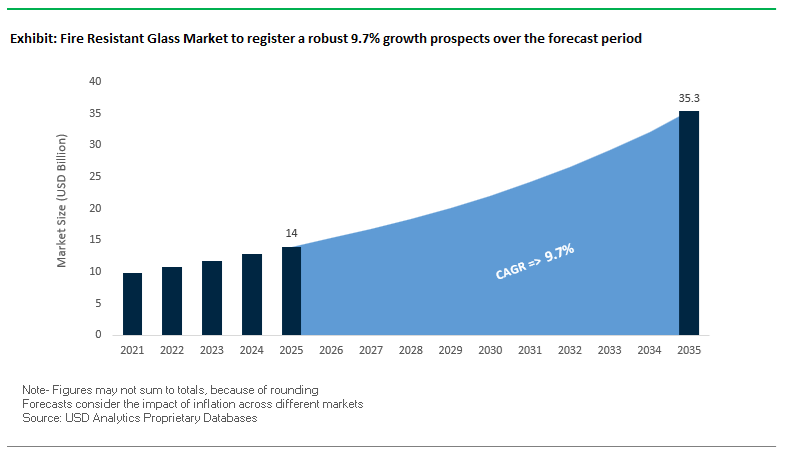

The Fire-Resistant Glass Market is poised to grow from USD 14 billion in 2025 to USD 35.3 billion by 2035, registering a strong CAGR of 9.7% between 2025 and 2035. For architects, façade consultants, and building code authorities, the market increasingly sits at the intersection of fire safety compliance, energy-efficient façades, and sustainable, low-carbon construction materials.

The global Fire-Resistant Glass Market is rapidly evolving from a niche compliance product category into a strategic pillar of high-performance building envelopes. In December 2025, AGC’s Low-Carbon Pyrobel Glass launch underscored how sustainability is becoming a core differentiator in fire-rated glazing, with architects and developers increasingly seeking low-embodied-carbon Fire-Resistant glass for green building certifications. The move builds on earlier collaborative initiatives including the November 2024 partnership between AGC and a European window fabricator to deliver a pre-tested timber-frame system with Pyrobel EW glass, simplifying certification for wooden fire-rated doors and partitions and supporting sustainable construction practices. In parallel, March 2025 saw SCHOTT AG committing EUR 50 million to expand its glass-ceramic facility in Germany for large-format PYRAN® S production, signaling strong confidence in monolithic glass-ceramic solutions for large-area façades and industrial applications.

Performance and regulatory escalation remain key growth vectors. In November 2025, Vetrotech Saint-Gobain secured a major contract to supply more than 15,000 m² of EI 120-rated CONTRAFLAM butt-joint glazing for a high-speed rail terminal in Southeast Asia, demonstrating how infrastructure projects are embracing frameless EI systems for both aesthetics and safety. Meanwhile, a January 2025 certification from a US fire testing laboratory—extending a gel-filled laminated fire glass system from 90-minute to 120-minute EI rating—expanded the applicability of such products to high-risk shafts and fire compartments, directly influencing specification patterns in high-rise and critical buildings. On the functional side, May 2025 brought Pilkington’s integration of advanced thermal insulation and solar control coatings into its Pyrostop® range, aligning Fire-Resistant glass with energy-efficient façades and tightening building energy codes.

Digitalization is emerging as a structural trend. In October 2024, Pilkington (NSG Group) showcased IoT-enabled sensors embedded in its Fireframes® steel curtain wall systems, capable of monitoring temperature and structural integrity in real time. The innovation supports predictive maintenance, improves lifecycle performance documentation, and provides asset owners with continuous insight into the condition of their fire-rated façades. Together, these developments demonstrate that the Fire-Resistant Glass Market is not just responding to regulatory pressure but is leveraging material science, sustainability, and digital technologies to create differentiated, high-value solutions for transport hubs, data centers, commercial towers, and public infrastructure.

