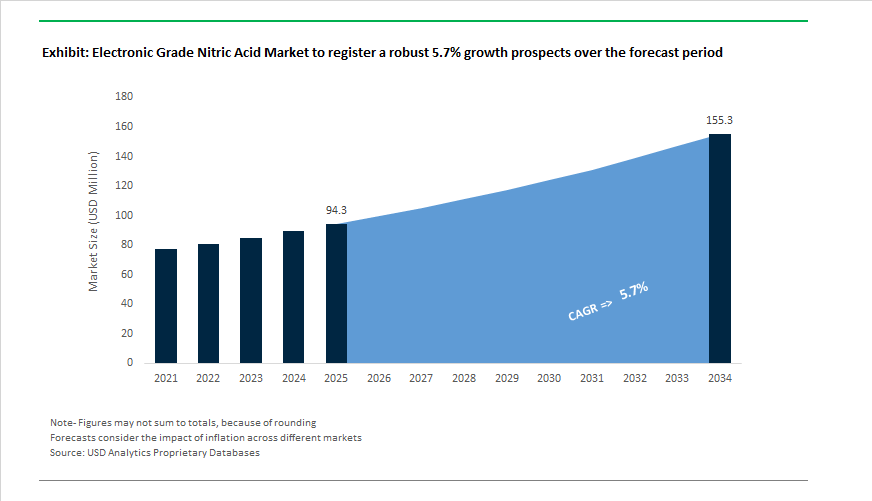

Electronic Grade Nitric Acid Market to Reach $155.3 Million by 2034 at 5.7% CAGR Amid Sub-7nm and 2nm Fabrication Expansion

The Electronic Grade Nitric Acid Market is projected to grow from $94.3 Million in 2025 to $155.3 Million by 2034, registering a CAGR of 5.7%. Growth is directly tied to semiconductor capital expenditure cycles, EU Chips Act–driven fab expansion, and escalating purity standards for advanced process nodes below 7nm. In April 2025, BASF SE announced a high double-digit million-euro investment to construct a state-of-the-art ultra-pure nitric acid facility at Ludwigshafen, Germany. The plant is engineered to meet sub-7nm wafer processing requirements, where contamination levels above parts-per-trillion thresholds can compromise yield integrity. This move aligns with Europe’s ambition to scale domestic chip manufacturing capacity and reduce dependency on imported wet chemicals.

Complementing this expansion, UBE Corporation increased high-purity nitric acid capacity by 30% at its Ube Chemical Factory in November 2024, targeting AI processors and quantum computing chip production under Japan’s advanced fabrication initiatives. In parallel, Mitsubishi Chemical Group expanded its Oregon production base in April 2024, strengthening supply for U.S.-based semiconductor clusters in the Pacific Northwest. The facility focuses on high-grade nitric acid for cleaning and etching stages, which are critical for oxide removal and metal patterning in advanced logic devices. By 2025, industry verification confirmed that Mitsubishi Chemical and BASF collectively controlled approximately 38% of global electronic grade nitric acid supply, supported by long-term contracts with TSMC, Samsung, and Intel as these players commissioned new fabs across the U.S. and Europe.

Integration strategies are reshaping competitive positioning. In October 2025, BASF initiated construction of an electronic ammonium hydroxide plant at Ludwigshafen, reinforcing its Electronic Chemicals Hub model. This vertically integrated system enables synchronized supply of ultra-pure nitric acid and ammonium hydroxide for wafer cleaning cycles, reducing logistics complexity for fabs operating high-volume production lines. Mitsubishi Chemical, during its December 2025 Corporate Strategy Meeting, designated semiconductor materials as a primary growth driver and committed approximately 200 billion yen in investments through FY2026 to fortify purification infrastructure and global supply resilience. Meanwhile, Kanto Chemical launched its SL-Grade nitric acid portfolio in 2025, engineered for 2nm and 3nm process nodes, where contamination above 10 parts-per-trillion of metallic ions can trigger catastrophic yield loss. The introduction of the Ultrapur™ branding underscores the intensifying competition in ultra-high-purity segments.

