Epoxy Primers Market Expansion Driven by Infrastructure Durability Needs, Marine Coatings Demand, and Low-Emission Primer Technologies

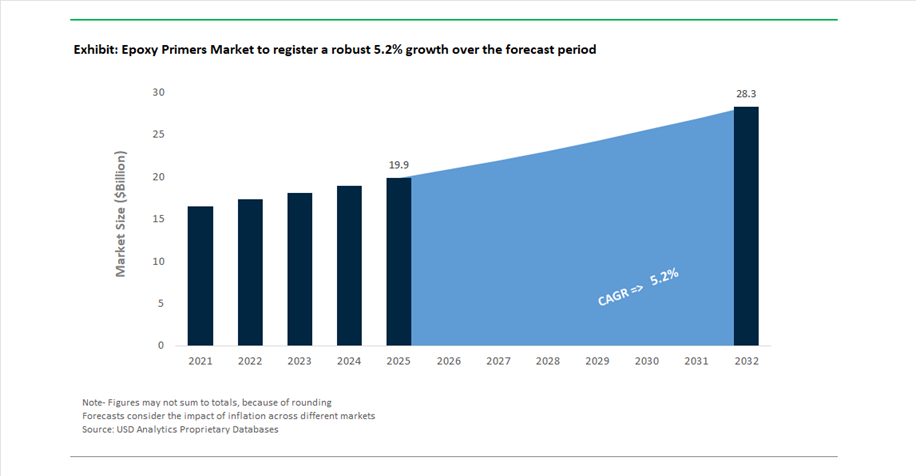

The global Epoxy Primers Market was valued at USD 19.9 billion in 2025 and is projected to grow at a CAGR of 5.2% between 2025 and 2032, reaching USD 28.4 billion by 2032. This growth is primarily driven by the increasing demand for high-performance corrosion protection systems across infrastructure, marine, automotive, and industrial applications. Epoxy primers serve as the foundational layer in coating systems, delivering adhesion, barrier protection, and chemical resistance, particularly in aggressive environments such as offshore structures, pipelines, and heavy machinery.

A key structural growth driver is the surge in global infrastructure investments and energy projects, including offshore wind farms, shipbuilding, and oil & gas facilities. These applications require high-build, long-life primer systems capable of withstanding moisture, salt exposure, and chemical corrosion. Additionally, the expansion of automotive production and repair ecosystems is boosting demand for fast-curing, energy-efficient epoxy primers, especially in collision repair and OEM manufacturing environments.

Sustainability and regulatory compliance are increasingly influencing product development. Manufacturers are focusing on low-VOC, high-solids, and powder-based epoxy primers that reduce environmental impact while maintaining superior protective performance. Innovations such as zinc-rich primers with higher transfer efficiency and low-temperature curing systems are enabling reduced material wastage and lower energy consumption. Furthermore, the push toward global standardization of coating systems is simplifying procurement for multinational engineering and construction projects.

Global Standardization, Low-Energy Primer Systems, and Marine Contract Wins Reshape Competitive Landscape

The epoxy primers market is undergoing a strategic transformation driven by product standardization, sustainability-focused innovation, and large-scale industrial contracts. In March 2025, Sherwin-Williams expanded its Global Core epoxy primer portfolio, including Macropoxy® 2600 and 4600 systems. These products are designed with a “same chemistry, same data sheet” approach, enabling global EPC firms to specify a single primer across multi-regional projects without the need for revalidation, significantly improving procurement efficiency and project consistency.

Sustainability-driven product innovation is accelerating. In August 2024, PPG Industries launched PRIMERON™ Optimal, an advanced zinc epoxy powder primer offering 85% transfer efficiency and compliance with ISO C5 corrosion protection standards. This development addresses the growing need for coatings that perform in extreme industrial environments while minimizing waste and emissions. Similarly, Hempel introduced its “Accelerate to Win” strategy in January 2026, committing to allocate 20% of its R&D budget toward low-emission epoxy technologies, particularly targeting energy and infrastructure sectors.

Technological advancements are also improving performance in challenging environments. In February 2026, Jotun launched hybrid epoxy primers with enhanced barrier and zinc-rich formulations, designed to maintain adhesion and integrity in high-humidity and equatorial climates, where conventional systems often fail. This innovation is particularly relevant for offshore platforms and tropical infrastructure projects.

