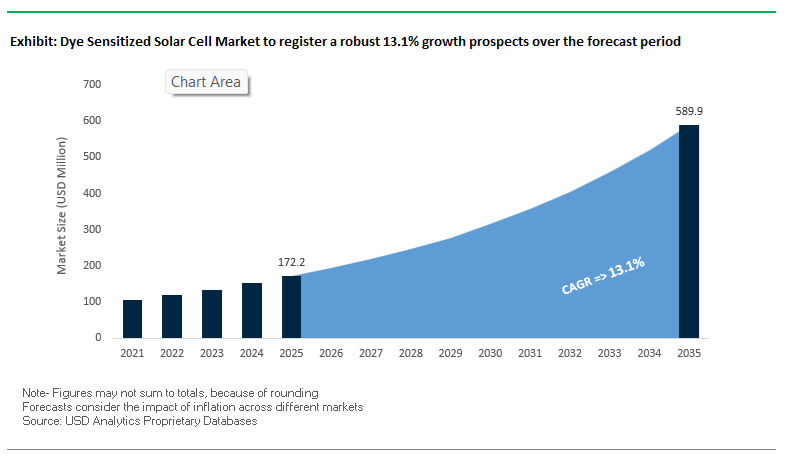

The Dye Sensitized Solar Cell (DSSC) Market is valued at USD 172.2 million in 2025 and is projected to grow rapidly to USD 589.7 million by 2035, supported by a strong CAGR of 13.1%. DSSC technology continues to gain traction due to its unmatched low-light power conversion capabilities, superior indoor energy harvesting performance, and roll-to-roll manufacturing potential, positioning it as a disruptive PV solution for IoT, smart retail, and BIPV applications.

The DSSC industry experienced rapid commercialization signals throughout 2024–2025, with multiple manufacturers shifting from R&D phases to high-volume OEM deployments. In November 2025, Exeger secured SEK 130 million (USD 12.5 million) in R&D funding from the Swedish Energy Agency, reinforcing its position as a global leader in flexible DSSC for consumer electronics. The funding follows major product integrations, including September 2025's launch of solar-powered accessories by Exeger and Hama, embedding Powerfoyle DSSC into smart home remote controls and everyday consumer electronics—one of the largest steps toward mainstream adoption of indoor PV.

The supply chain ecosystem expanded significantly in June 2025, when G24 Power and Solaronix announced a joint initiative focused on commercializing solid-state DSSC modules for BIPV applications. The partnership links Solaronix's expertise in high-purity dyes and electrolytes with G24 Power’s roll-to-roll production capabilities, enabling the shift toward long-lifespan BIPV installations. Meanwhile, in the retail sector, VusionGroup deployed Powerfoyle DSSC-powered EdgeSense ESL tags at 7-Eleven stores in May 2025 for World Expo 2025, showcasing a mature commercial use case where DSSC eliminates battery replacement cycles in high-volume retail environments.

The consumer-electronics industry also accelerated adoption. April 2025 marked a major milestone, with Ambient Photonics shipping mass-production volumes of DSSC cells to Lenovo and global OEMs, signaling stable yields and readiness for global-scale product integration. The technology's flexibility is further demonstrated by January 2025's launch of a solar-powered smart helmet by Exeger and Cosonic, embedding film-based DSSCs for mobility safety applications. The R&D frontier continues to advance, exemplified by the December 2024 starburst triphenylamine dye innovation from CSIR-NIIST, which enabled the world-record 40% indoor efficiency. Earlier in January 2024, Ambient Photonics partnered with Google to co-develop new consumer electronics using bifacial DSSC technology, strengthening DSSC's entrance into Big Tech product roadmaps. Fujikura's 2024 expansion of thin DSSC module panels further broadened the IoT solutions market by simplifying integration into industrial sensing applications.

