Fire Resistant Tapes Market Growth Driven by EV Safety Requirements, Halogen-Free Innovation, and High-Performance Adhesive Technologies

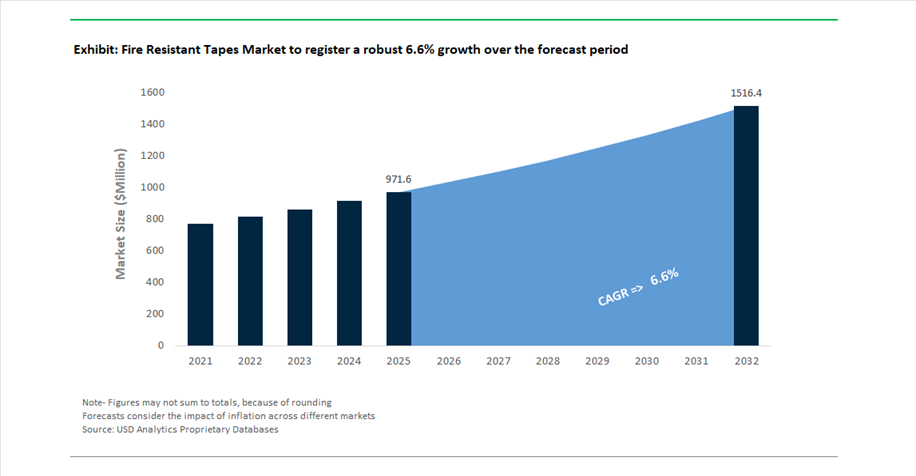

The global Fire Resistant Tapes Market was valued at USD 971.6 million in 2025 and is projected to grow at a CAGR of 6.6% between 2025 and 2032, reaching USD 1.52 billion by 2032. This growth is primarily driven by the increasing need for thermal management, fire safety, and electrical insulation solutions across electric vehicles (EVs), aerospace, construction, and industrial equipment sectors.

Fire resistant tapes are critical components in systems where flame retardancy, dielectric strength, and heat resistance are required to prevent fire propagation and maintain operational integrity. A major growth driver is the rapid expansion of the electric mobility ecosystem, where tapes are used in battery packs, wire harnesses, and high-voltage systems. These applications demand materials capable of withstanding thermal runaway events, high temperatures, and electrical stress, positioning advanced adhesive tapes as a key safety layer.

Another structural trend is the tightening of fire safety regulations and environmental standards, particularly in Europe and North America. This is accelerating the transition toward halogen-free, low-smoke zero halogen (LSZH) materials, which reduce toxic emissions during fire incidents. Additionally, the increasing adoption of multi-functional tapes that combine fire resistance with chemical, moisture, and mechanical protection is expanding their application scope across harsh industrial environments.

EV-Focused Tape Innovation, AI-Driven Quality Control, and Halogen-Free Material Transition Reshape Market Dynamics

The fire resistant tapes market is undergoing rapid transformation driven by electrification trends, sustainability mandates, and advanced manufacturing technologies. In August 2025, tesa SE introduced tesa® 67003, a high-performance tape specifically engineered for EV wire harness protection. This product provides a critical barrier against thermal runaway, ensuring electrical systems remain functional during high-heat events, a key safety requirement in modern electric vehicles.

Product innovation in EV battery systems is accelerating across the industry. In March 2024, Nitto Denko expanded its portfolio with silicone-based fire-retardant tapes, offering enhanced dielectric strength and flame resistance for high-voltage battery environments. The company further strengthened its position by implementing AI-driven “Digital Twin” quality control systems in January 2026, enabling real-time monitoring of adhesive properties and flame-retardant dispersion to ensure consistent product performance in critical applications.

Sustainability is emerging as a defining innovation theme. By January 2026, leading manufacturers including 3M and tesa SE scaled up halogen-free fire retardant tape systems, replacing traditional brominated flame retardants with phosphorus-based and mineral-based alternatives. This transition is driven by tightening REACH regulations and the growing demand for low-toxicity materials in public transportation, data centers, and building infrastructure.

