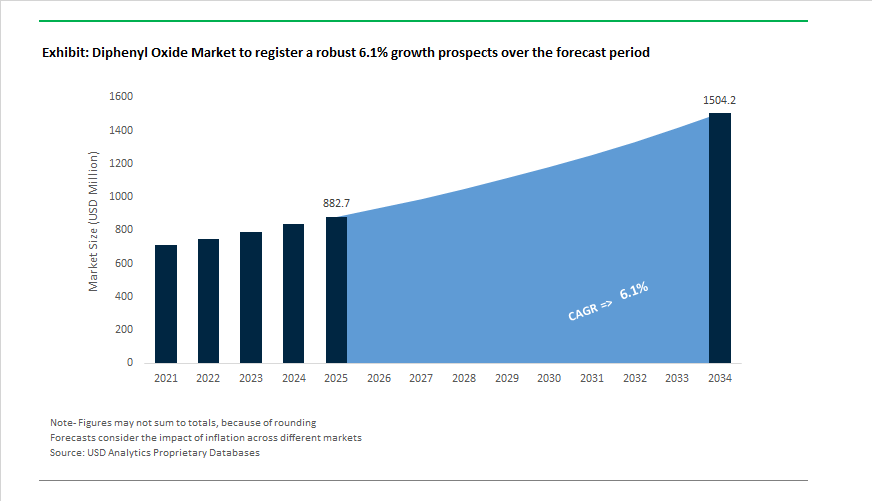

Diphenyl Oxide Market to Reach $1,504 Million by 2034 at 6.1% CAGR Driven by Heat Transfer Fluids, Fragrance Expansion, and Electronic-Grade Demand

The Diphenyl Oxide (DPO) Market is projected to grow from $882.7 Million in 2025 to $1,504 Million by 2034, registering a CAGR of 6.1%. Market expansion is underpinned by accelerating demand for high-temperature heat transfer fluids, aroma chemicals, flame-retardant intermediates, and electronic-grade aromatic ethers. In 2025, Jiangsu Zhongneng commissioned a new 10,000-ton DPO production facility in China, strengthening Asia’s supply base for eutectic DPO-biphenyl blends used in chemical processing and renewable energy plants. This capacity addition aligns with the increasing deployment of Concentrated Solar Power systems, where DPO mixtures operate at temperatures up to 400°C, enabling efficient thermal energy storage and grid stabilization.

Fragrance and personal care applications remain a structural demand pillar for high-purity Diphenyl Oxide. In Q1 2026, Givaudan announced an expansion of its Singapore production capacity to address rising Asia-Pacific consumption in laundry care and fine fragrance formulations. This followed its $110 million investment in February 2026 in a new compounding facility in Mexico, aimed at strengthening Latin American supply of DPO-based fragrance fixatives known for their geranium-like scent profile and high thermal stability. Simultaneously, the broader aromatic chemical value chain experienced strategic restructuring. Dow executed a 6% global workforce reduction through 2025, rationalizing its industrial intermediates portfolio to sustain cost competitiveness. Lanxess advanced its FORWARD! program targeting €150 million in annual savings by end-2025, optimizing its additives and intermediates network. In late 2025, BASF initiated a portfolio overhaul and agrochemical spin-off under its new leadership, reaffirming a core focus on industrial solutions and personal care chemistries that directly consume DPO derivatives. Eastman’s Kingsport molecular recycling facility also reported record performance in 2025, generating 2.5 times more recycled output than in 2024, supporting sustainable aromatic feedstock availability.

Regulatory compliance and high-performance specialization are reshaping product specifications. In January 2026, industry-wide adoption of tin-free catalyst synthesis accelerated to comply with updated REACH safety standards, particularly for food-contact packaging and electronics-grade applications. Between 2024 and 2025, manufacturers reported a sharp increase in demand for Ultra-High Purity (>99.7%) Diphenyl Oxide, driven by its role as a high-resistance solvent in electronic coatings and advanced polymer systems for 5G infrastructure. The material’s low volatility and exceptional thermal stability make it critical in high-frequency signal environments. Supporting this trend, the Dahej PCPIR project in India secured ₹300–360 crore in February 2026 to expand specialty chemical intermediate production, including aromatic ethers, reinforcing India’s export ambitions. These supply expansions and regulatory-driven product upgrades position Diphenyl Oxide as a strategic intermediate across renewable energy, high-performance electronics, and premium fragrance markets while global producers recalibrate toward high-purity and sustainable production pathways.

