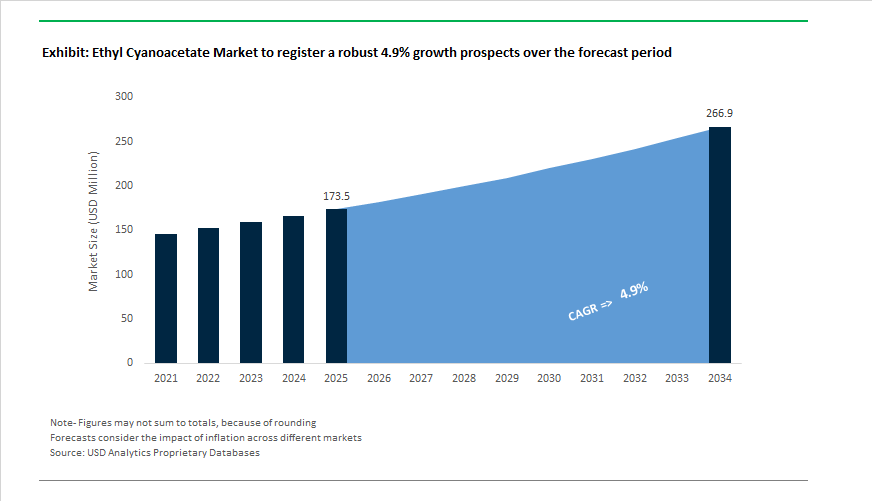

Ethyl Cyanoacetate Market to Reach $266.9 Million by 2034 at 4.9% CAGR Driven by Semiconductor Materials and High-Purity API Intermediates

The Ethyl Cyanoacetate Market is projected to expand from $173.5 Million in 2025 to $266.9 Million by 2034, registering a steady CAGR of 4.9%. Growth is increasingly tied to electronic-grade materials, advanced pharmaceutical intermediates, and specialty adhesive systems rather than legacy bulk applications. Ethyl cyanoacetate remains a critical building block in the synthesis of cyanine dyes, heterocyclic compounds, and cyanoacetylated intermediates used in active pharmaceutical ingredients (APIs), OLED materials, and high-performance adhesives.

In December 2024, Merck KGaA committed €70 million to establish an Advanced Materials Development Center at its Shizuoka site in Japan. The facility focuses on high-precision semiconductor patterning and OLED material development, where ethyl cyanoacetate derivatives serve as intermediates in photoresist and electronic specialty chemistries. This signals a structural pivot of the market toward ultra-high-purity electronic applications. Concurrently, the analog photography revival has unexpectedly stabilized technical-grade demand. Eastman Kodak reported a 21% revenue increase in its film division during 2024, supporting renewed consumption of cyanine dye precursors synthesized from ethyl cyanoacetate.

Pharmaceutical innovation remains a high-value demand driver. Funding programs from the National Institutes of Health during 2024–2025 increased support for antibody-drug conjugates (ADCs), where ethyl cyanoacetate functions as a selective cyanoacetylating reagent to enhance peptide binding and stability. In parallel, Northeast Pharmaceutical Group expanded capacity in 2025 for cardiovascular and anticonvulsant drug intermediates, incorporating dedicated production lines for ethyl cyanoacetate-derived precursors used in Allopurinol synthesis. Strategic catalog expansion also improved global research accessibility; BOC Sciences partnered with Spaya between late 2023 and 2024 to widen the availability of cyanoacetate-based organic building blocks for oncology and inflammation research.

Environmental compliance and regulatory restructuring are reshaping supply chains. In 2025, Hebei Chengxin modernized its downstream cyanide derivatives unit to reduce hydrogen cyanide emissions, aligning with China’s Green Chemical Park standards for 2026. In India, the Ministry of Chemicals revoked mandatory Quality Control Orders in November 2025, easing trade constraints for specialty esters while previously introduced BIS standards (IS 13105:2024) required recalibration of photographic-grade chemical production lines through January 2025. Ukraine enacted UA-REACH in January 2025, mandating chemical registrations exceeding one ton annually, increasing documentation requirements for regional suppliers.