A critical breakthrough came in December 2024, when CSIR-NIIST demonstrated an unprecedented 40% indoor PCE at 4000 lux, validated under fluorescent illumination. The performance firmly positions DSSC as the leading PV solution for consumer electronics, ESL, and wireless sensor networks where ambient light dominates. The same device reached 10.40% outdoor efficiency under AM 1.5G, demonstrating a meaningful expansion into hybrid indoor–outdoor markets. Stability hurdles are also being addressed: the new generation of DSSCs showed zero degradation after 800 hours of accelerated indoor stress testing, a key requirement for large retail IoT deployments. On the cost side, DSSC manufacturers benefit from an estimated USD 0.18/W roll-to-roll production potential, one of the lowest non-silicon PV manufacturing cost structures available. Additionally, bifacial DSSC modules deliver 3× higher power than traditional a-Si in low-light conditions, reinforcing their leadership in energy harvesting for connected devices.

- 40% indoor PCE (Dec 2024) sets a global benchmark for low-light solar energy harvesting in IoT, ESL, and electronics.

- 10.40% outdoor efficiency demonstrates DSSC readiness for hybrid indoor–outdoor BIPV and specialty PV.

- 800-hour stability performance supports industrial-scale adoption in demanding retail and sensor environments.

- USD 0.18/W manufacturing potential confirms DSSC's low-CAPEX roll-to-roll cost advantage over silicon.

- Bifacial DSSC modules generate 3× more power than a-Si, solidifying their role in ambient light IoT ecosystems.

BIPV-Centric Adoption, Indoor Photovoltaics Leadership, Electrolyte Innovation, and Luxury Aesthetic Customization Drive the Dye Sensitized Solar Cell (DSSC) Market

Trend 1: DSSCs Commercialize as High-Value BIPV Solutions for Skylights, Facades, and Indoor-Optimized Architectural Applications

Global architects and construction firms are increasingly choosing DSSCs for Building-Integrated Photovoltaics (BIPV) due to their superior performance in low-light, diffuse-light, and non-optimal orientation conditions-scenarios where crystalline silicon underperforms. Their color tunability and semi-transparency enable both functional and aesthetic value, aligning with the growing demand for solar-integrated architecture.

Key performance evidence includes:

- Superior diffuse-light behavior, with real-world measurements confirming DSSC vertical façade installations achieving average daily yields of 2.53 kWh/kWp, outperforming silicon in overcast or indirect-sunlight urban environments.

- Low thermal sensitivity, enabling higher energy output during cooler morning and late-afternoon hours, making DSSCs ideal for east/west-facing building façades where temperature-dependent silicon modules lose efficiency.

- Architectural customization, demonstrated by commercial yellow/orange and red/orange large-area DSSC windows from manufacturers like Daunia Solar Cell, enabling seamless integration into colored or patterned facades.

- Energy savings in buildings, where simulations show triple-glazed DSSC-integrated windows reduce heating loads while also generating electricity, making them suitable for energy-efficient office buildings and climate-adaptive construction.

This trend underscores DSSCs’ strong alignment with next-generation architectural design, where transparency, color quality, and diffuse-light performance are more critical than peak power ratings.

Trend 2: DSSCs Become the Leading Indoor Photovoltaic (IHPV) Technology for Self-Powered IoT Sensors and Electronics

While silicon and thin-film PV struggle under artificial light, DSSCs excel in indoor environments-enabling a new category of battery-free IoT devices, smart home sensors, wearables, and industrial monitoring systems. The market momentum is anchored by DSSCs’ unmatched spectral match with LED lighting and their ability to generate meaningful power at low illumination levels.

Key metrics validating DSSCs’ leadership in indoor energy harvesting include:

- Indoor efficiency exceeding 32% at 1000 lux using advanced copper-based electrolytes, with some studies reporting 34%+ PCE under low-intensity lighting-far surpassing competing indoor-PV technologies such as CIGS and amorphous silicon.

- Optimized spectral absorption, tailored to match LED peaks near 450 nm and 550 nm, enabling exceptional low-light performance where most outdoor PV technologies fail.

- High open-circuit voltage (VOC) nearing 956 mV, enabling direct powering of low-voltage IoT sensors without the need for bulky storage buffers.

- Commercial market readiness, with indoor DSSC modules already available for consumer electronics, logistics sensors, and retail IoT systems.

