Emulsion Coatings Market Expansion Driven by Water-Based Technologies, Renovation Demand, and Bio-Based Resin Innovation

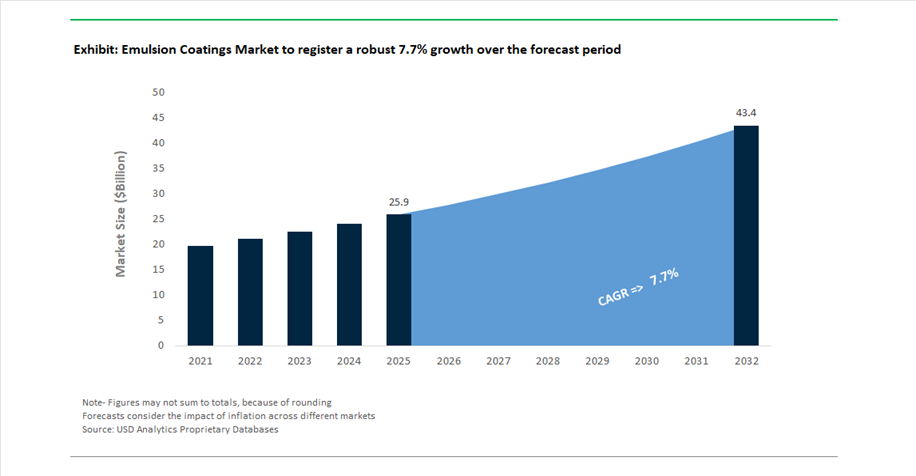

The global Emulsion Coatings Market reached a valuation of USD 25.9 billion in 2025 and is projected to expand at a CAGR of 7.7% between 2025 and 2032, reaching USD 43.5 billion by 2032. This strong growth trajectory reflects the accelerating shift toward water-based coating technologies, driven by tightening environmental regulations, rising urbanization, and increasing consumer preference for low-VOC, odor-free, and environmentally sustainable paints.

Emulsion coatings, primarily based on acrylic, vinyl acrylic, and styrene-butadiene binders, are widely used across residential, commercial, and industrial applications due to their ease of application, durability, color retention, and cost efficiency. A key growth driver is the global expansion of the housing renovation and repainting market, particularly in mature economies where new construction activity is stabilizing. This shift is leading manufacturers to develop high-performance emulsions with enhanced scrub resistance, stain resistance, and long-lasting finish quality, targeting premium interior and exterior segments.

Sustainability is becoming a central innovation axis in the emulsion coatings market. Increasing regulatory pressure in regions such as Europe and India is pushing manufacturers toward bio-based binders, reduced carbon footprint formulations, and green building certifications. Additionally, advancements in pigment dispersion technology and interference pigments are enabling new aesthetic possibilities such as “liquid-metal” and multi-dimensional finishes, traditionally associated with solvent-borne coatings.

Strategic Acquisitions, Premium Product Launches, and Bio-Based Resin Investments Redefine Competitive Landscape

The emulsion coatings market is undergoing significant transformation driven by strategic acquisitions, product innovation, and upstream material investments. In January 2026, Sherwin-Williams confirmed the successful integration of Suvinil, which contributed $164.5 million in Q4 2025 revenue, strengthening its leadership in the Latin American decorative coatings segment. This acquisition enhances Sherwin-Williams’ position in premium emulsion coatings, particularly in Brazil’s high-growth residential and repaint markets.

Product innovation remains a central competitive lever. In January 2026, PPG Industries launched the Master’s Mark Ballard™ Flat Interior Emulsion, an advanced all-in-one solution offering superior hiding power and scrub resistance. This launch targets the premium residential repaint segment in China, aligning with the company’s broader “Refresh & Sustain” strategy focused on low-emission, high-performance coatings. Similarly, in October 2025, BASF introduced its “Driving the Proxy” color collection, incorporating advanced emulsion binders and interference pigments to deliver multi-dimensional visual effects with reduced carbon intensity.