Emerging applications in electronics adhesives further diversify demand. In October 2025, specialty manufacturers introduced instant-cure, waterless adhesive systems utilizing ethyl cyanoacetate as a cross-linking agent for smartphone and wearable assembly, where low-moisture bonding is critical to prevent circuit degradation. By February 2026, European distributors reported increased nearshoring of high-purity ester procurement due to Red Sea logistics disruptions, with pharmaceutical firms securing long-term contracts from domestic and Turkish producers to protect API continuity.

Strategic Trends and Emerging Opportunities Transforming the Ethyl Cyanoacetate Market

Pharmaceutical API Expansion and Heterocyclic Drug Synthesis Driving Ethyl Cyanoacetate Demand Trends

Ethyl Cyanoacetate has evolved into a mission-critical pharmaceutical intermediate, underpinning high-growth therapeutic categories that rely on complex heterocyclic chemistry. As of 2025, the pharmaceutical segment accounts for approximately 39.2% of total Ethyl Cyanoacetate market revenue, establishing API synthesis as the dominant end-use sector. The molecule’s dual nitrile and ester functional groups make it indispensable in the formation of purine and pyrimidine rings used in drugs such as Allopurinol for gout, Ethosuximide for epilepsy, and the antibiotic Trimethoprim. Rising cardiovascular and anti-infective drug demand continues to strengthen consumption of high-purity ECA as a building block in advanced medicinal chemistry workflows.

Generic drug manufacturing is further amplifying demand momentum. Internal data from Tiande Chemical indicate that ECA usage in generic API production increased by 12% between 2023 and 2025, largely driven by patent expirations across high-volume heterocyclic drug classes. In October 2025, research published in the Research Journal of Pharmacy and Technology identified Ethyl Cyanoacetate as a precursor in synthesizing 2-aminoquinoline-3-carbonitrile derivatives with strong anti-mycobacterial activity, with one compound outperforming Ciprofloxacin in potency. These findings signal a high-value opportunity in next-generation tuberculosis treatments and reinforce ECA’s strategic importance in pharmaceutical innovation pipelines.

International Precursor Controls and Environmental Compliance Reshaping Ethyl Cyanoacetate Trade Dynamics

As a versatile organic synthesis intermediate, Ethyl Cyanoacetate is increasingly scrutinized under global chemical precursor control frameworks. On November 11, 2025, five Chinese ministries including Ministry of Commerce of China and National Medical Products Administration implemented a Specific Country export license requirement covering 13 precursor categories, mandating special permits for shipments to the United States, Mexico, and Canada. This policy shift directly impacts the global supply chain for ECA, introducing lead-time variability and increasing compliance complexity for multinational pharmaceutical manufacturers.

Regulatory divergence is becoming evident across regions. While China tightens oversight on sensitive precursors, India’s Ministry of Chemicals and Fertilizers revoked mandatory BIS certification for six industrial chemicals in November 2025 to promote ease of doing business, highlighting contrasting trade strategies. In parallel, the U.S. Environmental Protection Agency has strengthened oversight on facilities handling cyanide byproducts associated with ECA production, driving a 15 to 20% increase in operational overhead for smaller manufacturers due to hazardous waste mitigation and safety infrastructure upgrades. These compliance-driven cost pressures are reshaping competitive dynamics in the global Ethyl Cyanoacetate market.

Continuous Flow Manufacturing and High-Purity Production Unlocking Process Innovation Opportunities

The transition from batch processing to Continuous Flow Manufacturing represents a transformative opportunity in Ethyl Cyanoacetate production, particularly for pharmaceutical-grade material exceeding 99.5% purity. High-purity ECA currently accounts for more than 51% of total market revenue, reflecting escalating demand for analytical-grade intermediates that meet zero-impurity thresholds in regulated drug synthesis. Continuous flow systems enhance reaction control, reduce exposure to hazardous byproducts such as hydrogen cyanide, and improve process safety while delivering consistent quality for GMP-compliant API manufacturing.

