Dust Control Systems and Suppression Chemicals Market to Reach $20.8 Billion by 2034 at 4.9% CAGR Driven by AI-Enabled Monitoring and Stricter PM2.5 Regulations

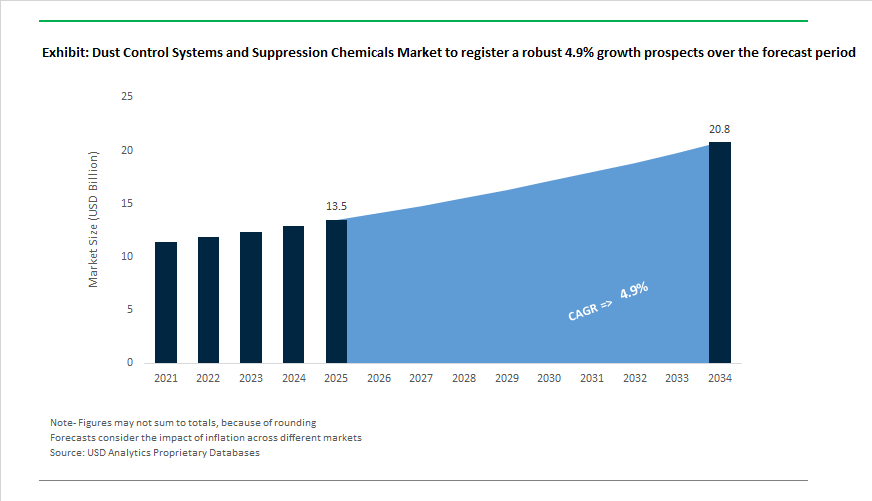

The Dust Control Systems and Suppression Chemicals Market is projected to grow from $13.5 billion in 2025 to $20.8 billion by 2034, reflecting a CAGR of 4.9%. Market expansion is being shaped by tightening environmental compliance standards, electrification of heavy equipment, and digital integration of air quality management systems. A major regulatory catalyst emerged in December 2024, when the European Union formally adopted a revised Ambient Air Quality Directive imposing stricter PM2.5 and PM10 limits. This policy shift has accelerated the replacement of legacy dust collectors with high-efficiency filtration systems and automated mist suppression technologies across manufacturing, mining, and construction sectors. In April 2024, Donaldson Company introduced the DFPRE 2 compact dust collector, engineered as a pre-assembled plug-and-play solution for facilities with limited floor space. The launch responded to increasing demand for modular systems capable of meeting evolving occupational health standards without major plant redesign.

Equipment innovation accelerated through 2024 and 2025 as suppliers aligned with electrification and automation trends. In March 2024, BossTek launched the DustBoss® DB-45 Surge®, a mobile mist cannon capable of projecting atomized water streams beyond 60 meters, even under high-wind conditions. Its remote-controlled surge functionality reduces water consumption and labor intensity on demolition and bulk material handling sites. In January 2025, Dynaset Oy introduced the EPW-DUST high-pressure suppression system specifically engineered for electric machinery. The solution converts DC or AC power into high-pressure mist, making it compatible with electric excavators and stationary crushing lines while optimizing water usage. Digital integration further strengthened the market in May 2025, when Emerson introduced industrial AI solutions that link real-time particulate sensors with automated suppression triggers. This enables facilities to dynamically adjust mist intensity and ventilation rates based on airborne dust concentration spikes, reducing manual intervention and improving compliance reporting accuracy.

Strategic acquisitions and chemical innovation are reinforcing supply chain capabilities across global mining and heavy industry markets. In March 2025, Nederman Holding AB completed the acquisition of Euro-Equip S.L., expanding its footprint in foundry and metallurgical dust extraction solutions in Southern Europe. Quaker Houghton confirmed in its 2024 annual disclosures the acquisition of two specialized additive companies to strengthen its industrial fluid portfolio, including advanced dust suppression chemistries tailored for steel and mining operations. Global Road Technology scaled its partnership with TotalEnergies throughout 2024, deploying SMART Dosing Units that autonomously regulate suppressant application, reducing water usage by up to 40% in large-scale mining operations. Meanwhile, Camfil introduced heavy-duty collectors with Gold Cone™ filter media in 2024, engineered for longer service life and reduced pressure drop to lower total cost of ownership. In September 2025, Ecovyst agreed to divest its Advanced Materials & Catalysts segment to Technip Energies, enabling strategic realignment of filtration material assets ahead of its Q1 2026 closing. These developments underscore the market’s transition toward energy-efficient filtration, AI-driven environmental control, and chemically optimized dust suppression systems tailored for high-compliance industrial environments.

