Epoxy Coatings Market Expansion Driven by Infrastructure Investment, Marine Protection Demand, and Specialty Epoxy Innovation

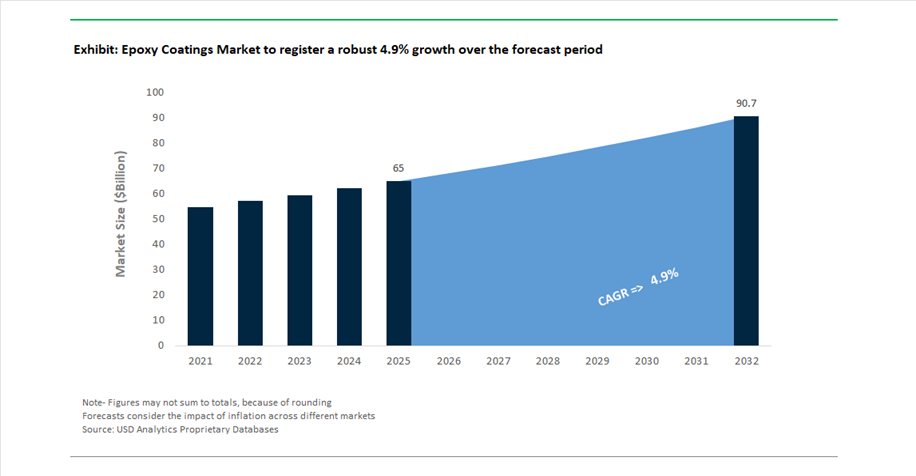

The global Epoxy Coatings Market reached a valuation of USD 65 billion in 2025 and is projected to grow at a CAGR of 4.9% between 2025 and 2032, reaching USD 90.9 billion by 2032. This steady growth trajectory is underpinned by the critical role epoxy coatings play in corrosion protection, chemical resistance, mechanical durability, and structural integrity across industrial, marine, construction, and energy sectors.

Epoxy coatings are widely utilized in infrastructure projects, offshore energy installations, pipelines, marine vessels, and heavy industrial equipment, where long-term performance under extreme environmental conditions is essential. A major growth driver is the continued global investment in infrastructure modernization and energy transition projects, including offshore wind farms, shipbuilding, and oil & gas assets. These applications require high-performance, long-lifecycle coatings capable of withstanding harsh chemical exposure, saltwater corrosion, and mechanical stress.

Another structural trend shaping the market is the shift toward high-solids, solvent-free, and low-VOC epoxy systems, driven by tightening environmental regulations and sustainability targets. Manufacturers are increasingly developing coatings that reduce application time, lower carbon emissions, and improve worker safety, while maintaining or enhancing protective performance. Additionally, the market is seeing growing demand for passive fire protection (PFP) epoxy coatings, particularly in public infrastructure and energy assets where fire safety compliance is critical.

Specialty Epoxy Breakthroughs, Capacity Rationalization, and AI-Driven Manufacturing Reshape Industry Dynamics

The epoxy coatings market is undergoing a structural shift driven by product innovation, supply chain optimization, and digital transformation in resin manufacturing. In March 2025, Hempel launched Hempafire Extreme 550, a next-generation epoxy-based passive fire protection coating. This solvent-free system provides up to four hours of fire resistance while reducing required dry film thickness by up to 40%, significantly improving application efficiency and lowering emissions in large-scale steel construction projects.

Supply-side rationalization is becoming increasingly evident. In January 2026, Olin Corporation announced the closure of its Brazil epoxy plant under its “Beyond250” strategy, reflecting a broader industry shift toward consolidated, high-efficiency production hubs and a strategic pivot toward specialty epoxy products rather than commodity-grade resins. This trend is reshaping global supply chains and pricing dynamics within the epoxy market.

Collaborative innovation is also accelerating the development of advanced formulations. In December 2024, Hexion partnered with Clariant to develop high-performance intumescent epoxy coatings, targeting aerospace and public infrastructure applications where enhanced fire safety and structural protection are critical. Complementing this, Hexion’s acquisition of Smartech has enabled AI-driven process optimization, reducing batch variability in epoxy resin production by over 15% as of early 2026.

