Electron Beam Curable Coating Market Growth Supported by Solvent-Free Processing and Sustainable Industrial Coating Demand

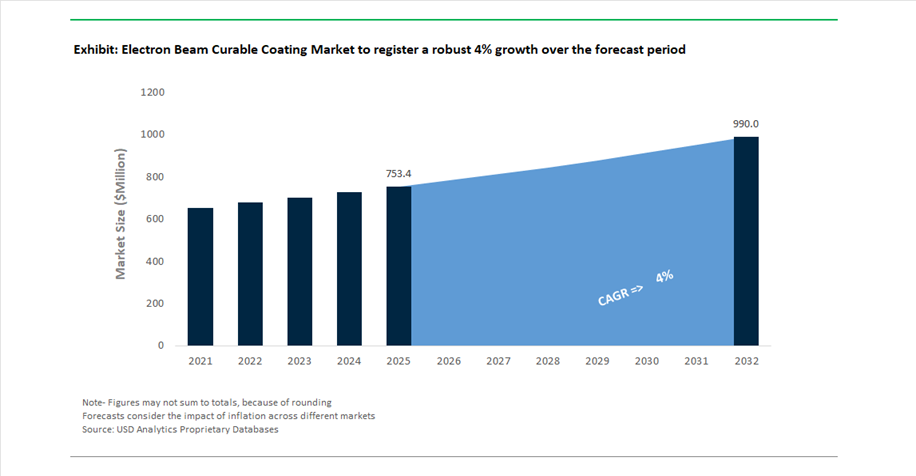

The global Electron Beam Curable Coating Market was valued at USD 753.4 million in 2025 and is projected to reach USD 991.4 million by 2032, expanding at a CAGR of 4% over the forecast period. This growth reflects the increasing adoption of energy-curable coating technologies, particularly in applications where low environmental impact, high-speed processing, and superior performance characteristics are critical. Electron Beam (EB) curing is gaining traction as a highly efficient alternative to conventional thermal and UV curing methods due to its ability to initiate polymerization without photoinitiators or heat, enabling solvent-free and low-VOC coating processes.

A primary growth driver is the rising demand for sustainable coating solutions across packaging, construction materials, electronics, and automotive sectors. EB-curable coatings are particularly advantageous in flexible packaging and labeling, where they support the development of recyclable monomaterial structures by eliminating thermal distortion risks. Additionally, EB technology allows for instant curing at ambient temperatures, significantly improving production throughput while reducing energy consumption, aligning with global decarbonization targets.

From a materials science perspective, EB coatings are evolving toward high-performance polyurethane acrylates, biomass-balanced resins, and high-solid formulations, which deliver enhanced chemical resistance, abrasion resistance, and adhesion properties. These innovations are enabling broader adoption in metal coil coatings, wood finishes, and advanced electronics manufacturing, where precision and durability are paramount.

EB Coil Coating Platforms, Circular Packaging Innovation, and Supply Chain Integration Driving Market Transformation

The Electron Beam curable coating market is undergoing structural transformation driven by technology innovation, sustainability mandates, and strategic supply chain investments. In July 2024, PPG Industries launched its DuraNEXT™ EB coil coating platform, specifically engineered for high-speed metal coil lines. This system eliminates the need for substrate heating, significantly reducing carbon emissions while maintaining high-performance coating characteristics. The platform’s recognition with the 2024 METALCON Top Products Award underscores the growing industry validation of EB-based solutions in construction materials.

Sustainability-driven innovation is particularly evident in the packaging sector. In July 2025, Sun Chemical expanded its EB curing portfolio to support compliance with the EU’s Packaging and Packaging Waste Regulation (PPWR). These EB systems enable the production of heat-resistant, recyclable monomaterial laminates, addressing one of the most pressing challenges in flexible packaging. Complementing this, the establishment of China’s first CI-FLEXO EB coating test center in Qingdao in November 2025, led by Xi’an Aerospace Huayang in collaboration with Energy Sciences Inc., represents a major step toward scaling solvent-free coating technologies in the Asia-Pacific region.