Trends and Opportunities in the Dust Control Systems and Suppression Chemicals Market

Integration of IoT, Edge AI, and Predictive Analytics for Proactive Dust Management

- Industrial operators are rapidly moving away from manual and schedule-based water spraying toward fully automated, sensor-driven dust suppression ecosystems. These systems integrate IoT-enabled weather stations, particulate sensors, and real-time analytics to activate chemical dosing and misting only when dispersion risk is high.

- During 2024 and 2025, global mining leaders such as Rio Tinto and BHP accelerated deployment of digitally integrated environmental platforms as part of their Mines of the Future programs. At its 2025 Capital Markets Day, Rio Tinto highlighted a target of USD 650 million in annual productivity benefits, with a measurable share attributed to predictive environmental controls that reduced water consumption by approximately 15% through precision chemical application rather than continuous spraying.

- Technologically, the adoption of Edge AI and smart dust continuum architectures is a major enabler. In North America alone, the smart environmental monitoring segment was valued at approximately USD 60.6 million in 2024. By processing wind speed, humidity, and particulate data locally, suppression systems now activate based on real dispersion thresholds instead of fixed schedules. Industrial benchmarks from 2025 indicate that this approach improves chemical efficiency by close to 30% while materially lowering operating costs in water-stressed regions.

- Operational outcomes are also improving from a compliance perspective. Mining companies using digital twins for environmental monitoring reported up to 75% fewer dust-related violations in 2025 by predicting and mitigating plume formation before dust migrated beyond site boundaries. This shift positions advanced dust control systems as a preventive risk-management tool rather than a reactive compliance expense.

Regulatory Tightening and Continuous Enforcement Driving Adoption of Best Available Technology

- Environmental and workplace safety regulators are transitioning from periodic audits to continuous, data-driven enforcement models, fundamentally altering expectations for dust suppression performance. This has increased demand for certified, high-retention chemical suppressants and engineered delivery systems capable of demonstrating continuous compliance.

- In November 2025, Safe Work Australia finalized the transition to updated Workplace Exposure Limits, with enforcement beginning December 1, 2026. The revised standards include a five-fold reduction in permissible exposure for several airborne particulates, sharply increasing compliance pressure on construction, mining, and heavy manufacturing sites.

- Enforcement actions are becoming more financially material. The Irish Environmental Protection Agency reported in April 2025 that penalties for unauthorized particulate emissions reached as high as EUR 500,000 per incident. In the United States, the South Coast Air Quality Management District expanded its 2025 Annual Emissions Reporting program, requiring facilities emitting more than four tons of particulate matter to submit detailed quadrennial disclosures.

- At the same time, regulators are adopting drone-mounted LiDAR and opacity sensors to detect fugitive dust in real time. This environment of continuous visibility has driven a roughly 50% increase in demand for high-tack chemical suppressants that form durable surface crusts on haul roads and stockpiles, outperforming water-only methods that lose effectiveness within hours under high wind conditions.

Securing Critical Mineral Supply Chains for Lithium and Copper

- The global race to secure lithium, copper, and other energy transition metals is creating a major growth opportunity for advanced dust suppression chemicals, particularly in arid and environmentally sensitive regions. Large-scale extraction and processing operations require dust control solutions that protect product purity while meeting stringent permitting requirements.

- In October 2025, the U.S. Department of Defense allocated USD 2.5 billion toward securing strategic reserves of critical minerals. Projects such as Standard Lithium’s USD 1.1 billion Arkansas development are being subjected to rigorous NEPA reviews, where air quality management is a key approval criterion. This is accelerating adoption of non-toxic, low-residue suppression chemistries that prevent cross-contamination of lithium brines and concentrates.

- In South America, the Chilean government introduced new environmental frameworks in December 2025 governing the SQM–Codelco lithium partnership. These rules mandate continuous air quality and soil monitoring, creating immediate demand for biodegradable dust suppressants that do not interfere with high-value brine chemistry or fragile desert ecosystems.