Trends and Opportunities Defining the Diphenyl Oxide (DPO) Market

DPO as a Non-Substitutable Heat Transfer Fluid for Concentrated Solar Power

- Diphenyl Oxide remains the backbone of high-temperature heat transfer fluid systems used in Concentrated Solar Power installations, particularly in parabolic trough and hybrid thermal storage designs. Its ability to maintain thermal stability up to 400°C positions it as the industry standard for projects designed with 25-year operational lifespans.

- China is now the epicenter of this demand surge. According to the 2025 Blue Book of China’s Concentrating Solar Power Industry, the country had 8.1 GW of CSP capacity either operational or under development by early 2025. This pipeline alone exceeds total global installed CSP capacity recorded in 2024, creating localized but very high-volume demand for DPO and DPO-biphenyl eutectic blends. Domestic sourcing and long-term supply assurance are becoming strategic priorities for Chinese EPCs and state-owned utilities.

- At the technical level, CSP operators are tightening impurity specifications. Studies published in October 2025 highlight a clear industry shift toward ultra-low chlorine DPO, with thresholds below 0.2 ppm now specified to prevent chloride-induced stress corrosion cracking in carbon steel receivers and piping. This trend is directly linked to the operational benchmarks set by large hybrid projects, including the 700 MW Yumen hybrid CSP installation completed in September 2024, which demonstrated the role of high-purity DPO systems in stabilizing intermittent renewable power through thermal storage.

Decoupling from Energy Cycles Through PAEK Polymer Demand

- Beyond energy, DPO demand is increasingly anchored in advanced materials manufacturing, where it serves as the critical ether linkage precursor for Polyaryletherketone polymers. This structural role is making DPO consumption more resilient and less exposed to short-term energy investment cycles.

- In aerospace applications, Polyetherketoneketone adoption accelerated sharply in 2025. Industry reports released in December 2025 indicate that PEKK now accounts for approximately 35% of all high-performance thermoplastic usage in aerospace, driven by aggressive lightweighting targets. Components produced using DPO-derived polymers enable 15 to 20% weight reduction compared with titanium while maintaining mechanical integrity under extreme thermal and chemical stress.

- Medical technology is reinforcing this trend. Medical-grade PEEK and PEKK materials derived from DPO are increasingly specified for spinal cages, dental implants, and surgical instruments due to their radiolucency, MRI compatibility, and sterilization resistance. In late 2025, multiple global med-tech manufacturers began integrating DPO-based polymers into new implant and tool portfolios, further anchoring demand in regulated, high-margin end markets.

High-Temperature Fluids for Advanced Nuclear and Hydrogen Systems

- Advanced nuclear reactor designs represent a blue-ocean opportunity for Diphenyl Oxide beyond solar thermal applications. Policy frameworks released by the International Atomic Energy Agency in 2025 confirm renewed global momentum behind Small Modular Reactors and Advanced High-Temperature Reactor concepts, many of which require stable, non-aqueous secondary heat transfer fluids.

- DPO-based fluids are being evaluated for secondary heat loops in these systems, particularly where process heat is transferred for hydrogen production or industrial cogeneration. Their ability to operate at low system pressures while maintaining stability at temperatures exceeding 700°C in intermediate exchangers offers a clear advantage over helium-cooled or water-based systems. From a safety perspective, the non-aqueous nature of DPO mixtures reduces the risk of high-pressure failures and enables more passive cooling architectures, aligning with next-generation nuclear safety philosophies.

Bio-Derived DPO from Lignin as a Decarbonization Lever

- Sustainability is emerging as a second major growth vector for the Diphenyl Oxide market. The chemical industry is actively exploring pathways to produce bio-based aromatics that can directly substitute petrochemical intermediates without compromising performance.