Green chemistry initiatives are reinforcing this process shift. During 2024 to 2025, DuPont and Ashland intensified R&D on catalytic esterification improvements aimed at reducing Product Carbon Footprint and aligning with the EU Ecodesign for Sustainable Products Regulation. Advanced micro-reactor technologies have demonstrated up to 10% higher yield compared to conventional stirred-tank reactors, making them attractive for just-in-time ECA synthesis in custom peptide production and high-end cosmetic formulations. These process innovations are positioning continuous flow, high-yield ECA manufacturing as a competitive differentiator through 2026 and beyond.

Diversion-Resistant Supply Chains and Digital Traceability Creating Strategic Market Opportunities

Heightened regulatory oversight is accelerating the adoption of diversion-resistant supply chains and digital traceability solutions in the Ethyl Cyanoacetate market. With the full implementation of the EU Ecodesign for Sustainable Products Regulation in late 2025, traceability has become a strategic requirement. Chemical distributors are increasingly deploying blockchain-enabled digital product passports to track ECA from feedstock sourcing through pharmaceutical laboratory delivery, ensuring transparent audit trails and regulatory compliance across cross-border transactions.

Geopolitical tensions and export license requirements are also fueling localized manufacturing strategies. In January 2026, supply chain experts from Mitsubishi Heavy Industries identified logistics sovereignty as a top industry trend, prompting North American pharmaceutical firms to evaluate near-shoring ECA production to mitigate delays associated with cross-border permits. AI-driven logistics platforms introduced in 2025 now enable Tier 1 chemical providers to cross-reference customs commodity codes and export licenses in real time, reducing shipment seizure risks and ensuring delivery within strict API manufacturing lead-time windows. These sovereign, digitally orchestrated supply chains represent a major opportunity for compliant and high-purity Ethyl Cyanoacetate suppliers in a tightly regulated global environment.

Ethyl Cyanoacetate Market Share and Segmentation Insights

Industrial Grade Ethyl Cyanoacetate Anchors Volume Demand Across Chemical Manufacturing

Industrial grade ethyl cyanoacetate commands 52% of total market share in 2025, supported by large-scale consumption in agrochemicals, adhesives, and dye manufacturing. Its cost efficiency and fit-for-purpose purity make it the preferred specification for high-volume production environments where pharmaceutical-grade compliance is unnecessary. Pharmaceutical grade represents a substantial premium segment, supplying API synthesis and regulated drug manufacturing under strict cGMP standards. This grade supports complex medicinal chemistry pathways, commanding higher margins due to rigorous quality control and documentation requirements. Electronic grade remains a niche but fast-evolving category, serving semiconductor and electronic chemical applications that demand ultra-low metallic impurities and tight particle specifications. While smaller in volume, this segment benefits from rising investments in advanced electronics manufacturing, positioning electronic grade ethyl cyanoacetate as a strategically important specialty chemical within high-tech supply chains.

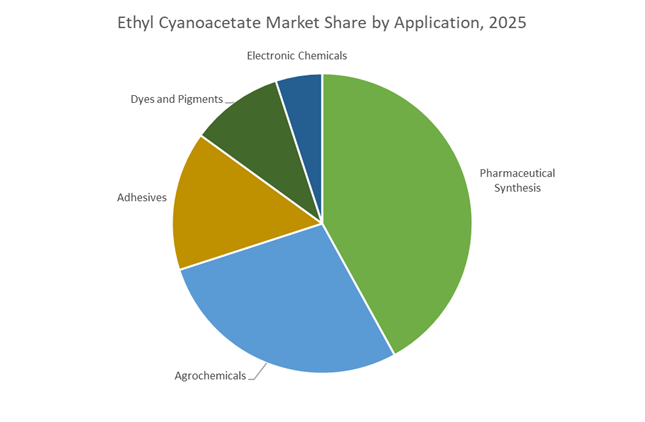

Pharmaceutical Synthesis Drives Core Consumption Supported by Agrochemical and Adhesive Growth

Pharmaceutical synthesis accounts for 42% of ethyl cyanoacetate demand in 2025, reflecting its role as a key intermediate in producing antihypertensives, anticonvulsants, antimalarials, and cardiovascular drugs. Its versatility in forming heterocyclic compounds makes it indispensable to modern medicinal chemistry. Agrochemicals represent the second-largest application segment, using ethyl cyanoacetate as a building block for herbicides, fungicides, and insecticides that enhance crop productivity. Adhesives follow as an important market, where ethyl cyanoacetate underpins cyanoacrylate “super glue” production, enabling rapid-bonding formulations for industrial and consumer use. Dyes and pigments maintain steady uptake in textile and printing ink synthesis, while electronic chemicals are expanding as high-purity grades find increasing adoption in photoresists and semiconductor precursor formulations.