Capacity expansion and regional demand alignment remain key strategic priorities. In February 2026, Jotun expanded its production capabilities in India to meet growing demand for marine and protective epoxy coatings, driven by shipbuilding and infrastructure initiatives. Meanwhile, AkzoNobel secured a major marine coatings contract in March 2026, supplying high-solids, low-VOC epoxy systems for large-scale ferry construction, reflecting the industry’s shift toward environmentally compliant marine coatings.

Technological advancements are also bridging sustainability and performance. In January 2026, PPG Industries introduced Enviro-Prime Epic 200R, a low-bake epoxy electrocoat system that reduces curing temperatures to 150°C, significantly lowering energy consumption in automotive manufacturing. Additionally, Kansai Helios strengthened its European footprint by integrating WEILBURGER’s high-performance epoxy portfolio in May 2025, expanding its offerings in chemical-resistant and non-stick industrial coatings.

From a financial performance perspective, Hempel reported record profitability in March 2026, driven by strong demand for specialty epoxy coatings in energy and infrastructure sectors, particularly offshore wind and passive fire protection applications.

EPA Safer Communities Rule Driving Demand for High-Performance Epoxy Secondary Containment Systems

The implementation of the U.S. Environmental Protection Agency’s Safer Communities by Chemical Accident Prevention rule is significantly reshaping demand patterns within the epoxy coatings industry, particularly for high-build, chemically resistant systems used in secondary containment infrastructure. The updated Risk Management Plan framework introduces stricter audit and compliance thresholds, requiring facilities with multiple reportable incidents to undergo third-party safety audits, which is accelerating proactive investments in high-integrity coating systems. Industrial operators are increasingly specifying novolac epoxy coatings for tank linings and containment zones due to their superior resistance to aggressive chemicals, including concentrated sulfuric acid environments. The mandate for passive safeguards such as containment berms and dikes that must withstand prolonged chemical exposure without degradation is further driving the adoption of fiber-reinforced epoxy systems capable of delivering enhanced structural integrity. Transparency requirements have also intensified, with facilities obligated to disclose hazard information publicly, prompting a surge in preventative maintenance programs aimed at avoiding coating failures that could signal operational risk. Industry estimates indicate that more than 1.2 billion dollars is being allocated across North American facilities in 2026 for coating upgrades and asset integrity improvements. In parallel, stricter incident investigation protocols that require root cause analysis of near-miss events are positioning coating performance as a critical compliance parameter, reinforcing the demand for high-solids, low-VOC epoxy formulations with validated long-term chemical resistance profiles.

EU Regulation 2024/3190 Accelerating BPA-Free Epoxy Coatings in Food Contact Applications

The enforcement of Regulation (EU) 2024/3190 is driving a structural transformation in epoxy coatings used in food contact packaging, eliminating reliance on Bisphenol A-based chemistries that have historically dominated the sector. The regulation introduces a stringent detection threshold of 1 microgram per kilogram for BPA, effectively requiring manufacturers to transition to BPA-intent-free resin systems with negligible migration potential. With the transition deadline set for July 20, 2026, manufacturers of coated cans, jar lids, and food-processing equipment are accelerating the adoption of polyester-epoxy hybrids and high-molecular-weight resin systems that comply with evolving food safety standards. This regulatory shift is reinforced by the European Food Safety Authority’s revision of the Tolerable Daily Intake for BPA, which has been reduced by a factor of 20,000, rendering conventional epoxy formulations unsuitable for modern food packaging applications. While limited derogations remain for certain repeat-use industrial equipment, these applications are also subject to stringent Declaration of Conformity requirements and ongoing reporting obligations, necessitating a gradual transition toward safer alternatives by 2027. This convergence of regulatory pressure and consumer safety expectations is driving innovation in non-bisphenol epoxy systems, creating opportunities for advanced resin chemistries that maintain adhesion, flexibility, and chemical resistance without compromising compliance.