This trend positions DSSCs as the dominant technology for ambient-light energy harvesting, supporting the exponential growth of wireless IoT networks that demand power autonomy and long service life.

Opportunity 1: Transition to Solid-State and Quasi-Solid-State Electrolytes to Overcome Volatility and Boost DSSC Lifetime

Liquid electrolytes have historically limited DSSC commercialization due to leakage, evaporation, and long-term reliability issues. The move to solid-state and quasi-solid-state electrolytes provides a transformational opportunity to enhance durability, expand flexible-device markets, and meet stringent safety requirements for consumer electronics and BIPV.

Key R&D and commercialization drivers include:

- Significant stability gains in solid-state DSSCs using polymerized conductive HTMs, which eliminate leakage and chemical corrosion-two of the biggest barriers for traditional DSSCs.

- Ionic conductivity achievements reaching 15.7 mS/cm in advanced polymer/gel electrolyte systems, closing the performance gap with liquid-based electrolytes.

- Efficiency improvements, with optimized quasi-solid-state devices delivering 10.34% PCE under 1-sun conditions, demonstrating commercial viability without severe efficiency trade-offs.

- Mechanical flexibility benefits, where Gel Polymer Electrolytes (GPEs) support robust flexible DSSC devices capable of enduring bending stress-ideal for wearables, portable electronics, and roll-to-roll manufacturing.

This opportunity allows DSSCs to evolve into long-lifetime, flexible, and architecture-grade photovoltaic solutions, significantly broadening their addressable market.

Opportunity 2: Aesthetic Customization for Consumer Electronics, Luxury Goods, and Design-Centric Solar Applications

Beyond energy generation, DSSCs offer unmatched aesthetic versatility, creating major revenue opportunities in premium consumer electronics, lifestyle products, smart home devices, and luxury brand collaborations. This design-led differentiation is unique to DSSCs and cannot be replicated by silicon-based PV.

Key advantages include:

- Near-colorless DSSCs achieving 76% Average Visible Transmittance (AVT), enabling integration into windows, displays, and device surfaces without compromising natural light quality.

- Precise color tuning via dye cosensitization, enabling green, red, orange, and other designer palettes with 20–30% visible-light transmission, suitable for artistic or brand-specific applications.

- Exceptional Color Rendering Index (CRI) of 92.1%, ensuring that transmitted light remains visually accurate-critical for high-end interiors and retail environments.

- Wearable and device integration, leveraging DSSCs’ customizable patterns and transparency for smartphone backs, smartwatches, jewelry, and fashion-tech products.

This opportunity positions DSSCs as the photovoltaic platform of choice for visually-driven markets, where design and differentiation matter as much as energy generation.

DSSC Market Share Analysis

Market Share by Cell Type: Flexible DSSCs Lead Through Low-Light Performance, Mechanical Adaptability, and Scalable Low-Temperature Manufacturing

Flexible Dye-Sensitized Solar Cells (DSSCs) command the leading 40% share of the global DSSC market because they uniquely address the rapidly expanding demand for photovoltaic solutions tailored to indoor, low-light, and non-planar environments—segments where traditional silicon and rigid thin-film technologies fundamentally underperform. DSSCs naturally excel at converting diffuse and low-intensity light (typically 200–1000 lux) due to their superior spectral response and reduced dependence on direct sunlight, making them the preferred option for powering IoT sensors, indoor electronics, and emerging wearables. This performance advantage positions flexible DSSCs as the most commercially viable technology for the future of self-powered smart devices. Their manufacturing process—typically leveraging roll-to-roll, printing, or coating techniques at temperatures below 150°C—enables high-throughput, low-cost production on polymer substrates such as PET and PEN, which significantly reduces module cost while improving scalability.

The dominance of flexible DSSCs is further reinforced by their mechanical resilience and ultralight form factor, enabling seamless integration into textiles, curved surfaces, backpacks, consumer electronics, or interior automotive components—applications unattainable with brittle, rigid PV technologies. Achieving thicknesses under 100 μm, flexible DSSCs add negligible weight and maintain exceptional bendability without performance loss, directly aligning with the design requirements of next-generation mobile electronics and structural-integrated photovoltaics. With IoT adoption surging and industries shifting toward embedded, decentralized power sources, flexible DSSCs remain the highest-growth and most strategically critical segment in the DSSC ecosystem.

