Dodecanedioic Acid Market to Reach $1,325 Million by 2034 at 6.2% CAGR Amid Bio-Based Nylon 612 and EV Polymer Expansion

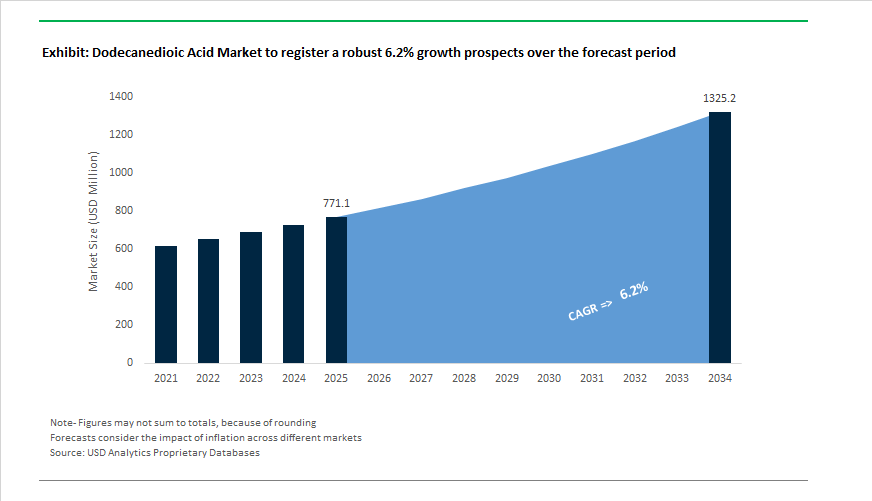

The Dodecanedioic Acid (DDDA) Market is projected to grow from $771.1 Million in 2025 to $1,325 Million by 2034, registering a CAGR of 6.2%. Structural growth is anchored in high-performance polyamides, specialty coatings, adhesives, and emerging bio-based chemical platforms. In March 2024, Cathay Industrial Biotech achieved industrial-scale production of 100% bio-based DDDA derived from renewable biomass feedstocks, marking a decisive transition away from fossil-derived C12 intermediates. This development directly supports sustainable Nylon 612 manufacturing, where DDDA provides superior hydrolysis resistance, chemical stability, and low-temperature impact strength. In parallel, stricter environmental inspections across key Chinese provinces in 2024 temporarily curtailed DDDA supply, triggering global rebalancing. Producers such as Ube Industries and Evonik optimized non-Chinese assets to stabilize automotive-grade polyamide output.

Innovation accelerated across downstream polymer systems through late 2024. In September 2024, Evonik introduced a new VESTAMID® grade synthesized with DDDA, targeting electric vehicle battery cooling lines and high-voltage insulation components that demand superior thermal endurance and weight optimization. The same month, Kraton launched bio-based styrene block copolymers incorporating DDDA chemistry, addressing medical and adhesive markets that require elastomeric flexibility with high purity profiles. In November 2024, BASF advanced its OneCarbonBio synthetic biology platform in collaboration with Acies Bio, scaling microbial fermentation routes to produce specialty intermediates such as DDDA with reduced carbon intensity. By April 2025, Invista expanded ISCC PLUS certification across global facilities in Shanghai and Rozenburg, enabling verification of biomass-balanced intermediates within the DDDA-nylon value chain and strengthening traceability for automotive OEM and consumer applications.

Demand patterns shifted materially in 2025, particularly in medical and construction sectors. Throughout the year, suppliers reported strong growth in Ultra-High Purity DDDA (≥99%) for medical-grade polyamides used in catheters and precision surgical instruments, where biocompatibility and antimicrobial performance are critical. Concurrently, regulatory tightening on VOC emissions in North America and Europe accelerated adoption of DDDA-based bio-adhesives for construction and woodworking applications, replacing solvent-heavy petrochemical binders. Strategic industrial collaborations further reinforced DDDA’s positioning in circular materials. In October 2025, Evonik partnered with Schneider Electric to improve thermoplastic recycling efficiency for smart grid and data center components utilizing DDDA-based polymers. Financial performance remained resilient; in February 2026, Evonik confirmed meeting its 2025 EBITDA guidance and outlined expansion of its Shanghai Multi-User-Site to strengthen supply of DDDA-derived PEBA materials for high-growth Asian markets. Additionally, Evonik expanded HTPB production capacity in February 2026, leveraging C12 chemistry integration across Marl and Shanghai sites, reinforcing operational synergies within the broader DDDA value chain.