Demand is being driven by stricter building codes, premium infrastructure projects, and the shift toward multi-functional fire-rated glazing systems that combine EI (Integrity and Insulation) and EW (Integrity and Radiation Control) performance with high transparency and impact safety. Industry buyers are asking whether Fire-Resistant glass can simultaneously deliver stringent fire ratings (up to EI 120), maintain daylighting, reduce radiant heat, and integrate into complex façade geometries and timber frames—current product portfolios from leading manufacturers largely answer “yes” to all of these requirements.

Beyond life safety, the market is being reshaped by sustainability and low-carbon Fire-Resistant glass, with manufacturers introducing reduced-embodied-carbon ranges and leveraging renewable energy in production. Further, digitalization and IoT-enabled fire-rated systems support real-time monitoring of critical façades and fire barriers, while new certifications extending EI ratings from 90 to 120 minutes unlock higher-value applications including shaft enclosures, rail terminals, and data-intensive public buildings. As multi-laminated, gel-filled, and ceramic-based Fire-Resistant glass continues to improve in visible light transmission, impact resistance, and large-format feasibility, the market is progressively moving away from purely utilitarian fire safety products toward architectural-grade, design-led fire-rated glazing solutions.

- Stringent performance classes (EI/EW) are core growth drivers, with EI 120-rated systems increasingly specified for high-risk zones, transport hubs, and vertical circulation areas.

- Radiation control and temperature limits are critical selection criteria, with EW glazing engineered to keep radiant heat below 15 kW/m² and EI products limiting surface temperature rise to 140°C above ambient.

- Impact safety is non-negotiable, with many multi-laminated fire-rated glass solutions achieving CPSC Category II ratings while still delivering up to 120-minute fire protection.

- Aesthetic and daylighting requirements remain high, with low-iron, high-VLT (>80%) intumescent glazing enabling transparent, open designs without compromising passive fire protection.

- Glass-ceramic systems enable very large panes and minimal framing, thanks to high softening points and self-supporting behavior under fire, supporting frameless and butt-jointed configurations in modern façades.

Code-Driven Upgrades and Multi-Functional Innovation Redefining the Fire-Resistant Glass Market

Trend 1 - EI-Class Fire-Resistant Glazing Becomes Mandatory for Compartmentation in Tall and Complex Buildings

Post-Grenfell regulatory reforms have fundamentally shifted glazing requirements in tall buildings, mandating the use of insulation-class (EI-rated) fire-resistant glass instead of basic integrity-only (E-class) systems. Under the UK Building Safety Act 2022 and stricter enforcement of Approved Document B, EI-class glass is now required in high-rise stairwells, evacuation corridors, and fire-protected shafts to ensure safe evacuation during fire events.

EI60-rated glazing is now common, driven by regulatory limits on temperature rise. As mandated, the non-fire side temperature must remain below an average of 140°C and a peak of 180°C, ensuring escape routes remain walkable and free from flashover. This performance requirement elevates EI-rated glass to the level of fire-resistive barrier walls, reflecting its critical role in building compartmentation.

Large commercial complexes and super-tall structures increasingly require unrestricted glazed areas in fire-rated assemblies-something not permitted with E-class systems. EI-rated glass enables architects to design expansive transparent fire partitions without the traditional 25% area limitation imposed on integrity-only solutions. This material freedom is driving specification growth in atriums, lobbies, transport hubs, and mixed-use developments.

The insulation performance of EI glazing results from multilayer constructions, often involving borosilicate glass and high-performance intumescent interlayers. Premium products achieve EI120 ratings, offering extended heat-blocking capability for mission-critical infrastructure such as hospitals, data centers, airports, and government buildings.

Trend 2 - Integration of Fire-Resistant Glass into Lithium-Ion BESS Safety Systems

The global proliferation of Lithium-Ion Battery Energy Storage Systems (BESS), combined with increasing thermal runaway incidents, has driven demand for highly specialized fire-resistant glass capable of withstanding extreme thermal and pressure conditions.

