Epoxy Powder Coatings Market Growth Driven by EV Battery Applications, Low-Energy Curing Technologies, and Sustainable Powder Systems

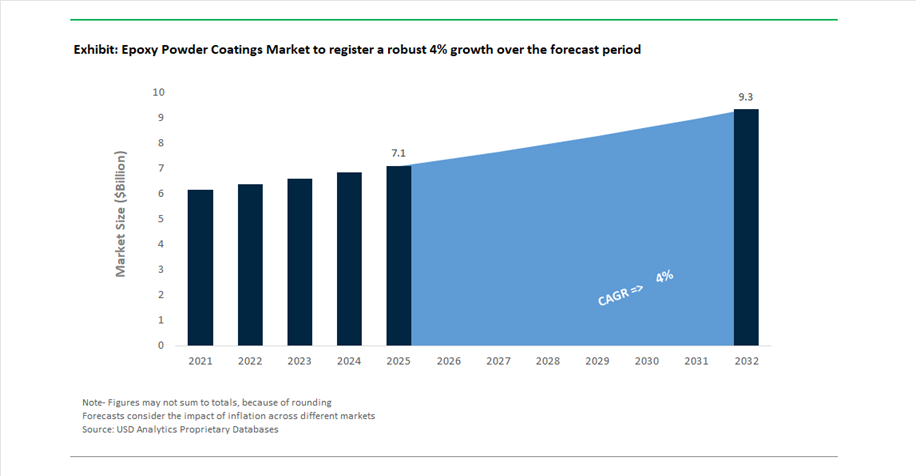

The global Epoxy Powder Coatings Market was valued at USD 7.1 billion in 2025 and is projected to reach USD 9.3 billion by 2032, expanding at a CAGR of 4% over the forecast period. This growth is supported by increasing adoption of solvent-free coating technologies, particularly in industrial, automotive, appliance, and infrastructure applications where durability, corrosion resistance, and environmental compliance are critical.

Epoxy powder coatings are gaining traction due to their zero-VOC emissions, superior adhesion, and excellent edge coverage, making them a preferred alternative to traditional liquid coatings in many applications. A major structural driver is the shift toward sustainable manufacturing processes, where powder coatings eliminate solvent usage and reduce hazardous emissions. Additionally, advancements in curing technologies and formulation chemistry are enabling epoxy powders to be used in more temperature-sensitive and high-throughput production environments.

The rapid expansion of the electric vehicle (EV) ecosystem is also creating new demand avenues. Epoxy powder coatings are increasingly used in battery enclosures, electrical insulation layers, and thermal management systems, where high dielectric strength and heat resistance are essential. Furthermore, the rise of global infrastructure projects and pipeline construction continues to drive demand for fusion-bonded epoxy (FBE) coatings, particularly in oil & gas and water transport systems.

Laser Curing Breakthroughs, Low-Temperature Powder Systems, and EV-Focused Innovation Redefine Market Dynamics

The epoxy powder coatings market is undergoing a phase of rapid technological transformation, driven by next-generation curing technologies, strategic collaborations, and application-specific product innovation. In March 2026, PPG Industries partnered with Whirlpool Corporation and IPG Photonics to accelerate the commercialization of laser-based powder curing systems. This breakthrough technology enables near-instantaneous curing, reducing factory floor space requirements by up to 70% and energy consumption by up to 90%, fundamentally reshaping industrial coating line economics.

Low-temperature curing technologies are also emerging as a critical innovation area. In September 2024, AkzoNobel launched the Interpon D2525 Low-E series, enabling curing at 150°C compared to conventional 180–200°C systems. This innovation allows manufacturers to either reduce energy consumption by up to 20% or increase production line speeds by 25%, addressing one of the primary cost and efficiency challenges in powder coating operations. Complementing this, in November 2025, Axalta Coating Systems received an R&D 100 Award for its fast-cure, low-energy epoxy powder system, driven by advanced catalyst chemistry that accelerates cross-linking at lower temperatures.

Electric vehicle applications are significantly influencing product development. In June 2025, Jotun introduced specialized epoxy powder coatings for EV battery packs, focusing on dielectric insulation and thermal management to enhance safety and mitigate thermal runaway risks. This reflects a broader industry shift toward electrification-driven coating solutions, where performance requirements extend beyond corrosion protection to include electrical and thermal functionalities.

