Elastomeric Coatings Market Scaling at 16.4% CAGR Driven by Cool Roof Adoption and Sustainable Building Envelope Innovations

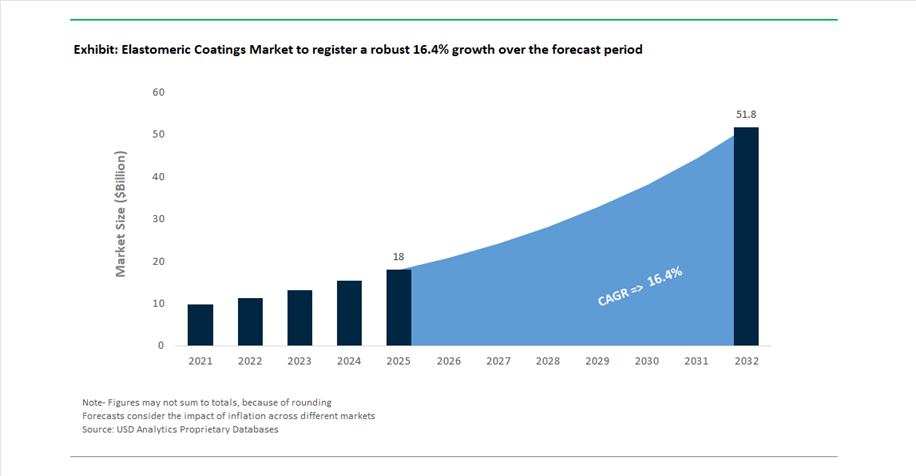

The global Elastomeric Coatings Market reached a valuation of USD 18 billion in 2025 and is projected to expand at a CAGR of 16.4% through 2032, ultimately reaching USD 52.1 billion by 2032. This accelerated growth trajectory positions elastomeric coatings among the fastest-growing segments within the broader architectural and industrial coatings industry. The market is being fundamentally driven by the rising demand for high-performance, flexible, and weather-resistant coatings used across roofing systems, exterior walls, and infrastructure assets.

Elastomeric coatings are increasingly recognized for their crack-bridging capabilities, UV resistance, waterproofing performance, and energy efficiency benefits, making them critical components in modern building envelope design. A major growth catalyst is the global push toward energy-efficient construction and climate-resilient infrastructure, particularly in regions experiencing extreme weather variability and urban heat island effects. Reflective elastomeric roof coatings, often categorized under “cool roof” technologies, are gaining traction due to their ability to reduce building cooling loads by up to 20%, aligning with green building certifications such as LEED.

From a materials innovation standpoint, the market is shifting toward bio-based binders, low-VOC formulations, and high-durability polymer systems such as polyurea and advanced acrylics. These innovations are enabling longer lifecycle performance, reduced maintenance costs, and compliance with tightening environmental regulations across Europe and North America. Additionally, the integration of elastomeric coatings with insulation systems and full building envelope solutions is redefining value propositions, particularly in commercial and industrial construction.

M&A Consolidation, Bio-Based Binder Innovation, and Cool Roof Demand Accelerate Elastomeric Coatings Market Transformation

The elastomeric coatings market is undergoing rapid transformation, shaped by strategic acquisitions, sustainability-driven product innovation, and expanding production capacities. In April 2026, RPM International completed the acquisition of Kalzip GmbH, significantly strengthening its Tremco Construction Products Group portfolio in Europe. This move integrates Kalzip’s advanced aluminum-based roofing systems with elastomeric liquid-applied membranes, enabling the delivery of comprehensive, high-performance building envelope solutions.

A defining industry event occurred in November 2025, when AkzoNobel and Axalta Coating Systems announced a $25 billion merger of equals. This consolidation is expected to create a dominant force in architectural and industrial elastomeric coatings, combining decorative elastic wall coatings with high-performance industrial polymers. The merged entity is anticipated to accelerate R&D efforts in next-generation flexible coatings, particularly those addressing durability, sustainability, and multifunctionality.

Sustainability and material innovation remain central to competitive differentiation. In October 2025, BASF introduced its AQAcell and Acronal bio-balanced binders, leveraging renewable feedstocks to replace fossil-based inputs. These binders are engineered for elastomeric coatings requiring high dirt-pickup resistance and superior crack-bridging performance, while complying with stringent European VOC regulations. Similarly, Dow launched ENDURANCE™ elastomeric insulation technology in March 2026, with material innovations adaptable to harsh industrial coating environments, including oil and gas infrastructure.