Trends and Opportunities in the Dodecanedioic Acid (DDDA) Market

Strategic Shift from Petrochemical to Bio-Based DDDA Production to De-Risk Supply Chains

- The transition from butadiene-based DDDA synthesis to fermentation-driven bio-based production has accelerated as manufacturers seek insulation from crude oil volatility and Scope 3 emission exposure. Petrochemical DDDA routes remain highly sensitive to C4 feedstock availability, a risk highlighted in October 2024 when China’s butadiene exports surged by 111% year over year, amplifying price instability across downstream intermediates.

- In contrast, Cathay Biotech has scaled fermentation-based DDDA production using renewable feedstocks such as glucose and vegetable oils. In 2024, the company reported approximately 75,000 metric tons of annual capacity for bio-based long-chain diacids, positioning fermentation as the only route capable of delivering long-term price stability at scale. Industrial benchmarking confirms that fermentation-based DDDA consumes up to 30% less energy than multi-step butadiene oxidation routes, materially reducing product carbon footprint and aligning with 2025 sustainability procurement requirements across Europe.

- This structural shift is influencing incumbent producers as well. Evonik has begun integrating mass-balanced bio-circular raw materials into its long-chain polyamide value chain, targeting up to 70% CO₂ emission reduction by 2030. Bio-based DDDA is increasingly viewed not only as a sustainability lever, but as a supply assurance mechanism in a market exposed to hydrocarbon cyclicality.

Downstream Integration into High-Performance Polyamides for Technical Applications

- DDDA is gaining strategic relevance as a core monomer for long-chain polyamides such as Nylon 6,12 and Nylon 5,12, which offer superior chemical resistance, dimensional stability, and low moisture absorption compared to conventional Nylon 6 or 6,6. These properties are critical in precision applications where thermal cycling, fuel exposure, and long service life are non-negotiable.

- Vertical integration is emerging as the dominant competitive model. Evonik operates approximately 3,000 metric tons of specialized DDDA capacity in Germany, with the majority consumed internally for VESTAMID® Nylon 6,12 production. This closed-loop model ensures margin protection, proprietary polymer grades, and tighter control over quality specifications required by automotive and electronics OEMs.

- Industry data from 2024–2025 indicates that resin and polymer applications now account for more than 60% of total DDDA consumption. Demand is concentrated in long-chain polyamides that rely on DDDA’s 12-carbon backbone to achieve hydrolytic stability and low creep, particularly in automotive fuel systems, electronic connectors, and fluid handling components.

Qualification as a Critical Raw Material for Electric Vehicle Battery Component Supply Chains

- The rapid scaling of electric vehicle platforms is creating a high-value, qualification-driven opportunity for DDDA-based polyamides in battery thermal management and safety systems. As of December 2025, the global EV battery coolant market is valued at approximately USD 2.20 billion, with Nylon 6,12 increasingly specified for cooling lines and fluid conduits due to its resistance to aggressive glycol-based coolants and sustained vibration loads.

- Leading OEMs such as Tesla and BYD are transitioning toward high-density structural battery packs. This shift places a premium on materials with low moisture uptake. DDDA-based polyamides typically absorb only 1.5% to 3% moisture, compared to 8% to 10% for Nylon 6, significantly reducing the risk of electrical leakage and mechanical degradation over a 10-year vehicle lifespan.

- Policy support further strengthens this opportunity. The U.S. Department of Energy, through its Vehicle Technologies Office, initiated multiple battery thermal management programs in 2024–2025. These initiatives create a direct pathway for DDDA producers to qualify within localized, domestic EV supply chains aligned with clean transportation mandates.