Emerging markets are building precursor capacity to support downstream electronic refining. In August 2024, Gujarat Narmada Valley Fertilizers & Chemicals approved a 600 metric tons per day weak nitric acid expansion, increasing capacity by 57% to serve India’s expanding electronics manufacturing ecosystem. Similarly, the February 2024 joint venture between Coal India Limited and BHEL to establish a large ammonium nitrate facility strengthens domestic nitric acid precursor availability, indirectly supporting high-purity acid refining for semiconductor applications. Structural consolidation accelerated through 2025–2026, as smaller manufacturers unable to finance multi-stage distillation and microfiltration upgrades exited the electronics segment. Specialized suppliers such as KMG Electronic Chemicals and Asia Union Electronic Chemical Corporation gained share as quality thresholds tightened for 5nm and below nodes. The market’s trajectory is increasingly dictated by semiconductor node migration, purity engineering investment, and regional supply chain localization strategies.

Trends and Opportunities in the Electronic Grade Nitric Acid Market

Intensifying Purity Specifications for Sub-3nm Semiconductor Node Fabrication

- The transition to sub-3nm logic nodes has fundamentally redefined acceptable impurity thresholds for electronic grade nitric acid. Foundries operating at these dimensions now require metal ion control at parts-per-trillion and even parts-per-quadrillion levels, as a single contaminant can bridge nanoscale features and trigger catastrophic yield loss.

- During 2024 and 2025, leading logic manufacturers such as TSMC and Samsung tightened incoming wet chemical specifications for gate-all-around processes. High-end commercial offerings such as Veritas Quantum from GFS Chemicals now certify trace metallic impurities below 500 parts per quadrillion across roughly 68 analytes. This represents a step change from the 10 to 100 ppt tolerance that was typical at the 7nm node.

- Meeting these standards requires capital-intensive purification infrastructure. Multi-stage distillation, ultra-low-leach materials of construction, and sub-0.1 micron particle filtration have become mandatory. In November 2024, UBE Corporation announced a further 30% expansion of high-purity nitric acid capacity at its Ube Chemical Factory, following a 50% expansion earlier in the year. These investments are closely aligned with surging demand from advanced logic, AI accelerators, and data center processors, where electronic grade nitric acid must consistently meet SEMI Grade 5 and above specifications.

On-Site Generation and Point-of-Use Distillation in Advanced Semiconductor Fabs

- As fabs scale in size and complexity, chemical logistics have emerged as a strategic vulnerability. A single advanced fab can consume between 5 and 10 tons of electronic grade nitric acid per month, and reliance on long-distance transport increases the risk of degradation, container leaching, and supply disruption.

- To address this, semiconductor manufacturers are increasingly evaluating on-site generation and point-of-use distillation systems. Patent activity and pilot deployments describe configurations where technical-grade nitric acid is distilled within the fab boundary and delivered directly through ultraclean piping to the tool interface. These systems often employ controlled reflux and continuous purge mechanisms to prevent impurity buildup, effectively locking in purity at the moment of use.

- This approach also creates an economic moat for next-generation fabs. With multi-billion-dollar investments underway in new facilities across Arizona, Texas, and East Asia, integrating chemical purification into the internal utility loop reduces long-term operating costs and insulates production from geopolitical and logistics volatility. As electronic grade nitric acid specifications tighten further, point-of-use purification is expected to move from experimental deployment to standard design practice in leading-edge fabs.

Critical Role in Wet Processing for Silicon Carbide and Gallium Nitride Power Devices

- The rapid adoption of wide-bandgap semiconductors is opening a high-value growth avenue for nitric acid suppliers capable of serving power electronics manufacturing. Silicon carbide and gallium nitride devices are increasingly deployed in electric vehicles, fast chargers, renewable energy inverters, and 5G infrastructure due to their superior breakdown voltage and switching efficiency.

- Manufacturing these materials requires aggressive wet processing steps. Nitric acid based etching mixtures are essential for substrate preparation, defect removal, and surface conditioning, particularly for silicon carbide, which is chemically inert compared to silicon. Power device manufacturers such as Infineon and STMicroelectronics are vertically integrating these processes to secure quality and yield for 800V electric vehicle platforms entering volume production in 2025.