Capacity expansion and regional growth strategies are also evident. In August 2025, PPG Industries expanded production of reflective elastomeric roof coatings in Mexico, targeting the rising demand for cool roof solutions across North America and Latin America. Meanwhile, Huntsman Corporation increased its polyurea elastomeric production capacity in September 2025, focusing on high-growth infrastructure markets in Asia-Pacific and the Middle East.

Strategic ecosystem expansion is further illustrated by Carlisle Companies, which acquired Bonded Logic in June 2025 to strengthen its integrated building envelope offerings. Complementing this, Tremco CPG established a new distribution center in the UK in February 2025, improving supply chain responsiveness for elastomeric membranes and sealants. Additionally, Henry Company received the RCMA Project of the Year award in October 2025, highlighting the growing adoption of liquid-applied roof restoration (LAR) systems over traditional replacement methods.

US GSA Buy Clean Policy Accelerating Low-Carbon Elastomeric Coatings Adoption in Federal Infrastructure

The elastomeric coatings industry in 2026 is undergoing a measurable transition toward low-carbon material innovation, driven by the operationalization of the U.S. General Services Administration Buy Clean Initiative across federal procurement frameworks. This policy is reshaping demand dynamics for high-performance exterior elastomeric coatings by prioritizing products with significantly reduced embodied carbon relative to established industry baselines. A central compliance requirement is the mandatory submission of product-specific Environmental Product Declarations, which quantify lifecycle carbon emissions from raw material extraction through manufacturing processes. Coatings specified for federal infrastructure projects must now meet stringent Global Warming Potential benchmarks, falling within the top 20% to 40% of low-emission products, effectively excluding legacy solvent-heavy and energy-intensive formulations from competitive bids. This shift is directly aligned with national decarbonization targets aimed at achieving a 50% to 52% reduction in greenhouse gas emissions by 2030, placing pressure on manufacturers to reformulate products using low-VOC chemistries, optimized supply chains, and renewable raw materials. The policy impact is expanding beyond federal procurement, with states such as California, Colorado, and Washington adopting parallel standards in 2026, creating a harmonized domestic market environment where low-carbon elastomeric coatings are becoming a prerequisite for participation in large-scale public infrastructure projects.

China GB/T 41649-2024 Raising Weathering Durability and Crack-Bridging Performance Standards

China’s GB/T 41649-2024 standard is establishing a new performance baseline for high-performance exterior elastomeric coatings, particularly in densely urbanized environments across the Asia-Pacific region. The updated regulation significantly increases the technical requirements for weathering resistance, elongation, and pollution durability, reinforcing the shift toward long-life, infrastructure-grade coating systems. Under the revised standard, elastomeric coatings must withstand a minimum of 3,500 hours of xenon arc weathering without exhibiting visible degradation such as chalking, cracking, or blistering, representing a substantial increase from the previous 2,000-hour threshold. Mechanical performance requirements have also intensified, with coatings required to demonstrate tensile elongation of 200% to 300% at ambient conditions and at least 100% elongation at sub-zero temperatures of minus 10 degrees Celsius, ensuring structural flexibility across diverse climatic zones. In addition, the introduction of stricter dirt-pickup resistance metrics requires coatings to maintain gloss retention and color stability levels above 90% following standardized pollution exposure testing. Compliance has rapidly become a key differentiator in the Chinese market, with more than 65% of municipal construction projects in Tier 1 cities mandating adherence to GB/T 41649-2024 standards by 2026. This regulatory escalation is pushing manufacturers to develop advanced polymer systems and high-durability elastomeric formulations capable of meeting extended lifecycle performance expectations.