Strategic partnerships and contracts continue to reinforce market positioning. In March 2026, AkzoNobel secured a major marine coatings contract for new ferry constructions, emphasizing high-solids, low-VOC epoxy primer systems that reduce coating layers while meeting IMO environmental standards. Additionally, in January 2025, Axalta Coating Systems renewed its agreement with the BMW Group, supplying fast-cure, low-energy epoxy primers for global refinish networks, enabling reduced curing temperatures and improved operational efficiency in automotive repair facilities.

Emerging markets are also playing a critical role in demand expansion. In April 2025, Kansai Nerolac Paints strengthened its industrial coatings focus under new leadership, expanding capacity for epoxy primers to support India’s automotive and heavy machinery manufacturing growth under the “Make in India” initiative.

BPA Regulatory Ban Accelerating Shift Toward Food-Safe Epoxy Primer Alternatives

The epoxy primers market is undergoing a structural transformation as regulatory pressure intensifies around the elimination of Bisphenol A (BPA) in food-contact applications. The enforcement of the European Commission Regulation (EU) 2024/3190, has mandated a complete phase-out of BPA, its salts, and hazardous derivatives in epoxy-based coatings used for metal packaging. This includes internal primers and varnishes applied to food and beverage cans, creating a large-scale reformulation challenge for coating manufacturers. While a transition window allows non-compliant materials to remain in circulation until July 20, 2026, industry participants are rapidly shifting toward BPA-free epoxy primer technologies to ensure long-term compliance.

This regulatory action follows a significant safety reassessment by the European Food Safety Authority (EFSA), which reduced the tolerable daily intake of BPA by a factor of 20,000, fundamentally altering risk thresholds for food-contact materials. As a result, traditional “BPA-NI” formulations are no longer sufficient, driving innovation in polyester-based and acrylic-based primers. The transition is particularly impactful given the scale of the global beverage can market, exceeding 100 billion units annually. Parallel developments in the United States, where regulatory updates are anticipated by 2026, are prompting multinational beverage brands and coating suppliers to proactively audit supply chains, accelerating global alignment toward BPA-free epoxy primer systems.

Offshore Wind Expansion Exposes Limitations of Epoxy Primers Under Cathodic Protection Systems

The rapid deployment of offshore wind infrastructure is revealing critical performance limitations in conventional epoxy primer systems, particularly in submerged environments where cathodic protection (CP) is employed. Research findings published on ResearchGate (April 2026) highlight the growing issue of Cathodic Disbondment (CD), where alkaline conditions generated by sacrificial anodes compromise primer adhesion. This phenomenon is leading to accelerated corrosion rates, in some cases exceeding design expectations by 25% to 40%, posing a significant risk to long-term asset integrity in offshore wind farms.

Operational case studies further underscore the challenge, particularly for large-scale monopile foundations supporting turbines in deeper waters. For example, a 5 MW offshore wind structure at 20-meter depth demonstrated that traditional high-build epoxy primers are unable to withstand the elevated current densities required for modern installations. This has driven demand for next-generation primers compliant with ISO 12944-9 standards, which require less than 10 mm of disbondment under accelerated testing conditions. With a substantial portion of offshore assets expected to reach mid-life by 2030, the industry is witnessing a surge in demand for specialized subsea-applied maintenance epoxy coatings, as highlighted in innovation programs supported by Innovate UK.

Low-Temperature Curing Epoxy Primers Unlock Year-Round Infrastructure Coating Efficiency

A significant opportunity in the epoxy primers market lies in the development of low-temperature curing systems that enable application in sub-zero environments. Infrastructure projects, particularly pipelines and bridges in cold climates, often face delays due to the temperature sensitivity of traditional epoxy primers, which typically require curing conditions above 10°C. Leading coating manufacturers such as Hempel A/S and Jotun Group have capitalized on this gap by introducing advanced epoxy primer formulations capable of curing at temperatures as low as -10°C (14°F), contributing to strong financial performance in 2025.