- As power densities increase into the 650V to 2200V range, surface integrity becomes non-negotiable. This creates a premium niche for so-called power-grade nitric acid that bridges industrial volumes with semiconductor-level impurity control, allowing suppliers to command higher margins than conventional bulk acid markets.

Demand from TOPCon and HJT Solar Cell Manufacturing

- The photovoltaic industry is transitioning away from PERC technology toward higher-efficiency Tunnel Oxide Passivated Contact and Heterojunction architectures, both of which significantly increase wet chemical intensity per wafer. Nitric acid plays a critical role in post-texturing cleaning, residue removal, and surface preparation prior to thin-film deposition.

- TOPCon manufacturing involves roughly a dozen wet process steps, with nitric acid used to neutralize and remove organic and metallic residues after alkali texturing. In HJT lines, it supports precise surface cleaning before amorphous silicon deposition, where even trace contamination can degrade cell efficiency.

- The opportunity lies in volume scale. While semiconductor fabs consume smaller quantities at extreme purity, solar manufacturing demands orders of magnitude higher volumes with tight but more cost-sensitive specifications. Countries such as India, which is targeting 479 GW of installed solar capacity by 2047, are driving rapid expansion of gigawatt-scale cell and module factories. This creates sustained demand for solar-grade nitric acid that balances consistent metal ion control with supply reliability and cost efficiency, positioning the segment as a strategic volume anchor for producers serving both electronics and energy transition markets.

Electronic Grade Nitric Acid Market Share and Segmentation Insights

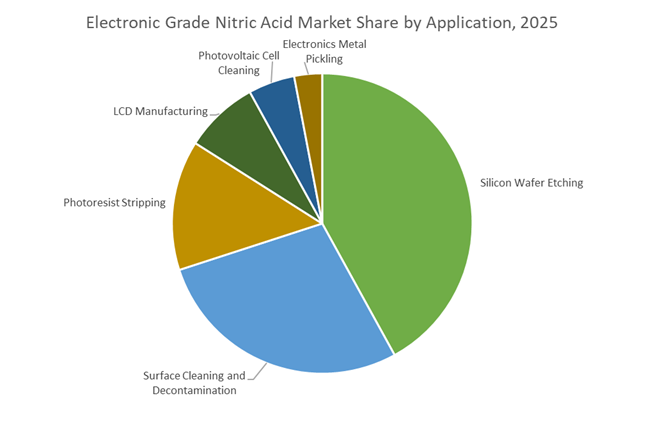

Silicon Wafer Etching Accounts for the Largest Application Share in Semiconductor Processing

Silicon wafer etching represents 42% of total electronic grade nitric acid consumption in 2025, underscoring its critical role in advanced semiconductor fabrication. As a powerful oxidizing agent, electronic grade nitric acid is a core component in isotropic silicon etching mixtures, enabling precise pattern definition and surface modification during integrated circuit manufacturing. Surface cleaning and decontamination constitute a significant secondary segment, driven by ultra-high-purity requirements as device geometries shrink below 5nm and contamination tolerances tighten across leading-edge fabs. Photoresist stripping also consumes a notable share, with nitric acid-based formulations effectively removing resist residues after pattern transfer while preserving underlying microstructures. LCD manufacturing maintains stable demand for thin-film transistor processing, while photovoltaic cell cleaning is emerging rapidly as solar wafer texturization standards evolve. Electronics metal pickling remains a specialized niche focused on oxide removal from precision metal components used in electronic assemblies.

Semiconductor Fabrication Drives Majority Demand for Ultra-High-Purity Nitric Acid

Semiconductor fabrication accounts for 58% of total end-user demand in 2025, positioning it as the dominant revenue contributor within the electronic grade nitric acid market. Expanding production of advanced logic, memory, AI accelerators, automotive semiconductors, and 5G infrastructure components continues to stimulate capacity additions and chemical consumption across global foundries. Flat panel display manufacturing forms a substantial secondary segment, utilizing high-purity nitric acid for substrate cleaning and etching in LCD and OLED production lines serving consumer electronics markets. Solar and renewable energy represents the fastest-growing end-user category, supported by accelerating photovoltaic manufacturing expansion and the need for high-purity wafer cleaning to enhance solar cell efficiency. Aerospace and defense electronics remain a niche but strategically important segment, demanding the highest purity grades and rigorous quality assurance for mission-critical electronic systems operating under extreme environmental conditions.