Industrial and aerospace applications are also benefiting from multi-functional innovation. In October 2025, 3M announced increased R&D investment in multi-functional fire-resistant tapes, combining flame resistance with water repellency and chemical durability. These solutions are designed for extreme environments such as oil & gas facilities and aerospace systems, where materials must withstand high heat, pressure, and corrosive exposure.

Regional manufacturing expansion is strengthening supply chains. In September 2025, Avery Dennison expanded its production capacity in Mexico to support nearshoring trends in North America, particularly for automotive and appliance applications requiring fire-resistant adhesive tapes. Additionally, Scapa (part of Mattr) expanded its European footprint in July 2024, focusing on glass cloth and Nomex-based tapes for aerospace and defense sectors.

Construction applications are also evolving. In April 2025, Avery Dennison introduced AAMA-certified flashing and sealing tapes, designed to enhance fire-safe building envelopes by maintaining structural integrity and preventing smoke infiltration under high-temperature conditions.

Mica-Based Fire Resistant Tapes Enabling Thermal Runaway Protection in EV Battery Systems

The rapid expansion of electric vehicle production is significantly influencing the fire resistant tapes market, with mica-based thermal barrier tapes emerging as a critical safety component in lithium-ion battery packs. OEMs are prioritizing these materials to mitigate thermal runaway propagation between cells and modules in high-energy-density battery architectures. Phlogopite mica-based tapes offer exceptional thermal resistance, maintaining structural and dielectric integrity at continuous temperatures up to 1,000°C, even under direct flame exposure during battery venting events. This performance is essential for ensuring passenger safety and compliance with stringent EV safety regulations. In addition to thermal protection, these tapes provide dielectric breakdown strength exceeding 20 kV/mm, preventing electrical short circuits during high-temperature incidents. The integration of mica tapes also supports design optimization, enabling a reduction of approximately 30% in insulation volume compared to conventional ceramic-based barriers, thereby improving overall battery energy density. Testing data from 2025 and 2026 EV platforms confirms compliance with UL 94 V-0 flammability standards, with zero flame penetration for more than 15 minutes. These capabilities are positioning mica-based fire resistant tapes as a foundational technology in next-generation EV battery safety systems, supporting both performance and regulatory compliance requirements.

Aerospace Adoption of Radiation-Crosslinked Fire Resistant Tapes for High-Performance Wiring Systems

The aerospace sector is transitioning toward radiation-crosslinked fire resistant tapes, particularly those based on ETFE, to meet increasingly stringent requirements for chemical resistance, mechanical durability, and fire safety in aircraft systems. Electron-beam crosslinking technology enhances the molecular structure of tape backings, resulting in significantly improved resistance to aviation fluids such as Skydrol hydraulic fluid and jet fuel, with performance exceeding conventional solvent-cured tapes by more than 50% in long-term exposure tests. These tapes also maintain mechanical flexibility and fire-resistant properties across a wide operating temperature range from -65°C to 200°C, making them suitable for demanding environments such as engine nacelles and avionics compartments. Abrasion resistance is a critical performance parameter in aerospace wiring applications, and crosslinked tapes demonstrate up to four times greater resistance to mechanical wear compared to traditional alternatives, ensuring long-term reliability in high-vibration conditions. Additionally, compliance with stringent safety standards such as FAR 25.853 and Airbus ABD0031 requires minimal smoke generation and low toxicity during combustion, a requirement effectively met by modern crosslinked fire resistant tapes. These advancements are reinforcing the adoption of high-performance tape solutions in aerospace applications where safety, durability, and regulatory compliance are paramount.

