application growth.

India Plasticizer Alcohol Market– Feedstock Localization and Compliance-Led Market Reorientation

India’s plasticizer alcohol industry is entering a structurally transformative phase, driven by upstream petrochemical investments, regulatory traceability, and an export-oriented policy stance. A pivotal inflection point is the Paradip petrochemical expansion, where Indian Oil Corporation is investing over ₹61,000 crore to build specialized refining and downstream units. These assets are designed to secure domestic availability of oxo-alcohol feedstocks critical for 2-Ethylhexanol and related plasticizer alcohols. In parallel, private-sector debottlenecking initiatives in 2025 have expanded domestic 2-EH capacity, directly addressing India’s 40% import dependence for flexible PVC cables, wires, and medical-grade tubing.

Regulation and infrastructure are acting as dual demand accelerators. The Plastic Parks Scheme, with 10 parks being finalized across Karnataka and Assam, is creating shared effluent treatment and utilities tailored for alcohol-based plasticizer users. At the same time, the July 2025 digital traceability mandate under Plastic Waste Management Rules has forced producers to implement QR-linked and blockchain-enabled batch tracking, raising compliance costs but improving export readiness. On the demand side, the NRDC’s April 2025 launch of BioSHEAL paper-based labels is subtly reshaping plasticizer consumption in excise and liquor packaging, favoring higher-purity specialty alcohols. The Ministry of Commerce’s 2027 export roadmap, targeting $25 billion in plastic-related exports, further positions India as a future supplier of medical- and food-contact-grade plasticizer alcohols.

Germany Plasticizer Alcohol Market– Low-Carbon Oxo Alcohol Leadership through Verbund Optimization

Germany continues to anchor Europe’s plasticizer alcohol value chain through capital-intensive Verbund optimization and catalyst-driven decarbonization. In December 2025, BASF committed to annual investments of €1.5–2 billion at Ludwigshafen through 2028, with the C4 Verbund upgrade explicitly targeting higher-yield and energy-efficient production of 2-Ethylhexanol and Isononanol. These investments are structurally improving Europe’s supply security for PVC plasticizers, coatings, and specialty surfactants.

Catalyst and circularity innovations are reinforcing this advantage. Evonik and BASF jointly rolled out SYNSPIRE catalysts in 2025, cutting steam consumption by roughly 40,000 metric tons per year during oxo-alcohol synthesis. German R&D has also commercialized INA-based biodegradable surfactants, opening adjacent demand channels beyond plasticizers. Life cycle management initiatives introduced in 2025 are integrating recycled and biomass-derived feedstocks into oxo-alcohol chains, enabling certified low-carbon and drop-in 2-EH production by early 2026. This positions Germany as the benchmark supplier for low-PCF plasticizer alcohols in regulated European markets.

China Plasticizer Alcohol Market– Capacity Scale-Up under Green and Medical Compliance Pressure

China’s plasticizer alcohol landscape is characterized by large-scale integration, regulatory tightening, and a decisive shift toward higher-purity alcohols. During 2024–2025, players such as Nan Ya Plastics implemented high-efficiency catalyst systems that eliminated an estimated 38,000 metric tons of CO₂ annually while sustaining record 2-EH output. These upgrades align with the final phase of the 14th Five-Year Plan, which prioritizes intelligent and green chemical production and accelerates the phase-out of coal-based calcium carbide PVC routes.

Capacity additions are being strategically aligned with premium end uses. The August 2025 commissioning of a second Cangzhou production line for alcohol-derivative additives strengthened supply for high-end nylon and PVC applications. Meanwhile, BASF’s Zhanjiang Verbund startup in 2025, powered entirely by renewable electricity, has materially increased regional availability of plasticizer alcohols in southern China. Regulatory pressure is intensifying demand shifts, as late-2025 tightening by the National Medical Products Administration on phthalate migration in medical devices is accelerating substitution toward non-phthalate alcohols such as DOTP-compatible feedstocks.

United States Plasticizer Alcohol Market– Pricing Discipline and Application-Led Diversification

The U.S. plasticizer alcohol market in 2025 reflects a combination of pricing discipline, regulatory adaptation, and diversification into adjacent applications. In May 2025, Eastman Chemical Company implemented a $0.11/kg price increase across 2-Ethylhexanol, n-Butanol, and Isobutanol, citing persistent raw material volatility and operating cost inflation. Despite this, downstream demand has remained resilient due to structural shifts in packaging, automotive, and energy applications.