Low-Temperature Cure Epoxy Coatings Enabling Year-Round Pipeline Maintenance and Energy Efficiency

The development of low-temperature curing epoxy coatings is unlocking significant operational advantages in infrastructure maintenance, particularly for pipelines and industrial assets exposed to sub-zero environments. Traditional epoxy systems require elevated temperatures to achieve full cure, limiting their applicability in cold climates and leading to costly project delays during winter months. Advanced formulations utilizing phenalkamine curing agents are now capable of achieving full mechanical performance at temperatures as low as minus 10 degrees Celsius, enabling uninterrupted maintenance operations throughout the year. This capability is delivering substantial economic benefits, with pipeline operators able to avoid downtime costs that can exceed 50,000 dollars per day during peak demand periods. In addition to improved scheduling flexibility, these coatings exhibit strong adhesion performance on damp and cold substrates, maintaining pull-off strengths above 15 megapascals even under high humidity conditions where condensation is present. From an energy perspective, low-temperature curing eliminates the need for external heating methods such as induction or infrared systems, reducing operational energy consumption and lowering the carbon footprint of maintenance activities. Performance metrics have also improved significantly, with modern formulations achieving up to 90% cross-linking density within 24 hours at near-freezing temperatures, compared to curing times of up to 10 days for conventional systems. This advancement is positioning low-temperature epoxy coatings as a critical solution for resilient infrastructure management in extreme environments.

Graphene-Enhanced Epoxy Coatings Extending Marine Asset Lifespan and Corrosion Resistance

The incorporation of graphene nanomaterials into epoxy coatings is emerging as a high-impact innovation in marine corrosion protection, particularly for ballast water tanks exposed to aggressive chloride environments. Graphene-enhanced epoxy systems create a highly impermeable barrier by forming a tortuous path that significantly restricts the diffusion of water, oxygen, and corrosive ions through the coating matrix. Technical evaluations conducted in 2026 demonstrate corrosion resistance efficiencies exceeding 99% in chloride-rich conditions, representing a substantial improvement over conventional marine epoxy coatings. The presence of graphene derivatives such as reduced graphene oxide and graphene oxide contributes to a reduction in moisture permeability by up to 40%, mitigating the risk of blistering and coating degradation commonly observed in traditional systems after extended service periods. Additionally, functionalized graphene fillers improve interfacial adhesion between the coating and substrate, reducing the likelihood of delamination under mechanical stress, vibration, and thermal cycling conditions. These performance enhancements translate into extended maintenance intervals, with projected increases in ballast tank service life from approximately 15 years to over 25 years before requiring major recoating. This extension significantly improves return on investment for ship operators by reducing dry-docking frequency and associated maintenance costs. The integration of nanotechnology into epoxy coatings is therefore redefining performance standards in marine and offshore applications, positioning graphene-enhanced systems as a next-generation solution for long-term asset protection.

Two-Component Epoxy Coatings Dominate Market with 71% Share Driven by Ambient Cure and High-Performance Protection

Component Type Analysis: 2K Epoxy Systems Lead with In-Situ Crosslinking and Field Application Versatility

Two-component (2K) epoxy coatings account for a dominant 71.0% share of the global epoxy coatings market in 2025, driven by their ability to deliver high-performance curing under ambient conditions for large-scale industrial and infrastructure applications. These systems combine epoxy resin (Part A) and hardener (Part B) to form a densely cross-linked thermoset network, providing superior adhesion, chemical resistance, and mechanical durability. A key advantage is their adaptability through various hardener chemistries—polyamides for surface tolerance, amine adducts for rapid curing, cycloaliphatic amines for chemical resistance, and phenalkamines for low-temperature environments—making them suitable for marine, oil & gas, pipeline coatings, and industrial flooring applications. Their ability to achieve near factory-grade performance in field conditions positions 2K systems as the backbone of the global protective epoxy coatings market.

Anti-Corrosion Epoxy Coatings Lead Market with 48% Share Driven by Infrastructure Protection and Industrial Demand

Functional Requirement Analysis: Barrier Protection and Three-Coat Systems Drive Epoxy Adoption

Anti-corrosion coatings represent a leading 48.0% share of the epoxy coatings market in 2025, driven by the urgent need to protect steel and concrete infrastructure from corrosion-related degradation. Epoxy coatings serve as the critical intermediate (build) layer in the industry-standard three-coat protective system (zinc-rich primer / epoxy intermediate / polyurethane topcoat), enhancing barrier performance, adhesion, and mechanical durability. These coatings are essential in oil & gas facilities, marine environments, bridges, water treatment plants, and industrial assets, where exposure to moisture, chemicals, and harsh conditions accelerates corrosion. A key sub-segment is epoxy mastics, which provide surface-tolerant application and high solids content, enabling effective coating over minimally prepared substrates in maintenance scenarios. This combination of versatility, durability, and cost-effective protection reinforces anti-corrosion as the primary growth driver in the global epoxy coatings market.