Strategic investments in materials and supply chains are also reshaping the competitive landscape. In February 2024, Arkema expanded its R&D and production footprint in India, focusing on low-VOC and EB-compatible resin systems to support regional demand in automotive and electronics coatings. Similarly, Covestro strengthened its supply chain for aliphatic isocyanates through acquisitions in August 2025 and H1 2026, ensuring stable availability of key raw materials used in polyurethane acrylates for EB coatings.

Regional adoption milestones further highlight the market’s expansion. In June 2024, Taiwan saw the signing of its first EB flexo printing and coating line agreement between Ruey Chang, Comexi, and Energy Sciences Inc., signaling a shift away from solvent-based curing in high-tech packaging industries. Additionally, BASF scaled its biomass-balanced EB binder portfolio in May 2025, contributing to significant CO₂ reduction targets and enabling formulators to adopt renewable feedstocks.

Competitive dynamics are intensifying with adjacent technology advancements. In June 2025, IST Metz introduced FREEcure and SMARTcure systems, leveraging AI-driven power modulation to compete with EB technology in penetration depth and surface finishing capabilities. This reflects a broader trend toward “lamp-free” and energy-efficient curing solutions, increasing innovation pressure within the EB coatings segment.

EU REACH 2024/3190 BPA Ban Accelerating Shift to BPA-Free EB-Curable Food Packaging Coatings

The implementation of Regulation (EU) 2024/3190 is acting as a structural catalyst for reformulation across the electron beam curable coatings industry, particularly within food-contact packaging applications. The regulation mandates a complete ban on Bisphenol A in all food-contact materials by July 20, 2026, directly impacting EB-curable systems that historically relied on BPA-derived epoxy acrylates for mechanical strength and chemical resistance. This regulatory shift is forcing a rapid transition toward BPA-intent-free polyester acrylates and urethane acrylates, which must deliver comparable performance while meeting stringent migration safety standards. The regulation also enforces near-zero migration thresholds, effectively setting the specific migration limit at the limit of detection for BPA residues, including contamination from recycled feedstock streams. EB-curable coatings hold a strategic advantage under this framework due to their photoinitiator-free curing mechanism, eliminating one of the primary sources of migratory contaminants found in UV-cured systems. As a result, the industry is witnessing accelerated adoption, with approximately 85% of Tier 1 packaging converters in the European Union transitioning to EB-curable technologies for high-speed flexible packaging lines by 2026. This shift is reinforcing EB curing as a compliance-driven technology, reshaping formulation strategies and strengthening its position in food-safe, low-migration coating applications.

FDA Food Contact Substance Reassessments Elevating EB-Curable Coatings for Low-Migration Performance

The U.S. Food and Drug Administration’s revised Food Contact Substance reassessment framework is significantly increasing scrutiny on migration behavior in energy-cured coatings, creating a favorable regulatory environment for EB-curable technologies. The updated approach emphasizes the degree of cure as a critical determinant of safety, particularly for coatings used in indirect food contact applications. EB-curable systems demonstrate a consistently high cross-linking density exceeding 95%, even in opaque or highly pigmented films, overcoming limitations associated with UV-curing technologies such as incomplete surface cure due to shadowing effects. The FDA’s 2026 guidelines also introduce cumulative exposure assessments, requiring manufacturers to evaluate the combined dietary impact of chemically related substances, which is driving the adoption of high-molecular-weight oligomer systems with reduced bioavailability. For functional barrier coatings, the FDA is applying a stringent migration threshold of 10 parts per billion, with EB-curable coatings demonstrating migration levels approximately 40% below this limit in field conditions. In response to increased enforcement actions and compliance risks, major consumer packaged goods companies in the United States have expanded their specification of EB-cured overprint varnishes by roughly 30% between 2025 and 2026. This regulatory alignment is reinforcing EB curing as a preferred technology for high-performance, low-migration packaging coatings in global food safety applications.

