Global Drilling Fluids Market Overview

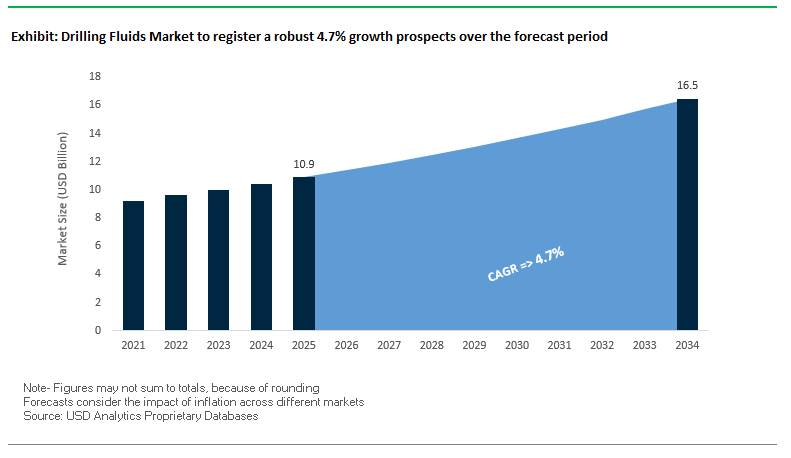

The global drilling fluids market is projected to grow from $10.9 billion in 2025 to $16.5 billion by 2034, at a CAGR of 4.7%. This growth is primarily fueled by the increasing demand for high-performance drilling fluids that enhance drilling efficiency in complex formations, minimize non-productive time (NPT), and maintain wellbore stability in extended-reach and horizontal wells.

The market is also being shaped by the rise of deepwater and unconventional drilling operations in regions such as the Gulf of Mexico, offshore Brazil, and the North Sea. Operators are seeking drilling fluids capable of withstanding high-pressure, high-temperature (HPHT) conditions, while adhering to evolving environmental regulations. Water-based fluids (WBF) are gaining popularity due to their biodegradability, lower toxicity, and ease of disposal, aligning with stricter offshore drilling and waste management standards.

Key Insights for Industry Stakeholders:

- High-Performance Fluids: Advanced drilling fluids reduce NPT and improve drilling efficiency.

- Deepwater and Unconventional Drilling: Fluids for HPHT environments are in growing demand.

- Environmental Compliance: Water-based and biodegradable fluids are increasingly adopted.

- Wellbore Stability: Drilling fluids maintain hydrostatic pressure, preventing collapse and formation damage.

- Digital Integration: AI-enhanced and automated systems improve drilling precision and resource management.

Market Analysis: Recent Developments in Drilling Fluids

The drilling fluids market has witnessed significant developments in 2024–2025, with companies leveraging technology, mergers, and advanced product offerings to strengthen market presence. In August 2025, ProFrac partnered with Seismos to implement Closed Loop Fracturing across U.S. basins, optimizing the use of drilling fluids and resources. The same month, Crescent Energy announced a $3.1 billion all-stock acquisition of Vital, reflecting broader industry consolidation trends aimed at enhancing operational efficiency and technology integration.

In July 2025, Halliburton launched its LOGIX™ automated geosteering service, integrating real-time data with smart drilling fluid systems for optimized performance. June 2025 saw ADNOC Drilling securing a five-year, $800 million oilfield services contract, likely including deployment of advanced drilling fluids to enhance well productivity. In October 2024, Azure Holding Group Corp. completed a strategic merger with CST Drilling Fluids, consolidating expertise to deliver high-quality fluid solutions across drilling operations.

Environmental and technological advancements also mark the period. In August 2024, Angarsk Petrochemical Company (Rosneft) began manufacturing Rosneft Drilltec B2Ih drilling fluids, featuring low-viscosity hydrocarbons for environmentally friendly operations. ABB’s next-generation electromagnetic flowmeters, introduced in the same month, enable real-time monitoring of fluid properties and flow rates, optimizing drilling fluid management. Earlier in January 2024, Schlumberger Technology Corporation launched its AI-enhanced DrillXpert system, using machine learning to optimize fluid performance in offshore drilling.