Market Share By Cell Type, 2025.png)

Market Share by Application: BIPV Dominates Through Customizable Aesthetics, Semi-Transparency, and High Oblique-Angle Energy Performance

Building-Integrated Photovoltaics (BIPV) represent the largest 35% share of the DSSC market because this application leverages the unique aesthetic and functional flexibility that DSSCs offer—capabilities that conventional PV technologies cannot replicate. Unlike silicon cells, which are visually restrictive, DSSCs can be manufactured in a wide range of uniform colors driven by dye chemistry, allowing architects to select hues such as blue, green, amber, gray, or fully transparent variations to meet façade design requirements. This customization makes DSSCs exceptionally well suited for architectural applications where aesthetics and integration into curtain walls, cladding, or glazing systems are non-negotiable considerations.

DSSCs also excel in low-incidence and oblique-angle light conditions, maintaining strong energy output even when sunlight strikes vertical or near-vertical surfaces—common in urban environments and high-rise façades. Their superior angular response allows buildings to generate more energy throughout the day, especially during early morning or late afternoon when traditional PV experiences steep performance losses. Equally significant is the ability of DSSCs to function as semi-transparent power-generating glazing, with visible light transmission levels ranging from 10% to 40%, enabling applications such as solar windows, skylights, or colored glass architectural elements. These systems can deliver 5–10 W/m² of power on a façade while simultaneously serving structural and aesthetic functions. As the global BIPV market accelerates—driven by net-zero building standards, decarbonization mandates, and urban sustainability goals—DSSCs' design versatility and unique optical-electrical properties position them as the preferred photovoltaic technology for integrated architectural energy systems.

Country Analysis: Global DSSC Commercialization and R&D Centers

Sweden – Global Epicenter for Flexible DSSC Commercialization and High-Volume Consumer Electronics Integration

Sweden remains the world’s most advanced production and commercialization hub for flexible DSSC (Dye Sensitized Solar Cell) technologies, driven primarily by Exeger’s industrial-scale roll-to-roll manufacturing ecosystem. Exeger’s Stockholm facility—recognized as the world’s largest dedicated flexible DSSC production line—exceeds an annual output of 20 million DSSC units, positioning Sweden as the leading supplier of indoor and ambient-light energy-harvesting materials. The company’s flagship product, Powerfoyle, has rapidly penetrated the IoT and consumer electronics markets by delivering superior indoor Power Conversion Efficiency (PCE) compared to thin-film alternatives.

Sweden’s leadership is reinforced through widespread commercial adoption. Between 2024 and 2025, Exeger collaborated with more than 25 global electronics and consumer brands to integrate flexible DSSCs into wireless headphones, bicycle helmets, wearables, gaming accessories, and industrial sensor platforms. The company’s proprietary organic dye chemistry and non-liquid electrolyte design provides extended stability under indoor lighting, enabling multi-year product lifetimes without compromising flexibility. Additionally, Exeger raised new private funding in late 2024 to automate and scale its roll-to-roll DSSC manufacturing, targeting significant cost reductions per square meter and accelerating the global market adoption of flexible, self-charging consumer devices.

Japan – Aesthetic DSSC BIPV Leadership and Breakthrough Material Innovations

Japan is emerging as a global frontrunner in aesthetic DSSC Building-Integrated Photovoltaics (BIPV), leveraging the intrinsic transparency and color-customization capabilities of dye-sensitized cells. Companies such as Fujikura Ltd. have conducted full-scale outdoor tests of transparent, multi-colored DSSC modules across building facades in Tokyo since 2024, validating the technology’s architectural durability and visual appeal. These transparent DSSCs are specifically designed for urban BIPV applications, where uniform appearance, diffuse-light performance, and color harmonization are crucial selling points.