China’s Fire-Stopping Regulations Driving Demand for Intumescent Fire Resistant Tapes in High-Rise Buildings

China’s strengthened enforcement of fire-stopping regulations for building penetrations is creating a significant growth opportunity for intumescent fire resistant tapes in the construction sector. Updates to the GB 50016 code require that all service penetrations, including plastic pipes and cable trays in high-rise buildings, incorporate fire-stop materials capable of preventing flame and smoke propagation. Intumescent tapes, particularly graphite-based formulations, are engineered to expand up to 25 times their original volume when exposed to high temperatures, effectively sealing gaps and maintaining compartmentalization during fire events. The scale of urban development in China, coupled with a focus on ultra-high-rise safety, has driven approximately 20% growth in the specification of these materials for new construction projects. In addition to new builds, government-led initiatives targeting the renovation of older urban communities are creating substantial retrofit demand, where adhesive-backed fire resistant tapes provide a practical and cost-effective solution for upgrading existing infrastructure. Certification requirements are also becoming more stringent, with manufacturers needing to meet three-hour fire resistance ratings under GB 23864 standards to qualify for public sector tenders. These regulatory and infrastructure dynamics are positioning intumescent fire resistant tapes as a critical component in modern fire safety systems within rapidly urbanizing regions.

US Navy Lithium-Ion Battery Programs Driving High-Performance Fire Resistant Tape Demand

The modernization of naval energy systems, particularly the transition to lithium-ion battery technology in submarine platforms, is generating a high-value opportunity for advanced fire resistant tapes. The U.S. Navy’s safety requirements, defined under NAVSEA standards, emphasize the need for fire-blocking and thermally stable materials capable of preventing cascading cell failures in confined environments. Fire resistant pressure-sensitive adhesive tapes are increasingly specified for internal battery stabilization, offering both mechanical support and thermal insulation. A key requirement in submarine applications is low smoke and toxicity emission, driving the adoption of halogen-free tape chemistries that prevent the release of corrosive gases during thermal incidents. Additionally, these tapes must maintain full adhesive integrity under extreme environmental conditions, including prolonged exposure to salt spray, with performance benchmarks requiring 100% bond strength retention after 1,000 hours of testing. Funding allocations under the 2026 defense budget for submarine power and propulsion systems are supporting research and procurement of advanced thermal insulation materials, including fire resistant tapes designed for lithium-ion battery systems. These developments are positioning the defense sector as a strategic growth avenue for high-performance fire resistant tape technologies.

Fire Resistant Tapes Market Share 2025: Single-Coated Tapes and PSA Technology Lead Demand

Coating Type Insights: Single-Coated Tapes Dominate with Cost Efficiency and EV Adoption

The single-coated tapes segment holds a leading 55% market share in the fire resistant tapes market in 2025, driven by its cost-effectiveness and ease of application across multiple industries. These tapes, featuring adhesive on one side and a fire-resistant substrate such as mica or fiberglass on the other, are widely used for wire harnessing, cable wrapping, and HVAC duct sealing. Their simple design reduces material usage and installation complexity, making them a preferred choice in both industrial and construction applications. A significant growth driver is the rapid expansion of the electric vehicle (EV) market, particularly in Asia-Pacific, where single-coated fire resistant tapes are increasingly used for battery module insulation, thermal barriers, and busbar wrapping. Their ability to provide reliable flame resistance and electrical insulation under high temperatures is accelerating adoption in next-generation mobility solutions, reinforcing their dominant market position.

Technology Insights: Pressure-Sensitive Adhesives (PSA) Lead with Fast Application Benefits

The pressure-sensitive tapes (PSA) segment dominates the fire resistant tapes market with a 62% share in 2025, owing to its superior convenience and performance in high-temperature applications. PSA tapes provide instant bonding without the need for heat or water activation, making them ideal for field repairs, aerospace wiring systems, construction joints, and industrial maintenance tasks where speed and efficiency are critical. The growing use of silicone-based PSA adhesives is further enhancing market growth, as these materials maintain strong adhesion and thermal stability at temperatures ranging from 200°C to 300°C, outperforming traditional acrylic-based systems. This makes them particularly suitable for fire-rated applications such as oven seals, exhaust systems, and high-heat electrical insulation. As industries increasingly prioritize fast installation and reliable fire protection, PSA technology is expected to remain the backbone of innovation in the fire resistant tapes market.

Fire Resistant Tapes Market Competitive Landscape Driven by EV Battery Safety, PFAS-Free Innovation, and High-Performance Adhesive Technologies

The fire resistant tapes market is highly competitive, driven by demand from EV batteries, aerospace interiors, electronics, and green construction. Key players are focusing on PFAS-free adhesives, flame-retardant materials, and multifunctional tapes integrating thermal management, EMI shielding, and sustainability compliance.