From an operational standpoint, these low-temperature epoxy primers significantly enhance pipeline construction efficiency by eliminating the need for induction heating during girth weld coating. According to technical sessions conducted by the Association for Materials Protection and Performance (AMPP) in 2025, this can reduce on-site energy consumption by up to 15%. In bridge infrastructure maintenance, particularly across Northern Europe and the UK, the ability to conduct coating operations year-round is critical for reducing maintenance backlogs and meeting net-zero infrastructure targets. These performance advantages position low-temperature curing epoxy primers as a high-growth segment within protective coatings.

Edge-Retentive Epoxy Primers Enhance Protection of Laser-Cut Steel in Heavy Equipment and Automotive Applications

The increasing adoption of laser-cut steel components in automotive and heavy equipment manufacturing is creating demand for specialized edge-retentive (ER) epoxy primers. Laser cutting produces sharp edges that are prone to insufficient coating coverage due to the “pull-back” effect during curing, resulting in localized corrosion initiation points. Industry standards outlined by Association for Materials Protection and Performance (AMPP) emphasize that high-performance ER primers must retain at least 70% of their dry film thickness on sharp 90-degree edges to ensure long-term corrosion resistance.

In response, coating leaders such as PPG Industries, Inc. and Axalta Coating Systems have introduced high-solids, chromate-free epoxy primer solutions tailored for electrostatic and airless spray applications. These systems comply with stringent VOC limits below 540 g/l while delivering superior wrap-around coverage and adhesion on complex geometries. Performance validation from CORCON-2025 technical discussions indicates that ER epoxy primers can extend time-to-first-maintenance by 5 to 7 years in highly corrosive C5 environments. This value proposition is particularly compelling for OEMs such as Caterpillar Inc. and Komatsu Ltd., where durability and lifecycle cost reduction are critical competitive factors.

Two-Component Epoxy Primers Dominate Market with 76% Share Driven by Ambient Cure and High Adhesion Performance

Product Type Analysis: 2K Epoxy Primers Lead with Cross-Link Density and Field Application Versatility

Two-component (2K) epoxy primers account for a dominant 76.0% share of the epoxy primers market in 2025, driven by their ability to deliver high-performance curing at ambient or low-bake temperatures for large-scale industrial and infrastructure applications. These systems—comprising epoxy resin and hardener components—form a dense thermoset polymer network, ensuring exceptional adhesion, chemical resistance, and moisture barrier protection. Their versatility is enhanced through different hardener chemistries, including polyamide systems for surface tolerance, amine adducts for rapid curing, and zinc-rich formulations for cathodic protection, making them suitable for bridges, pipelines, offshore platforms, and industrial equipment. Critically, 2K epoxy primers provide near-factory-level performance in field-applied conditions, reinforcing their dominance in the global industrial and protective coatings market.

Steel Priming Leads Epoxy Primers Market with 72% Share Driven by Global Infrastructure and Corrosion Protection Demand

Substrate Analysis: Carbon Steel Protection Drives High-Volume Epoxy Primer Consumption

Steel priming represents a leading 72.0% share of the epoxy primers market in 2025, reflecting the extensive global use of carbon steel in infrastructure, construction, and industrial manufacturing. Steel’s inherent susceptibility to oxidation and corrosion—especially in environments exposed to moisture, chlorides, and industrial pollutants—necessitates robust protective coatings. Epoxy primers are specifically formulated to bond with abrasive blast-cleaned steel surfaces (SSPC-SP10 / Sa 2½), creating a strong mechanical and chemical anchor for multi-layer coating systems. A key driver within this segment is the widespread adoption of zinc-rich epoxy primers, which provide sacrificial cathodic protection by corroding preferentially to the steel substrate, ensuring long-term durability even in harsh environments such as marine, offshore, and bridge structures. These factors position steel priming as the cornerstone of the global epoxy primer coatings market.

Epoxy Primers Market Competitive Landscape Driven by High-Solids Formulations, EV Insulation, and Advanced Corrosion Protection

The epoxy primers market is highly competitive, driven by demand for corrosion-resistant coatings, fast-curing systems, and dielectric protection for EV and aerospace applications. Key players focus on low-VOC formulations, digital coating integration, and high-performance primers for infrastructure, marine, and automotive sectors.