Material innovation is also addressing long-standing mechanical limitations. In January 2026, Tiger Coatings launched FlexCURE technology, enabling coated metal substrates to undergo post-forming processes such as bending and stamping without cracking or delamination. This significantly expands the applicability of epoxy powders in industries requiring complex forming operations.

Strategic standardization and supply chain shifts are further shaping the market. In March 2025, Sherwin-Williams expanded its “Global Core” epoxy powder line, ensuring consistent formulation and performance across regions for multinational infrastructure projects. Meanwhile, in January 2026, Olin Corporation announced the closure of its Brazil epoxy plant as part of its “Beyond250” strategy, signaling a broader consolidation of epoxy resin production into high-efficiency global hubs.

Additionally, PPG Industries reached a milestone in March 2026 by completing its 200th electrostatic powder application in marine dry docking, highlighting the growing adoption of epoxy powders in offshore structures and internal vessel components, where zero-VOC and superior edge coverage provide clear advantages.

EU REACH 2024/3190 Enforcing BPA-Free Epoxy Powder Coatings Across Food Contact and Durable Goods Applications

The implementation of Regulation (EU) 2024/3190 is fundamentally transforming the epoxy powder coatings market by eliminating the use of Bisphenol A-based chemistries in food-contact applications and extending its influence into adjacent industrial sectors. Effective July 20, 2026, the regulation mandates a complete ban on BPA in coatings used for food-contact materials, including epoxy powder coatings applied to metal packaging, appliance interiors, and storage systems. This regulatory shift is compelling manufacturers to transition toward BPA-intent-free polyester-epoxy hybrid systems that meet stringent migration requirements, where residual BPA presence must remain below the detection limit of 1 microgram per kilogram. Industry data indicates that approximately 85% of Tier 1 packaging converters have already transitioned to BPA-free powder formulations ahead of the compliance deadline, ensuring uninterrupted market access within the European Union. The impact of this regulation is extending beyond food-contact applications, with European specifiers increasingly demanding BPA-free coatings for medical equipment, white goods, and interior appliance components to mitigate future regulatory risks and liability exposure. This transition is accelerating innovation in alternative resin chemistries that deliver equivalent adhesion, flexibility, and corrosion resistance while maintaining compliance with evolving safety standards.

China GB/T 41647-2024 Driving TGIC-Free Epoxy Powder Coatings Adoption and Process Efficiency Gains

China’s enforcement of the GB/T 41647-2024 standard is catalyzing a major transition toward TGIC-free epoxy powder coating formulations, prioritizing worker safety, environmental compliance, and export competitiveness. Under the updated regulatory framework, triglycidyl isocyanurate-based powder coatings are subject to stricter hazard classifications and labeling requirements, prompting a rapid industry-wide shift toward hydroxyalkylamide-cured and alternative epoxy-polyester hybrid systems. This transition is particularly pronounced in the architectural and automotive sectors, where adoption of TGIC-free superdurable powder coatings has increased by approximately 40% in response to regulatory and market pressures. Chinese manufacturers are also aligning their production strategies with international standards, achieving near-complete TGIC-free certification across high-performance product lines to maintain export access to the European and North American markets. In addition to regulatory compliance, TGIC-free systems are delivering measurable process efficiency improvements, including a 15% increase in first-pass transfer efficiency, which reduces overspray waste and improves material utilization in high-volume coating operations. Enhanced regulatory enforcement, including increased inspection frequency by the State Administration for Market Regulation, is further accelerating the phase-out of legacy TGIC formulations. These developments are positioning TGIC-free epoxy powder coatings as the new industry standard for safe, efficient, and globally compliant coating solutions.