3M leads fire resistant tapes market with EV battery safety solutions and rapid-install fire barrier technologies

3M Company is a dominant player in the fire resistant tapes market, driven by innovation in fire-stop and dielectric tape solutions. In 2026, it formed a strategic joint venture integrating suppression technologies with its Scotch® fire protection portfolio. Its Fire and Water Barrier Tape (FWBT) delivers instant smoke and sound protection, meeting ASTM E2307 and E814 standards with up to 500% stretch for demanding construction joints. 3M is leading in EV battery safety with specialized tapes providing insulation and flame barriers in high-density battery architectures. Its products significantly reduce installation time by 35%, eliminating the need for traditional application tools. Fully LEED v4 compliant and VOC-free, 3M remains a preferred supplier for sustainable infrastructure projects.

Saint-Gobain advances fire resistant tapes with PFAS-free technologies and sustainable building solutions

Saint-Gobain is strengthening its position in the fire resistant tapes market through PFAS-free product innovation and sustainable adhesive technologies. The launch of SGP5 heat sealing tape offers continuous temperature resistance up to 260°C and short-term exposure up to 315°C, targeting medical and food-grade applications. Its 2555 PFAS-free composite molding tape provides a high-performance solution for aerospace manufacturing processes such as vacuum bagging and autoclave curing. The expansion of the Norseal® range supports modular construction with fire-resistant sealing systems featuring guided installation for improved airtightness. The company is also transitioning toward bio-attributed adhesives within its Norgard® portfolio. These initiatives align with growing regulatory pressure and sustainability demand in construction and industrial sectors.

Nitto Denko strengthens specialty fire resistant tapes with electronics and 5G-focused innovations

Nitto Denko Corporation holds a strong share in the Asian specialty tapes market, supported by expansion into India and Vietnam electronics manufacturing hubs. Its flame-retardant acetate and polyimide tapes are widely used in automotive wire harness systems, offering halogen-free chemistry and long-term thermal stability. The company has introduced PPS-based fire-resistant tapes designed for 5G infrastructure, combining EMI shielding with fire protection. Nitto is also developing dual-function tapes integrating thermal management capabilities for semiconductor applications. Its regional technical centers enable localized innovation and faster product deployment. This positions Nitto as a leader in high-performance electronic and industrial fire-resistant tapes.

Avery Dennison drives EV battery tape innovation with thermal runaway mitigation and PSA technologies

Avery Dennison Corporation is expanding its presence in the fire resistant tapes market through its EV battery venting materials portfolio, designed to mitigate thermal runaway risks. The company is scaling pressure-sensitive adhesive tapes with integrated flame retardants and biocides, enabling thin-profile bonding in high-temperature electronic environments. Its Performance Tapes segment is benefiting from strong growth in automotive and construction sectors, supporting a projected 7.2% growth rate. Avery Dennison leverages collaborative R&D with global OEMs to develop low-VOC fire-resistant solutions tailored for EV and electronics applications. Its global testing infrastructure enhances product customization and performance validation. These capabilities strengthen its position in advanced adhesive technologies.

tesa drives high-performance fire resistant tapes growth with aerospace-grade and solvent-free solutions

tesa SE is a key player in the fire resistant tapes market, focusing on high-performance specialty tapes within a global adhesive market valued at over $100 billion. Its flame-retardant tape series for aircraft interiors meets stringent FAR 25.853 safety standards, supporting applications in flooring and insulation bonding. The company is transitioning toward solvent-free coating technologies, targeting 80% conversion to water-based and hot-melt systems by late 2026. tesa is also integrating digital watermarking into its tapes to ensure traceability and compliance during aerospace maintenance operations. Partnerships with Tier-1 aerospace suppliers enhance its market reach. These innovations position tesa at the forefront of sustainable and high-performance fire-resistant tape solutions.