Competitive Landscape of the Ethyl Cyanoacetate Market

The global ethyl cyanoacetate market in 2026 is defined by Chinese scale leadership, rising ESG-driven process optimization, and premium demand from pharmaceutical intermediates, agrochemicals, adhesives, and specialty research chemicals, with purity, feedstock security, and regulatory compliance emerging as decisive competitive factors.

Hebei Chengxin Co., Ltd. dominates global supply through integrated cyanide chemistry

Hebei Chengxin is widely regarded as the world’s largest producer of cyanide-based downstream chemicals, including ultra-high-purity ethyl cyanoacetate (99.5% minimum). Its massive portfolio spans malonates and cyanoacetic acid derivatives, serving agrochemicals, pharmaceuticals, and specialty synthesis. The company’s core advantage lies in full sodium cyanide integration, giving it unmatched feedstock security and insulation from raw material volatility. Chengxin is the primary global supplier to the agrochemical segment, supporting herbicide and fungicide production at scale. By 2026, its heavy investment in proprietary waste-treatment and emissions control systems has turned environmental compliance into a competitive moat, enabling high-volume output while meeting China’s tightening green chemistry regulations.

Tiande Chemical Holdings Limited leads adhesive-grade ethyl cyanoacetate with low-moisture precision

Tiande Chemical holds a top-tier global position in cyanoacetate and malonate esters, with particular dominance in adhesive-grade ethyl cyanoacetate where moisture levels below 0.05% are critical. Its specialized grades are widely used in α-cyanoacrylate super glue synthesis, valued for fast curing and shelf-life stability. In late 2025, Tiande optimized its continuous distillation technology, sharply reducing energy per ton and strengthening its appeal to ESG-focused Western buyers in 2026. The company has also expanded export logistics to capture the 5.9% CAGR growth in India’s pharmaceutical intermediates market, positioning itself as a preferred supplier for both adhesives and drug synthesis value chains.

Shandong Xinhua Pharmaceutical Co., Ltd. integrates ethyl cyanoacetate into API production pipelines

Shandong Xinhua leverages a captive-first manufacturing model, consuming much of its own ethyl cyanoacetate internally for APIs such as Allopurinol, Trimethoprim, and CNS drugs including Ethosuximide. This backward integration shields margins from market price swings while ensuring pharmaceutical-grade consistency. In 2025 to 2026, Xinhua accelerated its shift toward advanced digital manufacturing, deploying AI-driven real-time purity monitoring to comply with US FDA and European GMP standards. Its strength lies in deep regulatory certification and long-standing audits by multinational pharma companies, creating high barriers to entry. Ethyl cyanoacetate remains central to its heterocyclic drug synthesis strategy.

Merck KGaA captures premium research demand via Sigma-Aldrich channels

Through its Life Science portfolio, Merck addresses the high-value, low-volume segment of the ethyl cyanoacetate market, supplying research and fine chemical customers that require certified purity above 99%. In 2026, Merck commands the highest price points, serving drug discovery labs and advanced organic synthesis workflows where ethyl cyanoacetate acts as a malononitrile precursor and oncology research intermediate. The company is executing a regionalized supply chain strategy to reduce Europe’s dependence on Asian imports, while expanding custom synthesis services introduced in 2025. These EHS-compliant blends support biotech firms seeking tailored pharmaceutical intermediates with full documentation and traceability.