Key Trends Driving Drilling Fluids Market Outlook

Rising Demand for Environmentally Friendly Drilling Fluids

The drilling fluids market is being significantly influenced by regulatory mandates and the push toward sustainability. Governments and agencies such as the U.S. Environmental Protection Agency (EPA), as well as policies like India’s Hydrocarbon Exploration and Licensing Policy (HELP), are promoting water-based and bio-based drilling fluids to reduce environmental impact. Academic research published in MDPI's Water highlights that organic brines, such as formate-based fluids, degrade naturally into carbon dioxide and water, providing an environmentally benign alternative to conventional fluids. This trend is driving adoption of eco-friendly drilling fluids in both onshore and offshore operations, aligning regulatory compliance with operational efficiency.

Integration of IoT and AI for Real-Time Fluid Optimization

The integration of IoT and AI is transforming drilling fluid management into a data-driven, proactive operation. Halliburton and other leading service providers are deploying digital monitoring platforms that use sensors to continuously measure fluid properties in real time. AI algorithms then optimize fluid composition, chemical dosing, and flow rates, ensuring wellbore stability and minimizing non-productive time (NPT). Academic studies from 2024 confirm that AI-powered predictive analytics reduce operational risks and enhance drilling performance, making digital fluid management systems a critical growth driver for the market.

High-Performance Fluids for Extreme Well Conditions

The development of high-performance drilling fluids is another key trend, particularly for high-pressure, high-temperature (HPHT) wells and extended-reach drilling. Research from 2025 highlights the use of advanced additives, rheology modifiers, and surfactants to improve fluid stability and lubricity under extreme conditions. Case studies from major oil companies show that these fluids reduce downtime during wellbore displacement, ensuring proper cleaning and enhanced efficiency during completions. As operators tackle more complex reservoirs, the demand for premium, high-performance drilling fluids is intensifying.

Opportunities in Drilling Fluids Market

Opportunities are emerging in the design and deployment of sustainable, high-performance, and digitally managed drilling fluids. The growing need for eco-friendly formulations, coupled with advanced AI and IoT-based monitoring solutions, creates a lucrative market for suppliers offering turnkey systems. Offshore drilling, deepwater, and HPHT applications provide high-value segments where premium synthetic-based fluids (SBFs) and specialized additives command significant margins. Additionally, the trend toward real-time optimization presents opportunities for fluid service providers to develop predictive maintenance, remote monitoring, and circular-use fluid solutions that enhance operational efficiency and reduce environmental footprints.

Market Share Analysis of Drilling Fluids Market

Market Share by Fluid Type: Water-Based Fluids Lead, SBFs Gain Traction

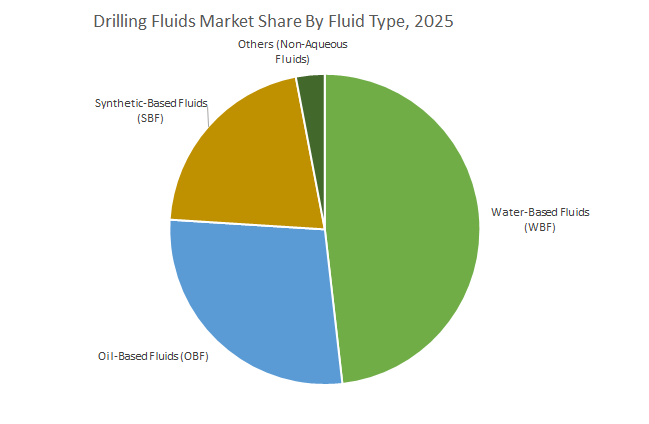

Water-based fluids (WBF, 48.5%) dominate the market due to cost-effectiveness and environmental acceptability, particularly for onshore and shallow offshore applications. Oil-based fluids (OBF, 26.9%) provide high-temperature stability and wellbore performance but face regulatory restrictions due to environmental concerns. Synthetic-based fluids (SBF, 22.5%) are the premium, high-performance segment, offering lower toxicity and superior biodegradability. SBFs are increasingly favored for HPHT and complex offshore wells, combining environmental compliance with technical excellence. Non-aqueous and brine-based emerging systems represent a small, niche portion of the market.