Market players are also adapting to shifting demand dynamics. In February 2026, Nippon Paint announced a strategic pivot toward the renovation and repair segment through its DGL Pacific operations, leveraging durable emulsion coatings to offset slower new construction activity. Meanwhile, Jotun expanded its production capacity in India to meet growing demand for high-performance, green-certified exterior emulsions, reinforcing its competitive position in a rapidly evolving regulatory environment.

India is emerging as a key battleground for market share. In January 2026, JSW Paints disrupted traditional pricing models through its “Think Beautiful” initiative, offering uniform pricing across all color shades. This approach simplifies purchasing decisions and targets semi-urban and rural consumers, where price transparency is a critical factor in brand selection.

Upstream investments are further accelerating innovation. In February 2024, Arkema increased its capacity for bio-based emulsion resins, enabling paint manufacturers to achieve 20–30% reductions in lifecycle carbon footprint. These materials are becoming essential for companies aiming to meet sustainability targets and differentiate their product portfolios in competitive markets.

CARB SCM 2024 Enforcing 50 g/L VOC Limits Reshaping Architectural Emulsion Coatings Formulation

The enforcement of the California Air Resources Board Suggested Control Measure framework has established a new regulatory baseline for low-VOC emulsion coatings across North America, particularly within architectural applications. Between 2024 and 2026, major air districts, including South Coast AQMD, have aligned key coating categories such as non-flat paints, primers, and floor coatings to a stringent 50 g/L VOC limit, effectively phasing out traditional 100 g/L and 150 g/L solvent-containing formulations. This regulatory shift is compelling manufacturers to accelerate the development of near-zero-VOC and waterborne emulsion technologies that can meet performance expectations previously associated with solvent-based systems. The environmental impact is significant, with CARB data indicating that transitioning a typical large-scale commercial project from 150 g/L to 50 g/L coatings can reduce site-specific organic emissions by approximately 66%, supporting compliance with municipal air quality standards. In parallel, Section 39613 of the California Health and Safety Code imposes financial penalties on manufacturers exceeding 250 tons of VOC emissions annually, reinforcing the economic rationale for adopting low-emission chemistries. To maintain durability at reduced VOC levels, 2026-grade emulsion coatings are increasingly based on self-crosslinking acrylic copolymers capable of delivering performance comparable to AAMA 2605 specifications, ensuring long-term weather resistance and film integrity in demanding exterior applications.

China GB/T 9756-2024 Elevating Performance Benchmarks for Synthetic Resin Emulsion Coatings

China’s GB/T 9756-2024 standard is redefining the performance expectations for synthetic resin emulsion coatings, introducing stricter technical criteria that elevate the overall quality threshold within the world’s largest architectural coatings market. The updated standard, which replaces the 2018 version, significantly increases scrub resistance requirements for high-performance interior wall coatings, with “Superior” grade products now required to achieve at least 6,000 scrub cycles, compared to the previous 5,000-cycle benchmark. Even entry-level “Acceptable” grade coatings must now meet a minimum of 350 scrub cycles, eliminating low-durability formulations from both residential and commercial applications. The revision also mandates improved hiding power through higher contrast ratio requirements, ensuring that white and light-colored paints achieve at least a 5% improvement in opacity, thereby reducing material consumption and application costs. Regulatory enforcement has been strengthened through the integration of water-based architectural coatings into China’s Compulsory Certification framework, requiring third-party verification of both performance and hazardous substance compliance under GB 18582 standards. This convergence of durability, efficiency, and compliance requirements is driving manufacturers toward advanced binder systems, optimized pigment formulations, and higher-quality raw materials to maintain competitiveness in the Chinese market.