- Research published in August 2025 demonstrated catalytic hydrodeoxygenation routes capable of converting lignin-derived phenolics into aromatic hydrocarbons with bio-oil yields approaching 96.89% by weight. These breakthroughs create a viable pathway for producing bio-derived DPO from paper mill waste and other lignocellulosic residues, offering a direct route to decarbonize both heat transfer fluids and high-performance polymer supply chains.

- This opportunity is gaining strategic traction at the corporate level. In 2025 guidance, leading specialty chemical producers outlined plans to integrate more sustainable intermediates into their production networks. Transitioning to bio-based DPO could reduce the carbon footprint of PEEK and PEKK manufacturing by up to 30 %, a compelling value proposition for automotive and aerospace OEMs targeting carbon neutrality milestones between 2030 and 2035.

Diphenyl Oxide (DPO) Market Share and Segmentation Insights

Diphenyl Oxide Market Share by Grade : Industrial Grade Leads High-Volume Thermal and Chemical Applications

Industrial grade diphenyl oxide dominates the market with 68% share, serving as the standard specification for heat transfer fluids, flame retardants, and chemical intermediates where cost efficiency and thermal stability are paramount. Its widespread use in high-temperature processing and specialty polymer synthesis underpins large-scale demand. Cosmetic and fragrance grade represents a substantial secondary segment, valued for its consistent odor profile and alkaline stability in soaps, detergents, and perfumery, delivering a characteristic rose-like fragrance. Pharmaceutical grade remains a niche but premium category, supplying API synthesis and regulated manufacturing environments that require stringent purity and quality assurance. While smaller in volume, pharmaceutical-grade DPO commands higher margins due to compliance with cGMP standards. Across all grades, demand is supported by DPO’s versatility as a solvent, intermediate, and thermal fluid, reinforcing its strategic importance in specialty chemicals and performance material value chains.

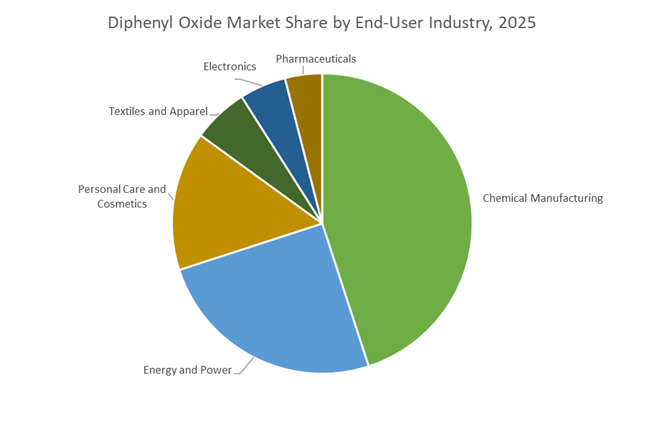

Diphenyl Oxide Market Share by End-User Industry : Chemical Manufacturing and Energy Drive Core Consumption

Chemical manufacturing leads diphenyl oxide demand with 45% market share, utilizing DPO as a key intermediate in polyimide resins, flame retardants, and specialty chemicals for high-performance materials. Energy and power represent a major segment, deploying diphenyl oxide-based heat transfer fluids in concentrated solar power (CSP) plants and industrial heating systems where thermal stability is critical. Personal care and cosmetics account for a significant share through fragrance applications in detergents and toiletries. Textiles and apparel maintain steady consumption as a dye carrier in polyester processing, enabling uniform color development. Electronics remain a niche but strategic application, leveraging high-purity DPO in specialty polymers and electronic materials. Pharmaceuticals contribute limited volume, using diphenyl oxide as an intermediate in API synthesis. Collectively, these sectors sustain DPO’s role across thermal management, specialty chemistry, and fragrance-driven markets.

Competitive Landscape of the Diphenyl Oxide Market

The Diphenyl Oxide (DPO) market in 2026 is defined by strong demand from high-temperature heat transfer fluids, concentrated solar power (CSP), specialty polymers, fragrances, and industrial intermediates, with competition centered on purity levels, thermal stability, vertical integration, and lifecycle service capabilities. Market leaders are differentiating through renewable energy exposure, REACH-compliant grades, circular DPO initiatives, and Asia-Pacific capacity expansions.