Market Share by Application: Onshore Drives Volume, Offshore Commands Value

The onshore segment (64.3%) leads in terms of volume due to the extensive number of wells in shale and conventional plays, where cost efficiency drives fluid choice, favoring WBFs. The offshore segment (35.7%), although smaller in volume, represents a higher value market, driven by complex wells, HPHT conditions, and deepwater challenges. Offshore applications demand premium fluids such as SBFs and advanced OBFs to ensure operational reliability, making this segment a significant revenue contributor for fluid service providers. The two segments reflect distinct market dynamics: volume vs. value.

Market Share by Well Type: Conventional Wells Dominate, HPHT Fuels High-Value Growth

Conventional wells (74.5%) form the core market, typically using WBF and standard OBF systems. These wells are highly price-sensitive and account for the majority of global drilling activity. In contrast, HPHT wells (26.9%) are a high-growth, high-value niche requiring specialized synthetic fluids and custom-designed systems capable of maintaining stability under extreme pressures and temperatures. The HPHT segment drives technological innovation, including high-performance additives, rheology modifiers, and environmentally friendly base fluids. Its expansion supports higher profit margins and R&D investment in the drilling fluids market.

United States: Technological Leadership and Federal Support Accelerating Drilling Fluids Market Expansion

The United States drilling fluids market remains a global leader, driven by its dominance in unconventional drilling across shale-rich regions such as the Permian Basin, Marcellus Shale, and Bakken Formation. The rising demand for high-performance drilling fluids capable of withstanding complex, high-pressure, and high-temperature (HPHT) environments is reinforced by a strong wave of technological innovations.

In 2024, Badger Meter acquired remote water monitoring hardware and software from Trimble, marking a consolidation trend in the industry where companies integrate IoT-enabled smart water management solutions for real-time drilling fluid monitoring and predictive analysis. Additionally, Newpark Resources Inc.’s sale of its Fluids Systems business to SCF Partners, Inc. illustrates how U.S. companies are restructuring to focus on high-value markets.

The U.S. federal government, through the Bipartisan Infrastructure Law (BIL), is injecting over $50 billion into water infrastructure improvements, further supporting drilling fluid management and sustainability. With shale gas and deep-well campaigns intensifying, the U.S. drilling fluids market outlook is set to expand as operators demand cost-effective, high-efficiency, and environmentally compliant solutions.

Saudi Arabia: Massive Infrastructure Investments and Offshore Expansion Driving Drilling Fluid Demand

The Saudi Arabia drilling fluids market is propelled by the nation’s position as the holder of 17% of the world’s proven oil reserves and the operational dominance of Saudi Aramco. With a large number of active drilling rigs, Saudi Arabia sustains strong demand for oil-based, water-based, and synthetic drilling fluids.

In 2023, ADNOC Drilling secured a landmark contract for the Upper Zakum field, deploying state-of-the-art drilling units in one of the Middle East’s largest offshore production projects. This development is part of a broader strategy to boost deepwater and ultra-deepwater capacity in the Persian Gulf, creating a surge in demand for high-density, specialized drilling fluids.

The market is further driven by the need to execute multi-lateral, pressure-isolated wells from single boreholes, requiring advanced formulations of specialty drilling fluids. As Saudi Arabia continues to scale capacity, the region’s drilling fluids market size is expected to expand in line with rising offshore and unconventional oilfield developments.

China: Shale Gas Development and Smart Monitoring Technologies Enhancing Drilling Fluids Market Growth

The China drilling fluids market is witnessing robust expansion due to the country’s aggressive development of shale gas reserves, which account for over 15% of global shale gas resources. Government-backed initiatives to strengthen energy independence have accelerated investment in hydraulic fracturing and HPHT drilling campaigns, fueling strong demand for drilling fluids that can withstand complex reservoir conditions.

Technological adoption is another growth driver. China is increasingly deploying Smart Water Management (SWM) systems using IoT and artificial intelligence to enable real-time monitoring of drilling fluid properties, improve efficiency, and enhance safety. These innovations allow predictive adjustments to drilling fluid formulations, significantly improving operational resilience.