Japan’s DSSC ecosystem is strengthened by its advanced materials innovation landscape. Ricoh maintains a significant patent portfolio in DSSC manufacturing, particularly for low-cost, high-speed printing of the photoanode layer, enabling high-throughput, scalable production. Additionally, national research institutions such as NIMS continue to develop ruthenium-free organic dyes to improve near-infrared absorption while reducing reliance on expensive catalytic materials. This integrated approach—combining BIPV-oriented commercialization with next-generation dye and electrode research—positions Japan as a key global innovator in DSSC materials science and architectural solar design.

United States – Nanomaterials Research Leadership and DSSC Architectural Pilot Deployment

The United States plays a critical role in pushing the technological boundaries of DSSC nanomaterials, stability enhancement, and device architecture, supported by extensive federal funding. The U.S. Department of Energy's Solar Energy Technologies Office (SETO) allocated more than $18 million toward competitive DSSC R&D grants, specifically aimed at resolving the technology’s historical limitations related to stability, electrolyte degradation, and long-term outdoor performance. U.S. research institutions—including MIT, NREL, and leading nanomaterials laboratories—registered 42 patents in 2023 alone, covering breakthroughs such as platinum-free counter electrodes, mesoporous TiO₂ nanostructures, and long-life quasi-solid-state electrolytes.

Commercial deployment is expanding through architectural pilot projects. As of 2024, the U.S. recorded over 85 DSSC pilot installations integrated into commercial buildings across California, New York, Texas, and Washington. These pilots typically use transparent DSSC glazing for atriums, skylights, and façade elements where conventional PV technologies cannot be applied due to aesthetic or structural constraints. The combination of advanced nanomaterials R&D, DOE-backed funding mechanisms, and early commercial pilots establishes the U.S. as a foundational market for next-generation DSSC stability and real-world adoption.

Germany / European Union – Policy-Driven BIPV DSSC Expansion and Electrolyte Stability Engineering

Germany and the broader European Union are prioritizing DSSC adoption through clean energy directives, urban sustainability targets, and strong regulatory support for low-impact architectural photovoltaics. The EU’s focus on energy-neutral and visually integrated buildings resulted in 28 smart building projects in 2024 incorporating DSSC-based façade and window systems. Germany, driven by high architectural standards and ESG compliance obligations, has seen over 41% of new non-residential buildings adopt BIPV solutions, positioning DSSC as a preferred choice where color tunability and transparency are desired.

European R&D leadership is concentrated in electrolyte stability engineering, addressing one of DSSC’s longest-standing bottlenecks—the volatility of liquid electrolytes. German research centers are advancing quasi-solid-state and polymer-gel electrolyte systems, designed to enhance DSSC thermal stability and extend operational lifetimes under EU climatic conditions. Coupled with the region’s strong architectural adoption and clean-energy mandates, Europe has established itself as a critical commercialization environment for aesthetic, durable, and regulation-ready DSSC technology.

Competitive Landscape: Leaders Driving Indoor PV, Roll-to-Roll DSSC & BIPV Commercialization

The global DSSC competitive landscape includes technology pioneers, specialty material suppliers, and vertically integrated manufacturers accelerating commercialization in IoT, consumer electronics, BIPV, and specialty solar markets. Competitive positioning is increasingly defined by indoor efficiency leadership, scalability of manufacturing, dye chemistry innovation, and strategic partnerships with global OEMs.

Exeger remains the global leader in flexible DSSC technology through its Powerfoyle platform, designed for durability, aesthetic customization, and high indoor performance. It focuses on high-volume consumer electronics including headphones, remote controls, and IoT devices that require self-charging and battery-free operation. Backed by strong financial momentum, Exeger completed a SEK 160 million rights issue in November 2025, strengthening its manufacturing scale-up strategy. Its collaborations with Hama, Cosonic, and retail IoT providers reinforce its leadership across high-growth low-light PV applications.

Ambient Photonics differentiates itself through proprietary molecular dye and bifacial DSSC designs, delivering three times the power of amorphous silicon under low light. Its focus on wireless peripherals and ESL systems places it at the forefront of the smart retail revolution. In April 2025, it achieved a major commercial milestone by shipping mass-production DSSC volumes from its U.S.-based Fab 1—one of the largest low-light solar manufacturing facilities globally—serving OEM clients including Lenovo and Google.