- From an economic standpoint, dust control is increasingly viewed as product loss prevention. For copper producers such as Teck Resources, which is targeting 800,000 tonnes of annual copper output by 2030, industrial estimates suggest that effective chemical crusting and wind-barrier systems can prevent the loss of 1 to 2% of fine ore concentrates otherwise dispersed by wind erosion. At current copper prices, this translates into a material revenue protection lever.

Supporting Offshore Wind Port Infrastructure and Precision Assembly Operations

- The rapid expansion of offshore wind is opening a specialized niche for marine-safe dust control systems at coastal assembly and marshalling ports. These sites concentrate high-intensity cutting, grinding, and surface preparation activities for turbine towers, blades, and foundations, generating fine particulates in close proximity to sensitive marine environments.

- At the EERA DeepWind 2025 conference, industry participants highlighted that the shift toward 15 MW and larger turbines has effectively doubled the surface area requiring finishing and coating. This has significantly increased localized dust generation during onshore assembly, raising compliance and safety challenges for port operators.

- Major port expansion programs associated with offshore wind and renewable fuel hubs are investing in modular, electrified misting and chemical suppression systems. These installations require low-VOC, marine-compliant formulations that prevent runoff contamination while maintaining worker safety during abrasive blasting and composite finishing.

- Under the EU Fit for 55 framework, offshore wind developers are prioritizing zero-emission construction sites. This creates a strong opportunity for electrically powered, mobile dust suppression skids that eliminate diesel emissions while delivering high-pressure atomization and long-lasting chemical binding. As offshore wind installations accelerate through the next decade, dust control systems are becoming a critical enabler of schedule certainty, regulatory compliance, and ESG alignment at coastal infrastructure hubs.

Dust Control Systems and Suppression Chemicals Market Share and Segmentation Insights

Chloride-Based Dust Suppressants Capture the Largest Share Driven by Mining and Construction Road Applications

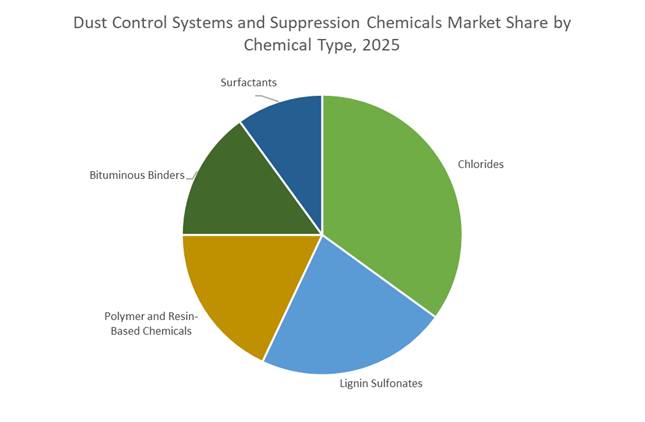

Chlorides account for 35% of global dust control chemicals market share in 2025, led by widespread adoption of calcium chloride, magnesium chloride, and sodium chloride across mining haul roads and construction access routes. Their hygroscopic properties enable continuous moisture absorption from ambient air, keeping unpaved surfaces damp and significantly reducing airborne particulate emissions. Cost efficiency and global availability position chlorides as the default solution for large-scale dust suppression programs. Lignin sulfonates follow as a significant segment, offering organic particle binding with lower corrosivity, particularly valued in soil stabilization and secondary road treatment. Polymer and resin-based dust suppressants are the fastest-growing category, delivering extended performance through film formation and encapsulation, increasingly specified in pharmaceutical manufacturing and food processing environments. Bituminous binders maintain importance for heavy-duty haul roads requiring surface hardening, while surfactants serve niche roles, enhancing wetting efficiency in integrated water spray and chemical dust control systems.