Competitive Landscape of the Electronic Grade Nitric Acid Market

The Electronic Grade Nitric Acid Market in 2026 is defined by ultra-high purity standards, semiconductor node miniaturization, and ESG-driven low-carbon chemical production, with leading suppliers competing on ppt-level metal control, backward integration, fab-adjacent logistics, and AI-enabled purification systems.

Low-carbon ultra-pure nitric acid leadership by BASF SE

BASF remains a dominant supplier of electronic grade nitric acid (EL and UL grades), leveraging its integrated Verbund model for ammonia and acid production stability. In March 2024, BASF secured $75 million from the U.S. Department of Energy to develop low-carbon nitric acid at its Freeport, Texas site, reinforcing its 2026 sustainable chemistry leadership. Between 2025 and 2026, the Ludwigshafen expansion introduced advanced distillation units achieving 99.999%+ purity while cutting byproducts by 30%. Backward integration into ammonia feedstock insulated BASF from 2025 supply shocks. The company maintains a strong footprint serving European and North American semiconductor foundries focused on advanced-node wafer cleaning.

Asia-Pacific giga-foundry focus from UBE Corporation

UBE concentrates on high-margin electronic and ultra-low metal nitric acid grades for wafer texturization and precision etching in LCD and solar panel manufacturing. In late 2024 and early 2025, UBE completed a 30% capacity expansion at its Yamaguchi facility to support rising demand from Japanese and South Korean semiconductor manufacturers. With Asia-Pacific accounting for over 58% of global electronic grade nitric acid consumption, UBE strategically prioritizes EL and VL grades over commodity fertilizer applications. Its “specialty over bulk” model strengthens profitability while aligning with sub-10nm semiconductor cleaning requirements and high-purity wet chemical demand in advanced chip fabrication.

Integrated wet chemical solutions with AI purification by Mitsubishi Chemical Group

Mitsubishi Chemical differentiates through integrated wet chemical solutions, bundling high-purity nitric acid with ammonia and hydrogen peroxide for total fab cleaning systems. In 2025 and 2026, the company expanded Product Carbon Footprint (PCF) tracking across its electronic chemical portfolio, supporting semiconductor leaders in Scope 3 emission audits. Its nitric acid is widely used in wafer surface preparation for sub-5nm chip architectures, where ultra-low metal-ion contamination is critical. In 2026, Mitsubishi deployed AI-powered predictive analytics across purification lines, reducing batch-to-batch impurity variation by 20%, enhancing yield stability for high-density logic and memory chip production.

Parts-per-trillion purity benchmark by Kanto Chemical Co., Inc.

Kanto Chemical is widely regarded as the purity benchmark in electronic reagents, offering its Ultrapur™ nitric acid series with metal impurities controlled at the ppt level. Products are packaged in high-grade PFA containers to prevent glass-leached contamination, a key differentiator for advanced node fabs. As of February 2026, Kanto expanded its Kanto-PPC joint venture to serve semiconductor hubs in Southeast Asia, strengthening localized supply chains. Its custom specification services enable fab operators to request concentration blends optimized for 3D NAND and logic chip etching recipes. Facility upgrades include Class 1 cleanroom bottling lines, reinforcing contamination control leadership.

Fab-adjacent supply resilience from KMG Electronic Chemicals

As part of the Entegris ecosystem, KMG Electronic Chemicals plays a critical role in North America’s semiconductor supply chain. Leveraging CHIPS and Science Act funding in 2025, the company expanded high-purity chemical distribution centers near major fab sites in Arizona and Ohio. Its electronic grade nitric acid supports semiconductor etching and PCB fabrication, with a strong focus on just-in-time delivery to prevent operational downtime. In 2026, KMG introduced a closed-loop container return system, reducing chemical waste and enhancing environmental compliance while strengthening supply chain resilience in the Silicon Heartland region.