Cool Wall Elastomeric Coatings Enabling Urban Heat Island Mitigation and Energy Efficiency Gains

The increasing intensity of urban heat islands is creating a significant growth opportunity for cool wall elastomeric coatings designed to reflect solar radiation and reduce building envelope temperatures. These high-performance coatings incorporate infrared-reflective pigments that enable substantial reductions in surface temperatures, with high Solar Reflectance Index systems capable of lowering facade temperatures by up to 20 degrees Celsius compared to conventional dark coatings. This temperature reduction directly translates into improved building energy efficiency, particularly in high-temperature climate zones, where studies indicate cooling energy savings ranging from 10% to 40% on an annual basis. The economic viability of these systems is supported by relatively short payback periods of three to five years under 2026 energy cost conditions. At a macro level, widespread adoption of cool wall technologies across urban environments has the potential to reduce ambient city temperatures by up to 2 degrees Celsius, contributing to reduced heat stress and lower incidences of heat-related health risks during peak summer conditions. Regulatory frameworks such as LEED and WELL certifications are further reinforcing demand, with manufacturers targeting Solar Reflectance Index values above 64 for vertical applications to maximize eligibility for heat island reduction credits. This convergence of regulatory incentives, energy efficiency benefits, and climate resilience positioning is accelerating the adoption of cool wall elastomeric coatings across both public and private sector infrastructure projects.

Photocatalytic Self-Cleaning Elastomeric Coatings Transforming Urban Air Quality and Maintenance Economics

The integration of photocatalytic functionality into elastomeric coatings represents a high-value innovation pathway, particularly for urban infrastructure exposed to high levels of air pollution and environmental degradation. Titanium dioxide-based photocatalytic coatings are engineered to utilize ultraviolet radiation to initiate chemical reactions that decompose organic pollutants, nitrogen oxides, and airborne contaminants on contact. In 2026, advanced formulations are achieving nitrogen oxide reduction efficiencies of up to 45% in localized environments surrounding coated surfaces, effectively positioning these coatings as passive air purification systems within dense urban settings. The self-cleaning properties of these coatings also deliver measurable economic benefits by significantly reducing maintenance requirements, with cleaning frequency lowered by 50% to 70% due to the continuous breakdown of organic grime, algae, and fungal growth. Performance validation indicates that photocatalytic elastomeric coatings can decompose up to 99.9% of surface-borne volatile organic compounds and allergens when exposed to natural sunlight, maintaining long-term aesthetic and functional performance of coated surfaces. Market adoption is accelerating across key regions including China, Japan, and the European Union, where municipal infrastructure tenders increasingly specify photocatalytic additives for applications such as road tunnels, transit systems, and high-rise exteriors to address localized air quality challenges. This technology is redefining elastomeric coatings as active environmental solutions rather than passive protective layers, expanding their role within smart and sustainable urban infrastructure systems.

Roof Coatings Dominate Elastomeric Coatings Market with 44% Share Driven by Cost-Effective Roof Restoration Solutions

Application Analysis: Liquid-Applied Elastomeric Roof Coatings Lead with High ROI and Energy Efficiency Benefits

Roof coatings account for a dominant 44.0% share of the elastomeric coatings market in 2025, driven by their unmatched ability to provide cost-effective roof restoration and long-term waterproofing. These coatings—primarily acrylic, silicone, and polyurethane elastomeric systems—offer a compelling alternative to full roof replacement, reducing costs from $8–$15 per sq. ft. to $2–$4 per sq. ft. while extending roof life by 10–20 years. A key growth driver is their integration with cool roof technologies, where white elastomeric coatings achieve high solar reflectance (TSR 0.85–0.90) and reduce roof temperatures by 40–70°F, lowering cooling energy consumption by 10–30%. Additionally, compliance with Title 24, ASHRAE 90.1, and LEED standards, along with utility rebates, further accelerates adoption. The segment is also witnessing strong demand for silicone coatings, particularly for flat roofs with ponding water issues, reinforcing roof coatings as the leading segment in the global elastomeric coatings market.

Commercial Sector Leads Elastomeric Coatings Market with 42% Share Driven by Large Roof Footprints and ESG Compliance

End-Use Industry Analysis: Commercial Buildings Drive High-Volume Demand for Roof and Wall Coatings

The commercial sector holds a leading 42.0% share of the elastomeric coatings market in 2025, driven by the extensive use of low-slope roofing systems and large surface-area structures such as warehouses, retail complexes, office buildings, and multi-family housing. These buildings have high roof-to-volume ratios, making roof performance critical for both energy efficiency and waterproofing. Elastomeric coatings provide a seamless, flexible barrier that reduces maintenance costs while supporting corporate ESG and carbon reduction initiatives by lowering HVAC energy consumption. In addition to roofing, the segment benefits from widespread adoption of elastomeric wall coatings (EWC) applied to concrete, stucco, and EIFS surfaces, offering crack-bridging, moisture resistance, and long-term durability. The combination of energy savings, asset protection, and sustainability compliance positions the commercial sector as the primary growth driver in the global elastomeric coatings market.