Scapa Group expands niche fire resistant tape applications with aerospace and marine-focused solutions

Scapa Group is strengthening its position in the fire resistant tapes market through specialization in aerospace and marine applications. The company offers halogen-free adhesive tapes with low smoke emission and high durability, widely used in aircraft interiors for carpet and insulation fixing. Its fire-retardant glass cloth tapes have been optimized for marine engine rooms, providing both flame resistance and vibration damping. Scapa has improved production efficiency with a 12% increase in throughput driven by AI-based coating control systems. Its products are engineered for harsh environments, offering combined waterproofing, chemical resistance, and electrical insulation. These capabilities position Scapa as a niche leader in high-reliability fire-resistant tape solutions.

China Fire-Resistant Tapes Market: EV Battery Safety and High-Temperature Innovation Driving Global Dominance

China is the global leader in fire-resistant tapes, particularly in mica-based insulation systems, driven by EV battery expansion and industrial safety mandates. Under the 15th Five-Year Plan (2026), industries must improve thermal insulation efficiency by ~25%, accelerating demand for advanced fireproof tapes.

Innovation is centered on high-temperature performance. The launch of nano-inorganic coated mica tapes enables fire resistance up to ~1100°C, while ceramic-fiber-backed tapes are being deployed to manage thermal runaway events in EV batteries. Additionally, graphene-enhanced adhesives are reducing coating thickness by ~30% without compromising fire ratings (V-0). Large-scale automation—especially in the Pearl River Delta—has increased production throughput by ~23%, reinforcing China’s scale advantage.

United States Fire-Resistant Tapes Market: EV Safety, Aerospace Innovation, and Regulatory Compliance Driving Growth

The U.S. market is focused on high-performance, multi-functional fire-resistant tapes, particularly for EVs, aerospace, and infrastructure. A key development is the launch of integrated battery venting tapes, combining fire resistance with pressure-relief functionality for EV battery systems.

Regulatory and technological shifts are shaping demand. Federal funding under the Infrastructure Investment and Jobs Act (IIJA) is driving use of glass cloth and Nomex tapes in grid modernization, while aerospace programs are investing in anisotropic fire-barrier tapes for lightweight aircraft and spaceports. Additionally, stricter PFAS regulations (2026) are accelerating the transition toward fluoropolymer-free tape systems, and semiconductor fabs are increasing demand for ultra-low outgassing fire tapes. Compliance with UL 510 standards is also pushing adoption of high-performance polyimide tapes for sustained flame resistance.

Germany Fire-Resistant Tapes Market: Halogen-Free Chemistry and Renewable Energy Driving Sustainability

Germany leads Europe in sustainable fire-resistant tapes, with a strong transition toward halogen-free formulations. By 2026, the market has achieved ~90% penetration of halogen-free fire tapes in public transportation systems, aligning with strict EU toxicity regulations.

Renewable energy and automotive sectors are major drivers. Offshore wind projects are deploying high-voltage mica-glass tapes for interconnectors exposed to thermal and saline stress, while EV manufacturers are adopting self-healing fireproof tapes for motor housings. Regulatory frameworks such as Digital Product Passports (DPP) are improving traceability and recyclability. Additionally, R&D into PVC-free tapes for hydrogen infrastructure is expanding applications, reinforcing Germany’s leadership in clean chemistry and advanced materials.

India Fire-Resistant Tapes Market: Infrastructure Expansion and Localization Driving Rapid Growth

India is experiencing rapid growth in fire-resistant tapes, driven by infrastructure expansion and localization policies. Under the Gati Shakti master plan, fire-rated tapes are being widely adopted in railways, airports, and metro systems, particularly for cable insulation and safety.

Policy support is a key driver. The PLI scheme (2026 expansion) now includes high-temperature Nomex and PPS tapes, promoting domestic manufacturing and reducing import dependence. Urban metro projects are increasing demand for fire-resistant cable bundling tapes to ensure 120-minute safety windows, while desalination and water infrastructure are using nanocomposite fire tapes for corrosion-prone environments. Additionally, innovations such as antimicrobial fire tapes for healthcare HVAC systems and new synthetic mica clusters in Jharkhand are strengthening India’s supply chain.