With Asia Pacific forecasted as the fastest-growing drilling fluids market globally, China will remain central to growth, particularly across HPHT wells, unconventional reserves, and shale formations that demand advanced drilling fluid solutions.

Norway: Stringent Environmental Rules and Offshore Innovation Shaping Drilling Fluids Market

The Norway drilling fluids market is anchored by stringent offshore drilling regulations, driving the adoption of biodegradable and environmentally friendly drilling fluids. Norway’s North Sea projects require fluid systems that can perform under extreme temperature and pressure conditions, while meeting strict environmental compliance standards.

In March 2025, the Norwegian Offshore Directorate (NOD) authorized Equinor to drill two wildcat wells (34/6-8 A and 34/6-8 S) in the North Sea, reaffirming Norway’s commitment to upstream expansion. In line with regulatory expectations, companies are innovating: Repsol’s enhanced riserless mud recovery system at the Yme field allows drilling fluid recycling without a riser, minimizing discharge and boosting operational efficiency.

The country’s focus on sustainable offshore oilfield development ensures that the Norway drilling fluids market will continue to evolve with eco-friendly formulations and recovery technologies at its core.

Canada: Research-Driven Wastewater Management Boosting Drilling Fluids Market Adoption

The Canada drilling fluids market is increasingly shaped by government-backed research projects targeting water management in hydraulic fracturing. For instance, Natural Resources Canada has funded a University of Alberta project focused on the fate of non-recovered fracturing water and the source of produced salts, which is expected to fill critical knowledge gaps in optimizing fluid formulations and reducing environmental risks.

With Alberta and British Columbia leading unconventional hydrocarbon development, Canada enforces robust regulatory frameworks for wastewater and drilling fluid management. The expanding exploitation of tight oil and shale gas resources is directly driving the demand for efficient, environmentally compliant drilling fluid solutions. This positions Canada as a key market in North America for innovative fluid systems supporting unconventional exploration.

Russia: Domestic Innovation and Exploration Investments Fueling Drilling Fluids Market Expansion

The Russia drilling fluids market benefits from the country’s aggressive oil and gas exploration activities and its move toward technological self-sufficiency in drilling fluid production. In August 2024, Angarsk Petrochemical Company (Rosneft division) began manufacturing low-viscosity hydrocarbon-based drilling fluids that are more environmentally sustainable. This reflects Russia’s broader strategy of reducing dependence on imports while developing domestic advanced drilling technologies.

The market is further driven by large-scale investment in conventional and unconventional oilfield development, where HPHT drilling environments and heavy hydrocarbon reservoirs demand customized drilling fluids. With exploration continuing across Siberian fields, the Arctic shelf, and unconventional reserves, Russia’s drilling fluids market size is set for consistent growth, reinforced by corporate innovations and rising operational demand.

Competitive Landscape of Drilling Fluids Market

The drilling fluids market is highly competitive, with leading companies focusing on high-performance formulations, digital integration, and sustainable solutions to serve deepwater, unconventional, and environmentally sensitive drilling operations. Market players differentiate themselves through innovation, AI-enabled systems, and strategic mergers and partnerships.

Schlumberger Limited (SLB) excels in AI-driven drilling fluid solutions

SLB offers a complete portfolio of drilling fluids, including water-based, oil-based, and synthetic formulations, backed by advanced solids control and waste management capabilities. Its M-I SWACO division is a leader in R&D-driven solutions, and the January 2024 DrillXpert launch highlights its use of AI to optimize fluid performance and real-time decision-making. SLB focuses on leveraging digital technologies to enhance operational efficiency and minimize environmental impact.

Halliburton Company provides customized, high-performance fluid systems

Halliburton specializes in customized water-based and nonaqueous drilling fluids, reservoir drilling fluids, and comprehensive solids control services. The LOGIX™ automated geosteering service, launched in July 2025, integrates digital solutions with fluid systems to enhance drilling precision. Halliburton’s strategic focus combines advanced fluid systems with sustainability initiatives, helping operators reduce environmental impact and optimize drilling operations.