Elastomeric Coatings Market Competitive Landscape Driven by Sustainable Innovation and Building Envelope Technologies

The global elastomeric coatings market is highly competitive, defined by sustainability-driven innovation, advanced polymer chemistry, and integrated building envelope solutions. Key players are scaling high-performance acrylic, silicone, and waterborne technologies while optimizing global supply chains and targeting energy-efficient, low-VOC coating systems.

Sherwin-Williams accelerates CUI-resistant elastomeric innovation through Heat-Flex expansion

Sherwin-Williams Company maintains a dominant position in the elastomeric coatings market through aggressive R&D cycles and a robust global distribution network. The company is advancing high-solids and waterborne elastomeric coating technologies that significantly reduce VOC emissions while maintaining superior film thickness and elasticity. Its 2025 expansion of the Heat-Flex® series, including Heat-Flex AEB, directly addresses corrosion under insulation (CUI), a critical challenge in industrial coatings. Flagship offerings such as Loxon® and ConFlex™ deliver up to 300% elongation, reinforcing their leadership in crack-bridging masonry coatings and concrete protection systems. The March 2025 global standardization initiative enhances product consistency for multinational clients, strengthening its industrial coatings footprint. Recognition through the 2025 MP Corrosion Innovation of the Year Award further validates its leadership in high-performance elastomeric barrier coatings.

PPG drives sustainable elastomeric coatings growth through advanced manufacturing investments

PPG Industries, Inc. is reinforcing its competitive position through large-scale investments in advanced manufacturing and supply chain resilience. The company’s $300 million investment through 2026, including a major Tennessee facility, supports capacity expansion in high-performance coatings. Sustainability remains central, with 41% of 2024 sales derived from sustainably advantaged products, including EnviroLuxe Plus coatings incorporating recycled plastics. PPG’s portfolio optimization strategy targets high-growth elastomeric coatings segments, supported by mid-single-digit revenue growth projections and strong aerospace coatings demand. Its R&D investment of $574 million focuses on low-temperature curing technologies that reduce energy consumption in industrial applications. This combination of sustainable coatings innovation and operational efficiency positions PPG as a key growth driver in the global elastomeric coatings industry.

AkzoNobel advances Eco+ elastomeric coatings portfolio aligned with carbon reduction goals

AkzoNobel N.V. is positioning itself as a sustainability leader in the elastomeric coatings market through its Eco+ product framework and aggressive carbon reduction strategy. Achieving a 47% reduction in Scope 1 and 2 emissions versus its 2018 baseline, the company is aligning its operations with global environmental mandates. The 2026 launch of the Eco+ portfolio highlights coatings with reduced curing temperatures and minimized waste, strengthening its sustainable coatings offering. Key brands such as Interpon and Resicoat are being integrated into this platform, enhancing durability for architectural and automotive elastomeric applications. Operating across more than 150 countries, AkzoNobel leverages value-driven sustainability to support regulatory compliance for industrial clients. The proposed Axalta merger further signals a strategic consolidation aimed at scaling global market share.

RPM leverages decentralized innovation to scale elastomeric roofing and building envelope systems

RPM International Inc. differentiates itself through a decentralized operating model that empowers brands like Tremco and Rust-Oleum to innovate within niche elastomeric coatings applications. The company’s $100 million annual cost optimization program is designed to improve margins while reallocating capital toward high-growth segments. Expansion into Asia-Pacific is supported by a new manufacturing facility in Malaysia, targeting rising demand for performance coatings. RPM’s Construction Products Group, generating approximately $737 million in Q2 2026, leads in seamless elastomeric roofing membranes and airtight building envelope transitions. Strong financial performance, including $583.2 million in operating cash flow in H1 2026, provides liquidity for its MAP 2025 initiatives. This strategy reinforces RPM’s leadership in construction-focused elastomeric coatings systems.

