E-Coat Market Size, Growth Trajectory, and Strategic Industry Positioning (2025–2032)

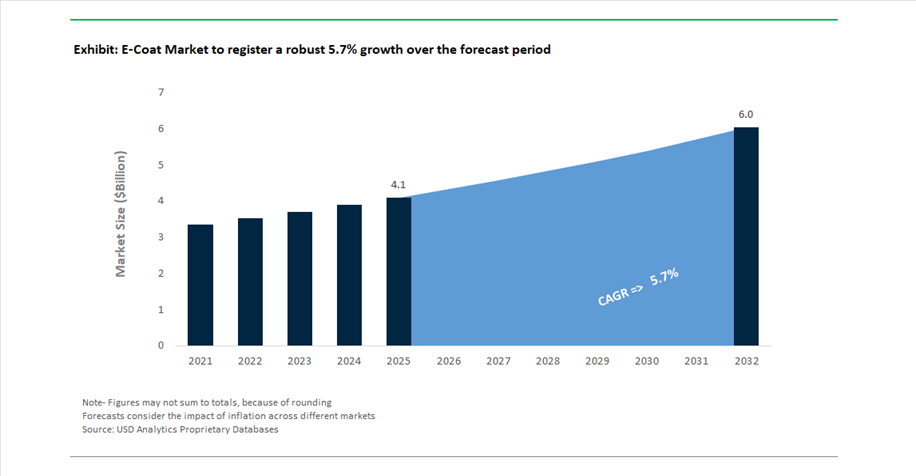

The global E-Coat Market reached a valuation of USD 4.1 billion in 2025 and is projected to expand at a CAGR of 5.7% through 2032, ultimately attaining USD 6 billion by 2032. This growth trajectory reflects the increasing strategic importance of electrophoretic deposition (E-coating) technologies across automotive, industrial equipment, and emerging electric mobility ecosystems. E-coating remains a foundational corrosion protection solution, particularly valued for its uniform coating thickness, high transfer efficiency, and ability to coat complex geometries, including recessed and internal surfaces.

A major structural driver underpinning market expansion is the global transition toward electric vehicles (EVs) and lightweight material architectures. As OEMs shift toward aluminum-intensive body-in-white (BIW) designs and high-voltage battery systems, the technical requirements for E-coat formulations have evolved significantly. Demand is rising for dielectric coatings, high-edge protection performance, and compatibility with multi-material substrates, positioning advanced cathodic epoxy E-coats as a critical enabler in next-generation vehicle platforms.

From a competitive standpoint, the industry is consolidating around a few large multinational coating players, with increasing vertical integration and technology-driven differentiation. The market is transitioning from commoditized corrosion protection toward high-performance, application-specific coating solutions, particularly in EV battery enclosures, heavy machinery, and industrial components. This shift is expected to sustain long-term value creation across the E-Coat Market ecosystem.

Technology Evolution, M&A Consolidation, and EV-Centric Innovation Reshaping the E-Coat Market

The E-Coat Market is undergoing a phase of accelerated transformation, driven by strategic mergers, capacity expansions, and advanced material innovation. A landmark development occurred in November 2025, when AkzoNobel and Axalta Coating Systems announced a $25 billion merger of equals. This consolidation is expected to significantly reshape the competitive landscape by combining extensive E-coat portfolios across mobility and industrial segments. The merged entity aims to enhance scale efficiencies, expand R&D capabilities, and strengthen its position in corrosion protection technologies. The transaction is anticipated to close by late 2026, marking one of the most influential consolidations in the coatings industry.

Capacity expansion initiatives are also playing a critical role in addressing regional demand imbalances. In March 2025, BASF completed a major expansion at its Caojing facility in Shanghai, with further process optimization for electrocoat binder production scheduled for early 2026. This aligns with rising demand from EV manufacturers and industrial coaters across Asia-Pacific. Similarly, Kansai Nerolac Paints strengthened its domestic market presence through its February 2026 amalgamation with Nerofix, enhancing distribution capabilities and technical service integration in India’s automotive coatings segment.