Mining and Mineral Processing Drives Nearly Half of Global Dust Suppression Chemical Demand

Mining and mineral processing represent 48% of total end-use demand, making this sector the primary revenue driver for dust control systems and suppression chemicals in 2025. Applications span haul roads, stockpiles, tailings facilities, and crushing operations, where regulatory compliance, worker safety, and operational continuity mandate robust dust mitigation strategies. Building and construction forms the second-largest segment, utilizing dust suppressants during demolition, earthmoving, and site preparation to meet local air quality standards and community expectations. Oil and gas operations rely on dust control across well pad roads, pipeline corridors, and frac sand handling to protect equipment and personnel in remote locations. Power generation facilities, especially coal-fired plants, deploy suppression chemicals at coal yards and ash handling areas to prevent fugitive emissions. Chemical, petrochemical, pharmaceutical, and food processing industries represent smaller but high-value segments, requiring contamination-safe formulations aligned with stringent hygiene and safety regulations.

Competitive Landscape of the Dust Control Systems and Suppression Chemicals Market

The Dust Control Systems and Suppression Chemicals market in 2026 is defined by rising regulatory pressure on airborne particulates, accelerating mining and construction activity, and the convergence of filtration hardware with smart chemical suppression technologies to reduce PM10/PM2.5 emissions, improve worker safety, and optimize water usage.

Donaldson drives industrial dust collection growth with high-margin filtration platforms

Donaldson Company, Inc. dominates the mechanical side of the dust control systems market through its Industrial Solutions segment, projecting record FY2026 sales of $3.8 billion, largely driven by dust and fume collection equipment. In February 2026, Donaldson launched ArmorSeal™, engineered for high-vibration mining and construction environments where uptime is critical. The company is also leveraging efficiency actions from 2025 to deliver all-time high operating margins in 2026. Its Gold Series III modular dust collectors (via Camfil APC) reduce energy consumption while enhancing capture of hazardous particulates, reinforcing Donaldson’s leadership in industrial air filtration, combustible dust management, and energy-efficient dust collection architectures.

Ecolab Nalco Water leads chemical dust suppression with digital dosing intelligence

Ecolab Inc., through Nalco Water, is the undisputed leader in chemical dust suppression, specializing in water-saving additives for mining, power, and bulk material handling. Its DustBind™ Plus and DUST-BAN™ programs use organic surfactants and tackifiers to agglomerate fines and maintain suppression after drying. A key differentiator is the integration of 3D TRASAR™ real-time monitoring, enabling automated dosing and performance optimization. Nalco’s global field service network supports complex ash pond and stockpile management projects, highlighted by a major 2026 Indian government contract with National Aluminium Company. This combination of chemistry, analytics, and on-site expertise positions Ecolab as the benchmark for large-scale industrial dust control.

Nederman advances smart clean-air systems for explosion-safe manufacturing

Nederman Holding AB anchors the European dust control landscape with its focus on worker protection and material recovery. The company is shifting toward explosion-proof combustible dust systems aligned with ATEX and NFPA standards, particularly for food processing and woodworking. During 2025 to 2026, Nederman significantly upgraded its SmartFilter portfolio, introducing cloud-based analytics that predict filter life and prevent unplanned downtime. It dominates automotive and manufacturing environments requiring localized extraction and high-vacuum welding solutions. Nederman’s turnkey model, spanning environmental audits through PLC-controlled centralized extraction, makes it a preferred partner for factories seeking compliant, digitally enabled dust collection systems.

Benetech prevents dust at the source with engineered material flow control

Benetech, Inc. specializes in bulk material dust control for coal, cement, and biomass facilities, emphasizing prevention over suppression. Its Cornerless MaxZone® chute design minimizes dust generation by stabilizing material flow, while MaxZone Safe+® targets respirable crystalline silica to meet stringent 2026 workplace exposure limits. Benetech also offers wet dust extractors using bifurcated fans and atomized water to achieve 99.7% capture efficiency without bag changes or compressed air. The company’s strategy centers on reducing client housekeeping costs through systemic washdown and integrated suppression programs, positioning Benetech as a process-engineering specialist in conveyor transfer point dust mitigation.

Global Road Technology scales polymer suppression for water-scarce mining regions

Global Road Technology (GRT) is an innovation-driven provider of aqueous polymer dust suppressants for mining haul roads and tailings. Its solutions form semi-permanent surface crusts that can reduce water truck frequency by up to 90%, a critical advantage in arid operations. In 2026, GRT expanded its Dust Suppression as a Service (DSaaS) model, shifting customers toward outcome-based air quality contracts. The company also accelerated growth across Chile and Peru, supplying foaming agents for open-pit mines. With a strong emphasis on non-toxicity and groundwater safety, GRT differentiates through environmental compliance and performance-based dust management.