Henry strengthens building envelope leadership with system-centric elastomeric solutions

Henry Company, under Carlisle Companies, is central to advancing integrated building envelope systems in the elastomeric coatings market. Its Blueskin® VPTech™ solution, recognized as 2025 Sustainable Product of the Year, highlights innovation in air and vapor barrier technologies. The company is transitioning toward system-centric solutions, supported by its 2026 Waterproofing Training programs focusing on PUMA liquid-applied systems for high-moisture environments. Strategic integration of UltraTouch™ recycled denim insulation enhances sustainability while improving thermal and moisture management performance. Henry’s recognition through the 2025 RCMA Project of the Year underscores the growing shift toward elastomeric roof restoration over replacement. This integrated approach positions Henry as a leader in high-performance building envelope coatings.

BASF drives elastomeric coatings innovation through advanced materials and phygital surface technologies

BASF SE continues to lead in material science innovation, shaping next-generation elastomeric coatings through advanced pigment and resin technologies. Its 2025-2026 “Driving the Proxy” collection introduces high-performance pigments such as Tesseract Blue, utilizing interference technology for multidimensional coating effects. BASF is advancing “phygital” coatings that integrate physical durability with digital-responsive aesthetics, particularly in automotive and industrial applications. Sustainability is embedded through the use of renewable and recycled raw materials in elastomeric formulations. The company’s Verbund integration model ensures raw material security and cost efficiency amid volatile petrochemical markets. This deep vertical integration and innovation capability position BASF at the forefront of high-performance elastomeric coatings development.

United States Elastomeric Coatings Market: Smart Reflectivity and Climate-Responsive Systems Driving Innovation

The United States is leading the global shift toward high-performance elastomeric coatings, driven by strict energy codes and urban heat mitigation strategies. A major breakthrough is the commercialization of Temperature-Adaptive Radiative Coatings (TARC), which dynamically switch between cooling and heat-retention modes based on ambient conditions.

Policy support is accelerating adoption. Under the Inflation Reduction Act, tax credits are tied to high Solar Reflectance Index (SRI >100) coatings, pushing widespread use of reflective elastomeric systems. Technological innovation is also strong, with silicone-alkyd hybrid coatings offering superior ponding water resistance and adhesion. Additionally, new VOC regulations (EPA/CARB, 2026) are driving a transition toward 100% solids polyurethane elastomers, while demand for fire-retardant elastomeric coatings in EV charging infrastructure is emerging as a new application segment.

China Elastomeric Coatings Market: Green Building Mandates and Mega-Project Applications Driving Scale

China’s elastomeric coatings market is expanding rapidly under the 15th Five-Year Plan, which mandates the use of green building materials across infrastructure and industrial projects. Government policies now require 100% waterborne elastomeric membranes for roofing in public industrial parks.

Innovation is focused on performance and sustainability. The large-scale adoption of zirconia-doped cool roof coatings is reducing rooftop temperatures by up to 25°C, while graphene-enhanced elastomeric coatings provide crack-bridging capabilities of up to 2 mm. Major infrastructure projects—such as high-speed rail networks—are driving demand for anti-carbonation coatings to prevent rebar corrosion. Additionally, urban renewal programs are utilizing elastomeric textures to restore aging buildings, while photocatalytic TiO₂ additives are enabling self-cleaning surfaces in polluted environments.

Germany Elastomeric Coatings Market: Renovation Wave and Biocide-Free Chemistry Driving Sustainability

Germany is at the forefront of sustainable elastomeric coatings, driven by strict environmental regulations and energy efficiency mandates. Government funding under the KfW/BEG programs is promoting elastomeric facade systems integrated with insulation technologies to achieve climate-neutral buildings by 2045.

A key innovation is the shift toward biocide-free elastomeric coatings, using mineral stabilization to meet stringent EU regulations. The commercialization of silane-terminated polyether (MS polymer) coatings is enhancing breathability and UV stability, particularly in historic buildings. Additionally, Germany is advancing circular economy practices through recycled-polymer-based elastomeric membranes, while RFID-enabled tracking systems are improving lifecycle monitoring in large infrastructure projects.