Technological innovation is increasingly centered on EV-specific coating requirements. In September 2025, PPG Industries introduced advanced dielectric E-coat systems designed for EV battery enclosures, addressing the shift toward 800V and 1,000V architectures. These formulations enhance electrical insulation and thermal management, which are critical for battery safety and performance. Parallel innovations include the commercialization of nanometer-scale silica and graphene-enhanced E-coat resins, improving edge protection and coating uniformity, thereby reducing secondary processing requirements.

Sustainability is emerging as a core innovation vector. BASF introduced its “ROUTING” automotive color trends (October 2024), incorporating bio-based and carbon-negative materials into E-coat systems to align with tightening environmental regulations. Additionally, Henkel enhanced its Alodine pretreatment solutions in November 2024, ensuring compatibility with modern E-coats on aluminum substrates, a critical requirement in lightweight vehicle manufacturing.

Strategic expansion into regional markets is also evident. Sherwin-Williams strengthened its Latin American footprint through the integration of Suvinil in January 2026, targeting agricultural and construction equipment sectors. Meanwhile, Nippon Paint Holdings adopted an “asset-assembly” M&A strategy in February 2026, focusing on acquiring localized industrial coating service providers in the U.S. and Europe to balance its strong Asian presence.

EU REACH Regulation 2024/3190 Accelerating BPA-Free Cationic Epoxy E-Coat Formulations

The enforcement of EU REACH Regulation (EU) 2024/3190 is fundamentally restructuring the chemistry landscape of the global e-coat industry, particularly within cationic epoxy electrodeposition coatings widely used in automotive and industrial applications. With the final implementation deadline set for July 20, 2026, the regulation mandates a complete ban on Bisphenol A-containing coatings, forcing manufacturers to transition toward BPA-intent-free resin systems. This shift is not limited to compliance adjustments but is driving a broader transformation in formulation science, as alternative cross-linking chemistries must deliver equivalent or superior corrosion resistance benchmarks, typically exceeding 1,000 hours in salt spray testing. The elimination of BPA as a monomer or starting substance is also closely aligned with tightening occupational safety standards across Europe, where regulatory bodies are targeting a 30% reduction in hazardous chemical exposure by 2030. While limited derogation windows extend until January 2028 for specialized reusable professional equipment, the majority of industrial and automotive supply chains are already undergoing rapid reformulation cycles to meet 2026 compliance thresholds. This regulatory pressure is intensifying R&D investments in phenol-free epoxy systems, hybrid resin platforms, and novel curing agents, reshaping competitive positioning among global e-coat manufacturers and creating a clear differentiation between compliant and legacy product portfolios.

China GB/T 33240-2024 Driving Lead-Free E-Coat and Zirconium-Based Pretreatment Adoption

China’s enforcement of GB/T 33240-2024 and associated environmental frameworks is accelerating the transition toward heavy-metal-free electrodeposition coating processes, reinforcing the country’s broader Green Factory initiative across automotive and industrial manufacturing hubs. By 2026, more than 75% of Tier 1 automotive e-coat lines in China have shifted from traditional zinc-phosphate pretreatment systems, which often contain chrome or nickel, to zirconium-based thin-film pretreatment technologies. This transition significantly reduces sludge generation by up to 90%, improving operational efficiency while lowering environmental impact. Simultaneously, the strict prohibition of lead-based pigments and catalysts in e-coat formulations under the updated standard requires manufacturers to maintain lead concentrations below 10 ppm, driving widespread adoption of bismuth-catalyzed systems. The elimination of heavy metals has also delivered measurable cost benefits, with facilities reporting a 15% to 20% reduction in wastewater treatment operating expenses due to simplified coagulation and filtration processes. Regulatory enforcement is intensifying through increased inspection frequency by the State Administration for Market Regulation, particularly under the General Rules for Safety Management of Coating Operations (GB 7691-2025), with unannounced audits becoming standard practice as of May 2026. These developments are accelerating technology upgrades, increasing compliance costs for smaller operators, and consolidating market share among technologically advanced e-coat solution providers.