Baker Hughes, a GE company, delivers integrated drilling solutions

Baker Hughes offers a broad range of drilling fluids, including invert emulsion, water-based, and synthetic-based systems, designed for onshore, deepwater, and geothermal wells. Its construction of Namibia’s first liquid mud plant enhances local supply chains and reduces costs. Baker Hughes integrates digital and AI technologies to improve well construction, delivering stable wellbores and optimized drilling performance.

Newpark Resources, Inc. emphasizes environmentally responsible fluid systems

Newpark provides high-performance water-based and nonaqueous drilling fluids, including Hydros™ and Nviros™ brands. The company is recognized for solutions addressing lost circulation and solids control, and its 2024 Teros system deployment in the DJ Basin demonstrates effectiveness in challenging drilling operations. Newpark focuses on seamless service delivery, continuous technical investment, and sustainable drilling solutions.

TETRA Technologies, Inc. focuses on sustainable and high-purity fluids

TETRA offers completion fluids and additives, including the TETRA CS Neptune® family, which are environmentally friendly and zinc-free. A 2024 report emphasizes the company’s commitment to sustainability and safety, reflected in its hybrid product lines and vertically integrated operations. TETRA combines high-purity fluids with laboratory services to enhance operational efficiency, reduce risks, and support cost-effective drilling operations.

Drilling Fluids Market Report Scope

Drilling Fluids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.9 Billion

|

|

Market Size (2034)

|

$16.5 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Fluid Type (Water-Based Fluids (WBF), Oil-Based Fluids (OBF), Synthetic-Based Fluids (SBF), Others), By Application (Onshore, Offshore), By Well Type (Conventional Wells, High-Pressure High-Temperature (HPHT) Wells)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Schlumberger Limited, Halliburton, Baker Hughes Company, TETRA Technologies, Inc., Newpark Resources, Inc., National Oilwell Varco, Weatherford International plc, CES Energy Solutions Corp., AkzoNobel N.V., Scomi Group Bhd, Solvay S.A., Newpark Resources Inc., Exxon Mobil Corporation, Flotek Industries, Inc., China Oilfield Services Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Drilling Fluids Market Segmentation

By Fluid Type

- Water-Based Fluids (WBF)

- Oil-Based Fluids (OBF)

- Synthetic-Based Fluids (SBF)

- Others

By Application

By Well Type

- Conventional Wells

- High-Pressure High-Temperature (HPHT) Wells

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Drilling Fluids Industry include-

- Schlumberger Limited

- Halliburton

- Baker Hughes Company

- TETRA Technologies, Inc.

- Newpark Resources, Inc.

- National Oilwell Varco

- Weatherford International plc

- CES Energy Solutions Corp.

- AkzoNobel N.V.

- Scomi Group Bhd

- Solvay S.A.

- Newpark Resources Inc.

- Exxon Mobil Corporation

- Flotek Industries, Inc.

- China Oilfield Services Limited

*- List not Exhaustive

Research Coverage

The Drilling Fluids Market Report by USDAnalytics this report investigates how next-generation fluid systems are improving rate of penetration, lowering NPT, and safeguarding wellbore integrity across extended-reach, deepwater, and HPHT campaigns; it highlights breakthroughs in eco-forward water-based systems, advanced rheology/filtration-control additives, and AI-assisted hydraulics; delivers analysis reviews on fluid selection trade-offs, waste minimization, and digital surveillance of mud properties; and clarifies procurement and risk levers for operators and service companies. By connecting fluid chemistries to operational KPIs stability windows, ECD management, and bit/run life this report is an essential resource for drilling managers, fluids engineers, and supply-chain leaders aiming to align performance, compliance, and cost. Scope Includes-

- Segmentation

- By Fluid Type: Water-Based Fluids (WBF); Oil-Based Fluids (OBF); Synthetic-Based Fluids (SBF); Others

- By Application: Onshore; Offshore

- By Well Type: Conventional; High-Pressure High-Temperature (HPHT)