Eastman Chemical Company dominates high-temperature heat transfer fluids with Therminol™ VP-1

Eastman Chemical Company is the global benchmark in vapor-phase heat transfer applications, anchored by Therminol™ VP-1, a eutectic blend of diphenyl oxide and biphenyl engineered for continuous operation up to 400°C. Eastman produces >99.9% purity DPO internally, ensuring unmatched consistency for chemical processing and CSP installations. During 2025–2026, the company expanded its Total Lifecycle Care program, providing 24/7 fluid analytics and system flush services that extend equipment life and reduce unplanned downtime. Strategically, Eastman is targeting large-scale CSP projects across MENA, where high-boiling-point DPO fluids directly improve turbine efficiency and thermal storage reliability, reinforcing its leadership in renewable-energy-grade diphenyl oxide.

LANXESS AG strengthens REACH-compliant fragrance and specialty DPO supply in Europe

LANXESS AG operates as a key European supplier, focusing on high-purity industrial and fragrance-grade diphenyl oxide within its Specialty Additives portfolio. In early 2026, LANXESS optimized German production to support rising demand for halogen-free flame retardants and specialty polymers. The company dominates the fragrance and cosmetics segment, supplying DPO with its characteristic geranium-like odor used as a stabilizer in soaps and detergents. A core differentiator is regulatory leadership, with LANXESS driving REACH-compliant aromatic ether production ahead of tightening 2026 environmental standards. Under its Asset Efficiency strategy, the company continues divesting commodity assets to concentrate on high-margin DPO derivatives for polyamides and polyimides.

Jiangsu Zhongneng Chemical Technology Co., Ltd. scales Asia-Pacific DPO capacity with cost-led regional dominance

Jiangsu Zhongneng Chemical Technology has emerged as a major APAC force following the 2025 commissioning of a 10,000-ton diphenyl oxide facility, dramatically expanding domestic supply for China’s petrochemical and textile industries. Its DYNOVA® Diphenyl Oxide serves deodorants, preservatives, and herbicide intermediates, while early-2026 CSP supply agreements in Northwest China position Zhongneng as a primary regional thermal-fluid provider. Leveraging localized production and scale economics, the company delivers aggressive pricing into the APAC merchant market, which now represents 38% of global DPO demand. Zhongneng’s cost-leadership model is rapidly challenging Western incumbents across renewable energy and industrial solvent applications.

Dow Inc. pioneers smart-monitored DPO systems through DOWTHERM™ A

Dow Inc. remains foundational to the DPO ecosystem via DOWTHERM™ A, a high-stability eutectic mixture containing 73.5% diphenyl oxide and 26.5% biphenyl. In 2026, Dow introduced Smart System Monitoring, deploying IoT sensors to detect early-stage thermal degradation and prevent exchanger fouling. The company holds a strong position in polyester and synthetic fiber processing, where DPO functions as a high-boiling solvent for precise polymerization temperature control. Strategically, Dow is advancing Circular DPO pilots, reclaiming and re-purifying spent heat-transfer fluids to reduce lifecycle emissions and align with industrial decarbonization targets.

Vizag Chemical expands export-led growth with customized industrial and pharma DPO grades

Vizag Chemical represents India’s rising specialty chemical capability, supplying industrial and pharmaceutical-grade diphenyl oxide across diverse end-use markets. During 2025–2026, Vizag expanded distribution into the Middle East marine and lubricants sector, while reporting a 12% increase in Southeast Asia exports driven by household and institutional cleaning demand. Operating as a full-spectrum supplier, Vizag bundles DPO with surfactants and specialty solvents for metalworking and coatings customers. Its competitive edge lies in agility and customization, offering niche DPO grades with flexible packaging formats tailored to small and mid-scale formulators, strengthening India’s footprint in the global diphenyl oxide supply chain.