Low-Cure 120°C E-Coat Technology Unlocking EV Battery Enclosure Applications

The rapid electrification of the automotive industry is generating a high-growth opportunity for low-cure e-coat technologies specifically engineered for electric vehicle battery enclosures and mixed-material assemblies. Traditional electrodeposition coatings require curing temperatures near 180°C, which can compromise heat-sensitive battery components and structural adhesives. The development of low-cure e-coat systems operating within the 120°C to 140°C range addresses these limitations while delivering substantial energy efficiency gains. Manufacturers adopting low-temperature curing processes are achieving a 20% to 30% reduction in oven energy consumption, directly supporting decarbonization targets and reducing operating costs in high-volume production environments such as EV giga-factories. The lower thermal exposure also improves material compatibility in multi-substrate assemblies, reducing the risk of thermal expansion mismatch and adhesive degradation by approximately 45%, a critical factor in battery pack integrity. Additionally, throughput efficiency is enhanced through faster cooling cycles, enabling up to 15% improvement in production line speed. From a performance standpoint, advanced low-cure e-coats are achieving dielectric breakdown voltages exceeding 1,000V, ensuring robust electrical insulation between battery modules and vehicle chassis. This combination of energy savings, material compatibility, and functional performance is positioning low-cure e-coat technology as a core enabler of next-generation electric mobility platforms.

Advanced E-Coat Solutions for High-Strength Steel and Press-Hardened Steel Protection

The increasing adoption of Advanced High-Strength Steel and Press-Hardened Steel in automotive structures is creating a specialized opportunity for high-performance e-coat formulations engineered for enhanced corrosion protection and mechanical integrity. These materials are critical for crash safety components such as B-pillars and structural rails but present unique coating challenges, particularly at sharp edges and laser-cut surfaces where corrosion initiation is most likely. Next-generation “Edge-Protect” e-coat technologies introduced by 2026 are delivering up to 200% improvement in film build at critical edge geometries, significantly enhancing corrosion resistance in high-stress zones. Concurrently, hydrogen embrittlement mitigation has emerged as a key innovation focus, with advanced amine-neutralized resin systems reducing the diffusion of atomic hydrogen into steel during the electrodeposition process, thereby minimizing the risk of delayed structural failure in safety-critical components. The ability of e-coat to provide uniform, high-performance coverage also supports the use of ultra-thin gauge high-strength steel, in some cases as low as 0.8 mm, contributing to vehicle lightweighting strategies and enabling weight reductions of up to 15 kilograms per body-in-white. Performance validation standards have also become more stringent, with coatings required to pass 1,500-hour cyclic corrosion tests such as GMW14872 while maintaining creepage values below 2 mm. These advancements are reinforcing the role of e-coat as a foundational technology in modern automotive design, particularly in the transition toward lightweight, high-strength vehicle architectures.

Water-Borne E-Coat Technology Dominates with 92% Share Driven by VOC Compliance and Superior Deposition Efficiency

Technology Analysis: Cathodic Epoxy Electrocoat Leads with Uniform Coverage and Near-Zero Waste

Water-borne electrocoat (E-Coat) technology commands an overwhelming 92.0% share of the global E-Coat market in 2025, driven by its unmatched ability to meet stringent VOC and HAP regulations while delivering high-volume industrial coating efficiency. These systems, composed of 95–98% deionized water with dispersed epoxy or acrylic resins, operate at VOC levels below 12 g/L, ensuring compliance with EPA NESHAP 6H and EU Industrial Emissions Directive (IED) standards. The electrophoretic deposition process provides >95% transfer efficiency, virtually eliminating coating waste compared to conventional spray systems. Additionally, the self-limiting film build mechanism ensures consistent coating thickness (15–25 microns) across complex geometries, including internal cavities and weld seams. Combined with intrinsic fire safety and reduced capital costs, water-borne cathodic epoxy E-Coat remains the backbone of the global industrial coating and automotive primer market.