Low-Dose EB Curing Below 30 kGy Enabling High-Speed Thin Film Packaging Production

The transition toward lightweight, mono-material flexible packaging is creating a substantial opportunity for low-energy electron beam curing technologies optimized for ultra-thin substrates. By reducing the electron beam dosage to below 30 kGy, manufacturers can achieve full polymerization without inducing thermal deformation or shrinkage in thin polymer films, particularly those with thicknesses around 12 microns. Advanced low-dose EB systems introduced in 2026 operate with a temperature rise below 5 degrees Celsius, preserving substrate integrity and maintaining optical clarity, which is critical for high-performance packaging applications. From an operational perspective, reducing the curing dose from traditional 50 kGy levels to approximately 25 kGy delivers a 40% reduction in energy consumption, significantly lowering the carbon footprint per unit of coated material. Production efficiency is also enhanced, with low-dose EB formulations achieving full cure at line speeds exceeding 400 meters per minute, supporting the throughput requirements of large-scale flexible packaging converters. Additionally, lower energy operation reduces ozone generation by approximately 25%, minimizing the need for extensive ventilation and nitrogen inerting systems, thereby reducing both capital and operating expenditures. These advantages position low-dose EB curing as a key enabler of sustainable, high-efficiency packaging production in the evolving materials landscape.

EB-Curable Silicone Release Coatings Scaling for EV Battery Separator Manufacturing

The rapid expansion of electric vehicle battery production is unlocking a high-growth application segment for EB-curable silicone release coatings, particularly in separator film manufacturing for lithium-ion and next-generation solid-state batteries. These coatings are critical for enabling precise release characteristics during high-speed electrode stacking processes, ensuring consistent assembly of delicate battery membranes. Industry collaborations in early 2026 are scaling EB-curable coating capacities to approximately 1.2 billion square meters annually, sufficient to support production volumes for around 1.7 million electric vehicles. EB-curable silicone systems offer a significant environmental and operational advantage due to their 100% solids formulation, eliminating volatile organic compound emissions and removing the need for costly regenerative thermal oxidizers required in solvent-based coating processes. The low-temperature nature of EB curing ensures dimensional stability of polyolefin separator films, preventing deformation and preserving the micro-porous structure essential for efficient lithium-ion transport. Additionally, EB technology enables the application of ultra-thin release layers below 1 micron, contributing to a reduction of approximately 5% in overall separator thickness. This reduction directly enhances battery energy density, supporting longer driving ranges and improved performance in electric vehicles. These performance and sustainability advantages are positioning EB-curable silicone coatings as a critical component in next-generation battery manufacturing ecosystems.

Roll Coating Dominates EB Curable Coatings Market with 58% Share Driven by High-Speed Industrial Processing

Application Method Analysis: Roll-to-Roll EB Coating Enables Ultra-Fast, High-Volume Production

Roll coating leads the electron beam (EB) curable coatings market with a 58.0% share in 2025, driven by its unmatched compatibility with high-speed, continuous web processing systems. This method is widely used across flexible packaging, graphic arts, and wood finishing applications, where production lines operate at speeds of 300–1,000+ feet per minute. EB curing provides instantaneous polymerization, transforming liquid coatings into fully cured films within milliseconds, eliminating drying time and increasing throughput efficiency. A key advantage is the ability to operate in nitrogen-inert environments, ensuring complete cure while preventing oxygen inhibition. Additionally, EB coatings are photoinitiator-free, resulting in ultra-low migration and extractables, making them ideal for food-grade packaging and pharmaceutical applications. These benefits position roll coating as the preferred technology for high-performance, sustainable EB coating solutions.

High-Barrier Coatings Lead EB Market with 36% Share Driven by Food Packaging and Sustainability Trends

Functional Characteristic Analysis: EB High-Barrier Coatings Enable Shelf-Life Extension and Recyclable Packaging

High-barrier coatings account for a leading 36.0% share of the EB curable coatings market in 2025, driven by increasing demand for advanced food packaging solutions and sustainable materials. EB-cured coatings form highly cross-linked, dense polymer networks, significantly improving resistance to oxygen, moisture vapor, grease, and aroma loss, which is critical for extending product shelf life. A major growth driver is the transition toward mono-material recyclable packaging, replacing traditional multi-layer laminates (e.g., PET/foil/PE) that are difficult to recycle. EB coatings enable single-layer films to achieve comparable barrier performance, aligning with global sustainability initiatives such as the Ellen MacArthur Foundation’s circular economy goals and emerging EPR regulations. Additionally, their low migration properties make them suitable for sensitive applications in food and pharmaceutical packaging, reinforcing their dominance in the EB curable coatings market.