Low-Temperature Cure Epoxy Powder Coatings Enabling MDF and Heat-Sensitive Substrate Applications

The advancement of low-temperature cure epoxy powder coatings is unlocking new application opportunities beyond traditional metal substrates, particularly in wood-based and heat-sensitive materials such as medium-density fiberboard and engineered composites. By reducing curing temperatures to approximately 130 degrees Celsius, these advanced formulations enable the application of durable powder coatings without causing substrate deformation, outgassing, or surface defects. This capability is significantly expanding the addressable market for powder coatings into furniture manufacturing, cabinetry, and interior architectural components. From an operational standpoint, lowering the curing temperature from conventional levels of around 180 degrees Celsius to 130 degrees Celsius results in energy savings of 25% to 30%, contributing to reduced production costs and lower carbon emissions. Modern low-temperature curing systems are also optimized for high-throughput manufacturing environments, achieving full mechanical cure within 8 to 10 minutes, aligning with industrial production cycle requirements. Adhesion performance has reached high reliability standards, with 2026 field tests demonstrating Grade 0 crosshatch adhesion on pre-treated MDF substrates, ensuring long-term durability. Additionally, powder-coated wood components enable seamless 360-degree surface coverage, eliminating the need for edge banding and reducing moisture-induced swelling by approximately 60% in applications such as kitchen and bathroom furniture. These advantages are driving the adoption of low-temperature epoxy powder coatings in non-metal substrate markets.

Antimicrobial Epoxy Powder Coatings Expanding in Healthcare and Food Processing Equipment Markets

The integration of antimicrobial functionality into epoxy powder coatings is creating a high-value growth segment driven by increasing hygiene standards across healthcare, food processing, and public infrastructure environments. Advanced formulations incorporating silver ions and copper nanoparticles are delivering active biocidal performance, achieving pathogen reduction rates of up to 99.9% against microorganisms such as MRSA and E. coli within two hours of contact, as validated by ISO 22196 testing protocols. Unlike conventional liquid antimicrobial coatings, epoxy powder systems offer superior durability, maintaining their antimicrobial efficacy even after exposure to more than 5,000 cycles of aggressive cleaning with hospital-grade disinfectants. This resilience is critical in high-contact environments where frequent sanitation is required. Market adoption is accelerating, with approximately 45% of new healthcare furniture tenders in Europe and North America specifying antimicrobial powder coatings as a standard requirement following heightened post-pandemic hygiene regulations. Additionally, advancements in non-leaching antimicrobial technologies ensure that active agents remain embedded within the coating matrix, providing long-term protection without environmental contamination or regulatory compliance issues. These coatings are also being designed to meet stringent food safety standards, enabling their use in food processing equipment and surfaces that require both corrosion protection and microbial control. This convergence of durability, safety, and active protection is positioning antimicrobial epoxy powder coatings as a critical solution in hygiene-sensitive applications.

Electrostatic Spray Deposition Dominates Epoxy Powder Coatings Market with 78% Share Driven by High Transfer Efficiency and Automation

Coating Method Analysis: Electrostatic Powder Coating Leads with Near-Zero Waste and High-Throughput Manufacturing

Electrostatic Spray Deposition (ESD) accounts for a commanding 78.0% share of the epoxy powder coatings market in 2025, driven by its unmatched material efficiency, automation compatibility, and consistent coating quality. This method uses high-voltage electrostatic charging (corona or tribo guns) to attract powder particles to grounded metal substrates, ensuring uniform coverage even on complex geometries. A key advantage is its >95% transfer efficiency, where overspray powder is recovered and recycled, resulting in near-zero coating waste—a significant improvement over liquid coatings with 30–50% losses. ESD systems are increasingly integrated with robotic arms and automated reciprocators, enabling precise control of film thickness (±5 microns) and repeatable performance in high-volume industries such as automotive components, appliances, and industrial equipment. This combination of cost efficiency, sustainability, and production scalability solidifies ESD as the leading technology in the global epoxy powder coatings market.

Standard Color Epoxy Powder Coatings Lead with 62% Share Driven by Industrial Volume Demand and Cost Efficiency

Finish Analysis: Black, White, and Gray Coatings Dominate Functional Industrial Applications

Standard colors account for a dominant 62.0% share of the epoxy powder coatings market in 2025, reflecting their widespread use in high-volume, function-driven industrial applications. Common shades such as black, white, gray (RAL 7035/7040), and safety colors are the default choice for applications where corrosion protection, chemical resistance, and dielectric insulation are more critical than aesthetics. These coatings are extensively used in automotive chassis components, electrical enclosures, pipelines (FBE coatings), and epoxy-coated rebar, where performance and durability take precedence. A major driver of this segment is economies of scale, as standard colors are produced in large batches, ensuring lower costs, consistent quality, and immediate availability for just-in-time manufacturing. In contrast, customized and specialty finishes command higher prices but represent a smaller share, reinforcing standard colors as the backbone of the global epoxy powder coatings market.