Tokyo Chemical Industry Co., Ltd. enables innovation with research-grade cyanoacetate derivatives

TCI specializes in research-grade ethyl cyanoacetate and niche derivatives such as 2-ethylhexyl cyanoacetate, serving specialty polymers, electronics, and early-stage drug development. In 2025 to 2026, TCI gained traction in electronics, where cyanoacetate derivatives are used in cross-linking resins for 5G components. Its unique strength is catalog breadth, offering quantities from 25 g to 25 kg at consistent purity, making it the on-ramp for projects that later scale to bulk production. TCI also strengthened Digital Lab integration in 2026, enabling researchers to access molecular batch data via QR codes, now standard in high-end laboratories.

China: Feedstock Surplus Meets API-Centric Scale-Up

China’s ethyl cyanoacetate market is structurally advantaged by upstream feedstock economics and policy-backed fine chemical expansion. In September 2025, Ministry of Industry and Information Technology released a multi-ministerial Work Plan targeting more than 5% average annual growth in the chemical sector through 2026. High-end fine chemicals such as ethyl cyanoacetate are explicitly prioritized due to their strategic role in pharmaceutical intermediates and electronic materials. This policy tailwind coincides with a projected ethylene surplus reaching 121% of domestic demand by 2026, materially reducing production costs for cyanoacetate derivatives and improving margin resilience for integrated producers.

Industrial restructuring is reinforcing quality leadership. By 2026, China is enforcing the retirement of facilities older than 20 years, which still account for roughly 12% of ethylene capacity. This consolidation is accelerating migration toward Smart Verbund chemical parks that integrate cyanoacetate synthesis with high-purity downstream purification. Leading producers such as Hebei Chengxin have standardized 99.5% purity ethyl cyanoacetate since 2025, securing preferred supplier status for global API chains producing Vitamin B6, caffeine, and allopurinol. In parallel, Zhejiang-based clusters expanded captive conversion of ethyl cyanoacetate into ethyl cyanoacrylate during late 2025, directly supplying fast-growing automotive and appliance assembly demand across Asia-Pacific.

India: Decarbonization Mandates and Pharma Localization

India’s ethyl cyanoacetate market is being reshaped by environmental regulation and pharmaceutical localization rather than scale alone. The Carbon Credit Trading Scheme, notified on October 8, 2025, imposes legally binding emission intensity targets on petrochemical manufacturers. Producers of cyanoacetate intermediates are required to achieve up to 40% intensity reduction during the 2025–26 cycle, accelerating adoption of greener catalysts and solvent recovery systems. This regulatory pressure is favoring technologically agile plants capable of meeting both cost and compliance thresholds.

On the demand side, regulatory clarity has stabilized agrochemical and pharmaceutical pull. The extension of the Fertilizers Control Second Amendment Order compliance deadline to June 16, 2025 reduced procurement uncertainty for cyanoacetate-based biostimulant intermediates. More importantly, India’s Department of Pharmaceuticals achieved its 2026 milestone for domesticating 26 critical drug intermediates, with ethyl cyanoacetate identified as a key building block for folic acid and theophylline synthesis. This positions India as a credible secondary supply base for regulated pharma markets seeking alternatives to East Asian sourcing concentration.

South Korea: High-Purity Demand from Bioprocessing and OLED Materials

South Korea’s ethyl cyanoacetate demand profile is technology-driven and purity-sensitive. In March 2024, Merck KGaA announced a more than $325 million investment in a bioprocessing production center in Daejeon, scheduled to reach key operational milestones by 2026. While not a direct cyanoacetate producer, the facility significantly increases regional consumption of high-purity cyanoacetates used in pharmaceutical purification and synthesis workflows.

Simultaneously, Korean chemical firms are expanding the use of ethyl cyanoacetate as a cyanating agent in palladium-catalyzed reactions for next-generation OLED materials and electronic adhesives. This application shift reflects Korea’s broader move toward high-value electronic chemicals where impurity control directly impacts device yield and reliability, elevating specification requirements for upstream suppliers.

United States: Nearshoring and Medical-Grade Adhesive Innovation

In the United States, trade policy and downstream innovation are reshaping procurement strategies for ethyl cyanoacetate. Trade adjustments introduced during 2025–2026 prompted procurement teams to reassess dependence on long-haul imports, accelerating interest in nearshored or domestic supply from Gulf Coast chemical clusters. This shift is less about volume substitution and more about supply chain resilience and regulatory alignment for sensitive applications.