India Elastomeric Coatings Market: Infrastructure Supercycle and Waterproofing Evolution Driving Growth

India is experiencing rapid growth in elastomeric coatings, transitioning from traditional paints to engineered waterproofing systems. The Gati Shakti master plan is driving adoption of polyurea-elastomer hybrids in bridges, metro tunnels, and airports, targeting 50-year service life.

Sustainability and urbanization are key drivers. The expansion of IGBC-certified green buildings (+40% YoY) is increasing demand for low-VOC, reflective elastomeric coatings. Coastal regions are seeing strong uptake of anti-fungal elastomeric systems to combat humidity, while the Smart Cities Mission is deploying cool-roof coatings across 100 cities. Additionally, manufacturing expansion by companies like Saint-Gobain and UltraTech is enabling production of high-elongation coatings (up to 600%), supporting durability in diverse climatic conditions.

Japan Elastomeric Coatings Market: Seismic Resilience and Advanced Silicone Technologies Driving Precision

Japan’s elastomeric coatings market is defined by seismic resilience and long-term durability. Innovations include ultra-high elongation coatings (>800%), designed to maintain waterproofing integrity during seismic activity.

Material science advancements are also significant. High-solids silicone elastomers developed by Japanese manufacturers offer 20+ years of color stability and resistance to chalking. Emerging applications include offshore wind turbine protection and conductive elastomeric coatings for smart buildings, enabling real-time monitoring of structural stress. Additionally, automation trends—such as drone-applied coatings for high-rise maintenance—are improving efficiency and safety in dense urban environments.

UAE Elastomeric Coatings Market: Extreme Climate Engineering and Smart Urban Design Driving Demand

The UAE is a global testbed for extreme-performance elastomeric coatings, designed for high temperatures and intense UV exposure. Innovations such as hollow glass bubble-infused coatings can reflect over 90% of solar radiation, making them critical for large industrial and logistics facilities.

Government initiatives under the Dubai 2040 Urban Master Plan mandate cool-roof solutions for commercial buildings, accelerating adoption. Additionally, specialized sand-resistant elastomeric coatings are being developed to maintain reflectivity in desert conditions. Applications are expanding into water infrastructure, with elastomeric liners used in desalination plants and storage tanks to prevent evaporation and chemical degradation. High-end real estate projects are also driving demand for premium “cool facade” coatings, balancing thermal performance with aesthetics.

Elastomeric Coatings Market Report Scope

Elastomeric Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18 Billion

|

|

Market Size (2032)

|

$52.1 Billion

|

|

Market Growth Rate

|

16.4%

|

|

Segments

|

By Resin Type (Acrylic, Silicone, Polyurethane, Butyl, Polyurea, Others), By Technology (Water-borne, Solvent-borne, Others), By Application (Roof Coatings, Wall Coatings, Floor, Bridge and Infrastructure Coatings), By Function (Waterproofing and Moisture Barrier, Thermal Insulation, Corrosion Protection, Chemical Protection, Crack Bridging and Structural Reinforcement), By End-Use Industry (Residential, Commercial, Industrial, Infrastructure), By Substrate (Concrete and Masonry, Metal, Wood, Stucco, Plastic and Composites)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., BASF SE, Dow Inc., Nippon Paint Holdings Co., Ltd., Sika AG, RPM International Inc., Jotun A/S, Kansai Paint Co., Ltd., Asian Paints Limited, Hempel A/S, Henry Company, 3M Company, Holcim Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Elastomeric Coatings Market Segmentation

By Resin Type

- Acrylic

- Silicone

- Polyurethane

- Butyl

- Polyurea

- Others

By Technology

- Water-borne

- Solvent-borne

- Others

By Application

- Roof Coatings

- Wall Coatings

- Floor

- Bridge and Infrastructure Coatings

By Function

- Waterproofing and Moisture Barrier

- Thermal Insulation

- Corrosion Protection

- Chemical Protection

- Crack Bridging and Structural Reinforcement

By End-Use Industry

- Residential

- Commercial

- Industrial

- Infrastructure

By Substrate

- Concrete and Masonry

- Metal

- Wood

- Stucco

- Plastic and Composites

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Elastomeric Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- BASF SE

- Dow Inc.

- Nippon Paint Holdings Co., Ltd.

- Sika AG

- RPM International Inc.

- Jotun A/S

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- Hempel A/S

- Henry Company

- 3M Company

- Holcim Ltd.

*- List not Exhaustive