Bio-Based Emulsion Coatings with ≥25% Renewable Content Aligning with LEED v5 Demand

The emergence of LEED v5 certification frameworks is creating a substantial opportunity for bio-based emulsion coatings that incorporate at least 25% renewable content, positioning these products at the intersection of sustainability and high-performance architectural applications. These coatings leverage renewable raw materials such as plant oils, agricultural byproducts, and bio-derived polymers to replace conventional petroleum-based monomers, enabling manufacturers to align with evolving green building requirements. Under LEED v5, coatings verified through ASTM D6866 carbon dating for bio-based content are eligible for maximum scoring under the Building Product Disclosure and Optimization and low-emitting materials credits, making them highly attractive for large-scale commercial and institutional projects. From an environmental perspective, transitioning to bio-based binders can achieve a reduction of approximately 41% in cradle-to-gate carbon emissions compared to traditional acrylic emulsions, supporting broader decarbonization goals in the construction sector. Performance improvements are also notable, with soy-based and castor-oil-modified emulsions demonstrating up to 15% higher adhesion performance on challenging substrates such as recycled metals and composites. Additionally, the use of non-food agricultural waste streams as raw materials can reduce production costs by up to 17% for high-volume manufacturers, enhancing both economic and environmental value propositions.

Formaldehyde-Eliminating Emulsion Coatings Advancing Indoor Air Quality in High-Occupancy Spaces

The growing emphasis on indoor air quality and healthy building standards is creating a strong market opportunity for formaldehyde-eliminating emulsion coatings designed to actively neutralize indoor pollutants. These advanced coatings incorporate active scavenging chemistries capable of converting airborne formaldehyde into inert compounds, significantly improving air quality in enclosed environments. By 2026, high-performance formulations are capable of removing up to 75% of airborne formaldehyde within treated spaces over a service period of approximately 36 months, making them particularly relevant for environments with high off-gassing potential such as newly furnished interiors. These coatings enable compliance with stringent indoor air quality thresholds, including maintaining formaldehyde concentrations below 0.1 parts per million as recommended by global health authorities. Adoption is accelerating across healthcare and educational infrastructure, where more than 40% of new projects are specifying coatings that combine pollutant scavenging with antimicrobial or antiviral properties, including up to 99.9% viral inactivation performance. Additional functional benefits include rapid odor reduction, with these coatings capable of lowering ambient odor levels by approximately 50% within 24 hours of application, enabling faster re-occupancy of treated spaces. This shift toward active, performance-driven coatings is expanding the functional role of emulsion coatings beyond protection and aesthetics into health-centric building solutions.

Paints & Coatings Segment Dominates Emulsion Coatings Market with 71% Share Driven by Global Architectural Paint Demand

Product Type Analysis: Waterborne Emulsion Paints Lead with Massive Volume and Regulatory Compliance

Paints and coatings account for a dominant 71.0% share of the emulsion coatings market in 2025, driven by the extensive use of waterborne acrylic, styrene-acrylic, and vinyl acetate ethylene (VAE) emulsions as the primary binder technology in architectural paints. These emulsions form the backbone of the global paint industry, with total production exceeding 40–45 billion liters annually, largely concentrated in interior and exterior wall coatings. The dominance is reinforced by stringent global VOC regulations (EPA AIM, SCAQMD Rule 1113, EU Deco Paint Directive, China GB 18582), which have effectively phased out solvent-borne alternatives in most applications. Additionally, the rise of low-VOC and zero-VOC emulsion formulations, along with bio-based polymer innovations, is supporting sustainability goals and green building certifications such as LEED v4.1 and WELL. These factors position emulsion-based paints as the core driver of the global waterborne coatings market.