Corrosion Protection Function Leads with 68% Share Driven by Automotive Durability Standards and Multi-Metal Compatibility

Functional Requirement Analysis: Anti-Corrosion E-Coat Systems Enable Long-Term Asset Protection

Corrosion protection accounts for a dominant 68.0% share of the E-Coat market in 2025, as it represents the core functional requirement across industries such as automotive, appliances, construction equipment, and electrical enclosures. In the automotive sector, cathodic epoxy E-Coat is essential for meeting 10–12 year corrosion warranty requirements, providing uniform protection to entire vehicle bodies, including hidden cavities, hem flanges, and boxed structures that are inaccessible to traditional spray coatings. This technology also offers excellent adhesion across multi-metal substrates, including galvanized steel, aluminum, and magnesium alloys, supporting lightweight vehicle designs. Additionally, advanced high-throw power E-Coat formulations enable deep penetration into complex structures, enhancing durability and corrosion resistance. These performance advantages position corrosion protection as the primary driver of demand in the global electrocoating (E-Coat) market.

E-Coat Market Competitive Landscape Driven by Cathodic Electrocoat Technology, EV Applications, and Sustainable Resin Innovation

The E-coat market is highly competitive, driven by demand for cathodic electrocoating, corrosion protection, and energy-efficient coating systems. Key players focus on EV battery protection, low-temperature curing, AI-driven coating development, and sustainable resin technologies across automotive OEM, industrial, and infrastructure applications.

PPG Leads Cathodic E-Coat Innovation with AI Integration and EV Battery Protection

PPG Industries, Inc. continues to dominate the E-coat industry with $15.9 billion in 2025 sales, supported by a strong shift toward sustainably advantaged coatings, which account for 43% of revenue. The company is advancing AI-designed coatings and digital tools to optimize first-pass yield and reduce production defects in high-volume electrocoat lines. PPG’s leadership in cathodic electrocoat technology is reinforced by its focus on dielectric coatings for EV battery housings, securing major OEM contracts in Europe and North America. Its streamlined portfolio emphasizes high-margin automotive and industrial coatings following strategic divestitures. The company’s innovation and digitalization strategy enhances efficiency and sustainability. PPG remains a global leader in advanced E-coat technologies.

BASF Advances Premium E-Coat Systems with Sustainable Resins and Multi-Metal Protection

BASF Coatings is strengthening its position in the E-coat market with advanced cathodic epoxy systems designed for premium automotive applications. Its DRIVING THE PROXY collection integrates aesthetic innovation with high-performance protection, offering liquid-metal effects within E-coat layers. BASF is pioneering renewable and recycled raw materials in resin formulations to meet EU circular economy requirements. Its coatings deliver superior throw-power and edge protection, critical for lightweight aluminum and multi-material vehicle structures. The company maintains strong dominance in the EMEA automotive coatings segment. Its focus on sustainability and technical excellence reinforces its leadership in next-generation electrocoat systems.

Axalta Expands Functional E-Coatings with High Margin Growth and Low-Temperature Cure Technologies

Axalta Coating Systems achieved strong financial performance with a 22.0% EBITDA margin and $5.11 billion in 2025 sales, supporting its leadership in industrial and automotive coatings. The company is investing in fast-cure, low-temperature E-coatings that reduce energy consumption for OEMs by up to 15%. Its Zencore™ system demonstrates integration across diverse substrates beyond traditional automotive applications. Axalta’s innovation leadership is highlighted by multiple Edison Awards for advancements in EV safety coatings and AI-driven color technologies. Strong free cash flow enables continued R&D investment. Its focus on energy-efficient and functional coatings strengthens its competitive position in the E-coat market.

Sherwin-Williams Expands Industrial E-Coatings with Strong Supply Chain and Equipment Sector Growth

The Sherwin-Williams Company is strengthening its E-coat presence through its Performance Coatings Group, which reported a 12.6% increase in segment profit in 2025. Demand for high-durability electrocoatings in heavy equipment and agricultural sectors is driving growth. The integration of Suvinil enhances its reach in emerging markets and supports broader industrial coatings expansion. Sherwin-Williams leverages its robust supply chain and logistics network to scale specialty coatings efficiently across North and Latin America. Its financial outlook for 2026 reflects steady growth despite macroeconomic challenges. The company’s operational strength supports its competitive positioning in industrial E-coatings.