Epoxy Powder Coatings Market Competitive Landscape Driven by Low-Bake Technologies, EV Battery Insulation, and Sustainable Powder Innovations

The epoxy powder coatings market is intensifying with innovations in low-temperature curing, dielectric coatings for EV batteries, and sustainable resin systems. Key players compete through digital coating platforms, circular economy initiatives, and high-performance corrosion protection across automotive, industrial, and infrastructure applications.

PPG Accelerates Epoxy Powder Innovation with Laser Curing and EV Dielectric Technologies

PPG Industries, Inc. is leading epoxy powder coatings innovation through its laser-based curing collaboration with IPG Photonics and Whirlpool, enabling instant curing and reducing energy consumption by 40%. Its Envirocron® portfolio includes PRIMERON Optimal zinc epoxy primers with up to 85% transfer efficiency, ensuring superior corrosion protection. The company is scaling dielectric powder coatings for EV battery safety, preventing thermal runaway in high-voltage systems. PPG’s low-bake powder coatings reduce oven temperatures by 20°C to 40°C, improving sustainability and throughput by 25%. Integration of the PPG LINQ™ platform enables precise coating application and reduced material waste. Its strong focus on energy-efficient and high-performance coatings reinforces market leadership.

AkzoNobel Expands Epoxy Powder Leadership with Axalta Merger and Circular Coatings Strategy

AkzoNobel N.V., through its Interpon brand, is strengthening its epoxy powder coatings portfolio via its strategic merger with Axalta, targeting $600 million in synergies. The company raised €1.1 billion to invest in smart surface technologies and sustainable resin systems. Its “Rhythm of Blues” collection introduces advanced epoxy-polyester hybrids for architectural applications. AkzoNobel is transitioning toward full circularity, eliminating heavy-metal catalysts from curing agents. Operating in over 150 countries, it is developing “coatings on command” technologies for recyclable surfaces. Its sustainability-driven innovation and global scale enhance its competitive positioning.

Sherwin-Williams Strengthens Epoxy Powder Portfolio with Recycled Resins and Rapid Customization

The Sherwin-Williams Company is expanding its epoxy powder coatings presence through strategic acquisitions in Europe and digital innovation. Its Powdura® ECO line incorporates up to 25% recycled plastic, aligning with LEED-certified construction demand. The company introduced the Colour Express Powder Programme, enabling custom epoxy powders to be delivered within 48 hours. Sherwin-Williams benefits from strong demand in heavy equipment and material handling industries. Its 5,000+ store network and DesignHouse services provide technical support for complex industrial applications. The company’s focus on sustainability and rapid customization strengthens its market position.

Axalta Advances Epoxy Powder Coatings with Digital Color Systems and Bio-Attributed Resins

Axalta Coating Systems is driving growth in epoxy powder coatings through its “A-Plan 2026,” achieving strong cash flow and operational efficiency. Its MyColor digital platform reduces approval times for custom coatings from 26 weeks to 4 weeks. Axalta is integrating NextJet™ technology with robotics to enable overspray-free powder application, minimizing material waste. The company is developing bio-attributed epoxy resins using forestry waste, supporting sustainability goals. Its acquisition of CoverFlexx expands its presence in protective and refinish coatings. Axalta’s innovation in digital coatings and sustainable materials strengthens its competitive edge.

Jotun Leads Epoxy Powder Applications in EV Batteries and Harsh Industrial Environments

Jotun A/S is strengthening its epoxy powder coatings portfolio with specialized solutions for EV batteries and energy storage systems. Its EV Battery Solutions provide insulation and durability under repeated charge cycles. The company is partnering with Chinese manufacturers to deliver high-performance coatings with C5VH corrosion resistance. Jotun’s Jotacote Universal S120 remains a benchmark for marine and offshore epoxy primers. Its powder-on-powder technology reduces process time by 30% in industrial applications. The company’s focus on durability and sustainability enhances its leadership in harsh environment coatings.