Professional Segment Leads Emulsion Coatings Market with 54% Share Driven by High-Volume Projects and Premium Product Adoption

User Type Analysis: Contractors and Commercial Projects Drive Value Growth in Emulsion Coatings

The professional segment holds a leading 54.0% share of the emulsion coatings market in 2025, driven by the high consumption of coatings in large-scale construction, renovation, and industrial projects. Professional painters and contractors prioritize premium, high-performance coatings that reduce labor time—the largest cost component of any project—through features such as high opacity (fewer coats), fast drying, superior flow and leveling, and long-term durability. This drives demand for 100% acrylic emulsions and advanced waterborne alkyd-acrylic hybrids, which command higher price points. Additionally, the segment is heavily influenced by specification-driven demand (MPI standards, MasterSpec guidelines) and supported by the pro dealer distribution network, offering services such as job-site delivery, technical support, and precise color matching. These factors create strong brand loyalty and consistent demand, positioning the professional segment as the primary value generator in the global emulsion coatings market.

Emulsion Coatings Market Competitive Landscape Driven by Low-VOC Technologies, AI Color Systems, and High-Performance Waterborne Binders

The emulsion coatings market is highly competitive, shaped by demand for waterborne coatings, low-VOC formulations, and AI-enabled color innovation. Leading players are focusing on sustainable binders, decorative emulsions, and advanced architectural coatings to serve residential, commercial, and automotive applications globally.

PPG Advances Emulsion Coatings with AI-Driven Color Innovation and Automotive Integration

PPG Industries, Inc. is strengthening its position in emulsion coatings through AI-driven color forecasting and premium finish technologies. Its 2026 “Parallels” design theme and Secret Safari color highlight advanced multi-dimensional finishes for automotive OEM and architectural coatings. The company reported $15.9 billion in 2025 sales, supported by strong growth in Asia-Pacific collaborations, including projects with Chery and Xiaomi. PPG’s emulsion coatings integrate substrate protection with dynamic color-shifting properties. Its localized R&D and joint labs enhance responsiveness to regional demand trends. The company’s innovation in high-performance emulsions positions it as a leader in premium coatings.

AkzoNobel Elevates Premium Emulsion Coatings with Bio-Based Binders and Global Expansion

AkzoNobel N.V., through its Dulux brand, is focusing on ultra-premium interior emulsion coatings such as Velvet Touch Eterna. Following strategic portfolio realignment, the company is strengthening its presence in Latin America through Grupo Orbis integration. Its “Winning Ways” strategy emphasizes industrial efficiency and sustainable product innovation. AkzoNobel is developing bio-based binders to support circular packaging goals and low-VOC urban coatings demand. The company maintains leadership in architectural coatings with a focus on contractor-grade performance. Its sustainability-driven emulsion portfolio enhances its global competitiveness.

Sherwin-Williams Drives Emulsion Growth with Waterborne Technologies and AI-Based Color Matching

The Sherwin-Williams Company is expanding its emulsion coatings portfolio through advanced waterborne technologies and zero-VOC formulations. The company is leveraging a 5.4% growth trajectory supported by rising residential construction and home completions. Its AI-powered color-matching systems optimize coating selection based on climate and substrate conditions. Sherwin-Williams is promoting cool roof emulsion coatings and high-reflectivity finishes to meet energy efficiency standards. Its vertically integrated supply chain ensures resilience amid raw material volatility. The company’s strong retail network reinforces its dominance in architectural emulsion coatings.

Nippon Paint Strengthens Emulsion Market Position with Asset Assembler Strategy and APAC Focus

Nippon Paint Holdings is leveraging its “Asset Assembler” model to expand its emulsion coatings footprint across Asia-Pacific. The company is achieving steady growth through targeted acquisitions and organic expansion in home-care and decorative segments. Its operations in China remain resilient, supported by strong demand in both professional and consumer channels. Nippon Paint’s premium emulsions are widely recognized for durability in tropical climates. The company has broadened its portfolio to include both water-based and solvent-based decorative coatings. Its regional branding and consumer engagement strategies enhance market penetration.

Asian Paints Expands Emulsion Coatings Leadership with Nanotechnology and Smart Manufacturing

Asian Paints Limited continues to dominate the emulsion coatings market in Asia-Pacific, supported by strong revenue growth. The company is integrating coatings with home décor and waterproofing services, creating a holistic customer offering. Its Apex Ultima and Royale emulsions are being enhanced with nanotechnology for improved dirt resistance. Asian Paints is investing in smart manufacturing facilities to manage input cost volatility and maintain margins above 18%. Its strong distribution network ensures penetration across urban and semi-urban markets. The company’s innovation in durable emulsions strengthens its leadership position.