Nippon Paint Expands Asia-Pacific E-Coat Leadership with Sustainability and Resin Integration

Nippon Paint Holdings (NIPSEA Group) is expanding its E-coat market presence through its asset assembler strategy and the $2.3 billion acquisition of AOC, strengthening upstream resin integration. The company is prioritizing sustainability, with 59% of its development portfolio focused on eliminating hazardous chemicals. Asia-Pacific remains its core market, accounting for over 55% of global E-coat demand. Nippon Paint is improving financial flexibility, targeting a Net Debt/EBITDA ratio of ~2.0x by 2026 to support further expansion. Its decentralized structure enables rapid regional responsiveness. The company’s focus on sustainable coatings and regional dominance strengthens its position in the E-coat industry.

AkzoNobel Strengthens E-Coat Portfolio with Self-Healing Technologies and Strategic Consolidation

AkzoNobel N.V. is advancing its E-coat capabilities through a proposed merger with Axalta, which would significantly enhance its R&D scale and market presence. The company is investing in self-healing electrocoat technologies to extend asset life in protective and marine applications. Its strong financial performance, including a 27% increase in operating income in 2025, supports continued innovation and expansion. AkzoNobel is also focusing on nearshoring strategies to support agricultural and construction equipment manufacturers in Latin America. Its emphasis on cost discipline and advanced coatings technology reinforces its competitive positioning. The company’s strategic initiatives align with long-term growth in electrocoating solutions.

China E-Coat Market: Green Industrialization and EV Expansion Driving Global Dominance

China remains the epicenter of the e-coat (electrodeposition coating) market, driven by aggressive decarbonization policies under the 15th Five-Year Plan (2026–2030). The integration of green finance mechanisms—including over $6.2 trillion in green loans—is accelerating the transition toward waterborne and high-solids e-coat systems in industrial parks.

Regulatory pressure is reshaping production. Policies are phasing out traditional spray booths in favor of automated electrodeposition systems with zero-liquid discharge (ZLD) compliance. The rapid growth of the EV sector is also a key driver, with expansion of cathodic epoxy e-coat lines for lithium-ion battery housings, providing dielectric insulation. Additionally, regional innovation hubs such as Jiangsu are advancing hybrid coating systems for plastic-metal substrates, reinforcing China’s leadership in scalable and sustainable e-coat technologies.

United States E-Coat Market: Infrastructure Investment and Fire-Safety Innovation Driving High-Performance Demand

The United States market is evolving toward high-performance epoxy systems and specialized coatings. Federal infrastructure investments are driving demand for durable e-coat systems in bridges, marine assets, and industrial equipment.

Innovation is particularly strong in safety and advanced materials. The launch of intumescent polyurethane e-coats (2025) is enhancing passive fire protection (PFP) in EV components. Developments such as advanced amine curing agents (e.g., Baxxodur EC 151) are improving chemical resistance in industrial applications. Regulatory enforcement under EPA NESHAP is pushing manufacturers toward closed-loop e-coat recovery systems, while aerospace adoption of chrome-free anodic e-coatings is supporting lightweight aluminum structures. Additionally, automotive OEM demand is rising, with coatings optimized for sensor compatibility in autonomous vehicles.

Japan E-Coat Market: Precision Engineering and Smart Manufacturing Driving Innovation

Japan leads in high-precision and miniaturized e-coating applications, particularly for electronics and advanced manufacturing. The commercialization of low-temperature curing cathodic e-coat systems (2025) enables coating of heat-sensitive plastic-metal hybrids, expanding application scope.

The market is also defined by digitalization. The adoption of real-time traceability tools ensures aerospace-grade quality control, while specialized e-coat lines deliver ultra-thin (5–10 micron) coatings for wearable devices and sensors. Growth in robotics and EV sectors is driving demand for corrosion-resistant coatings in robotic joints and thermally conductive coatings for battery components. These innovations position Japan as a leader in precision and smart e-coating technologies.

Germany E-Coat Market: Circular Coating Systems and Automotive Innovation Driving Sustainability

Germany is redefining the e-coat market through sustainability and automotive innovation. The adoption of UV-cured e-coat technologies is reducing energy consumption by eliminating traditional thermal curing processes, significantly lowering carbon emissions in automotive manufacturing.