Japan: Ultra-High Purity Leadership and Supply Chain Hardening

Japan continues to anchor the global electronic grade nitric acid market through precision-driven capacity expansion and purity innovation aligned with sub-5 nm semiconductor roadmaps. In November 2024, UBE Corporation confirmed a 30% capacity expansion for high-purity electronic grade nitric acid at its Ube Chemical Factory in Yamaguchi Prefecture. The project is engineered specifically for advanced logic and memory fabs supporting AI accelerators and data center hardware, with full operational readiness targeted by mid-2026. This expansion reflects Japan’s strategic intent to remain indispensable to next-generation semiconductor etching and cleaning processes.

Purity differentiation remains Japan’s competitive cornerstone. In early 2025, Kanto Chemical introduced its SL Grade nitric acid with metallic impurities restricted to below 10 ppt, a specification calibrated for 2 nm logic chip etching. Complementing this, UBE launched its Specialty Material Application Center at its Osaka R&D hub in May 2025 to customize nitric acid purity profiles for EUV lithography yield optimization. On the sustainability front, Mitsubishi Chemical has deployed digital twin systems to reduce energy intensity in acid distillation, targeting a 12% carbon footprint reduction by 2026. Meanwhile, geopolitical risk mitigation has prompted Japanese producers to maintain a minimum 90-day buffer stock of ammonia feedstock as of Q3 2025, reinforcing supply continuity for domestic and export-facing semiconductor fabs.

Taiwan: Foundry-Driven Demand and Net-Zero Chemical Qualification

Taiwan’s electronic grade nitric acid market is tightly synchronized with foundry expansion cycles, particularly the 2 nm ecosystem led by TSMC. At the November 2025 Supply Chain Management Forum, TSMC highlighted key chemical suppliers, including Chang Chun Petrochemical, for scaling high-purity chemical infrastructure to support fab ramps in Hsinchu and Kaohsiung through 2026. This recognition underscores the strategic role of localized nitric acid supply in minimizing contamination and logistics risks.

Demand acceleration is reinforced by macro output growth. The Industrial Technology Research Institute projected a 19.1% rise in Taiwan’s semiconductor output value in 2025, directly translating into higher consumption of electronic-level nitric acid. Local producers such as T.N.C. Industrial have responded by upgrading distillation efficiency and yield consistency. Parallel to volume growth, TSMC’s 2025 Net-zero: Transforming Supply Chains initiative has imposed strict environmental audits, requiring nitric acid suppliers to submit detailed Scope 1 and Scope 2 emissions data by Q1 2026. This mandate is reshaping supplier qualification from a purity-only benchmark to a combined purity-plus-carbon performance model.

South Korea: Fab Megaclusters and Localization of Ultra-Pure Acids

South Korea’s electronic grade nitric acid landscape is being redefined by an unprecedented semiconductor investment cycle. Samsung Electronics and SK Hynix have outlined combined operating profit projections of 200 trillion won for 2026, supported by aggressive fab construction. Samsung’s P5 fab at Pyeongtaek, initiated in late 2025, represents a major captive demand center for ultra-high purity nitric acid etchants.

Structural demand is further amplified by SK Hynix’s 128 trillion won investment in the Yongin Semiconductor Cluster between 2025 and 2028. This project embeds on-site chemical parks to house high-purity acid suppliers, reducing transportation risk and ensuring real-time supply reliability. Policy support reinforces this trend. The Ministry of Trade, Industry and Energy issued a 2025 policy framework incentivizing localization of 100 key semiconductor materials, including G5-grade nitric acid. R&D grants and tax incentives are now driving domestic producers to cut reliance on Japanese imports by an estimated 25% by 2027.

United States: CHIPS-Driven Decentralization and Regulatory Tightening

The U.S. electronic grade nitric acid market is expanding in parallel with semiconductor reshoring under the CHIPS and Science Act. By August 2024, more than 90 manufacturing projects across 28 states had been announced, representing $450 billion in planned investments. This surge is catalyzing the construction of decentralized chemical purification units in Arizona and Texas to serve advanced fabs operated by Intel and TSMC.