BASF Drives Emulsion Coatings Innovation with High-Performance Binders and Circular Economy Solutions

BASF SE, through its Dispersions & Resins division, is advancing emulsion coatings with Acronal® high-performance binders designed for one-coat applications. The company is focusing on sustainable coatings by integrating mass-balance certified raw materials into its formulations. Its Zhanjiang Verbund site in China enhances production capacity for high-purity resins used in low-VOC coatings. BASF’s solutions help developers reduce labor time and material consumption in large-scale projects. The company is aligning its portfolio with net-zero and circular economy goals. Its leadership in binder technology positions it as a key enabler of next-generation emulsion coatings.

China Emulsion Coatings Market: Green Industrialization and Monomer Integration Driving Global Leadership

China remains the global leader in emulsion coatings, driven by aggressive sustainability mandates under the 15th Five-Year Plan (2026–2030). A major structural shift is underway, with ~60% of solvent-based coating lines being converted to waterborne emulsion systems due to strict VOC regulations.

Upstream integration is a key advantage. Projects like BASF’s Zhanjiang Verbund expansion are strengthening domestic supply of glacial acrylic acid and butyl acrylate, the core building blocks for acrylic emulsions. Demand is also being fueled by large-scale infrastructure and climate initiatives, including cool roof programs using ceramic-microsphere acrylic emulsions to reduce urban heat islands. Additionally, growth in EVs is driving use of emulsion-based dielectric coatings for LFP battery separators, while textile exports are accelerating adoption of fluorine-free water-repellent emulsions.

United States Emulsion Coatings Market: Bio-Based Innovation and Infrastructure Demand Driving High-Value Growth

The United States market is evolving toward sustainable and high-performance emulsion systems, supported by regulatory and fiscal incentives. Under the Inflation Reduction Act, tax credits are linked to Solar Reflectance Index (SRI)-certified coatings, boosting adoption of reflective emulsion coatings in commercial buildings.

Innovation is strong across multiple segments. The launch of waterborne acrylic-polyurethane hybrid emulsions provides solvent-like performance with faster drying times, particularly in automotive refinish applications. Regulatory pressure is also accelerating the shift toward PFAS-free additives, while partnerships (e.g., Evonik–IMCD) are expanding availability of low-odor, high-durability emulsion resins. Additionally, demand from EV systems is increasing use of metallized emulsion films in traction capacitors, and strong residential construction is driving growth in stain-resistant interior emulsions.

Germany Emulsion Coatings Market: Circular Chemistry and Energy Efficiency Driving Sustainability Leadership

Germany is at the forefront of sustainable emulsion coatings, driven by strict EU regulations and the “Renovation Wave.” The adoption of UV/EB-curable emulsion hybrids has enabled up to 70% reduction in carbon footprint in industrial wood applications.

Regulatory frameworks are shaping innovation. Compliance with EU Biocide Regulations (2026) is accelerating the development of biocide-free, mineral-stabilized emulsions, while government subsidies are promoting Exterior Wall Insulation (ETICS) systems using self-healing polymer emulsions. Germany is also pioneering recycled-monomer acrylic emulsions, supporting circular economy goals. Additionally, investments in hydrogen infrastructure are driving demand for emulsion-based protective coatings that resist embrittlement, reinforcing Germany’s leadership in eco-friendly coatings.

India Emulsion Coatings Market: Capacity Consolidation and Smart Cities Driving Rapid Expansion

India is experiencing rapid growth in emulsion coatings, supported by infrastructure expansion and supply chain localization. A major milestone is the JSW Paints acquisition of Akzo Nobel India (2025), creating a strong domestic player focused on high-volume architectural emulsions.