Material innovation is also a key focus. German manufacturers are shifting toward bio-based epoxy resins to reduce dependence on fossil-based feedstocks, while developing coatings that enhance adhesion across multi-material vehicle structures (e.g., carbon fiber, aluminum, steel). Additionally, e-coat formulations are being optimized to ensure compatibility with LiDAR and radar systems, critical for next-generation EVs. Strict compliance with REACH and EU emission directives has also resulted in the elimination of lead and chromium-based pigments.

India E-Coat Market: Capacity Expansion and Automotive Growth Driving High Demand

India is experiencing rapid growth in the e-coat market, supported by expanding manufacturing and policy incentives. The establishment of Coating Technical Centers (e.g., Gurugram, 2025) is strengthening localized R&D and application support.

The automotive sector is a major driver. Growth in commercial vehicle fleets is increasing demand for cathodic epoxy e-coats, while the PLI scheme for Advanced Chemistry Cells (ACC) is driving dedicated e-coat lines for EV battery housings. The market is also seeing increased adoption in the refinish sector, with OEM-grade primers integrated into body shops. Additionally, rural industrialization is expanding demand for low-cost anodic e-coats in agricultural equipment, improving durability in harsh environments.

Brazil E-Coat Market: Agribusiness Expansion and Heavy Equipment Demand Driving Growth

Brazil’s e-coat market is closely tied to its agribusiness and heavy machinery sectors. Government investments under the Harvest Plan (BRL 475 billion) are driving strong demand for e-coated tractors and harvesters, ensuring durability under harsh field conditions.

Industrial expansion is also a key factor. Growth in ethanol production is increasing demand for corrosion-resistant e-coated storage and processing equipment, while infrastructure investments are boosting use of e-coated transport frames and containers. Local manufacturers are also advancing automation in e-coating processes, improving efficiency and consistency. Additionally, R&D into coatings resistant to humidity and acidic soil conditions is enhancing equipment lifespan, positioning Brazil as a resilient and application-driven market.

E-Coat Market Report Scope

E-Coat Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2032)

|

$6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Cathodic Electrocoating, Anodic Electrocoating), By Resin Type (Epoxy, Acrylic, Polyurethane, Hybrid, Others), By Technology (Water-borne, Solvent-borne), By Application (Automotive, Industrial Equipment, Consumer Goods and Appliances, Building and Architecture, Aerospace and Defense, Marine), By Substrate (Steel, Aluminum, Copper, Magnesium and Other Alloys), By Functional Requirement (Corrosion Protection, Decorative, High-Throw Power, Dielectric)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., BASF SE, Axalta Coating Systems Ltd., The Sherwin-Williams Company, AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Henkel AG & Co. KGaA, Jotun A/S, KCC Corporation, H.B. Fuller Company, B.L. Downey Company LLC, Tatung Fine Chemicals Co., Ltd., Dymax Corporation, Modine Manufacturing Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

E-Coat Market Segmentation

By Type

- Cathodic Electrocoating

- Anodic Electrocoating

By Resin Type

- Epoxy

- Acrylic

- Polyurethane

- Hybrid

- Others

By Technology

- Water-borne

- Solvent-borne

By Application

- Automotive

- Industrial Equipment

- Consumer Goods and Appliances

- Building and Architecture

- Aerospace and Defense

- Marine

By Substrate

- Steel

- Aluminum

- Copper

- Magnesium and Other Alloys

By Functional Requirement

- Corrosion Protection

- Decorative

- High-Throw Power

- Dielectric

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in E-Coat Market

- PPG Industries, Inc.

- BASF SE

- Axalta Coating Systems Ltd.

- The Sherwin-Williams Company

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Henkel AG & Co. KGaA

- Jotun A/S

- KCC Corporation

- H.B. Fuller Company

- B.L. Downey Company LLC

- Tatung Fine Chemicals Co., Ltd.

- Dymax Corporation

- Modine Manufacturing Company

*- List not Exhaustive