Electron Beam Curable Coatings Market Competitive Landscape Driven by Low-Energy Curing, High-Solids Resins, and Sustainable Industrial Finishing

The electron beam curable coatings market is rapidly evolving, driven by demand for solvent-free coatings, instant curing technologies, and energy-efficient industrial processes. Key players compete through EB-curable resins, advanced acrylates, and digital integration across packaging, automotive, electronics, and industrial wood applications.

Allnex Leads EB Resin Innovation with Photoinitiator-Free Systems and Bio-Based Focus

Allnex Holdings S.à r.l. is a global leader in radiation-curable coatings, highlighted by the launch of EBECRYL® 350 in 2026, enhancing slip, flow, and surface durability in EB systems. Its EBECRYL® LEO resins eliminate the need for photoinitiators, addressing migration concerns in food packaging coatings. The UCECOAT® 7690 platform delivers high outdoor durability and energy-efficient processing for industrial wood applications. Allnex offers a broad portfolio of urethane, polyester, and epoxy acrylates optimized for low-energy EB curing systems. The company is advancing bio-preferred and recycled-content resins to replace petroleum-based materials. Its innovation in self-curing resins positions it at the forefront of sustainable EB coatings.

PPG Expands EB-Coating Applications with Powder Systems and Digital Process Monitoring

PPG Industries, Inc. is advancing electron beam coatings through innovations in EB-curable powder coatings, enabling coating of heat-sensitive substrates such as plastics and engineered wood. Its ENVIROCRON® EB series supports single-pass industrial finishing, improving efficiency and reducing energy consumption. The company reported strong financial performance with Q1 2026 EPS of $1.83, driven by sustainably advantaged coatings. PPG is integrating EB curing into aerospace and automotive OEM applications for lightweight, high-performance components. Its LINQ™ platform enables real-time monitoring of curing density, ensuring optimal cross-linking and durability. PPG’s combination of digital tools and EB technology strengthens its competitive position.

AkzoNobel Drives Energy-Efficient EB Coatings with Laser Integration and EV Applications

AkzoNobel N.V. is accelerating the adoption of EB-curable coatings through its collaboration with IPG Photonics, targeting a 30% reduction in energy consumption by replacing traditional curing ovens. Its Resicoat EB-curable insulation coatings provide dielectric protection for EV motors and battery systems with rapid curing capabilities. The company maintains strong profitability with a 14.2% EBITDA margin, supported by its Industrial Excellence strategy. AkzoNobel is investing in bio-based radiation-curable materials to reduce lifecycle carbon emissions. Its expertise in architectural finishes is being extended to EB-assisted surface texturing for long-lasting coatings. The company’s focus on sustainability and innovation reinforces its leadership in EB coatings.

Arkema Strengthens EB Materials Leadership with Sartomer Oligomers and Circular Composites

Arkema, through its Sartomer® business, is a key supplier of EB-curable monomers and oligomers, supporting a significant share of the global market. The company introduced low-viscosity EB-curable acrylates for additive manufacturing, enabling production of high-performance industrial components. Its Elium® resin technology supports circular composite manufacturing, aligning with sustainability goals. Arkema’s EB materials are widely used in electronics, including scratch-resistant films for foldable displays. The company is advancing bio-based polymer solutions under its Rilsan® roadmap. Its innovation in specialty materials strengthens its leadership in EB-curable coatings and advanced manufacturing applications.

BASF Enhances EB Coatings with Advanced Pigments and Multi-Layer Automotive Systems

BASF SE is leveraging its expertise in polymer chemistry and pigments to develop advanced EB-curable coatings for automotive and electronics applications. Its DRIVING THE PROXY collection utilizes EB multi-layer systems to achieve unique metallic and textured finishes with zero solvent emissions. Innovations such as PHYGITAL MAGNETAR demonstrate the integration of EB technology with aesthetic design trends. BASF is expanding its Surface Technologies segment to target battery and electronics markets with EB-curable protective coatings. Its EB systems enable instant curing while maintaining complex surface textures. The company’s R&D capabilities position it as a leader in high-performance EB coatings.