Epoxy Coatings Market Competitive Landscape Driven by Low-VOC Formulations, EV Battery Protection, and High-Performance Industrial Applications

The epoxy coatings market is highly competitive, driven by demand for corrosion-resistant coatings, dielectric protection for EVs, and antimicrobial industrial flooring. Key players compete through low-VOC epoxy technologies, digital coating systems, and advanced applications across automotive, infrastructure, marine, and energy sectors.

PPG Leads Epoxy Coatings Innovation with AI-Driven Formulations and EV Battery Protection

PPG Industries, Inc. dominates the epoxy coatings market with strong positioning in automotive OEM and industrial segments, supported by $15.9 billion in revenue. Over 43% of its portfolio consists of sustainably advantaged low-VOC epoxy coatings. The company is heavily investing in dielectric epoxy coatings for EV battery systems, securing Tier-1 contracts in China and the U.S. Its AI-designed formulations reduce R&D cycles by 30%, enhancing performance attributes such as gloss retention and anti-static properties. PPG’s LINQ™ platform enables real-time monitoring of coating thickness and cure density, reducing waste by 12%. Its integration of digital tools and advanced epoxy systems reinforces market leadership.

AkzoNobel Expands Epoxy Portfolio with Hybrid Powder Coatings and Energy-Efficient Curing

AkzoNobel N.V. is strengthening its epoxy coatings portfolio through innovations in hybrid epoxy-polyester powder coatings showcased in its Futura Collection 2026–2029. Its Resicoat line delivers high-performance electrical insulation for EV batteries, ensuring safety under extreme conditions. The company is advancing laser-based curing technologies in collaboration with IPG Photonics, reducing energy consumption by 25%. AkzoNobel maintains strong profitability with a 14.2% EBITDA margin driven by its Eco+ solutions. Its focus on thin-film coatings and low-energy curing supports sustainability goals. The company’s expertise in corrosion protection and insulation coatings enhances its competitive position.

Sherwin-Williams Drives Epoxy Growth with Industrial Flooring and Infrastructure Coatings

The Sherwin-Williams Company is leveraging its Performance Coatings Group to expand its epoxy coatings presence across industrial and infrastructure applications. The company is benefiting from increased demand for antimicrobial epoxy flooring in food processing and pharmaceutical facilities. Its integration of Suvinil strengthens its footprint in Latin America for epoxy primers. Sherwin-Williams is targeting large-scale infrastructure projects, including metro and airport developments in India, with high-build epoxy rebar coatings. Its vertically integrated supply chain supports consistent delivery across global markets. The company’s focus on durable and compliant epoxy systems drives sustained growth.

Hempel Strengthens Epoxy Coatings with Sustainable Marine Solutions and Cleanroom Applications

Hempel A/S is advancing epoxy coatings through high-performance solutions for marine, offshore wind, and healthcare applications. Its Hempafloor Anti-Microbial 500 provides solvent-free protection for cleanrooms and quarantine facilities. The company reported strong financial performance with an 18.2% EBITDA margin in 2026. Hempel’s Avantguard technology enhances corrosion protection while reducing lifecycle emissions significantly. The company is implementing sustainability-based supplier screening for epoxy raw materials. Its focus on environmentally responsible coatings and high-durability solutions strengthens its market position.

RPM International Expands Epoxy Leadership with Industrial Linings and Seamless Flooring Systems

RPM International Inc., through Carboline and Stonhard, is a major player in high-performance epoxy coatings for industrial applications. Carboline leads in epoxy linings for oil and gas infrastructure, while Stonhard dominates seamless epoxy flooring in data centers. The company is benefiting from increased demand for static-dissipative flooring systems in mission-critical facilities. RPM’s MAP 2025 strategy has optimized supply chains, delivering over $200 million in annual savings. Its epoxy systems are engineered for high strain tolerance, resisting cracking under thermal stress. The company’s diversified portfolio enhances its competitive strength.