UL 9540A remains the definitive test standard for assessing the fire propagation risk in BESS installations across the US and Canada. Under this standard, any viewing window or inspection port incorporated into BESS enclosures must be certified to withstand the high-temperature thermal runaway, rapid gas release, and pressure spikes generated during cell failure events. Fire-resistant glass now forms an essential component of safe BESS enclosures.

Because solid barriers obstruct inspection, fire-rated viewports have become critical for real-time visual assessment by firefighters and operators. These windows allow safe monitoring of early thermal runaway indicators without compromising the enclosure’s fire boundary or explosion-containment capabilities-two essential requirements reinforced by the 2025 edition of UL 9540A, which integrates the propagation prevention criteria of NFPA 855.

High-risk BESS installations in commercial buildings, substations, and microgrids increasingly specify fire-resistant glass as part of multi-layered passive fire protection systems designed to contain fires, prevent horizontal spread, and mitigate deflagration hazards. The evolution of safety standards and the rapid scaling of grid storage projects ensure continued demand for advanced fire-resistant glass in energy infrastructure.

Opportunity 1 - Smart, Switchable EI-Class Fire Glass for Dynamic Partitions in High-Value Buildings

A major emerging opportunity lies in the development of “switchable” fire-rated glass systems that combine mandatory EI-class fire protection with dynamic smart-building functionality. This dual-performance approach directly responds to the demand for multi-functional partitions in premium commercial, healthcare, and institutional environments.

Academic and industrial R&D is converging around the integration of electrochromic (EC) layers-capable of adjusting transparency and light transmission-within EI-rated glazing assemblies. The future product roadmaps envision fire-resistive smart glass that maintains full EI performance whether the EC layer is transparent, tinted, or unpowered.

Smart glazing is already proven to reduce cooling loads by 30% or more through dynamic solar control. Integrating this with EI-rated fire performance creates a high-value product that simultaneously addresses energy efficiency, occupant comfort, privacy, and life safety, making it ideal for hospitals, airports, high-end offices, research labs, and hospitality environments.

Privacy functionality is another differentiator. Technologies such as polymer-dispersed liquid crystal (PDLC) films enable instant switching between transparent and opaque modes-an invaluable feature for meeting rooms, medical exam rooms, secure facilities, and data centers. Embedding these capabilities into fire-rated architectures allows designers to meet stringent compartmentation codes without sacrificing flexibility or aesthetics.

This fusion of smart technology and advanced fire-protection performance represents one of the most commercially promising innovation avenues in the fire-resistant glazing market.

Opportunity 2 - Lightweight, Ballistic-Resistant Fire Glass for High-Security and Public Infrastructure

The convergence of physical security threats and fire safety requirements is accelerating demand for multi-threat, high-performance fire-resistant glass in public buildings, transit hubs, government facilities, embassies, schools, and high-security commercial complexes.

Security-driven installations increasingly require glazing that offers UL Level 3 ballistic resistance, capable of stopping three .44 Magnum rounds, while also providing EI60 or higher fire resistance. Meeting both threat categories in a single composite system presents significant engineering complexity and creates a premium market segment.

Manufacturers are addressing this through hybrid constructions combining laminated polycarbonates, glass-ceramic layers, and specialized interlayers that dissipate ballistic energy without compromising fire insulation performance. These systems are designed to resist forced entry, withstand thermal shock, and maintain compartmentation integrity under extended fire exposure.

A key innovation focus is on weight reduction. Conventional laminated security glass is extremely heavy, complicating installation and limiting retrofitting potential. Newer glass-clad polycarbonate composites deliver equivalent or superior performance at significantly reduced thickness and weight. This enables easier installation, lower structural load, and compatibility with existing door and window frames-an essential requirement for modernizing aging public infrastructure.

The rise in security-focused architecture, combined with stricter fire safety standards, positions lightweight ballistic fire glass as a high-growth market opportunity for specialized glazing manufacturers.

Fire-Resistant Glass Market Share Analysis

Market Share by Fire Class & Rating: EI-60 Fire-Resistant Glass Leads Through Regulatory Alignment and Superior Thermal Protection

The EI 60-minute fire-resistant glass segment, holding a 28% market share, leads the Fire-Resistant Glass Market because it represents the globally accepted minimum safety benchmark for protecting escape routes in commercial, institutional, and high-occupancy buildings. Its dominance is directly linked to stringent fire safety codes that require corridor and stairwell enclosures to maintain both Integrity (E) and Insulation (I), ensuring the barrier prevents flame spread while also restricting heat transfer to safe levels. EI-rated glass must keep the non-fire side below a 140°C average and 180°C peak, which is critical for preventing ignition of nearby combustibles and avoiding severe radiant heat exposure that could render evacuation routes unusable. These performance requirements support the broader movement toward performance-based fire engineering, where radiant heat control is viewed as just as important as structural integrity. While cheaper classifications such as “E” or “EW” glass may satisfy basic integrity needs, they fail to limit radiant heat, making them unsuitable for most life-safety pathways. As architects increasingly demand transparent façade elements and larger glazed zones without compromising safety, EI 60 glass emerges as the optimal balance of cost, protection, and design flexibility, enabling compliance with international fire codes while supporting modern architectural aesthetics.

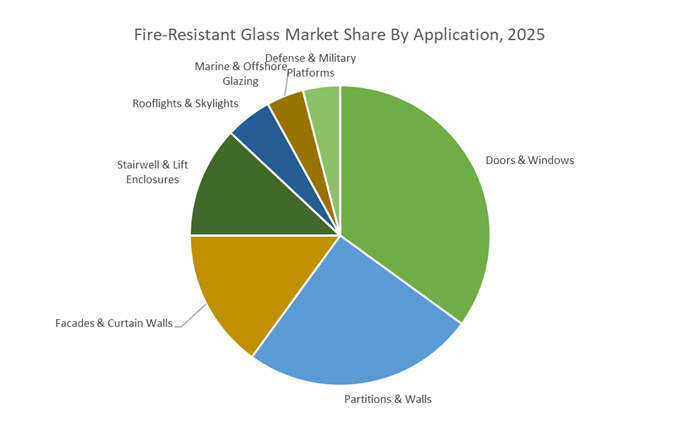

Market Share by Application: Doors & Windows Dominate Due to High Installation Volume and Stringent Opening-Protection Requirements

Doors & Windows, holding a commanding 35% share, represent the largest application segment because they are inherently the most vulnerable points within fire-rated barriers and thus face the tightest regulatory scrutiny. Fire-resistant glazing in these openings—particularly door vision panels, stairwell windows, corridor glazing, and perimeter wall openings—must meet fire-resistance standards as complete assemblies, with the glass typically determining the achievable rating. Because modern buildings incorporate a high density of functional openings to support occupant visibility, daylighting, and architectural flow, the cumulative square footage of fire-rated doors and windows far exceeds that of specialized installations such as fire-rated rooflights or façade-specific systems. Code frameworks such as the International Building Code (IBC) and NFPA provisions often restrict the allowable size of lower-performance ceramic or fire-protective glass (sometimes to <100 square inches in 60- or 90-minute fire doors), compelling builders to adopt higher-performance EI-rated fire-resistive glass to achieve full-vision doors, large window panels, or continuous glazing lines. As contemporary architectural designs increasingly prioritize transparency and large glazing spans while still requiring full compartmentation performance, the demand for fire-resistant glass in doors and windows continues to accelerate, reinforcing this segment’s leadership in the overall market.

Country Analysis: Global Fire-Resistant Glass Development Hubs

United Kingdom: Regulatory Overhaul Accelerating Demand for Non-Combustible Laminated Fire-Resistant Glass

The United Kingdom is undergoing one of the most significant regulatory transformations in its building safety history, fundamentally reshaping demand for non-combustible laminated fire-resistant glass. Following the Building Safety Act 2022 and updated Approved Document B (March 2025), the U.K. has tightened fire safety accountability for architects, developers, and building owners—particularly in high-rise residential construction. One of the most impactful regulatory shifts is the lowered ban threshold for combustible materials on external walls and balconies to 11 meters, effectively eliminating the use of conventional laminated glass containing PVB interlayers, which are considered combustible under the revised framework. This shift is redirecting the market toward A2-classified fire-resistant glazing, necessitating advanced interlayer technologies capable of achieving non-combustible performance.

Innovation is rapidly following regulation. Pyroguard’s launch of its intumescent gel-based laminated glass, achieving A2 reaction-to-fire classification, has redefined the specification landscape for high-rise balconies and façade elements. This development comes alongside a broader U.K. movement to replace outdated British fire test standards with more stringent European EN fire test standards, accelerating market adoption of cuttable, certifiable, EN-compliant safety glass. Key applications driving this surge include escape routes, fire-protected lobbies, stair enclosures, and external balustrades, all of which now require verified non-combustible laminated glass solutions. Reinforcing domestic production, Pyroguard has invested in an additional manufacturing line at its Haydock facility to support output of its Pyroguard Advance series—engineered to meet the latest EN classifications. The U.K. is thus emerging as a regulatory-driven innovation hub for next-generation, non-combustible fire-resistant glazing.

European Union: EI-Class Fire Resistance and Low-Carbon Glazing Driving Sustainable Fire-Resistant Glass Adoption

The European Union Fire-Resistant Glass Market is shaped overwhelmingly by its dual emphasis on fire performance (EI classifications) and sustainability, tied closely to the European Green Deal and the revised Energy Performance of Buildings Directive (EPBD). As EU member states prepare to fully transpose the EPBD into national legislation by May 2026, demand for highly insulating, energy-efficient fire-resistant glazing is strengthening across both new construction and large-scale renovation projects. This includes EI-rated systems capable of delivering both Integrity (E) and Insulation (I) performance, essential for compartmentation in public infrastructure and high-occupancy buildings.

European manufacturers are responding with low-carbon innovation. AGC Glass Europe’s Low-Carbon Pyrobel (2024) achieves a 45–50% reduction in embodied carbon by combining refined production processes, low-carbon float glass, and renewable energy. This aligns perfectly with the EU’s sustainability objectives while preserving full fire-resistant performance. Multi-functional glazing is also rising in importance, with AGC’s Pyrobel 16 BR4NS and Pyrobel 42 BR4NS—released in 2025—delivering EI 30/EI 90 fire protection alongside P8B break-in resistance for security-critical sites such as embassies, banks, airports, metro stations, and medical facilities. Across the EU, strict enforcement of ERP (Establishments Receiving Public) safety protocols is driving broad specification of fire-resistant glass in high-traffic environments. The region’s integration of sustainability and fire performance is making Europe a global benchmark for eco-efficient, multi-functional fire-resistant glass systems.

United States: Large-Format Ceramic Fire-Rated Glass and IBC-Driven Compliance Shape Market Direction

The United States continues to rely heavily on ceramic fire-resistant glass technologies, shaped by widespread adoption of the International Building Code (IBC) and fire marshal–led enforcement of high-performance glazing in life-safety zones. The U.S. market demands fire-resistant glass capable of withstanding high temperatures while maintaining optical clarity—making ceramic fire-rated glass a preferred solution for stairwells, corridors, fire barriers, and horizontal exits. Technical Glass Products (TGP) remains a key innovator, with enhancements to its FireLite® ceramic glass using ultraHD® Technology, delivering improved clarity, color neutrality, and surface quality in large-format sizes while achieving 90-minute and higher fire ratings. These properties make FireLite® highly desirable for architects who require both aesthetics and life safety.

Regulatory momentum also supports retrofit demand. As older educational institutions, commercial properties, and healthcare facilities undergo compliance reviews aligned with IBC and NFPA standards, the market is seeing rising replacement volumes of fire-rated doors, sidelights, windows, and interior partitions. The emphasis on both EW (radiant heat control) and EI (full insulation) classifications is expected to intensify as U.S. jurisdictions adopt more stringent fire protection frameworks. Driven by ceramic innovation, performance-based code adoption, and increased retrofit activity, the U.S. market remains a core global hub for large-format, code-compliant fire-resistant glass technologies.

Japan: Advanced Ceramic Glass Technologies and Transportation Safety Fuel Demand for High-Reliability Fire-Resistant Glazing

Japan’s Fire-Resistant Glass Market is defined by its advanced material science leadership, with strong specialization in transparent glass-ceramics engineered for extreme thermal stability. Companies such as Nippon Electric Glass (NEG) are globally recognized for producing fire-resistant glass-ceramics with ultra-low thermal expansion, enabling exceptional performance under rapid temperature rise—an essential requirement for high-hazard environments. These materials maintain structural integrity in prolonged fire exposure, making them ideal for critical infrastructure applications.

Japan’s transportation sector—particularly high-speed rail and marine systems—drives major demand for specialized fire-resistant glazing. Safety protocols for Shinkansen rail systems and commercial marine vessels require bespoke fire-resistant partitions, viewing panels, and control room barriers to protect passengers and sensitive equipment. With stringent national fire codes governing public transport, Japanese manufacturers continue to supply precision-engineered, high-reliability glazing that withstands vibration, pressure changes, and severe thermal loads. Japan’s fusion of material science excellence and transportation safety requirements positions it as a global leader in high-performance ceramic fire-resistant glass for mission-critical environments.

Competitive Landscape: Global Fire-Resistant Glass Manufacturers Scale EI Solutions and Low-Carbon Portfolios

The competitive landscape in the Fire-Resistant Glass Market is defined by a combination of deep material science expertise, certification breadth across EI/EW classes, and system-level integration capabilities. Leading players are moving beyond standalone fire-rated glass panes to offer fully tested glazing systems, including frames, sealants, and hardware, ensuring end-to-end compliance with EN 13501-2, ASTM, and local building codes. Strategic investments in low-carbon manufacturing, large-format production, and multi-functional coatings are enabling suppliers to align Fire-Resistant glass with ESG targets, energy performance requirements, and architectural design flexibility. Further, system integrators and framing specialists are creating complete curtain wall and partition solutions that simplify specification and approval for architects, specifiers, and fire consultants.

Vetrotech Saint-Gobain is a leading global provider of comprehensive fire and security glazing systems, with core brands including CONTRAFLAM® (EI-rated insulated glass) and PYROSWISS® (E-rated integrity-only glass). Its strategic focus is on multi-functional Fire-Resistant glass, often combining fire protection with security, blast resistance, or bullet resistance in one solution. Vetrotech’s VDS steel framing systems are fully tested with their glass, giving customers complete, compliant system packages. A major highlight is the promotion of CONTRAFLAM Structure butt-jointed EI glazing, which enables frameless, highly aesthetic fire barriers for rail terminals, airports, and commercial atria, illustrated by the large EI 120 contract awarded in Southeast Asia in November 2025.

SCHOTT AG specializes in glass-ceramic and composite fire-resistant glass, with flagship brands like PYRAN® (monolithic borosilicate glass-ceramic for E/EW) and PYRANOVA® (laminated composite glass for EI). Its competitive edge lies in advanced material science, where PYRAN®’s borosilicate composition provides superior thermal shock resistance and eliminates the risk of NiS (nickel sulphide) inclusions and spontaneous breakage. In March 2025, SCHOTT announced a EUR 50 million investment in its German glass-ceramic facility to expand production of large-format PYRAN® S sheets, targeting high-demand applications in façades, industrial fire screens, and transportation. The capacity expansion positions SCHOTT as a key supplier for projects requiring large, self-supporting Fire-Resistant glass-ceramic panes.