Enabling Sustainable Coatings and Corrosion Protection for Offshore Wind Infrastructure

- The expansion of offshore wind capacity is emerging as a structurally durable growth lever for DDDA-based resins and coatings. Offshore turbines operate under extreme salt spray, UV radiation, and mechanical stress, demanding coating systems with long maintenance cycles and high corrosion resistance.

- In December 2024, PPG and Jotun launched advanced anti-corrosive coating systems for offshore applications. These formulations incorporate DDDA-derived polyesters that improve salt spray resistance by up to 35% and extend maintenance intervals by 20% to 30%, directly lowering lifetime operating costs for wind farm operators.

- Regional policy momentum is reinforcing demand. Ministry of New and Renewable Energy is targeting 500 GW of non-fossil capacity by 2030, with a strong emphasis on tapping India’s estimated 1,164 GW offshore wind potential. Offshore installations increasingly favor DDDA-based powder coatings due to their VOC-free profiles and superior edge retention on turbine towers and nacelles.

- Approximately 71% of offshore turbines now rely on multi-layered protective coating systems. With offshore wind installations projected to increase by more than 68% between 2024 and 2033, DDDA demand linked to corrosion-resistant resins is expected to grow faster than the broader chemical intermediates market.

Dodecanedioic Acid (DDDA) Market Share and Segmentation Insights

Dodecanedioic Acid Market Share by Production Process: Synthetic Routes Dominate While Bio-Based DDDA Accelerates

In 2025, synthetic dodecanedioic acid production commands 68% of total DDDA market share, reinforcing its position as the most established and cost-effective manufacturing pathway. Derived mainly from butadiene, synthetic DDDA delivers consistent purity and performance, making it the preferred choice for high-demand applications across polyamides, specialty coatings, and industrial lubricants. Paraffin wax oxidation continues to hold a meaningful presence, particularly in select regional markets, although this traditional process faces increasing pressure due to lower production efficiency and broader product variability. Meanwhile, bio-based dodecanedioic acid represents the fastest-growing segment, fueled by rising sustainability mandates across automotive, consumer goods, and electronics sectors. Fermentation-based DDDA from renewable feedstocks enables manufacturers to reduce carbon footprints while maintaining material performance, positioning bio-based DDDA as a key growth catalyst within the global specialty chemicals and sustainable polyamide intermediates landscape.

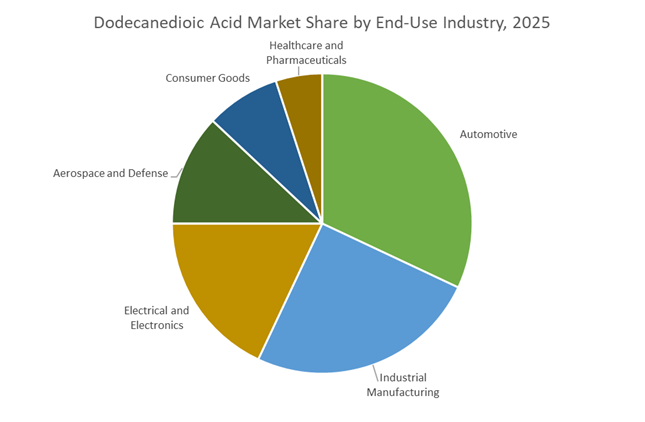

Dodecanedioic Acid Market Share by End-Use Industry: Automotive Leads High-Performance Polyamide Demand

The automotive industry accounts for 32% of global DDDA consumption, driven by strong demand for nylon 6,12 and nylon 12,12 in fuel lines, brake systems, coolant pipes, and under-hood components requiring superior thermal stability and chemical resistance. Industrial manufacturing follows closely, leveraging DDDA in corrosion-resistant coatings, engineering plastics, bearings, and gears where low friction and durability are critical. Electrical and electronics applications remain significant, utilizing DDDA-derived polyamides for wire insulation and electronic components offering dielectric strength and dimensional stability. Aerospace and defense rely on DDDA for lightweight composites, fuel-resistant sealants, and high-temperature lubricants. Consumer goods maintain steady uptake across appliances and sports equipment, while healthcare and pharmaceuticals form a niche but high-value segment, using high-purity DDDA in medical devices and biocompatible materials that demand strict regulatory compliance.