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Schlumberger Limited; Halliburton; Baker Hughes Company; TETRA Technologies, Inc.; Newpark Resources, Inc.; National Oilwell Varco; Weatherford International plc; CES Energy Solutions Corp.; AkzoNobel N.V.; Scomi Group Bhd; Solvay S.A.; Exxon Mobil Corporation; Flotek Industries, Inc.; China Oilfield Services Limited

Methodology

USDAnalytics applies a mixed-methods framework combining primary interviews (drilling superintendents, fluids specialists, offshore HSE leads, and procurement teams) with secondary validation (operator well files, service company disclosures, MSDS/spec sheets, regulatory filings, and academic literature). Bottom-up models quantify fluid demand by basin, rig count, lateral length, hole size, and HPHT incidence, then reconcile with top-down spend, mud plant throughput, and additive pricing. Forecasts (2025–2034) incorporate deepwater FIDs, unconventional activity indices, environmental policy shifts, and digital adoption rates (real-time mud logging/AI optimization). Competitive benchmarking scores systems on stability under temperature/pressure, ECD control, lubricity, shale inhibition, biodegradability, and total cost per foot drilled.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Drilling Fluids Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Drilling Fluids Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $10.9 Billion

2.2.2. Forecasted Market Size (2034): $16.5 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 4.7%

2.3. Market Drivers and Challenges

2.3.1. Drivers: High-Performance Fluids for Complex Wells, and Deepwater/Unconventional Drilling

2.3.2. Challenges: Oil Price Volatility and Environmental Regulations

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Rising Demand for Environmentally Friendly Drilling Fluids

3.2. Integration of IoT and AI for Real-Time Fluid Optimization

3.3. High-Performance Fluids for Extreme Well Conditions

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Corporate Mergers and Acquisitions

3.4.2. Technology and Product Launches

4. Drilling Fluids Market – Segmentation Insights

4.1. By Fluid Type

4.1.1. Water-Based Fluids (WBF, 48.5% Market Share)

4.1.2. Oil-Based Fluids (OBF, 26.9% Market Share)

4.1.3. Synthetic-Based Fluids (SBF, 22.5% Market Share)

4.1.4. Others

4.2. By Application

4.2.1. Onshore (64.3% Market Share)

4.2.2. Offshore (35.7% Market Share)

4.3. By Well Type

4.3.1. Conventional Wells (74.5% Market Share)

4.3.2. High-Pressure High-Temperature (HPHT) Wells (26.9% Market Share)

5. Country Analysis and Outlook: Drilling Fluids Market

5.1. United States: Technological Leadership and Federal Support

5.2. Saudi Arabia: Massive Infrastructure Investments and Offshore Expansion

5.3. China: Shale Gas Development and Smart Monitoring

5.4. Norway: Stringent Environmental Rules and Offshore Innovation

5.5. Canada: Research-Driven Wastewater Management

5.6. Russia: Domestic Innovation and Exploration Investments

6. Drilling Fluids Market Size Outlook by Region (2025–2034)

6.1. North America Drilling Fluids Market Size Outlook to 2034

6.1.1. By Fluid Type

6.1.2. By Application

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Drilling Fluids Market Size Outlook to 2034

6.2.1. By Fluid Type

6.2.2. By Application

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Drilling Fluids Market Size Outlook to 2034

6.3.1. By Fluid Type

6.3.2. By Application

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Drilling Fluids Market Size Outlook to 2034

6.4.1. By Fluid Type

6.4.2. By Application

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Drilling Fluids Market Size Outlook to 2034

6.5.1. By Fluid Type

6.5.2. By Application

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. Schlumberger Limited (SLB)

7.1.1. Company Overview

7.1.2. AI-Driven Drilling Fluid Solutions

7.2. Halliburton Company

7.2.1. Company Overview

7.2.2. Customized, High-Performance Fluid Systems

7.3. Baker Hughes, a GE company

7.4. Newpark Resources, Inc.

7.5. TETRA Technologies, Inc.

7.6. Other Prominent Companies

7.6.1. National Oilwell Varco

7.6.2. Weatherford International plc

7.6.3. CES Energy Solutions Corp.

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures