Faux Finish Coatings Market Growth Driven by Designer-Led Aesthetics, Luxury Renovation Trends, and Low-VOC Decorative Systems

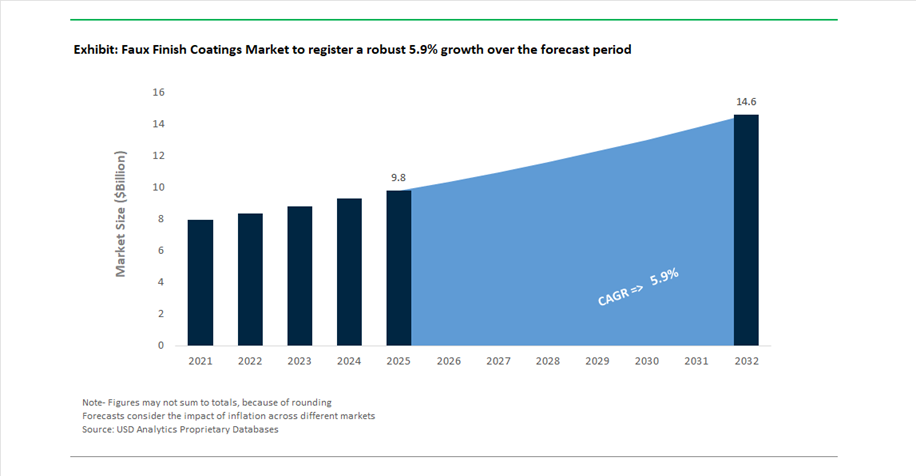

The global Faux Finish Coatings Market was valued at USD 9.8 billion in 2025 and is projected to grow at a CAGR of 5.9% between 2025 and 2032, reaching USD 14.6 billion by 2032. This growth is being driven by the increasing demand for premium decorative coatings that replicate high-end materials such as marble, wood, stone, concrete, and metallic surfaces, offering cost-effective and customizable alternatives for residential and commercial interiors.

A key structural driver is the global rise in renovation and interior design-led spending, particularly in urban residential and hospitality segments. Consumers are shifting away from plain wall finishes toward textured, layered, and visually dynamic surfaces, including Venetian plaster, glazing, color washing, and trompe l’oeil techniques. These finishes are increasingly being specified in luxury homes, boutique hotels, retail environments, and office interiors, where differentiated aesthetics and brand identity are critical.

Sustainability is also influencing product innovation within the faux finish segment. The growing adoption of low-VOC, odor-free, and water-based formulations is enabling complex, multi-layer decorative applications in occupied environments such as hospitals, hotels, and commercial spaces. Additionally, advancements in binder chemistry, pigment dispersion, and surface engineering are improving durability, stain resistance, and ease of application—historically key limitations of faux finishes.

Color-Driven Design Trends, Primer Innovation, and Luxury Texture Expansion Reshape Market Dynamics

The faux finish coatings market is being actively reshaped by color trend leadership, product innovation, and expansion into high-end decorative segments. In October 2024, Benjamin Moore introduced “Cinnamon Slate 2113-40” as its Color of the Year 2025, specifically positioned to complement natural wood and stone-inspired finishes. This palette is widely adopted in modern glazing and washing techniques, bridging traditional faux aesthetics with contemporary design preferences. Building on this momentum, in October 2025, Benjamin Moore announced “Silhouette AF-655” as its 2026 Color of the Year, a deep charcoal tone optimized for trompe l’oeil and industrial metallic faux effects, enabling designers to create high-contrast, visually immersive surfaces.

Product innovation is also addressing application challenges. In November 2025, Sherwin-Williams launched a new line of specialized primers under its HGTV Home® range, engineered for “Purposeful Prep.” These primers create uniform substrates for complex faux finishes such as Venetian plaster and stippled textures, ensuring consistent adhesion and depth of color, which are critical for professional-grade decorative applications. Additionally, in January 2026, PPG Industries refreshed its MASTER’S MARK™ brand identity, emphasizing coatings that maintain high durability, stain resistance, and scrub resistance even in textured faux applications.

Strategic expansion into regional and luxury markets is accelerating growth. In January 2026, Sherwin-Williams expanded its presence in Latin America through the integration of Suvinil, a brand known for its texturized and effect coatings, enabling the scaling of faux finish solutions across high-growth markets. Meanwhile, in February 2026, Asian Paints expanded its Nilaya luxury texture line, focusing on liquid textures that mimic fabrics and minerals, targeting premium renovation demand in Tier-1 Indian cities.

Sustainability and application flexibility are also key innovation areas. In May 2025, Benjamin Moore launched Eco Spec®, a low-odor, environmentally friendly paint line that enables multi-layer faux applications in sensitive environments without VOC-related disruptions. Additionally, in April 2026, BASF showcased acForm® technology, enabling the creation of 3D faux veneer surfaces on complex furniture components, expanding the application of faux finishes into industrial design and manufacturing.

High-Definition Faux Finishes Replacing Natural Stone in Luxury Architectural Applications

The faux finish coatings market is experiencing a structural transition as high-definition decorative coatings increasingly replace natural stone across luxury residential, hospitality, and commercial construction projects. The shift is primarily driven by cost optimization, structural efficiency, and sustainability considerations. Modern faux limestone and travertine finishes offer a significant weight advantage, with coatings weighing approximately 90% less than traditional 2 cm natural stone slabs, enabling architects and engineers to reduce load-bearing requirements and foundation costs in high-rise developments. This is particularly relevant in urban megaprojects where structural optimization directly impacts capital expenditure. In parallel, the growing adoption of biophilic design principles is accelerating demand for coatings that replicate natural textures such as marble veining, wood grains, and mineral finishes. By 2025, lime-based Venetian plasters have recorded a 15% year-over-year increase in specification within commercial interiors, reflecting a clear preference for natural aesthetic replication over synthetic wall coverings. Performance improvements in acrylic-modified faux coatings have also enhanced durability, delivering surface hardness suitable for high-traffic environments such as hotel lobbies while reducing long-term maintenance costs by approximately 40% compared to polished natural stone. Additionally, the additive application process of faux finishes eliminates the material wastage associated with stone cutting, which can reach up to 30%, aligning with LEED v4.1 zero-waste construction objectives. These combined factors are positioning high-definition faux finishes as a cost-efficient, sustainable, and design-flexible alternative in the global decorative coatings market.

Regulatory Phase-Down of High-VOC Glazes Accelerating Water-Borne Faux Finish Technologies

The regulatory tightening of volatile organic compound emissions is forcing a fundamental transformation in the chemistry of faux finish coatings, particularly in specialty glazes and decorative topcoats. The U.S. Environmental Protection Agency’s 2025 amendments to national VOC emission standards have aligned federal regulations with California Air Resources Board limits, mandating a transition away from high-VOC aerosolized coatings by mid-2025. This has created an urgent need for reformulation across faux finish primers, sealers, and glaze systems. In response, coating manufacturers have accelerated the development of water-borne alkyd and hybrid glaze technologies that replicate the performance characteristics of traditional oil-based systems. Laboratory data from 2025 indicates that advanced water-based glazes now achieve wet-edge open times of 45 to 60 minutes, matching the workability required for complex decorative techniques such as scumbling and marbling. Globally, indoor air quality regulations are reinforcing this transition, with frameworks such as Dubai’s Al Sa’fat mandating low-emission material documentation, leading to a 60% increase in the adoption of formaldehyde-free and zero-VOC mineral paints for interior decorative applications. Additionally, electronic compliance reporting requirements introduced under updated EPA frameworks are increasing transparency across the supply chain, reducing the prevalence of non-compliant boutique formulations. These regulatory pressures are accelerating innovation in eco-friendly decorative coatings, positioning water-borne faux finishes and low-VOC glaze systems as the new industry standard.

Biophilic and High-Reflectance Faux Finishes Supporting Dubai’s “Organic Look” Architectural Mandate

Dubai’s evolving regulatory framework, particularly under the Al Sa’fat 2025 and 2026 building codes, is creating a strong growth avenue for faux finish coatings that replicate natural materials while delivering enhanced thermal performance. The shift toward “organic look” architecture is reducing reliance on reflective glass facades and encouraging the use of natural-mimicry coatings that align with urban sustainability and aesthetic objectives. High solar reflectance faux finishes integrated with advanced pigments are capable of reducing exterior wall surface temperatures by up to 10°C in extreme desert climates, improving building energy efficiency and occupant comfort. This thermal performance advantage is critical in reducing cooling loads in high-temperature environments. Additionally, there is increasing demand for multifunctional coatings that combine natural aesthetics with self-cleaning, anti-fungal, and humidity-regulating properties, particularly in coastal regions where environmental stress factors are high. The integration of lime-wash and clay-based finishes also supports wellness-oriented building certifications such as the WELL standard, due to their natural ability to regulate indoor humidity and inhibit microbial growth. With Dubai’s 2040 Urban Master Plan emphasizing green and nature-integrated design, projects that incorporate eco-friendly decorative coatings are gaining faster regulatory approvals and higher market value. This is positioning faux finish coatings as a strategic solution for sustainable, climate-responsive architectural design in the Middle East.

Historic Preservation Funding Driving Demand for Traditional Faux Finishing Techniques in the United States

The increasing allocation of federal and state funding for historic preservation is creating a specialized, high-margin opportunity for faux finish coatings in restoration applications. The U.S. Department of the Interior’s fiscal year 2026 budget includes dedicated funding under the Historic Preservation Fund, with approximately 12 million dollars allocated for the conservation of cultural and historic assets. A significant portion of this funding is directed toward restoring traditional architectural elements, including faux wood graining, marbleizing, and trompe l'oeil finishes in heritage buildings. The broader context of a 33 billion dollar deferred maintenance backlog across federal properties is further amplifying demand for skilled restoration services and specialized coating materials. At the state level, programs such as the State Historic Preservation Office grants have distributed over 62 million dollars in matching funds, supporting the preservation of non-federal historic structures and driving regional demand for artisanal decorative coatings. Compliance with the Secretary of the Interior’s Standards for the Treatment of Historic Properties is mandatory for grant eligibility, effectively requiring the use of traditional faux finishing techniques rather than modern flat coatings. This regulatory framework is reinforcing the value of heritage-compatible coating systems and skilled craftsmanship, creating sustained demand for high-quality faux finish coatings tailored for restoration and preservation projects across the United States.

Faux Finish Coatings Market Share 2025: Dominance of Textured Finishes and Restoration Projects

Finish Type Insights: Plaster and Textures Lead the Faux Finish Coatings Market

The plaster and textures segment dominates the faux finish coatings market with a 32% market share in 2025, emerging as the most preferred finish type across residential and commercial interior design projects. High demand for rustic, industrial, and luxury interior aesthetics is a primary growth driver, with finishes such as Venetian plaster, lime wash, and sand textures widely adopted in boutique hotels, premium residential spaces, and statement commercial walls. These textured coatings not only deliver visual depth but also provide a durable and low-maintenance alternative to traditional smooth paints, making them highly attractive in high-traffic renovation projects. Their ability to conceal surface imperfections and reduce repainting frequency further strengthens their adoption, especially in cost-sensitive yet design-focused markets. As interior design trends continue shifting toward authenticity and tactile finishes, plaster-based faux coatings are expected to maintain strong market leadership.

Project Type Insights: Maintenance and Restoration Drive Market Expansion

The maintenance and restoration segment accounts for a leading 54% share of the faux finish coatings market in 2025, reflecting the growing emphasis on renovation over new construction. A major growth catalyst is the rising demand for heritage building restoration, where historic hotels, churches, and government structures require authentic faux finishing techniques such as marbleizing and wood graining to preserve original architectural aesthetics. Additionally, faux finish coatings offer a cost-effective alternative to complete structural replacement, particularly in residential and high-end interior renovation projects. Applying decorative finishes over existing surfaces significantly reduces labor and material costs while achieving premium visual outcomes. This economic advantage, combined with increasing investments in interior refurbishment and adaptive reuse projects, is driving strong adoption. As sustainability and preservation trends gain momentum globally, the maintenance and restoration segment is expected to remain a key revenue contributor.

Faux Finish Coatings Market Competitive Landscape Driven by Design Innovation, AI Visualization, and Artisan-Grade Finishes

The faux finish coatings market is evolving rapidly, driven by demand for decorative textures, AI-enabled design tools, and premium aesthetic coatings. Competition is defined by color innovation, digital visualization platforms, DIY-professional convergence, and sustainable decorative systems that replicate natural materials such as wood, stone, and metallic surfaces.

AkzoNobel transforms faux finish coatings with AI-driven Dulux Maestro ecosystem and bio-based innovation

AkzoNobel is advancing the faux finish coatings market through the launch of Dulux Maestro in May 2026, an integrated platform combining high-performance decorative coatings with AI-driven texture visualization tools for design professionals. The company strengthened its financial position by raising €1.1 billion to accelerate its transition toward bio-based binders and support its "Rhythm of Blues" color initiative. This 2026 color concept emphasizes multi-tonal layering systems that enable artisans to create depth-rich, visually dynamic wall finishes. AkzoNobel’s nearing merger with Axalta further enhances its leadership in architectural and specialty coatings. Its extensive presence across 150 countries ensures accessibility to ready-to-use faux finish systems that simplify complex decorative applications. These capabilities position the company as a leader in next-generation decorative and faux finish coating technologies.

PPG Industries advances multi-dimensional faux finishes through global color strategy and tech collaborations

PPG Industries is strengthening its foothold in the faux finish coatings market through its 2026 design theme "Parallels," which emphasizes dynamic, light-responsive finishes that shift appearance under varying conditions. The company reported strong financial performance with $15.9 billion in net sales, driven partly by its "Secret Safari" color palette designed for rugged, organic textures. PPG is collaborating with technology leaders such as Xiaomi and BYD to develop multi-dimensional coatings that blend automotive-grade metallic aesthetics with residential faux finishes. Following its $2 billion divestiture of its North American architectural business, the company is reallocating resources toward high-value specialty coatings. Its Shanghai-based color styling team plays a central role in global design innovation. This strategy reinforces PPG’s position in premium decorative coatings and advanced surface technologies.

Sherwin-Williams captures DIY-professional faux finish demand with digital tools and sustainable decorative coatings

The Sherwin-Williams Company continues to dominate the North American faux finish coatings market through its extensive network of over 5,000 stores, serving both DIY consumers and professional contractors. The company’s Virtual Panel Studio, showcased at KBIS 2026, enables architects to digitally simulate faux-wood and composite finishes prior to application, enhancing project accuracy. Its DesignHouse team developed 1,850 custom panels, focusing on sculptural textures and rich material combinations aligned with 2026 design trends. Financially, Sherwin-Williams projects EPS between $11.50 and $11.90, reflecting stable growth. The expansion of Powdura® ECO into decorative coatings incorporates 25% recycled plastic, supporting sustainability goals. This integrated approach strengthens its leadership in customizable, eco-friendly faux finish coatings.

RPM International expands artisan-grade faux finish solutions through acquisitions and specialty coatings strength

RPM International is reinforcing its position in the faux finish coatings market through strong financial performance, reporting $1.61 billion in quarterly sales with 8.9% growth driven by its MAP 2025 program. The acquisition of Kalzip GmbH enhances its capabilities in metal-based facade textures and decorative architectural systems. RPM’s Consumer Group is undergoing restructuring to accelerate the rollout of artisan-grade DIY faux finish kits under new leadership. Its Tremco Construction Products Group integrates decorative coatings into high-performance building envelope solutions, ensuring durability alongside aesthetics. The company’s dominance in specialty coatings enables it to cater to both industrial and consumer decorative markets. These initiatives position RPM as a key player in scalable, high-quality faux finish systems.

Benjamin Moore elevates faux finish coatings with “Quiet Luxury” palette and advanced glazing technologies

Benjamin Moore is shaping the faux finish coatings market with its 2026 Color of the Year, Silhouette AF-655, reflecting the growing "Quiet Luxury" trend in interior and exterior design. The company focuses on the psychology of color, promoting sanctuary-driven spaces through rich midtones that replicate natural wood and textile textures. Its Color Trends 2026 palette includes eight carefully curated hues designed to enhance depth and surface detailing. R&D efforts are directed toward improving glaze open time, enabling artisans to achieve more refined blending and layering effects. Benjamin Moore is also emphasizing long-lasting, timeless finishes over short-term trends. This strategy strengthens its position in premium decorative coatings and high-end faux finish applications.

Behr Process drives consumer-centric faux finish innovation with expressive colors and mass customization

Behr Process Corporation is expanding its influence in the faux finish coatings market through consumer-driven innovation and accessible design solutions. The launch of "Hidden Gem" (N430-6A) as its 2026 Color of the Year highlights a trend toward expressive, nature-inspired finishes. The company’s research shows that 82% of consumers associate paint color with personal confidence, reinforcing demand for customized decorative coatings. Behr introduced "Taupe" as its Exterior Stain Color of the Year alongside an 18-color Outdoor Accent collection designed to enhance faux-wood architectural elements. Through its partnership with The Home Depot, Behr offers over 1,600 computer-matched finishes, enabling cost-effective replication of premium materials. This mass customization strategy positions Behr strongly in the DIY and mid-market faux finish coatings segment.

India Faux Finish Coatings Market: Luxury Customization and Smart City Expansion Driving Global Leadership

India has emerged as a global leader in faux finish coatings, fueled by rapid urbanization, rising disposable income, and strong government backing. Under Smart Cities Mission 2.0 (2026), the use of venetian plasters, marbleizing, and textured finishes is being actively promoted in public infrastructure and hospitality projects.

Innovation is a major differentiator. Companies like Asian Paints are integrating silver-ion antimicrobial technology into faux finishes for healthcare and educational spaces, while domestic resin manufacturers are developing advanced synthetic binders that improve adhesion on complex substrates. Industry consolidation—such as JSW Paints’ acquisition of AkzoNobel’s decorative business—is strengthening the supply of water-based faux-effect coatings tailored for Indian climatic conditions. Additionally, the rise of VR-enabled experience centers ($120M investment) is transforming the consumer experience by allowing real-time visualization of decorative effects. Regulatory changes are also shaping the market, with BIS norms mandating a 30% reduction in VOC content, accelerating the shift toward eco-friendly coatings.

United States Faux Finish Coatings Market: UV-Curable Systems and Labor Efficiency Driving Transformation

The U.S. market is undergoing a shift toward high-speed, low-emission application technologies, driven by rising labor costs and regulatory pressure. A key trend is the rapid adoption of UV-curable faux finish systems, which enable instant curing and zero-VOC emissions, particularly in commercial interior applications.

Technological innovation is focused on performance and sustainability. The introduction of “Edge Plus” coating technology ensures uniform thickness even on complex architectural features, while bio-based adhesives are replacing petroleum-derived bonding agents in decorative finishes. Growth in semiconductor infrastructure under the CHIPS Act is also driving niche demand for ESD-safe faux finishes in executive and cleanroom-adjacent environments. Additionally, stricter EPA VOC regulations (2026) are accelerating the phase-out of traditional solvent-based glazing systems.

China Faux Finish Coatings Market: Liquid Stone and Graphene Integration Driving Scale Leadership

China is redefining the faux finish coatings market through large-scale adoption of liquid stone (ceramic-emulsion coatings), which replace traditional stone cladding while reducing structural load. Government mandates now require ~20% usage of lightweight decorative coatings in new high-rise developments.

Material innovation is a key strength. The commercialization of graphene-infused plasters is improving crack resistance and enabling electromagnetic shielding for smart buildings. Additionally, the expansion of AI-driven robotic application systems is enabling efficient large-scale deployment of complex multicolor finishes. Sustainability is also a priority, with investments in PFAS-free fluoropolymer faux coatings and widespread adoption of photocatalytic self-cleaning surfaces. These developments position China as the global leader in both scale and advanced material integration.

Germany Faux Finish Coatings Market: Circular Economy and Biocide-Free Chemistry Driving Sustainability

Germany leads Europe in sustainable faux finish coatings, driven by strict environmental regulations and circular economy principles. The development of biocide-free mineral coatings allows mold resistance without regulated chemical additives, aligning with updated REACH (2026) standards.

Innovation is focused on sustainable materials and digitalization. The commercialization of bio-attributed acrylic resins derived from organic waste is supporting premium faux finishes, while Digital Twin technology enables precise simulation of texture and reflectivity before production. Government subsidies under energy efficiency programs are also driving demand for thermal-insulative faux coatings with aerogel additives, combining aesthetics with performance. Additionally, pilot projects using recycled-monomer glazes are advancing circular economy goals.