PPG Accelerates Epoxy Primer Performance with Fast-Curing Systems and EV Dielectric Coatings

PPG Industries, Inc. is advancing epoxy primer technologies with the launch of SIGMAFAST™ 278, a high-solids zinc-phosphate primer enabling faster overcoating and reducing infrastructure downtime by up to 25%. The company is integrating AI-driven vapor plume control into aerospace-grade epoxy primers to enhance coating precision. Its Envirocron® dielectric powder primers are widely adopted for EV battery enclosures, offering 1,000V+ insulation resistance. PPG continues to expand sustainably advantaged coatings, which accounted for 44% of 2025 sales. Its strong vertical integration supports rapid innovation and scalability across global markets. The company’s focus on high-performance and low-VOC epoxy primers reinforces its leadership.

AkzoNobel Strengthens Epoxy Primer Leadership with Laser Curing and Interpon Redox Portfolio

AkzoNobel N.V., through its Interpon and International® brands, is strengthening its epoxy primer portfolio with advanced corrosion protection technologies. The company’s Interpon Redox range remains a benchmark for multi-layer corrosion systems in heavy-duty machinery. Its collaboration with IPG Photonics introduces laser-curing technology, reducing energy consumption by up to 30%. AkzoNobel is nearing completion of its merger with Axalta, targeting $600 million in synergies. The company achieved a 14.2% EBITDA margin through operational efficiency and pricing strategies. Its focus on energy-efficient curing and high-performance primers enhances its competitive positioning.

Sherwin-Williams Expands Epoxy Primer Capabilities with Aerospace Systems and Digital Tools

The Sherwin-Williams Company is expanding its epoxy primer portfolio through innovation and strategic acquisitions. Its chrome-free epoxy primer systems provide advanced corrosion resistance for aerospace applications. The company introduced the Aircraft Color Visualizer, integrating primer and topcoat selection to reduce OEM design cycles by 15%. Sherwin-Williams benefits from strong logistical capabilities through its 5,000+ store network, enabling just-in-time delivery. Its acquisitions in Latin America and Europe strengthen its global epoxy footprint. The company’s focus on digital integration and high-performance coatings drives sustained growth.

Axalta Advances Epoxy Primer Market with Waterborne Electrocoat Systems and Sustainable Resins

Axalta Coating Systems is strengthening its position in epoxy primers with its AquaEC™ electrocoat series, widely adopted in Asia’s automotive manufacturing sector. The company achieved strong financial performance with a 22.0% EBITDA margin and $5.12 billion in sales. Its acquisition of CoverFlexx enhances its presence in automotive refinish coatings. Axalta is investing in bio-attributed epoxy resins derived from forestry waste to reduce carbon emissions. The company’s focus on waterborne technologies aligns with regulatory trends in automotive coatings. Its innovation in sustainable and high-performance primers strengthens its market position.

Jotun Expands Epoxy Primer Applications in Marine and Infrastructure with Low-VOC Solutions

Jotun A/S is a key player in epoxy primers, particularly in marine and offshore applications. Its Penguard HB primer delivers high-build corrosion protection for C5 environments such as offshore wind and oil platforms. The company introduced Jotacote Universal S120, a solvent-free epoxy primer reducing VOC emissions by up to 90%. Jotun is experiencing strong growth in Asia-Pacific, driven by infrastructure investments. Its coatings perform exceptionally in immersion environments, including water treatment and power plants. The company’s focus on durability and sustainability strengthens its competitive edge.

BASF Drives Epoxy Primer Innovation with Circular Feedstocks and High-Performance Electrocoat Systems

BASF SE is advancing epoxy primer technologies through its CathoGuard® 800 series, offering superior edge protection and eliminating tin-based catalysts. The company is expanding production capacity through its Zhanjiang Verbund site to serve high-growth EV and electronics markets. BASF is integrating recycled feedstocks into epoxy resin production through its ChemCycling™ process. Its focus on circular economy solutions aligns with global sustainability goals. The company forecasts strong EBITDA growth, supported by its Surface Technologies division. BASF’s innovation in sustainable and high-performance primers strengthens its role as a key industry enabler.