TIGER Coatings Drives Epoxy Powder Innovation with Digital Finishes and Smart Surface Textures

TIGER Coatings GmbH & Co. KG is advancing epoxy powder coatings through design-led innovation and digital tools. Its TRANSFORMATION 2026 collection introduces advanced finishes for smart infrastructure and consumer applications. The TIGITAL® platform enables high-definition printing on heat-sensitive substrates using epoxy powder technology. Its Series 67 coatings deliver superior durability for smart-city infrastructure projects. TIGER is integrating tactile textures to enhance user experience in premium products. Its Tigerator AR-based tool enables real-time visualization of finishes, supporting faster decision-making. The company’s focus on aesthetics and functionality strengthens its niche leadership.

China Epoxy Powder Coatings Market: EV Battery Insulation and Zero-VOC Manufacturing Driving Global Dominance

China has positioned itself as the global leader in epoxy powder coatings, driven by its dominance in EV manufacturing and strict environmental mandates. Under the 15th Five-Year Plan, industries are rapidly transitioning from liquid coatings to zero-VOC epoxy powder systems, enabling large-scale decarbonization.

The EV sector is the primary growth engine. Strategic collaborations—such as Jotun’s partnerships with Chinese battery manufacturers—are accelerating deployment of dielectric epoxy powder coatings that prevent thermal runaway in lithium-ion batteries. Supply chain integration is also strengthening, with BASF–KHUA partnerships stabilizing NPG feedstock availability for epoxy-polyester hybrids. Additionally, large infrastructure initiatives like the Jiangsu Coating Corridor ($1.2B investment) are boosting production of fusion-bonded epoxy (FBE) coatings for pipelines, while innovations such as IR-cured powders are reducing curing time by ~22%, enhancing manufacturing efficiency.

United States Epoxy Powder Coatings Market: Infrastructure Renewal and Defense Applications Driving High-Performance Demand

The U.S. market is evolving through federal infrastructure investments and defense procurement, making epoxy powder coatings the preferred choice for durability and compliance. Updated EPA “Safer Choice” guidelines (2026) are reinforcing adoption of low-VOC powder coatings in publicly funded projects.

Infrastructure modernization is a key driver. Federal funding is boosting demand for fusion-bonded epoxy coatings in municipal water systems and bridge structures. Innovation is also strong, with the launch of PPG’s Envirocron Extreme Protection Edge Plus, a one-coat system offering superior edge coverage for industrial components. Additionally, the CHIPS Act is driving demand for ESD-safe epoxy powders in semiconductor fabs, while defense applications are expanding use of Mil-Spec epoxy coatings for military vehicles, emphasizing chemical resistance and durability.

India Epoxy Powder Coatings Market: Localization and Industrial Expansion Driving Rapid Growth

India is experiencing the fastest growth in epoxy powder coatings, supported by government incentives and manufacturing expansion. Under the PLI scheme (~₹6,200 crore allocation), the country is targeting full self-sufficiency in advanced coatings by 2028.

Industrial demand is rising across multiple sectors. The establishment of Sherwin-Williams’ Pune facility (2025) is strengthening domestic supply for automotive and appliance coatings. Infrastructure initiatives under Gati Shakti are driving adoption of anti-corrosive and anti-graffiti epoxy powders in railway and metro systems, including Vande Bharat trains. Additionally, innovation is accelerating with the launch of the Bengaluru Coating Lab (2026), focusing on low-temperature cure (LTC) powders for heat-sensitive substrates. The renewable energy sector is also contributing, with growing demand for epoxy-coated energy storage systems (ESS) in solar and wind projects.

Germany Epoxy Powder Coatings Market: Circular Economy and Precision Engineering Driving Sustainability Leadership

Germany is leading the transition toward a circular economy in epoxy powder coatings, where closed-loop recycling and high material reuse rates (~99%) are becoming industry standards. Government subsidies are encouraging manufacturers to adopt powder-on-powder (POP) systems and recycling technologies.

Technological innovation is focused on sustainability and efficiency. The commercialization of low-temperature cure powders (<120°C) enables coating of heat-sensitive materials such as MDF and aerospace composites. Additionally, UV-cured epoxy powders are reducing energy consumption and enabling applications in medical devices. Regulatory pressure under REACH (2026 updates) is also driving adoption of bio-based epoxy resins, while AI-driven robotic systems are improving coating efficiency and reducing waste by ~15%.

