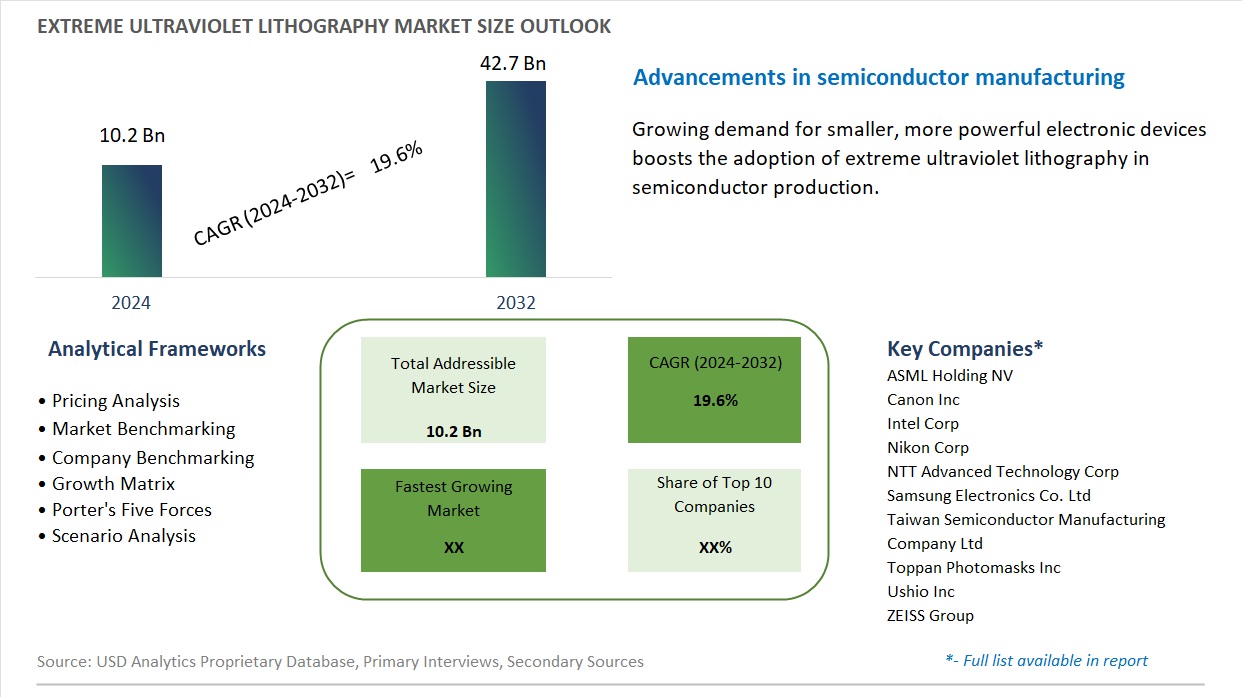

Global Extreme Ultraviolet Lithography Market Size is valued at $10.2 Billion in 2024 and is forecast to register a growth rate (CAGR) of 19.6% to reach $42.7 Billion by 2032.

The global Extreme Ultraviolet Lithography Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Equipment (Light Source, Optics, Mask, Others), By End-User (Integrated Device Manufacturer (IDM), Foundries).

An Introduction to Extreme Ultraviolet Lithography Market

The extreme ultraviolet (EUV) lithography market is witnessing substantial growth, driven by the increasing demand for advanced semiconductor manufacturing technologies that enable the production of smaller, faster, and more efficient microchips. EUV lithography, which uses short-wavelength ultraviolet light to create extremely fine patterns on semiconductor wafers, is becoming a critical technology for fabricating next-generation integrated circuits with nodes below 7 nanometers. The push for more powerful and compact electronic devices, including smartphones, high-performance computing systems, and AI-driven applications, is fueling the adoption of EUV lithography. Key players in the semiconductor industry are investing heavily in EUV technology to enhance their production capabilities and maintain a competitive edge. Despite challenges such as high equipment costs and technical complexities, ongoing advancements in EUV systems, including improvements in throughput and defect reduction, are accelerating its deployment. The EUV lithography market is also benefiting from government initiatives and strategic partnerships aimed at boosting domestic semiconductor manufacturing. As the semiconductor industry continues to innovate and push the boundaries of Moore's Law, the EUV lithography market is poised for robust growth, reflecting broader trends in technology miniaturization and digital transformation.