In March 2025, TSMC deepened its U.S. commitment with an additional $100 billion investment for three advanced fabs, prompting suppliers such as KMG Electronic Chemicals to expand high-purity nitric acid distillation capacity in North America through 2026. Regulatory dynamics are also reshaping plant design. The U.S. Environmental Protection Agency is preparing updated TSCA risk evaluations for inorganic acids in 2026, pushing manufacturers toward closed-loop chemical delivery and on-tool refill systems to reduce occupational exposure in cleanroom environments. Compliance readiness is increasingly a prerequisite for long-term supply contracts.

China: Self-Sufficiency Push and ZLD-Enabled Purification

China’s electronic grade nitric acid market is advancing rapidly under the final phase of Made in China 2025, with a strong emphasis on domestic substitution. In mid-2025, Juhua Group and Jianghua Microelectronics Materials reported successful trial production of EL-grade nitric acid exceeding 99.999% purity for domestic fabs capable of 7 nm processing. These milestones mark a critical step toward reducing dependence on imported electronic chemicals.

A notable differentiator in China is cross-industry technology transfer. Chemical parks are adapting Zero Liquid Discharge systems originally developed for water-intensive textile dyeing into high-purity acid manufacturing. This integration supports compliance with China’s 2026 National Environmental Standards while enabling higher recycling rates of process water and acids. As a result, Chinese producers are positioning electronic grade nitric acid not only as a strategic semiconductor input but also as a showcase for environmentally compliant, large-scale purification infrastructure.

Electronic Grade Nitric Acid Market: Country-Level Strategic Snapshot

Electronic Grade Nitric Acid Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Differentiator

|

Structural Impact

|

|

Japan

|

Purity innovation and buffer stock policy

|

<10 ppt impurity grades

|

Leadership in sub-5 nm fabs

|

|

Taiwan

|

Foundry expansion and net-zero mandates

|

Supplier carbon audits

|

Dual focus on purity and emissions

|

|

South Korea

|

Fab megaclusters

|

On-site chemical parks

|

Reduced logistics and import reliance

|

|

United States

|

CHIPS-led reshoring

|

Decentralized purification units

|

Regionalized supply chains

|

|

China

|

Self-sufficiency targets

|

ZLD-enabled purification

|

Import substitution and scale

|

Electronic Grade Nitric Acid Market Report Scope

Electronic Grade Nitric Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$94.3 Million

|

|

Market Size (2034)

|

$155.3 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Grade (Electronic Grade, VLSI Grade, ULSI Grade, Super Level Grade), By Application (Silicon Wafer Etching, Surface Cleaning and Decontamination, Photoresist Stripping, LCD Manufacturing, Photovoltaic Cell Cleaning, Electronics Metal Pickling), By End-User Industry (Semiconductor Fabrication, Flat Panel Displays, Solar and Renewable Energy, Aerospace and Defense Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mitsubishi Chemical Group Corporation, Kanto Chemical Co., Inc., BASF SE, UBE Corporation, Dow Inc., KMG Electronic Chemicals, Asia Union Electronic Chemical Corp., T.N.C. Industrial Co., Ltd., Juhua Group, Suzhou Crystal Clear Chemical, Jianghua Microelectronics Materials, Columbus Chemicals, EuroChem Group, Honeywell International Inc., Shin-Etsu Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electronic Grade Nitric Acid Market Segmentation

By Product Grade

- Electronic Grade

- VLSI Grade

- ULSI Grade

- Super Level Grade

By Application

- Silicon Wafer Etching

- Surface Cleaning and Decontamination

- Photoresist Stripping

- LCD Manufacturing

- Photovoltaic Cell Cleaning

- Electronics Metal Pickling

By End-User Industry

- Semiconductor Fabrication

- Flat Panel Displays

- Solar and Renewable Energy

- Aerospace and Defense Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Electronic Grade Nitric Acid Industry

- Mitsubishi Chemical Group Corporation

- Kanto Chemical Co., Inc.

- BASF SE

- UBE Corporation

- Dow Inc.

- KMG Electronic Chemicals

- Asia Union Electronic Chemical Corp.

- T.N.C. Industrial Co., Ltd.

- Juhua Group

- Suzhou Crystal Clear Chemical

- Jianghua Microelectronics Materials

- Columbus Chemicals

- EuroChem Group

- Honeywell International Inc.

- Shin-Etsu Chemical Co., Ltd.

*- List not Exhaustive