China: Capacity Scale, Cluster Integration, and Energy Transition Pull

China is consolidating its position as a structurally significant producer and consumer in the diphenyl oxide market, driven by capacity additions, petrochemical integration, and clean-energy deployment. In Q1 2025, Jiangsu Zhongneng Chemical Technology completed commissioning of a new 10,000 tpa DPO facility, explicitly designed to serve domestic demand for high-temperature heat transfer fluids in chemical processing and textile finishing. This expansion reflects a broader policy push under the MIIT’s 2025–2026 Petrochemical Stabilization Plan, which prioritizes integrated chemical clusters in Zhejiang and Jiangsu. By co-locating benzene and phenol feedstocks with etherification units, these clusters have reduced precursor logistics costs by an estimated 15%, materially improving DPO cost competitiveness.

Regulatory tightening has simultaneously reshaped the competitive landscape. New national air toxics standards for synthetic organic chemical plants, enforced from April 2025, mandate closed-loop vapor recovery and stricter emission controls. Compliance costs have accelerated consolidation, favoring large, capitalized producers such as Xingfa and Jiangsu Suhua while forcing smaller, high-emission units to exit. On the demand side, China’s expansion of concentrated solar power installations in western provinces has emerged as a non-traditional growth vector. CSP projects increasingly rely on biphenyl–diphenyl oxide eutectic mixtures for thermal storage above 390°C, anchoring DPO consumption to long-duration energy infrastructure rather than cyclical industrial output.

United States: Regulatory Reframing and Specialty Downstream Pull

In the United States, the diphenyl oxide market is being reshaped less by capacity growth and more by regulatory reinterpretation and downstream specialty applications. In September 2025, the U.S. Environmental Protection Agency proposed revisions to TSCA Section 6 risk evaluations, shifting toward condition-of-use–specific assessments rather than blanket chemical determinations. For aromatic ethers such as DPO, this change alters occupational handling requirements and creates differentiated compliance pathways across industrial solvent, fragrance, and surfactant uses.

Feedstock economics remain favorable. Stabilizing benzene and phenol prices on the U.S. Gulf Coast, down approximately 5–7% year over year by Q4 2025, have enabled producers such as Eastman Chemical and Dow to maintain competitive export pricing for DPO-based intermediates shipped to Europe. Regulatory validation has also opened new consumer-facing opportunities. The addition of select aromatic derivatives to the EPA’s Safer Chemical Ingredients List in July 2025 has supported the use of DPO-derived fragrance components in Safer Choice certified cleaning products, accelerating substitution away from synthetic musks and expanding DPO’s role in premium household formulations.

India: Import Substitution and Pharmaceutical-Led Demand

India’s diphenyl oxide market is evolving through industrial policy support and pharmaceutical downstream growth. Under the Production Linked Incentive framework for specialty chemicals, the government has explicitly encouraged domestic production of aroma chemicals. In response, Vikram Aroma expanded capacity in 2025 to reduce reliance on imported DPO, which historically supplied a large share of India’s fragrance raw material needs. This localization trend is strategically important as compliance and logistics costs rise for imported aromatics.

Export momentum has reinforced this shift. In August 2025, India’s chemical exports to ASEAN markets increased by 7.4%, with DPO-based pharmaceutical intermediates recording notable volume gains. This aligns with the Aatmanirbhar Bharat initiative to strengthen domestic API manufacturing. Innovation is also visible at the materials interface. The introduction of APION ion-exchange polymers in 2025, which utilize DPO-derived intermediates, has created incremental demand from pharmaceutical coating and purification applications clustered around Hyderabad and Mumbai, anchoring DPO consumption in higher-margin specialty uses rather than bulk solvents.

Germany: Compliance Transparency and Industrial Heat Recovery

Germany’s diphenyl oxide market is increasingly compliance-driven and technologically specialized. Following the adoption of Regulation (EU) 2025/1731 in August 2025, German producers such as LANXESS have implemented digital product carbon footprint disclosures for aromatic ether shipments. This transparency supports downstream automotive and electronics customers in meeting 2026 EU supply chain due diligence and sustainability reporting requirements, effectively embedding DPO into regulated value chains.

Beyond compliance, Germany is positioning DPO as an efficiency-enabling material for heavy industry. In mid-2025, pilot projects in the Ruhr Valley integrated high-purity DPO into advanced waste-heat recovery systems. These demonstrations reported a 12% improvement in thermal efficiency when DPO-based eutectic fluids replaced conventional heat transfer media, reinforcing DPO’s relevance in energy-intensive industries facing high energy costs and decarbonization pressure.