United States Epoxy Primers Market: Aerospace Innovation, Regulatory Compliance, and Infrastructure-Led Demand

The United States epoxy primers market is anchored by its leadership in aerospace coatings, defense-grade corrosion protection, and environmentally compliant epoxy technologies. In early 2026, Sherwin-Williams expanded the global rollout of its CM0483800 Next Gen Chrome-Free Epoxy Primer, a water-based, hexavalent chromium-free solution engineered for military and commercial aviation corrosion resistance. This innovation aligns with tightening environmental policies, particularly the Environmental Protection Agency 2025 NESHAP standards, which are accelerating the transition toward low-VOC and waterborne epoxy primer systems across industrial facilities.

Federal investments under the Infrastructure Investment and Jobs Act (IIJA) are significantly boosting demand for high-build epoxy primers in bridge rehabilitation, port infrastructure, and coastal steel protection, especially in high-salinity environments. Meanwhile, PPG Industries finalized a $300 million expansion across North America (2024–2025), enhancing production capacity for industrial epoxy primers used in heavy machinery and structural applications. Growth in semiconductor fabrication, supported by the CHIPS Act, is also increasing demand for low-outgassing epoxy primers for cleanroom coatings, while offshore wind projects along the Atlantic coast are driving the adoption of subsea-grade epoxy primers resistant to cathodic delamination. The U.S. market continues to set benchmarks in high-performance epoxy coatings, regulatory compliance, and advanced manufacturing integration.

China Epoxy Primers Market: Offshore Wind Expansion, VOC Regulations, and Urban Renewal Projects

The China epoxy primers market is transitioning toward sustainable, high-performance coatings, supported by strong policy frameworks and industrial expansion in maritime and energy sectors. The China Classification Society updated its 2025 guidelines, mandating advanced anti-corrosive epoxy primers for offshore wind structures, particularly monopiles and transition components exposed to aggressive saline conditions. This aligns with China’s continued dominance in offshore wind installations, reinforcing demand for marine-grade epoxy primers with long-term durability.

Environmental regulations such as the National Air Pollution Prevention and Control Action Plan are imposing strict VOC limits, accelerating the shift toward solvent-free and waterborne epoxy primer technologies across coastal manufacturing hubs. Additionally, directives from the Ministry of Industry and Information Technology promoting “Industrial Green Development” are incentivizing the adoption of bio-based epoxy resins through tax credits, strengthening sustainability integration. Increased shipyard maintenance cycles in Shanghai and Ningbo are driving demand for surface-tolerant epoxy primers suitable for high-humidity conditions, while rapid EV infrastructure expansion is boosting applications in protective coatings for steel charging stations. Urban renewal initiatives in Tier-1 cities are further accelerating the use of moisture-resistant epoxy primers for concrete rehabilitation, positioning China as a key player in green epoxy coatings and large-scale infrastructure protection.

India Epoxy Primers Market: Infrastructure Megaprojects, Automotive Scale-Up, and Renewable Energy Demand

The India epoxy primers market is experiencing robust expansion driven by government-backed infrastructure programs, refinery upgrades, and automotive manufacturing growth. The Sagarmala Program is catalyzing large-scale demand for marine-grade epoxy primers used in port modernization, cargo terminals, and logistics infrastructure, while refinery expansions led by Indian Oil Corporation are increasing the use of chemical-resistant epoxy primers for pipelines and storage tanks.

Urban transit development is another major driver, with metro expansions in Mumbai and Bengaluru standardizing anti-carbonation epoxy primers for reinforced concrete protection, enhancing durability and lifecycle performance. The Production Linked Incentive (PLI) scheme has significantly boosted domestic automotive production, increasing the adoption of electrocoat (E-coat) epoxy primers for primary corrosion protection in passenger vehicles. Simultaneously, India’s ambitious target of 500 GW non-fossil fuel capacity is fueling demand for epoxy primers in solar module frames and wind turbine towers, particularly in harsh outdoor environments. Regulatory tightening by the Bureau of Indian Standards through updated Quality Control Orders (QCOs) is ensuring improved product performance, higher solids content, and enhanced durability in domestic epoxy primer formulations, reinforcing India’s position as a high-growth epoxy coatings market.