Regulatory developments are opening secondary demand pools. State-level PFAS bans in packaging, notably in Minnesota and Rhode Island, are forcing reformulation of barrier coatings, increasing reliance on alcohol-based plasticizers in compliant films. In the energy segment, the rollout of TOP TIER+ gasoline standards in 2025 has created incremental demand for specialty alcohols as blending and performance components. Eastman’s December 2025 announcement that its alcohol-derived advanced interlayers are now used in 50% of new EV models underscores the growing role of plasticizer alcohols in acoustic and thermal insulation. Looking ahead, U.S. investments in methanol-to-alcohol pathways using captured carbon are positioning circular feedstocks as a 2026 growth lever.

Saudi Arabia Plasticizer Alcohol Market– Crude-to-Chemicals Integration for Export-Oriented Growth

Saudi Arabia is emerging as a strategic production and blending hub for plasticizer alcohols, underpinned by crude-to-chemicals integration and additive system investments. In October 2025, Songwon Industrial announced a One Pack Systems facility in the Kingdom, which will consume significant volumes of plasticizer alcohols to support regional polyolefin compounding. This investment enhances local value addition and reduces dependence on imported additive blends across the GCC.

At the upstream level, Vision 2030 has fast-tracked the Yanbu Crude-to-Chemicals project, incorporating integrated C8–C10 alcohol units aimed at export markets in Asia, Africa, and Europe. These assets leverage the Kingdom’s cost-advantaged feedstocks to supply competitively priced plasticizer alcohols, positioning Saudi Arabia as a structurally important swing supplier in the global market.

Comparative Snapshot – Plasticizer Alcohol Industry by Country

Plasticizer Alcohol Market County Level Snapshot

|

Country

|

Core Growth Driver

|

Strategic Focus

|

Market Positioning

|

|

India

|

Feedstock localization and digital compliance

|

2-EH expansion, export-grade purity

|

Emerging manufacturing hub

|

|

Germany

|

Energy efficiency and decarbonization

|

Low-carbon 2-EH and INA

|

Technology and sustainability leader

|

|

China

|

Scale expansion with medical compliance

|

High-purity alcohols, green production

|

High-volume premium supplier

|

|

United States

|

Application diversification

|

EV interlayers, PFAS-free packaging

|

Value-added specialty market

|

|

Saudi Arabia

|

Crude-to-chemicals integration

|

C8–C10 alcohol exports

|

Cost-advantaged export hub

|

Plasticizer Alcohol Market Report Scope

Plasticizer Alcohol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.4 Billion

|

|

Market Size (2034)

|

$13.4 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Alcohol Type (2-Ethylhexanol, Isononanol, N-Butanol, Isobutanol, 2-Propylheptanol, Isodecanol), By Application (Phthalate Plasticizers, Non-Phthalate Plasticizers, Solvents & Extraction Agents, Surfactants & Detergents, Lubricant Additives, Acrylates & Esters), By End-Use Industry (Building & Construction, Automotive, Medical & Healthcare, Packaging, Consumer Goods, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, Eastman Chemical Company, ExxonMobil Product Solutions, LG Chem Ltd., SABIC, Nan Ya Plastics Corporation, INEOS Group, UPC Group, Sibur, Formosa Plastics Corporation, Mitsubishi Chemical Group, Indo-Nippon Chemical Co. Ltd., Sasol Limited, Perstorp Holding AB

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plasticizer Alcohol Market Segmentation

By Alcohol Type

- 2-Ethylhexanol

- Isononanol

- N-Butanol

- Isobutanol

- 2-Propylheptanol

- Isodecanol

By Application

- Phthalate Plasticizers

- Non-Phthalate Plasticizers

- Solvents & Extraction Agents

- Surfactants & Detergents

- Lubricant Additives

- Acrylates & Esters

By End-Use Industry

- Building & Construction

- Automotive

- Medical & Healthcare

- Packaging

- Consumer Goods

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Plasticizer Alcohol Industry

- BASF SE

- Evonik Industries AG

- Eastman Chemical Company

- ExxonMobil Product Solutions

- LG Chem Ltd.

- SABIC

- Nan Ya Plastics Corporation

- INEOS Group

- UPC Group

- Sibur

- Formosa Plastics Corporation

- Mitsubishi Chemical Group

- Indo-Nippon Chemical Co. Ltd.

- Sasol Limited

- Perstorp Holding AB

*- List not Exhaustive