Sherwin-Williams Expands EB Coatings in Packaging and Industrial Wood with High-Speed Finishing Solutions

The Sherwin-Williams Company is expanding its presence in EB-curable coatings by targeting food packaging and industrial wood applications with solvent-free systems. Its ValueV™ EB-curable lacquer series enables high-speed finishing lines, allowing immediate packaging without cooling delays. The company is aligning its coatings with stringent FDA and EU regulations on chemicals of concern. Sherwin-Williams leverages its strong logistics and OEM support to accelerate adoption of EB technology across North America. Its Performance Coatings Group continues to drive growth in high-speed industrial applications. The company’s focus on high-solids, sustainable coatings strengthens its competitive position in EB-curable systems.

China Electron Beam (EB) Curable Coatings Market: Semiconductor Scaling and Green Manufacturing Driving Dominance

China is rapidly scaling the EB-curable coatings market, positioning it as a core technology under the 15th Five-Year Plan (2026–2030) for industrial decarbonization. The country’s dominance in electronics is a major catalyst, accounting for 42% of global semiconductor equipment spending, which is driving strong demand for EB-cured conformal coatings in high-density circuit boards.

Policy support is accelerating adoption. The Green Manufacturing Support Project (2025) provides subsidies for replacing solvent-based thermal curing with high-speed EB-curing systems, while the Jiangsu EB-Tech Hub is dedicated to radiation-cured polymers, especially for lithium-ion battery separator coatings. Innovation is also expanding into food packaging, with low-migration EB inks exceeding EU safety standards, and automotive applications, where EB-curing reduces energy consumption by ~40% in headlight lens production.

United States EB Curable Coatings Market: Defense Applications and Smart Coatings Driving High-Value Growth

The United States market is focused on high-performance and defense-driven applications of EB-curable coatings. The Department of Defense is funding EB-curable aerospace primers that enable on-site repairs of composite airframes, eliminating the need for autoclaves.

Innovation is centered on smart functionality. The launch of nanotechnology-infused EB coatings (2026) enables self-healing surfaces for pipelines and industrial infrastructure. Trade policies are also shaping the market, with tariffs driving domestic production of EB-curable acrylates and epoxies. Additionally, federal support under the Clean Air Act is encouraging retrofitting of legacy coating plants with EB systems, while the EPA has designated EB curing as a Best Available Control Technology (BACT)—reducing VOC compliance burdens.

Germany EB Curable Coatings Market: Energiewende and Digital Twin Integration Driving Sustainability

Germany is a global leader in energy-efficient EB-curing technologies, driven by the Energiewende transition. Manufacturers have achieved up to 70% reduction in carbon emissions in wood-panel production by replacing thermal ovens with 100% solids EB-curing systems.

Precision engineering is a key differentiator. The integration of digital twin systems with optical emission spectroscopy ensures ±1% thickness uniformity during curing. Innovation is also focused on sustainability, with the development of biocide-free EB-curable resins for facade restoration and bio-based resins derived from agricultural waste. Additionally, EB coatings are gaining traction in hydrogen fuel cells, where they provide chemical resistance and enable high-speed manufacturing.

Japan EB Curable Coatings Market: High-Purity Materials and Electronics Miniaturization Driving Precision

Japan’s EB-curable coatings market is defined by material purity and precision engineering, particularly in electronics and medical devices. Japanese firms supply over 65% of global ultra-high-purity EB-curable monomers, critical for advanced semiconductor and sensor applications.

Innovation is driven by miniaturization. EB-cured dielectric coatings are being used in wearable medical sensors, where traditional thermal curing would damage sensitive components. Advanced automation using AI-driven robotic manipulators ensures defect-free coating on complex geometries, while new high-thermal-conductivity coatings are supporting next-generation data centers. Regulatory compliance with low-odor standards has also eliminated the need for photo-initiators in food-contact applications.