South Korea: Electronics and Semiconductor Specialization

South Korea represents a technology-driven demand center for diphenyl oxide, anchored in electronics and semiconductor manufacturing. In late 2025, domestic specialty chemical firms introduced DPO-modified epoxy resins optimized for emerging 6G telecommunications infrastructure. These materials offer enhanced dielectric performance and moisture resistance, critical for high-frequency printed circuit board substrates. The application shifts DPO from a thermal fluid role into functional electronics materials.

Semiconductor fabrication has emerged as an additional driver. From 2026 onward, Korean fabs have increasingly adopted DPO-based solvent blends for photoresist stripping and precision cleaning. The compound’s high boiling point and low volatility support ultra-clean processing environments, aligning DPO consumption with capital-intensive semiconductor investments rather than short-cycle industrial demand.

Diphenyl Oxide Market: Country-Level Strategic Snapshot

Diphenyl Oxide Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Demand Anchors

|

Market Character

|

|

China

|

Capacity scale and energy transition

|

HTFs, CSP thermal storage

|

Production and consolidation hub

|

|

United States

|

Regulatory reframing and specialty use

|

Fragrances, surfactants, exports

|

Compliance-driven specialty market

|

|

India

|

Import substitution and pharma growth

|

Aroma chemicals, APIs

|

Emerging localized supplier

|

|

Germany

|

REACH transparency and efficiency

|

Heat recovery, automotive

|

Regulation-led value market

|

|

South Korea

|

Electronics and semiconductor focus

|

6G PCBs, wafer fabs

|

High-tech niche demand

|

Diphenyl Oxide Market Report Scope

Diphenyl Oxide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$882.7 Million

|

|

Market Size (2034)

|

$1504 Million

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Grade (Industrial Grade, Cosmetic and Fragrance Grade, Pharmaceutical Grade), By Type (Liquid Diphenyl Oxide, Crystalline Diphenyl Oxide), By Application (Heat Transfer Fluids, Fragrances and Flavors, Chemical Intermediates, Resins and Polymers, Pharmaceuticals, Industrial Surfactants), By End-User Industry (Chemical Manufacturing, Energy and Power, Personal Care and Cosmetics, Pharmaceuticals, Textiles and Apparel, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Eastman Chemical Company, Dow Inc., LANXESS AG, Arkema S.A., Aarti Industries Limited, Vikram Aroma, Jiangsu Zhongneng Chemical Technology Co., Ltd., Shandong Dadi Alunite Co., Ltd., Merck KGaA, HJ Arochem Pvt. Ltd., Avantor, Inc., Shouguang Derun Chemistry Co., Ltd., KDAC Chem Pvt. Ltd., Augustus Oils Ltd., Beijing LYS Chemicals Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diphenyl Oxide Market Segmentation

By Grade

- Industrial Grade

- Cosmetic and Fragrance Grade

- Pharmaceutical Grade

By Type

- Liquid Diphenyl Oxide

- Crystalline Diphenyl Oxide

By Application

- Heat Transfer Fluids

- Fragrances and Flavors

- Chemical Intermediates

- Resins and Polymers

- Pharmaceuticals

- Industrial Surfactants

By End-User Industry

- Chemical Manufacturing

- Energy and Power

- Personal Care and Cosmetics

- Pharmaceuticals

- Textiles and Apparel

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Diphenyl Oxide Market

- Eastman Chemical Company, Dow Inc.

- LANXESS AG

- Arkema S.A.

- Aarti Industries Limited

- Vikram Aroma

- Jiangsu Zhongneng Chemical Technology Co., Ltd.

- Shandong Dadi Alunite Co., Ltd.

- Merck KGaA

- HJ Arochem Pvt. Ltd.

- Avantor, Inc.

- Shouguang Derun Chemistry Co., Ltd.

- KDAC Chem Pvt. Ltd.

- Augustus Oils Ltd.

- Beijing LYS Chemicals Co., Ltd.

*- List not Exhaustive