Germany Epoxy Primers Market: Hydrogen Infrastructure, Circular Chemistry, and Low-VOC Compliance Leadership

The Germany epoxy primers market is defined by its emphasis on advanced materials engineering, circular economy practices, and stringent environmental compliance. The country’s push toward a national hydrogen economy is driving the development of specialized epoxy primers resistant to hydrogen embrittlement and high-pressure storage conditions, opening new avenues in energy infrastructure coatings. In October 2025, AkzoNobel introduced hydrophilic resin-based primers designed to reduce maintenance cycles for industrial facades, highlighting Germany’s leadership in sustainable epoxy coating innovation.

German OEMs are increasingly adopting bio-carbon certified epoxy dispersions, setting new benchmarks for environmentally responsible industrial coatings. Advanced manufacturing integration is evident in automotive plants, where AI-driven surface preparation systems have optimized epoxy primer thickness, reducing material waste by approximately 12%. Compliance with the EU Industrial Emissions Directive is accelerating the phase-out of high-VOC epoxy primers, reinforcing Germany’s dominance in low-emission coating technologies. Additionally, R&D efforts are intensifying in BPA-free epoxy primers for food-grade and medical applications, reflecting the country’s strong foothold in high-value, specialty coatings markets.

Japan Epoxy Primers Market: Nanotechnology Integration, Smart Manufacturing, and Precision Coating Systems

The Japan epoxy primers market is at the forefront of nano-engineered coatings, precision application systems, and high-reliability industrial solutions. The resurgence of domestic semiconductor fabrication is increasing demand for ultra-pure, low-VOC epoxy primers used in cleanroom environments, where contamination control is critical. In infrastructure, Central Japan Railway Company and East Japan Railway Company are deploying nano-composite epoxy primers for Shinkansen networks, extending maintenance intervals up to 15 years and improving lifecycle efficiency.

Japan’s automotive sector is driving demand for multi-substrate compatible epoxy primers, supporting lightweighting strategies involving aluminum and carbon fiber composites. The country also leads in robotic and sensor-integrated coating application systems, achieving up to 99.9% uniformity in electronics manufacturing. Government mandates for disaster-resilient infrastructure are promoting high-elongation epoxy primers capable of withstanding seismic stress, ensuring structural integrity under dynamic conditions. Companies such as Nippon Paint are advancing carbon-neutral epoxy primer solutions, leveraging renewable energy in production to meet stringent ESG requirements, reinforcing Japan’s leadership in next-generation epoxy coatings and sustainable manufacturing technologies.

Epoxy Primers Market Report Scope

Epoxy Primers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.9 Billion

|

|

Market Size (2032)

|

$28.4 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Technology (Solvent-borne Epoxy Primers, Water-borne Epoxy Primers, High-Solids Epoxy Primers, Powder Epoxy Primers), By Substrate (Metal, Concrete and Masonry, Fiberglass, Wood, Plastics and Composites), By Product (Two-Component, One-Component), By Application (Automotive and Transportation, Building and Construction, Marine, Aerospace and Defense, Oil and Gas, General Industrial), By Metal (Steel Priming, Aluminum Priming, Galvanized Metal Priming)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Jotun A/S, Hempel A/S, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., RPM International Inc., BASF SE, Sika AG, Asian Paints Limited, Chugoku Marine Paints, Ltd., Tnemec Company, Inc., Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Epoxy Primers Market Segmentation

By Technology

- Solvent-borne Epoxy Primers

- Water-borne Epoxy Primers

- High-Solids Epoxy Primers

- Powder Epoxy Primers

By Substrate

- Metal

- Concrete and Masonry

- Fiberglass

- Wood

- Plastics and Composites

By Product

- Two-Component

- One-Component

By Application

- Automotive and Transportation

- Building and Construction

- Marine

- Aerospace and Defense

- Oil and Gas

- General Industrial

By Metal

- Steel Priming

- Aluminum Priming

- Galvanized Metal Priming

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Epoxy Primers Market

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Jotun A/S

- Hempel A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- BASF SE

- Sika AG

- Asian Paints Limited

- Chugoku Marine Paints, Ltd.

- Tnemec Company, Inc.

- Berger Paints India Limited

*- List not Exhaustive