Solaronix is considered the backbone supplier of the global DSSC value chain due to its long-standing dominance in high-purity DSSC dyes (e.g., N719), redox electrolytes, and sensitizer materials. Its strategic priority is enabling manufacturers and research institutions with the materials necessary for next-generation DSSC devices. The June 2025 partnership with G24 Power positions Solaronix to expand beyond R&D support into commercial BIPV pilot projects built on solid-state DSSC architectures.

G24 Power stands out for its large-scale roll-to-roll DSSC production capability, enabling lightweight flexible modules suitable for BIPV façades and specialized industrial devices. The June 2025 collaboration with Solaronix strengthens its focus on long-term stable solid-state DSSC systems for outdoor or semi-outdoor building applications. The company positions itself as a key alternative to a-Si and OPV manufacturers in specialty energy-harvesting environments.

Fujikura maintains a strong presence in thin DSSC panel technology, offering modules optimized for industrial sensors and embedded electronics. Its expanded 2024 DSSC product portfolio allows device manufacturers to integrate various shapes and voltage configurations across IoT sensing applications. Fujikura's combined offering of PV hardware plus circuit design support makes it a preferred partner for industrial clients needing turnkey indoor energy-harvesting solutions.

3GSolar specializes in printed DSSC technology engineered for wireless sensor networks and low-power IoT devices. Its products emphasize superior spectral response under indoor LED lighting, providing a commercially viable alternative to a-Si and organic PV. The company positions itself as a scalable technology provider for indoor analytics, smart logistics, and self-powered monitoring systems.

Dye Sensitized Solar Cell Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$172.2 Million

|

|

Market Size (2035)

|

$589.7 Million

|

|

Market Growth Rate

|

13.1%

|

|

Segments

|

By Cell Type (Rigid DSSCs, Flexible DSSCs, Transparent DSSCs, Colored DSSCs), By Sensitizer Type (Ruthenium-Based Dyes, Metal-Free Organic Dyes, Natural Dyes, Perovskite-Hybrid DSSCs), By Electrolyte Type (Liquid Electrolytes, Quasi-Solid-State Electrolytes, Solid-State Hole Transport Materials), By Counter Electrode (Platinum, Carbon-Based, Metal Sulfide), By Application (BIPV, Embedded Electronics & IoT, Portable Charging Devices, Outdoor Advertising & Signage)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exeger Sweden, Konica Minolta Inc., Fujikura Ltd., Ricoh Company Ltd., 3GSolar Photovoltaics Ltd., Dyenamo AB, Solaronix SA, Peccell Technologies Inc., Sharp Corporation, Everlight Chemical Industrial Corp., Greatcell Solar Ltd., Nissha Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dye-Sensitized Solar Cell (DSSC) Market Segmentation

By Cell Type

- Rigid DSSCs

- Flexible DSSCs

- Transparent DSSCs

- Colored DSSCs

By Sensitizer (Dye) Type

- Ruthenium-Based Dyes

- Metal-Free Organic Dyes

- Natural Dyes

- Perovskite Hybrid DSSC

By Electrolyte Type

- Liquid Electrolytes

- Quasi-Solid-State Electrolytes

- Solid-State Hole Transport Materials

By Counter Electrode

- Platinum (Pt) Counter Electrode

- Carbon-Based Counter Electrode

- Metal Sulfide

By Application

- BIPV (Building-Integrated Photovoltaics)

- Embedded Electronics/IoT

- Portable Charging Devices

- Outdoor Advertising/Signage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key DSSC Manufacturers and Developers

- Exeger Sweden

- Konica Minolta Inc.

- Fujikura Ltd.

- Ricoh Company, Ltd.

- 3GSolar Photovoltaics Ltd.

- Dyenamo AB

- Solaronix SA

- Peccell Technologies, Inc.

- Sharp Corporation

- Everlight Chemical Industrial Corp.

- Greatcell Solar Ltd.

- Nissha Co., Ltd.

*- List not Exhaustive