Japan Faux Finish Coatings Market: Precision Engineering and Cultural Aesthetics Driving Innovation

Japan’s market is defined by high-precision application and fusion of traditional aesthetics with modern technology. Government initiatives are supporting development of hybrid-silica faux finishes that replicate traditional materials like Shikkui plaster while offering improved durability and seismic flexibility.

Technological advancements include sub-500 nm release films for transfer-based decorative applications and high-elongation elastomeric coatings (>800%) that maintain integrity during seismic events. Additionally, photocatalytic self-cleaning topcoats are reducing maintenance requirements, while healthcare-driven demand is increasing adoption of antiviral and warm-touch faux finishes in elderly care facilities. Energy-efficient innovations—such as heat-reflective glass coatings—are also contributing to reduced HVAC loads.

UAE Faux Finish Coatings Market: Desert-Grade Performance and Luxury Demand Driving Growth

The UAE is a key market for high-performance faux finishes, particularly in luxury construction and hospitality sectors. Government initiatives like the Dubai 2030 Retrofit Plan are driving demand for UV-stable, heat-reflective faux coatings across large-scale building upgrades.

Innovation is focused on durability under extreme conditions. New sand-resistant, non-tacky coatings prevent dust adhesion and maintain surface quality during frequent sandstorms. Regulatory frameworks—such as TVOC limits (≤300 µg/m³)—are accelerating the shift toward water-based systems, which now account for ~74% of premium faux-finish demand. Additionally, megaprojects like NEOM and Red Sea developments are driving adoption of high-reflectance faux-stone coatings, combining aesthetic appeal with energy efficiency. The hospitality sector is also boosting demand for metallic and decorative finishes in preparation for global events.

Faux Finish Coatings Market Report Scope

Faux Finish Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.8 Billion

|

|

Market Size (2032)

|

$14.6 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Finish Type (Wall Glazing, Plaster and Textures, Metallic and Pearlescent, Marbleizing and Stone, Wood Graining, Fabric and Leather Finishes, Patina and Distressed Finishes), By Technology (Water-based, Acrylic-based, Powder-based, Solvent-based, Bio-based), By Product Category (Glazes and Washes, Plasters and Trowel-Applied Finishes, Metallic Paints and Flakes, Stains and Dyes, Protective Topcoats and Varnishes), By Application Area (Walls and Ceilings, Furniture and Cabinets, Architectural Trim and Moulding, Flooring, Interior Accents and Decorative Objects), By End-Use Sector (Residential, Commercial), By Project Type (New Construction, Maintenance and Restoration), By Application Method (Trowel Applied, Brush and Roller Applied, Spray Applied, Specialty Tooling)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Benjamin Moore & Co., Faux Effects International Inc., RPM International Inc., Asian Paints Limited, Masco Corporation, Berger Paints India Limited, Kansai Paint Co., Ltd., Jotun A/S, Farrow & Ball Ltd., Sto SE & Co. KGaA, Meoded Decorative Paints & Plasters

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Faux Finish Coatings Market Segmentation

By Finish Type

- Wall Glazing

- Plaster and Textures

- Metallic and Pearlescent

- Marbleizing and Stone

- Wood Graining

- Fabric and Leather Finishes

- Patina and Distressed Finishes

By Technology

- Water-based

- Acrylic-based

- Powder-based

- Solvent-based

- Bio-based

By Product Category

- Glazes and Washes

- Plasters and Trowel-Applied Finishes

- Metallic Paints and Flakes

- Stains and Dyes

- Protective Topcoats and Varnishes

By Application Area

- Walls and Ceilings

- Furniture and Cabinets

- Architectural Trim and Moulding

- Flooring

- Interior Accents and Decorative Objects

By End-Use Sector

By Project Type

- New Construction

- Maintenance and Restoration

By Application Method

- Trowel Applied

- Brush and Roller Applied

- Spray Applied

- Specialty Tooling

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Faux Finish Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Benjamin Moore & Co.

- Faux Effects International Inc.

- RPM International Inc.

- Asian Paints Limited

- Masco Corporation

- Berger Paints India Limited

- Kansai Paint Co., Ltd.

- Jotun A/S

- Farrow & Ball Ltd.

- Sto SE & Co. KGaA

- Meoded Decorative Paints & Plasters

*- List not Exhaustive