3M Advances Epoxy Technology with Fusion Bonded Coatings and Nano-Engineered Applications

3M is a global leader in epoxy coatings, particularly in fusion bonded epoxy (FBE) solutions for pipelines and infrastructure. Its Scotchkote™ products are widely used for corrosion protection in subsea and high-salinity environments. The company is innovating with ultra-thin nano-engineered epoxy coatings for high-frequency electronics and 5G/6G applications. Its Scotchcast™ resins are expanding into renewable energy storage systems, providing moisture-resistant encapsulation. 3M’s liquid epoxy coatings enable field repairs with factory-grade performance. Its strong R&D capabilities position it at the forefront of advanced epoxy coating technologies.

China Epoxy Coatings Market: Infrastructure Megaprojects and Green Transition Driving Global Scale

China remains the largest and most advanced market for epoxy coatings, supported by aggressive decarbonization policies under the 15th Five-Year Plan (2026–2030). Regulatory measures—such as VOC taxation on solvent-based systems—are accelerating a shift toward waterborne and high-solids epoxy coatings.

Infrastructure and industrial demand are key drivers. State-owned shipyards have deployed automated epoxy coating lines for ballast tanks, ensuring 20-year corrosion protection, while high-speed rail projects are adopting graphene-doped epoxy primers with ~30% higher corrosion resistance. The EV sector is also expanding usage, with dielectric epoxy coatings for LFP battery separators and housings. Additionally, semiconductor hubs are driving demand for cleanroom-grade epoxy flooring (>2 million m² projects), reinforcing China’s leadership in both scale and innovation.

United States Epoxy Coatings Market: Infrastructure Refurbishment and Advanced Applications Driving High-Value Growth

The United States market is driven by large-scale infrastructure upgrades and high-performance applications. Under the Infrastructure Investment and Jobs Act (IIJA), demand is surging for penetrating epoxy sealers and overlays in bridge restoration projects targeting 50-year service life.

Innovation is focused on multifunctionality and sustainability. The development of Faraday cage epoxy coatings enables simultaneous corrosion protection and EMI shielding for 5G infrastructure. The CHIPS Act is boosting demand for low-outgassing epoxy flooring in semiconductor fabs, while renewable energy expansion is increasing use of high-build epoxy coatings for offshore wind turbine foundations. Additionally, the introduction of bio-based epoxies (e.g., CNSL-derived) is aligning the market with sustainability goals.

Germany Epoxy Coatings Market: Clean Chemistry and Energy Transition Driving Sustainability Leadership

Germany is leading in eco-compliant epoxy coatings, driven by strict EU regulations and the Energiewende initiative. The shift toward preservative-free waterborne epoxies is aligned with updated EU Biocide Regulations (2026).

The energy transition is a key growth driver. Demand is rising for epoxy-polyurethane hybrids used in hydrogen electrolyzers, ensuring resistance to aggressive environments. Offshore wind maintenance backlogs (€400 million) are also driving procurement of underwater-curing epoxy repair systems. Additionally, innovation in UV-cured epoxy primers is reducing curing time by ~80% and energy use by ~60%, while the shift toward bio-based epoxy resins supports circular economy goals.

India Epoxy Coatings Market: Localization and Infrastructure Boom Driving Rapid Growth

India is transitioning into a regional hub for epoxy coatings, supported by policy incentives and infrastructure expansion. Under Atmanirbhar Bharat, the government has increased ECMS funding to ₹40,000 crore (~$4.8B), promoting domestic production of epoxy-based electronic components and display modules.

Infrastructure growth is a major driver. An 11.1% increase in capital outlay (Budget 2025–26) is boosting demand for epoxy grouts and mortars in metro and high-speed rail projects. Industrial consolidation—such as JSW Paints’ acquisition of AkzoNobel India—is strengthening local production of marine and industrial epoxies. Additionally, EV expansion is driving adoption of epoxy coatings for battery housings, while healthcare regulations are increasing demand for antimicrobial epoxy flooring in pharmaceutical clusters. Emerging R&D in bio-based epoxy resins (lignin, tannin) is also improving sustainability and reducing import dependence.

Saudi Arabia Epoxy Coatings Market: Vision 2030 Megaprojects and Oil & Gas Maintenance Driving Demand

Saudi Arabia is a global hotspot for high-performance epoxy coatings, driven by Vision 2030 megaprojects and energy sector investments. Developments such as NEOM and the Red Sea Project are using UV-stable epoxy coatings and marine-grade liners for coastal infrastructure.