Government initiatives are key drivers. The Smart Cities Mission mandates cool roof emulsion coatings in affordable housing across 100+ cities, significantly boosting demand. At the same time, the market is shifting toward domestic production of styrene-acrylic emulsions, reducing reliance on imports. Infrastructure projects under the Gati Shakti master plan are driving demand for emulsion-based corrosion protection primers for railways and bridges. Additionally, growth in cold-chain logistics is increasing use of antifungal emulsion coatings in storage facilities, expanding application scope.

Japan Emulsion Coatings Market: Nanotechnology and Thermal Management Driving Precision Innovation

Japan’s emulsion coatings market is defined by high-performance, precision-driven innovations, particularly in construction and electronics. Breakthroughs include aerogel-infused acrylic emulsions, offering superior thermal insulation in thin-film applications.

Technological advancements are also evident in manufacturing. The adoption of in-mold emulsion coating technology in automotive production reduces CO₂ emissions by up to 60% by eliminating traditional paint processes. Additionally, Japan is leading in ultra-thin emulsion films (<500 nm) for MLCC production and photocatalytic self-cleaning coatings for building facades. High-elongation elastomeric emulsions (>800% stretchability) are also being developed for seismic resilience, reinforcing Japan’s leadership in advanced materials.

UAE Emulsion Coatings Market: Desert-Grade Performance and Smart City Mandates Driving Demand

The UAE is a global testbed for extreme-performance emulsion coatings, designed for harsh desert environments. Regulations such as Dubai Municipality TG-04 standards have accelerated adoption of waterborne coatings, now accounting for >47% of market volume.

Demand is driven by megaprojects and infrastructure. High-reflectivity acrylic emulsions are being used in iconic developments like the Museum of the Future to combat intense solar loads. Innovations include sand-abrasion-resistant coatings that prevent dust adhesion, maintaining both performance and aesthetics. Additionally, the Dubai 2040 Urban Master Plan mandates reflective coatings for industrial buildings, while offshore energy projects are driving demand for nanotechnology-infused protective emulsions and intumescent fire-protection coatings.

Emulsion Coatings Market Report Scope

Emulsion Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.9 Billion

|

|

Market Size (2032)

|

$43.5 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Resin Type (Acrylic Emulsions, Vinyl Acetate Emulsions, Polyurethane Emulsions, Styrene-Butadiene, Alkyd Emulsions, Others), By Product Type (Paints and Coatings, Primers and Sealers, Varnishes and Lacquers, Adhesives and Sealants, Textile and Paper Coatings), By End-Use Sector (Residential, Commercial and Institutional, Industrial and Infrastructure, Marine and Aerospace), By Performance Characteristic (General Purpose, High-Performance), By User Type (Professional, DIY)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Kansai Paint Co., Ltd., RPM International Inc., Jotun A/S, BASF SE, Masco Corporation, Axalta Coating Systems Ltd., Berger Paints India Limited, Hempel A/S, Sika AG, DAW SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Emulsion Coatings Market Segmentation

By Resin Type

- Acrylic Emulsions

- Vinyl Acetate Emulsions

- Polyurethane Emulsions

- Styrene-Butadiene

- Alkyd Emulsions

- Others

By Product Type

- Paints and Coatings

- Primers and Sealers

- Varnishes and Lacquers

- Adhesives and Sealants

- Textile and Paper Coatings

By End-Use Sector

- Residential

- Commercial and Institutional

- Industrial and Infrastructure

- Marine and Aerospace

By Performance Characteristic

- General Purpose

- High-Performance

- Anti-microbial

- Chemical and Corrosion Resistant

- UV-Resistant and Weatherable

- Low-VOC

By User Type

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Emulsion Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- RPM International Inc.

- Jotun A/S

- BASF SE

- Masco Corporation

- Axalta Coating Systems Ltd.

- Berger Paints India Limited

- Hempel A/S

- Sika AG

- DAW SE

*- List not Exhaustive