Extreme Ultraviolet Lithography Competitive Landscape

The market report analyses the leading companies in the industry including ASML Holding NV, Canon Inc, Intel Corp, Nikon Corp, NTT Advanced Technology Corp, Samsung Electronics Co. Ltd, Taiwan Semiconductor Manufacturing Company Ltd, Toppan Photomasks Inc, Ushio Inc, ZEISS Group, and others.

Extreme Ultraviolet Lithography Market Dynamics

Market Trend: Advancements in EUV Technology for Semiconductor Manufacturing

The Extreme Ultraviolet (EUV) Lithography Market is experiencing a prominent trend towards advancements in EUV technology for semiconductor manufacturing. EUV lithography is increasingly being adopted as the technology of choice for producing the next generation of semiconductor devices with smaller feature sizes and higher performance. This trend is driven by the semiconductor industry's need to keep pace with Moore's Law, which demands continued scaling down of transistor sizes to enhance computing power and efficiency. Ongoing innovations and improvements in EUV technology, such as higher resolution and increased throughput, are essential for meeting these demands.

Market Driver: Growing Demand for High-Performance and Miniaturized Electronic Devices

The growing demand for high-performance and miniaturized electronic devices is a significant driver for the Extreme Ultraviolet Lithography Market. As consumer electronics, telecommunications, and computing devices continue to evolve towards more powerful and compact forms, there is a need for advanced lithography techniques that can produce increasingly smaller and more complex semiconductor components. EUV lithography addresses this need by enabling the production of smaller feature sizes and higher-density chips, thus driving its adoption in the semiconductor manufacturing process.

Market Opportunity: Expansion into Emerging Applications and Continued Technological Innovations

A notable opportunity for the Extreme Ultraviolet Lithography Market lies in the expansion into emerging applications and continued technological innovations. As the demand for advanced semiconductor devices grows, there is potential for EUV technology to be applied beyond traditional semiconductor manufacturing, such as in advanced packaging, high-performance computing, and emerging technologies like quantum computing. Additionally, ongoing research and development to enhance EUV system performance, reduce costs, and increase efficiency can provide competitive advantages and open new market opportunities. By focusing on these areas, companies can capitalize on the evolving landscape of semiconductor technology and drive future growth in the EUV lithography market.

Extreme Ultraviolet Lithography Market Share Analysis: Integrated Device Manufacturer (IDM) generated the highest revenue in 2024

In the Extreme Ultraviolet (EUV) Lithography Market, the Integrated Device Manufacturer (IDM) segment is the largest due to its substantial investments in advanced semiconductor technologies and its direct control over the entire semiconductor production process. IDMs, which include major technology companies such as Intel, Samsung, and TSMC, utilize EUV lithography to achieve cutting-edge semiconductor node advancements and enhance device performance. Their need for high-resolution patterning to meet the increasing demands for smaller, faster, and more efficient chips drives significant demand for EUV lithography equipment. This focus on innovation and quality control within IDMs ensures their prominent role in the EUV market, outpacing other end-users such as foundries.

Extreme Ultraviolet Lithography Market Share Analysis: Light Source is poised to register the fastest CAGR over the forecast period

In the Extreme Ultraviolet (EUV) Lithography Market, the Light Source segment is the fastest growing over the forecast period to 2032. This growth is driven by the increasing complexity and demand for advanced semiconductor manufacturing, where EUV lithography's high-resolution capabilities are critical. Light sources are essential components of EUV systems, providing the necessary high-energy photons to pattern semiconductor wafers with extreme precision. As semiconductor manufacturers push towards smaller node sizes and more advanced technologies, the demand for cutting-edge light sources, such as those using laser-produced plasma (LPP) technology, is accelerating. This segment’s rapid innovation and pivotal role in enabling advancements in semiconductor fabrication make it the fastest growing in the EUV lithography market.

Extreme Ultraviolet Lithography Market Segmentation

By Equipment

Light Source

Optics

Mask

Others

By End-User

Integrated Device Manufacturer (IDM)

Foundries

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Extreme Ultraviolet Lithography Companies Profiled in the Study

ASML Holding NV

Canon Inc

Intel Corp

Nikon Corp

NTT Advanced Technology Corp

Samsung Electronics Co. Ltd

Taiwan Semiconductor Manufacturing Company Ltd

Toppan Photomasks Inc

Ushio Inc

ZEISS Group

*- List Not Exhaustive

Extreme Ultraviolet Lithography Market Segmentation

By Equipment

Light Source

Optics

Mask

Others

By End-User

Integrated Device Manufacturer (IDM)

Foundries

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)