Pilkington, part of the NSG Group, offers a broad portfolio of intumescent and tempered fire-rated glazing under brands including Pilkington Pyrostop® (EI-rated insulating glass) and Pilkington Pyrodur® (EW-rated glass limiting heat radiation). A major strategic focus is on integrating Low-E and solar control coatings into its fire-rated products, enabling façades that meet both fire safety and energy efficiency targets. In May 2025, Pilkington implemented next-generation coating technology across its fire-resistant glass range, improving U-values and solar control without compromising fire performance. The company is also an early mover in IoT-enabled Fireframes® curtain wall systems, showcased in October 2024, which embed sensors to continuously monitor façade temperature and structural behavior under stress.

AGC Inc. is a major supplier of laminated and ceramic fire-resistant glass with its Pyrobel® brand serving both EI and EW classifications. AGC’s strategic differentiation lies in its strong sustainability agenda and high light-transmission performance, making Pyrobel suitable for daylight-intensive, design-led architecture. In December 2025, AGC launched its Low-Carbon Pyrobel Glass range, using renewable energy and alternative raw materials to significantly cut embodied carbon, an important feature for green building and ESG-focused projects. Earlier, in November 2024, AGC partnered with a European window fabricator to deliver a pre-tested timber-frame Pyrobel EW system, simplifying certification for fire-rated timber doors and partitions and aligning with the push toward bio-based, sustainable construction systems.

Technical Glass Products (TGP), part of Allegion, operates as a specialist system integrator and fabricator of fire-rated glazing solutions, leveraging glass from major producers including Pilkington and combining it with its proprietary Fireframes® steel and aluminum framing systems. TGP’s competitive strength is offering fully tested, single-source fire-rated curtain wall and door systems, including the Fireframes Curtain Wall Series with ratings up to 120 minutes. Its innovations include the Fireframes ClearFloor® System, enabling 60/120-minute fire-rated glass floors that also meet safety glass standards, opening new design possibilities for atria, viewing areas, and multi-level architectural features. The system-driven approach simplifies specification and approval, making TGP a preferred partner for complex, high-profile fire rated glass projects.

Fire Resistant Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14 Billion

|

|

Market Size (2035)

|

$35.3 Billion

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Fire Class (E, EW, EI), By Product Type (Laminated Fire-Resistant Glass, Ceramic Fire-Resistant Glass, Wired Glass, Tempered Fire-Resistant Glass), By Application/Use Case (Doors & Windows, Partitions & Walls, Facades & Curtain Walls, Stairwell & Lift Enclosures, Rooflights & Skylights, Marine & Offshore Glazing, Defense & Military Platforms), By Framing System (Steel Frame Systems, Timber Frame Systems, Aluminum Frame Systems, Composite Frame Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AGC Glass Europe, SCHOTT AG, NSG Group (Pilkington), Pyroguard, Technical Glass Products, Saint-Gobain, Nippon Electric Glass, Promat International, Vetrotech Saint-Gobain, McGrory Glass, Fuso Glass India Pvt. Ltd., Glaston Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fire-Resistant Glass Market Segmentation

By Fire Class

- E (Integrity)

- EW (Integrity & Radiation Control)

- EI (Integrity & Insulation)

- Fire Ratings: 30, 60, 90, 120 minutes

By Product Type

- Laminated Fire-Resistant Glass

- Ceramic Fire-Resistant Glass

- Wired Glass

- Tempered Fire-Resistant Glass

By Application / Use Case

- Doors & Windows

- Partitions & Walls

- Facades & Curtain Walls

- Stairwell & Lift Enclosures

- Rooflights & Skylights

- Marine & Offshore Glazing

- Defense & Military Platforms

By Framing System

- Steel Frame Systems

- Timber Frame Systems

- Aluminum Frame Systems

- Composite Frame Systems

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Fire-Resistant Glass Market

- AGC Glass Europe

- SCHOTT AG

- NSG Group / Pilkington

- Pyroguard

- Technical Glass Products (TGP)

- Saint-Gobain

- Nippon Electric Glass (NEG)

- Promat International

- Vetrotech Saint-Gobain

- McGrory Glass

- Fuso Glass India Pvt. Ltd.

- Glaston Corporation

*- List not Exhaustive