United States: AI-Controlled Suppression and Bio-Based Chemical Transition

The United States dust control systems and suppression chemicals market is undergoing a rapid shift toward intelligent, regulation-aligned solutions. In January 2025, industrial equipment manufacturers rolled out AI-controlled misting systems that use real-time particulate sensors to dynamically adjust droplet size between 10 and 50 microns. These systems are specifically engineered for Western U.S. mining operations where water scarcity is a structural constraint. By optimizing droplet dispersion and flow rates, operators are achieving measurable reductions in water consumption while maintaining effective PM suppression across haul roads and crushing zones.

Regulatory momentum is accelerating chemical innovation. Under the U.S. EPA 2025–2026 Strategic Plan, tighter PM2.5 thresholds have triggered a 15% rise in the adoption of bio-based soil binders and biodegradable surfactants. Operators are deliberately moving away from chloride-based salts to mitigate long-term soil salinity and groundwater contamination risks. This policy environment has directly supported portfolio expansion by Ecolab through its Nalsco Water division, which scaled up the HAULAGE-DC™ road dust control line in 2025. These formulations reportedly reduce spray truck requirements by 77%, delivering downstream benefits in diesel fuel savings and emissions reduction. Parallel demand growth is visible in high-precision manufacturing. Donaldson Company introduced advanced mechanical dust collectors with HEPA-grade hybrid filtration, achieving 98% capture efficiency for particles as small as 0.1 microns. These systems are increasingly specified in aerospace and semiconductor facilities across Texas and Arizona, where airborne contamination directly impacts yield and compliance.

Australia: Silica Regulation and Renewable-Powered Suppression

Australia’s dust control market is being reshaped by occupational health enforcement and climate-adaptive system design. The introduction of stricter crystalline silica regulations in September 2024, covering more than 600,000 workers, has made IoT-enabled dust monitoring and automated chemical dosing a baseline requirement for mining and construction tenders through 2026. Compliance now depends not only on suppression effectiveness but also on continuous data logging and audit-ready reporting.

Strategic partnerships are reinforcing the shift toward environmentally safer chemistries. In 2025, Global Road Technology formalized a nationwide distribution alliance with TotalEnergies Marketing Australia. The collaboration focuses on polymer-based, non-toxic dust suppressants that enhance soil cohesion without petroleum runoff. At the same time, mining hubs in the Pilbara region are integrating solar-powered suppression skids. These autonomous units activate based on satellite-linked meteorological data and wind forecasts, reducing reliance on diesel generators and aligning dust mitigation with decarbonization targets.

China: Urban Compliance and Electronics-Grade Dust Management

China’s dust control systems market reflects a dual focus on urban air quality enforcement and high-tech manufacturing integrity. The Ministry of Industry and Information Technology’s 2025 Green Packaging and Chemical Regime has incentivized waterless and low-water dust suppression solutions, particularly in northern provinces facing chronic water stress. In response, BASF expanded production of biodegradable dust suppression formulations at its Shanghai operations to meet rising municipal and industrial demand.

Urban redevelopment is another major driver. Large demolition and infrastructure projects in the Pearl River Delta now mandate mobile, high-pressure fog cannons equipped with noise-reduction features to comply with upcoming 2026 National Air Quality Standards. Beyond construction, the electronics sector is emerging as a high-value application area. Following MIIT’s 2025 roadmap, Chinese manufacturers have achieved mass production of electronic-grade ultra-high-purity dust collectors capable of removing sub-micron particles in EV battery assembly lines. The strategic objective is to reach 70% domestic content by 2027, reducing reliance on imported cleanroom filtration technologies.

Canada: Cold-Climate Infrastructure and Critical Minerals Compliance

Canada’s dust suppression market is closely tied to infrastructure resilience and critical minerals development. The 2025 Federal Budget allocated $1 billion over four years to the Arctic Infrastructure Fund, prioritizing all-season road construction in northern regions. These projects rely heavily on magnesium chloride and lignin-sulfonate suppressants formulated to perform under extreme freeze-thaw cycles, ensuring road stability and dust control during short construction windows.