United Kingdom Fire-Resistant Tapes Market: Regulatory Stringency and Building Safety Driving Demand

The UK is a global benchmark for fire safety regulation, particularly following reforms under the Building Safety Act. The removal of legacy BS 476 standards (2026) has mandated adoption of more stringent EN fire testing standards, significantly raising performance requirements.

Regulatory enforcement is driving demand. Policies such as Awaab’s Law Phase II require rapid remediation of fire hazards, boosting demand for intumescent tapes and fire-rated seals. Additionally, architects now require CCPI-certified products with verified performance data. Growth in mass timber construction is also increasing use of high-elongation fire tapes, while expanding data center infrastructure is driving demand for fireproof cable coatings and tapes to prevent cascading failures. Strict enforcement by regulators has led to a ~40% increase in certified audits, reinforcing compliance across the supply chain.

Japan Fire-Resistant Tapes Market: Precision Engineering and Seismic Resilience Driving Innovation

Japan leads in high-precision and seismic-resistant fire tapes, combining advanced materials with structural durability. The development of high-elongation tapes (>800%) ensures fireproof sealing even during structural movement caused by earthquakes.

Innovation is also focused on electronics and miniaturization. Japanese firms are advancing sub-micron coating techniques for polyimide-based fire tapes, supporting high-density electronic components. Additionally, transparent fire-retardant tapes are enabling visual inspection of wiring without removing protection, while demand in elderly care facilities is driving adoption of warm-touch fire-safe materials. Strategic expansion into Southeast Asia is also strengthening supply chains for specialty high-performance tapes.

Fire Resistant Tapes Market Report Scope

Fire Resistant Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$971.6 Million

|

|

Market Size (2032)

|

$1519.8 Million

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Backing Material (Fiberglass, Nomex, Acetate Cloth, Aluminum Foil, Polyphenylene Sulfide, Polyimide, Polyvinyl Chloride, Others), By Adhesive (Silicone-based Adhesives, Acrylic-based Adhesives, Rubber-based Adhesives, Specialty Flame-Retardant Resins), By Coating Type (Single-Coated Tapes, Double-Coated Tapes, Transfer Tapes), By Technology (Pressure-Sensitive Tapes, Heat-Activated Tapes, Water-Activated Tapes), By End-Use Industry (Electrical and Electronics, Automotive and Transportation, Building and Construction, Aerospace and Defense, Industrial and Marine)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Compagnie de Saint-Gobain S.A., Nitto Denko Corporation, tesa SE, Avery Dennison Corporation, Scapa Group Ltd., Berry Global Inc., DuPont de Nemours, Inc., Shurtape Technologies, LLC, Rogers Corporation, H.B. Fuller Company, Intertape Polymer Group Inc., Boyd Corporation, Lohmann GmbH & Co. KG, ORAFOL Europe GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fire Resistant Tapes Market Segmentation

By Backing Material

- Fiberglass

- Nomex

- Acetate Cloth

- Aluminum Foil

- Polyphenylene Sulfide

- Polyimide

- Polyvinyl Chloride

- Others

By Adhesive

- Silicone-based Adhesives

- Acrylic-based Adhesives

- Rubber-based Adhesives

- Specialty Flame-Retardant Resins

By Coating Type

- Single-Coated Tapes

- Double-Coated Tapes

- Transfer Tapes

By Technology

- Pressure-Sensitive Tapes

- Heat-Activated Tapes

- Water-Activated Tapes

By End-Use Industry

- Electrical and Electronics

- Automotive and Transportation

- Building and Construction

- Aerospace and Defense

- Industrial and Marine

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Fire Resistant Tapes Market

- 3M Company

- Compagnie de Saint-Gobain S.A.

- Nitto Denko Corporation

- tesa SE

- Avery Dennison Corporation

- Scapa Group Ltd.

- Berry Global Inc.

- DuPont de Nemours, Inc.

- Shurtape Technologies, LLC

- Rogers Corporation

- H.B. Fuller Company

- Intertape Polymer Group Inc.

- Boyd Corporation

- Lohmann GmbH & Co. KG

- ORAFOL Europe GmbH

*- List not Exhaustive