Oil & gas remains a core segment. Saudi Aramco is upgrading 3,000 km of pipelines with internal epoxy coatings to improve flow efficiency and reduce energy costs. Mining expansion is also driving demand for abrasion-resistant epoxy linings, while logistics hubs like Jeddah are increasing adoption of self-leveling epoxy flooring for automated warehouses. Additionally, stricter SABER compliance regulations are phasing out low-quality solvent epoxies, accelerating the shift toward low-VOC, high-performance systems.

South Korea Epoxy Coatings Market: EV Infrastructure and 6G Innovation Driving High-Tech Applications

South Korea is leveraging epoxy chemistry to maintain leadership in high-tech infrastructure and advanced electronics. Government plans to capture 10% of the global EV charger market by 2030 are driving demand for epoxy encapsulants and insulators.

Innovation is focused on next-generation technologies. Investments of $1.5 billion in 6G R&D (2026) are supporting development of low-loss dielectric epoxy films for terahertz communication modules. The EV sector is also driving adoption of thermally conductive epoxy coatings and adhesives for advanced battery architectures. Additionally, maritime industries are deploying low-friction epoxy hull coatings to improve fuel efficiency, while semiconductor clusters are using ESD-safe epoxy flooring to protect ultra-sensitive manufacturing processes.

Brazil Epoxy Coatings Market: Agribusiness Strength and Offshore Energy Driving Regional Growth

Brazil’s epoxy coatings market is driven by agribusiness expansion and offshore oil investments. Under the Harvest Plan (BRL 475 billion), demand is rising for epoxy-coated agricultural machinery and grain storage systems.

Energy and mining sectors are also key drivers. Petrobras is expanding use of glass-flake reinforced epoxy coatings for offshore platforms, ensuring durability in deep-sea conditions. Mining operations in regions like Carajás are adopting heavy-duty epoxy linings to resist chemical and mechanical wear. Additionally, growth in automotive manufacturing is increasing adoption of waterborne epoxy primers, while R&D into soy-based epoxy resins is supporting a more sustainable, locally sourced supply chain.

Epoxy Coatings Market Report Scope

Epoxy Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$65 Billion

|

|

Market Size (2032)

|

$90.9 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Technology (Water-borne Epoxy, Solvent-borne Epoxy, Powder-based Epoxy, Other Technologies), By Substrate (Metal, Concrete and Masonry, Wood, Fiberglass and Composites, Others), By Component Type (One-Component, Two-Component, Three-Component), By End-Use Sector (Building and Construction, Oil and Gas, Power Generation, Marine and Offshore, Automotive and Rail, General Engineering), By Functional Requirement (Anti-Corrosion Coatings, Chemical Resistant Coatings, Abrasion Resistant Coatings, Self-Leveling Coatings, Anti-static, Thermal Insulation), By Price Point (Industrial Grade, Commercial Grade, Premium)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, RPM International Inc., BASF SE, Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Jotun A/S, Hempel A/S, Asian Paints Limited, Sika AG, Berger Paints India Limited, Huntsman Corporation, Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Epoxy Coatings Market Segmentation

By Technology

- Water-borne Epoxy

- Solvent-borne Epoxy

- Powder-based Epoxy

- Other Technologies

By Substrate

- Metal

- Concrete and Masonry

- Wood

- Fiberglass and Composites

- Others

By Component Type

- One-Component

- Two-Component

- Three-Component

By End-Use Sector

- Building and Construction

- Oil and Gas

- Power Generation

- Marine and Offshore

- Automotive and Rail

- General Engineering

By Functional Requirement

- Anti-Corrosion Coatings

- Chemical Resistant Coatings

- Abrasion Resistant Coatings

- Self-Leveling Coatings

- Anti-static

- Thermal Insulation

By Price Point

- Industrial Grade

- Commercial Grade

- Premium

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Epoxy Coatings Market

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- RPM International Inc.

- BASF SE

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Jotun A/S

- Hempel A/S

- Asian Paints Limited

- Sika AG

- Berger Paints India Limited

- Huntsman Corporation

- Wacker Chemie AG

*- List not Exhaustive