Italy Epoxy Powder Coatings Market: Premium Aesthetics and Automotive Innovation Driving Niche Leadership

Italy has established itself as a hub for high-end epoxy powder coatings, particularly in architectural and automotive applications. Investments such as AkzoNobel’s €21 million expansion (Como, 2025) are boosting production of premium epoxy-polyester blends.

Innovation is centered on aesthetics and functionality. Italian manufacturers are developing thermochromic and photochromic coatings for luxury automotive interiors and furniture. The shift toward powder-based epoxy primers in automotive chassis components is improving impact resistance, while Eco-Design regulations (2026) are accelerating the transition from liquid to powder systems. Additionally, specialized non-yellowing epoxy powders are being used in historic restoration projects, reinforcing Italy’s leadership in premium coatings.

Japan Epoxy Powder Coatings Market: Ultra-Thin Precision and Electronics Integration Driving Advanced Applications

Japan leads in ultra-thin and high-precision epoxy powder coatings, particularly for electronics and miniaturized components. Advances in application technology now enable sub-15 micron coating thickness, critical for microelectronics and high-frequency devices.

Material purity and innovation are key strengths. Japanese suppliers dominate production of high-purity epoxy resins for telecommunications and semiconductor applications. Growth in robotics and wearable devices is driving demand for conductive epoxy powders for shielding and protection. Additionally, innovations such as plasma-pretreated powder coatings are improving adhesion by ~30% on low-energy surfaces. Applications are expanding into AI server cooling plates, where epoxy powders provide both thermal conductivity and electrical insulation, reinforcing Japan’s leadership in advanced materials.

Epoxy Powder Coatings Market Report Scope

Epoxy Powder Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.1 Billion

|

|

Market Size (2032)

|

$9.3 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Chemistry (Pure Epoxy, Epoxy-Polyester Hybrid, Fusion-Bonded Epoxy, Specialty Epoxy Powders), By Coating Method (Electrostatic Spray Deposition, Fluidized Bed Coating, Electrostatic Fluidized Bed Process, Flame Spraying), By Substrate (Metal, Medium-Density Fiberboard, Engineered Wood, Plastics), By Application (Pipes and Fittings, Reinforcing Bar, Coil Coating, Fasteners and Small Parts, Structural Steel), By End-Use Industry (Building and Construction, Automotive and Transportation, Oil and Gas, Appliances and Furniture, Electrical and Electronics, General Industrial), By Functional Characteristic (Corrosion Protection, Chemical and Solvent Resistance, Electrical Insulation, Decorative and Aesthetic, Abrasion and Impact Resistance), By Color and Finish (Standard Colors, Customized, Textured and Metallic Finishes)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Jotun A/S, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Tiger Coatings GmbH & Co. KG, BASF SE, RPM International Inc., Asian Paints Limited, Sika AG, IFS Coatings, Inc., 3M Company, Hempel A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Epoxy Powder Coatings Market Segmentation

By Chemistry

- Pure Epoxy

- Epoxy-Polyester Hybrid

- Fusion-Bonded Epoxy

- Specialty Epoxy Powders

By Coating Method

- Electrostatic Spray Deposition

- Fluidized Bed Coating

- Electrostatic Fluidized Bed Process

- Flame Spraying

By Substrate

- Metal

- Medium-Density Fiberboard

- Engineered Wood

- Plastics

By Application

- Pipes and Fittings

- Reinforcing Bar

- Coil Coating

- Fasteners and Small Parts

- Structural Steel

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Oil and Gas

- Appliances and Furniture

- Electrical and Electronics

- General Industrial

By Functional Characteristic

- Corrosion Protection

- Chemical and Solvent Resistance

- Electrical Insulation

- Decorative and Aesthetic

- Abrasion and Impact Resistance

By Color and Finish

- Standard Colors

- Customized

- Textured and Metallic Finishes

Leading Countries in the Industry

• North America (United States, Canada, Mexico)

• Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

• Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

• South and Central America (Brazil, Argentina, Rest of SCA)

• Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Epoxy Powder Coatings Market

- AkzoNobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Jotun A/S

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Tiger Coatings GmbH & Co. KG

- BASF SE

- RPM International Inc.

- Asian Paints Limited

- Sika AG

- IFS Coatings, Inc.

- 3M Company

- Hempel A/S

*- List not Exhaustive