South Korea EB Curable Coatings Market: EV Battery Leadership and 5G Expansion Driving High-Tech Demand

South Korea is leveraging EB technology to strengthen its leadership in EV batteries and telecommunications. Under the Nationwide 5G Coverage Plan (2025), millions of RF components are being protected with EB-curable conformal coatings, ensuring moisture resistance and reliability.

The EV sector is a major driver. Investments in EB-curable dielectric coatings for battery enclosures allow precise thickness control (25–75 microns) without compromising heat dissipation. Innovations such as thermal cycling-resistant coatings (2025) are improving durability in microelectronics. Government incentives—including tax credits for radiation-curing technologies—are further accelerating adoption, while growth in medical devices is increasing demand for residue-free EB coatings.

India EB Curable Coatings Market: Localization and Infrastructure Expansion Driving Emerging Growth

India is transitioning into a regional hub for EB-curable coatings, supported by policy initiatives and infrastructure development. Under Atmanirbhar Bharat, local assembly of Low-Energy Electron Beam (LEEB) systems is being promoted, particularly for flexible packaging applications.

Infrastructure and industrial growth are key drivers. EB-cured coatings are being deployed in metro tunnel construction to ensure 60-year durability, while investments in waterborne EB-curable hybrids are supporting sustainable textile finishing. The establishment of a Coating Excellence Center in Bengaluru (2026) is strengthening technical capabilities, and local sourcing of zirconia-based feedstocks is improving supply chain resilience. Additionally, EB coatings are being applied in cold-storage logistics to prevent fungal growth and enhance insulation, expanding their use in agriculture and rural infrastructure.

Electron Beam Curable Coating Market Report Scope

Electron Beam Curable Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$753.4 Million

|

|

Market Size (2032)

|

$991.4 Million

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Raw Material (Oligomers, Monomers, Additives, Pigments), By Formulation (Liquid Coatings, Powder Coatings, Water-borne EB Coatings), By Application Method (Roll Coating, Spray Coating, Curtain Coating, Inkjet, Coil Coating), By Substrate (Paper and Film, Plastic and Polymers, Wood, Metal, Glass), By End-Use Industry (Packaging, Electrical and Electronics, Automotive, Building and Construction, Aerospace and Defense, Media and Graphic Arts), By Functional Characteristic (High Barrier, Scratch and Abrasion Resistance, Chemical and Corrosion Resistance, Low-Migration, Anti-reflective)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, PPG Industries, Inc., AkzoNobel N.V., Arkema S.A., Allnex GMBH, The Sherwin-Williams Company, Sun Chemical, Beckers Group, Covestro AG, Evonik Industries AG, Dymax Corporation, Toyo Ink SC Holdings Co., Ltd., Rahn AG, IGM Resins B.V., Dai Nippon Printing Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electron Beam Curable Coating Market Segmentation

By Raw Material

- Oligomers

- Monomers

- Additives

- Pigments

By Formulation

- Liquid Coatings

- Powder Coatings

- Water-borne EB Coatings

By Application Method

- Roll Coating

- Spray Coating

- Curtain Coating

- Inkjet

- Coil Coating

By Substrate

- Paper and Film

- Plastic and Polymers

- Wood

- Metal

- Glass

By End-Use Industry

- Packaging

- Electrical and Electronics

- Automotive

- Building and Construction

- Aerospace and Defense

- Media and Graphic Arts

By Functional Characteristic

- High Barrier

- Scratch and Abrasion Resistance

- Chemical and Corrosion Resistance

- Low-Migration

- Anti-reflective

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Electron Beam Curable Coating Market

- BASF SE

- PPG Industries, Inc.

- AkzoNobel N.V.

- Arkema S.A.

- Allnex GMBH

- The Sherwin-Williams Company

- Sun Chemical

- Beckers Group

- Covestro AG

- Evonik Industries AG

- Dymax Corporation

- Toyo Ink SC Holdings Co., Ltd.

- Rahn AG

- IGM Resins B.V.

- Dai Nippon Printing Co., Ltd.

*- List not Exhaustive