Downstream, adhesive innovation is driving specification upgrades. In early 2026, U.S. manufacturers launched low-odor, low-blooming cyanoacrylate monomers designed for medical device assembly. These formulations rely on ultra-high-purity ethyl cyanoacetate to eliminate white residue and volatile byproducts, reinforcing demand for tighter impurity control rather than commodity-grade material.

Germany: REACH-Driven Purity and Green Chemistry Transition

Germany’s ethyl cyanoacetate market is governed by regulatory stringency and sustainability-led process innovation. Ahead of the 2026 REACH recast, European producers are upgrading distillation and finishing units to reduce trace impurities and preserve label-free status for consumer-grade instant adhesives. Compliance extends to demonstrable control over residual contaminants.

Concurrently, German chemical groups adopted greener synthesis routes during 2025. The transition toward bio-catalyst-enabled Knoevenagel condensation has reduced the carbon footprint of ethyl cyanoacetate production by an estimated 15% versus 2023 baselines. This positions German output as compliance-ready for both regulatory and customer-driven sustainability audits.

Strategic Snapshot: Ethyl Cyanoacetate Market by Country (2025–2026)

Ethyl Cyanoacetate Market County Level Snapshot

|

Country

|

Core Driver

|

Industrial Focus

|

Strategic Outcome

|

|

China

|

Feedstock surplus and policy backing

|

API-grade purity, integrated Verbund sites

|

Global supply dominance

|

|

India

|

Decarbonization and pharma PLI

|

Green synthesis, localized drug intermediates

|

Alternate pharma hub

|

|

South Korea

|

Electronics and bioprocessing

|

Ultra-high-purity specifications

|

Technology-led demand

|

|

United States

|

Supply chain resilience

|

Medical-grade adhesive innovation

|

Nearshoring momentum

|

|

Germany

|

REACH and sustainability

|

Low-impurity, low-carbon processes

|

Compliance-led differentiation

|

Ethyl Cyanoacetate Market Report Scope

Ethyl Cyanoacetate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$173.5 Million

|

|

Market Size (2034)

|

$266.9 Million

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Grade (Pharmaceutical Grade, Industrial Grade, Electronic Grade), By Application (Pharmaceutical Synthesis, Agrochemicals, Adhesives, Dyes and Pigments, Electronic Chemicals), By Distribution Channel (Direct Supply, Specialty Chemical Distributors, Online B2B Platforms)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hebei Chengxin Co., Ltd., Tiande Chemical Holdings Limited, Merck KGaA, Thermo Fisher Scientific Inc., Shandong Xinhua Pharmaceutical Co., Ltd., Zibo Xinao Chemical Co., Ltd., Penta Manufacturing Company, Tokyo Chemical Industry Co., Ltd., Anhui Meisenbao Chemical Co., Ltd., Ataman Kimya, Career Henan Chemical, Jubilant Ingrevia Limited, Avantor, Inc., Triveni Chemicals, Hubei Sanonda

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethyl Cyanoacetate Market Segmentation

By Grade

- Pharmaceutical Grade

- Industrial Grade

- Electronic Grade

By Application

- Pharmaceutical Synthesis

- Agrochemicals

- Adhesives

- Dyes and Pigments

- Electronic Chemicals

By Distribution Channel

- Direct Supply

- Specialty Chemical Distributors

- Online B2B Platforms

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethyl Cyanoacetate Industry

- Hebei Chengxin Co., Ltd.

- Tiande Chemical Holdings Limited

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Shandong Xinhua Pharmaceutical Co., Ltd.

- Zibo Xinao Chemical Co., Ltd.

- Penta Manufacturing Company

- Tokyo Chemical Industry Co., Ltd.

- Anhui Meisenbao Chemical Co., Ltd.

- Ataman Kimya

- Career Henan Chemical

- Jubilant Ingrevia Limited

- Avantor, Inc.

- Triveni Chemicals

- Hubei Sanonda

*- List not Exhaustive