Mining-related demand is also strengthening. The launch of the $2 billion Critical Minerals Sovereign Fund in 2026 is driving centralized dust monitoring installations at new copper and lithium mines in Saskatchewan and British Columbia. These systems support compliance with stringent provincial environmental assessments and enable continuous PM tracking in sensitive ecosystems, positioning dust control as a core element of mine permitting and long-term social license to operate.

Germany: Circular Chemistry and Hydrogen-Era Applications

Germany’s dust control chemicals market is being shaped by circular economy regulation and energy transition projects. In preparation for the EU Packaging and Packaging Waste Regulation 2026, German chemical producers are accelerating the rollout of REACH-compliant, plant-based surfactants designed for extended application intervals in cement and steel plants. Evonik has positioned these formulations within its Maintenance 4.0 framework, emphasizing reduced downtime and lower lifecycle chemical consumption.

A notable emerging application is in hydrogen production. In late 2025, Suez partnered with BASF to develop specialized dust control systems for methane pyrolysis facilities. These systems prevent carbon black particulate buildup inside reactors, directly improving the operational efficiency of zero-emission hydrogen processes. This use case highlights how dust suppression is evolving from a compliance tool into a productivity enabler in next-generation industrial processes.

Dust Control Systems and Suppression Chemicals Market: Country-Level Strategic Snapshot

Dust Control Systems and Suppression Chemicals Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Key Application Areas

|

Structural Direction

|

|

United States

|

PM2.5 regulation and AI adoption

|

Mining, aerospace, semiconductors

|

Smart misting, bio-based binders

|

|

Australia

|

Crystalline silica enforcement

|

Mining, construction

|

IoT monitoring, solar-powered systems

|

|

China

|

Urban air quality and EV manufacturing

|

Demolition, EV batteries

|

Waterless suppression, cleanroom-grade collectors

|

|

Canada

|

Arctic infrastructure and critical minerals

|

Roads, mining

|

Cold-climate suppressants, centralized monitoring

|

|

Germany

|

Circular economy and hydrogen transition

|

Cement, steel, hydrogen reactors

|

Plant-based surfactants, extended-cycle systems

|

Dust Control Systems and Suppression Chemicals Market Report Scope

Dust Control Systems and Suppression Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.5 Billion

|

|

Market Size (2034)

|

$20.8 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By System Type (Wet Systems, Dry Systems), By Chemical Type (Lignin Sulfonates, Chlorides, Polymer and Resin-Based Chemicals, Surfactants, Bituminous Binders), By Application (Haul Roads and Unpaved Surfaces, Material Handling and Conveying, Stockpile Management, Blasting and Crushing, Demolition and Construction), By End-Use Industry (Mining and Mineral Processing, Building and Construction, Oil and Gas, Chemical and Petrochemical, Pharmaceuticals and Food Processing, Power Generation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., BASF SE, Donaldson Company, Inc., Suez Water Technologies & Solutions, Martin Engineering, Camfil AB, Nederman Holding AB, Dow Inc., Global Road Technology, Midwest Industrial Supply, Inc., Borregaard ASA, Quaker Houghton, Cargill, Incorporated, Soilworks, LLC, Sly Environmental Technology Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dust Control Systems and Suppression Chemicals Market Segmentation

By System Type

By Chemical Type

- Lignin Sulfonates

- Chlorides

- Polymer and Resin-Based Chemicals

- Surfactants

- Bituminous Binders

By Application

- Haul Roads and Unpaved Surfaces

- Material Handling and Conveying

- Stockpile Management

- Blasting and Crushing

- Demolition and Construction

By End-Use Industry

- Mining and Mineral Processing

- Building and Construction

- Oil and Gas

- Chemical and Petrochemical

- Pharmaceuticals and Food Processing

- Power Generation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dust Control Systems and Suppression Chemicals Industry

- Ecolab Inc.

- BASF SE

- Donaldson Company, Inc.

- Suez Water Technologies & Solutions

- Martin Engineering

- Camfil AB

- Nederman Holding AB

- Dow Inc.

- Global Road Technology

- Midwest Industrial Supply, Inc.

- Borregaard ASA

- Quaker Houghton

- Cargill, Incorporated

- Soilworks, LLC

- Sly Environmental Technology Ltd.

*- List not Exhaustive