Competitive Landscape of the Dodecanedioic Acid Market

The global dodecanedioic acid (DDDA) market in 2026 is shaped by a dual-track competitive structure: bio-based DDDA innovators versus synthetic scale-driven producers, with leadership defined by polyamide integration, automotive lightweighting demand, specialty nylons, and sustainable chemical manufacturing.

Cathay Biotech drives bio-based DDDA leadership through synthetic biology scale-up

Cathay Biotech Inc. has firmly established itself as the global leader in bio-based dodecanedioic acid, powered by its proprietary synthetic biology platform. In March 2024, Cathay achieved industrial-scale production of 100% bio-based DDDA using renewable biomass, replacing traditional paraffin fermentation routes. By 2026, microbial strain engineering improved production efficiency enough to cut costs by ~30% versus 2024 levels, giving Cathay a decisive commercial edge. The company is fully integrated from biological strain R&D through fermentation to downstream polyamide polymerization, enabling reliable supply of DDDA for high-performance textiles and automotive applications. Its Terryl® bio-nylon portfolio positions Cathay at the center of drop-in sustainable materials for next-generation vehicles and technical fabrics.

Evonik strengthens premium DDDA demand via specialty polyamides and powder coatings

Evonik Industries AG operates at the high end of the DDDA value chain, embedding dodecanedioic acid into advanced polymers such as its VESTAMID® Terra PA610 and PA1010 grades. These materials rely on DDDA derivatives for high heat resistance, chemical durability, and lightweight performance. In May 2023, Evonik doubled global PEBA capacity at its Shanghai and Marl sites, directly lifting internal DDDA consumption. The company dominates VOC-free powder coatings, where DDDA-based resins are standard for ultra-thin finishes on automotive wheels and consumer electronics. Through its OneCarbonBio strategy, Evonik is scaling bio-technologically derived intermediates, targeting lower-carbon high-performance plastics for mobility, electronics, and sustainable coatings markets.

INVISTA leverages nylon 6,6 scale to anchor synthetic DDDA volumes globally

INVISTA remains a cornerstone of synthetic dodecanedioic acid production, benefiting from massive integration into the nylon 6,6 value chain. In August 2024, INVISTA expanded its Shanghai nylon facility, reinforcing APAC supply and boosting internal DDDA demand. Despite bio-based advances, butadiene-route DDDA still represents roughly 87% of global industrial volume in 2026, highlighting INVISTA’s continued relevance through scalability and reliability. The company is a primary supplier to automotive lightweighting, where DDDA-derived Nylon 6,12 delivers thermal stability for EV battery cooling systems. INVISTA’s strength lies in global logistics and consistent >99% purity grades, supporting pharmaceutical, lubricant, and engineering plastic applications.

UBE Corporation targets specialty DDDA for electronics and additive manufacturing

UBE Corporation focuses on high-purity synthetic DDDA for specialty resins used in toothbrush bristles, premium fishing lines, and engineering plastics. Following its 2022 acquisition of API Corporation, UBE strengthened pharmaceutical intermediate capabilities where DDDA derivatives act as key precursors. By 2026, Asia-Pacific accounts for over 52% of global DDDA demand, positioning UBE as a critical regional supplier. Its strategy emphasizes “Specialty over Commodity,” expanding into electronics and 3D printing, where DDDA-based photopolymers support high-performance additive manufacturing. UBE’s precision manufacturing and specialty nylon expertise make it a preferred partner for advanced materials customers seeking consistency, purity, and application-specific polymer performance.

BASF integrates DDDA into lubricants and polyamides via its Verbund platform

BASF SE maintains a strong position in the dodecanedioic acid market through its Verbund integration, linking DDDA production with downstream polyamides and synthetic esters. In June 2025, BASF neared completion of its PA 6,6 expansion in Freiburg, Germany, creating a major European pull on DDDA volumes. The company also partnered with Acies Bio in late 2024 to advance synthetic biology platforms, bridging petrochemical reliability with bio-based sustainability. DDDA plays a key role in BASF’s industrial lubricant esters, prized for high viscosity and biodegradability in marine and oil-field environments. Vertical integration into butadiene shields BASF from 2026 feedstock volatility.

China: Bio-Polyamide Timelines and NEV-Led Nylon 6,12 Prioritization

China’s dodecanedioic acid market is being reshaped by a recalibration of bio-based capacity timelines and a decisive push from New Energy Vehicles. In September 2025, Cathay Biotech, the world’s largest producer of bio-based DDDA, announced an extension to its flagship Shandong project. The facility, designed to anchor a 900,000-ton bio-based polyamide ecosystem, has been rescheduled for completion by December 31, 2027 due to industrial park infrastructure delays. This postponement tightens the anticipated 2026 availability of bio-derived resins and sustains near-term demand for incumbent DDDA producers supplying specialty polyamides. In parallel, the State Council’s Regulation on Ecological Environment Monitoring, promulgated in October 2025 and effective January 1, 2026, mandates unified digital monitoring of VOC emissions and wastewater. Compliance costs are accelerating the exit of inefficient butadiene-oxidation units, concentrating production among compliant, technology-advanced plants.

Demand visibility remains robust on the application side. With NEV sales projected to exceed 12 million units annually by 2026, the Ministry of Industry and Information Technology has prioritized high-performance Nylon 6,12. DDDA is increasingly specified for battery coolant lines and electrical connectors where hydrolysis resistance and thermal stability are critical. To reduce feedstock volatility across the C12 value chain, China is also advancing the Petrochemical Stabilization Plan through 2026, encouraging a shift from fossil butadiene toward paraffin-wax-derived fermentation routes.

United States: EAL Standards, Energy-Efficient Coatings, and Defense Localization

In the United States, regulatory alignment and industrial policy are elevating DDDA’s strategic relevance across lubricants, coatings, and advanced materials. Under the 2025–2026 EPA Strategic Plan, new mandates for Environmentally Acceptable Lubricants are redirecting procurement toward biodegradable formulations. Producers such as Invista are seeing stronger pull for DDDA-based complex esters used in maritime and forestry gear oils, where biodegradability and oxidative stability are mandatory. At the same time, TSCA Section 8(d) reporting deadlines set for May 22, 2026 are pushing manufacturers to standardize high-purity grades and improve transparency for long-chain diacids.

Innovation in coatings and defense adds further momentum. Mid-2025 commercialization of ultra-low-bake powder coatings using DDDA as a curative has enabled a 20% reduction in oven temperatures, aligning with federally funded infrastructure projects emphasizing energy efficiency. In late 2025, increased Department of Defense funding for localized manufacturing elevated DDDA-derived polymers in ballistic fibers and aerospace structural adhesives, reinforcing domestic supply chain resilience for critical materials.

Germany: Verbund Efficiency, Automotive Polyamides, and Regulatory Substitution

Germany’s DDDA market is characterized by deep integration and regulatory-driven substitution within the European Union. Evonik Industries highlighted in its 2025 Company Factbook a shift toward Next Generation Solutions at its Marl site, vertically integrating to consume all internally produced DDDA for Nylon 6,12. This strategy targets a 15% reduction in Scope 3 emissions by 2026 while improving supply security for automotive and industrial customers. Complementing this, BASF finalized a polyamide expansion in Freiburg in early 2025. Although centered on PA66, the upgraded polycondensation lines are flexible enough to incorporate DDDA monomers for specialty grades specified by OEMs such as BMW and Volkswagen.

Regulatory dynamics further favor DDDA adoption. The September 1, 2025 update to REACH Annex XVII tightened restrictions on CMR substances, positioning DDDA as a safer long-chain alternative to phthalate-based plasticizers in flexible PVC. This has accelerated qualification cycles across automotive interiors and technical films, reinforcing Germany’s role as a quality benchmark market for DDDA-based materials.

Japan: Precision Catalysis and Semiconductor Materials

Japan’s DDDA landscape is defined by yield optimization and electronics-grade purity. In September 2025, UBE Corporation reported a catalyst optimization breakthrough that improved pure DDDA crystal yields by 4%. The advance is tailored to zero-defect requirements in electronics components and high-performance filament applications such as toothbrush bristles. Concurrently, Japanese semiconductor manufacturers have increased the use of high-purity DDDA in CMP slurries for 2-nanometer wafer production, citing superior surface-active behavior during copper interconnect polishing. These applications elevate DDDA from a commodity diacid to a precision functional material.

Malaysia: Waste-to-Acid Fermentation and ASEAN Export Platform

Malaysia is emerging as a bio-based DDDA export platform through waste valorization. In August 2025, Verdezyne, in collaboration with local palm oil groups, successfully completed the first production run at its 6,000-metric-ton plant in southern Malaysia. The facility converts palm oil waste via yeast fermentation into bio-DDDA, positioning Malaysia as a sustainable supplier to ASEAN polymer and lubricant markets. The model aligns agricultural by-products with chemical value creation, offering cost and carbon advantages for regional buyers.

Dodecanedioic Acid Market: Country-Level Strategic Snapshot

Dodecanedioic Acid Market County Level Snapshot

|

Country

|

Policy or Technology Driver

|

Core Demand Anchors

|

Structural Direction

|

|

China

|

Environmental monitoring mandates, NEV policy

|

Nylon 6,12 for batteries and connectors

|

Feedstock diversification and compliant scale

|

|

United States

|

EAL standards, TSCA transparency

|

Biodegradable lubricants, low-bake coatings, defense

|

High-purity grades and localized supply

|

|

Germany

|

Verbund integration, REACH Annex XVII

|

Automotive polyamides, flexible PVC

|

Internal consumption and safer substitution

|

|

Japan

|

Catalyst yield optimization

|

Semiconductor CMP slurries, precision filaments

|

Electronics-grade specialization

|

|

Malaysia

|

Waste-to-acid fermentation

|

ASEAN polymers and lubricants

|

Bio-based export platform

|

Dodecanedioic Acid Market Report Scope

Dodecanedioic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$771.1 Million

|

|

Market Size (2034)

|

$1325 Million

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Production Process (Synthetic, Bio-Based, Paraffin Wax Oxidation), By Application (Polyamides and Resins, Powder and Liquid Coatings, Lubricants and Corrosion Inhibitors, Adhesives and Sealants, Cosmetics and Fragrances, Specialty Chemicals), By End-Use Industry (Automotive, Aerospace and Defense, Industrial Manufacturing, Electrical and Electronics, Consumer Goods, Healthcare and Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cathay Biotech Inc., Evonik Industries AG, UBE Corporation, INVISTA, BASF SE, Merck KGaA, Santech Industries, Verdezyne, Inc., BEYO Chemical Co., Ltd., Shandong Guangtong New Materials Co., Ltd., Henan Junheng Industrial Group, Zhengzhou Meiya Chemical Products Co., Ltd., Palmary Chemical, Tokyo Chemical Industry Co., Ltd., Augustus Oils Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dodecanedioic Acid Market Segmentation

By Production Process

- Synthetic

- Bio-Based

- Paraffin Wax Oxidation

By Application

- Polyamides and Resins

- Powder and Liquid Coatings

- Lubricants and Corrosion Inhibitors

- Adhesives and Sealants

- Cosmetics and Fragrances

- Specialty Chemicals

By End-Use Industry

- Automotive

- Aerospace and Defense

- Industrial Manufacturing

- Electrical and Electronics

- Consumer Goods

- Healthcare and Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dodecanedioic Acid Industry

- Cathay Biotech Inc.

- Evonik Industries AG

- UBE Corporation

- INVISTA

- BASF SE

- Merck KGaA

- Santech Industries

- Verdezyne, Inc.

- BEYO Chemical Co., Ltd.

- Shandong Guangtong New Materials Co., Ltd.

- Henan Junheng Industrial Group

- Zhengzhou Meiya Chemical Products Co., Ltd.

- Palmary Chemical

- Tokyo Chemical Industry Co., Ltd.

- Augustus Oils Ltd.

*- List not Exhaustive