Fireproof Ceramics Market Expansion Driven by High-Temperature Industrial Demand, Advanced Materials Innovation, and Semiconductor Integration

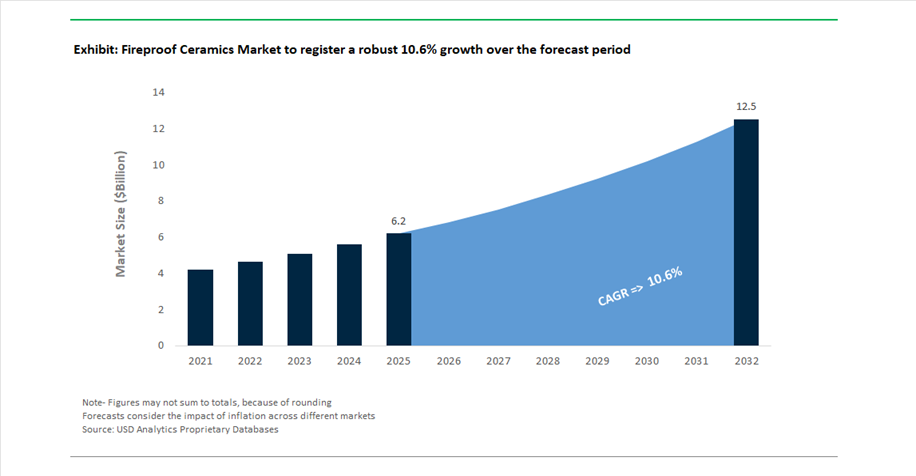

The global Fireproof Ceramics Market was valued at USD 6.2 billion in 2025 and is projected to grow at a CAGR of 10.6% between 2025 and 2032, reaching USD 12.6 billion by 2032. This strong growth reflects the increasing demand for high-temperature resistant materials across steel production, energy, aerospace, and advanced electronics industries.

Fireproof ceramics, including refractory materials, ceramic fibers, and advanced composites, are essential for applications requiring thermal stability, non-flammability, and chemical resistance. A major growth driver is the expansion of industrial high-temperature processes, particularly in steel, cement, and glass manufacturing. Additionally, the rise of clean energy technologies, such as fuel cells and hydrogen systems, is creating new demand for ceramics that can withstand extreme operating conditions.

The market is also benefiting from increasing adoption in high-tech sectors, including semiconductor packaging and aerospace, where ceramics provide thermal management and fire resistance for sensitive components. Sustainability trends are further influencing the market, with manufacturers focusing on energy-efficient materials, reduced emissions during production, and improved installation safety.

Aerogel Breakthroughs, Advanced Ceramic Fibers, and Strategic Industry Consolidation Reshape Market Dynamics

The fireproof ceramics market is experiencing rapid transformation driven by material innovation, strategic acquisitions, and industrial modernization initiatives. In September 2025, Alkegen launched AlkeGel™, a next-generation aerogel insulation with 80% reduced dust levels, significantly improving installation safety and enabling faster deployment in industrial fire protection applications.

Advanced fiber technology is also enhancing performance. In December 2024, RATH Group began production of ALTRA FLEX oxide ceramic fibers, offering 20–40% energy savings compared to traditional refractory materials. These fibers are critical for ceramic matrix composites (CMCs) used in aerospace and high-temperature industrial applications.

Strategic consolidation is strengthening market positioning. In February 2025, Vesuvius PLC acquired PiroMET, integrating refractory technology with robotic application systems to improve installation efficiency in steel and foundry industries. Similarly, in March 2025, H.C. Starck completed the acquisition of CeramTec, creating a major global player in advanced ceramic components across medical, automotive, and electronics sectors.

Large-scale investment strategies are accelerating capacity expansion. In October 2025, Saint-Gobain announced a $14 billion investment plan, focusing on fire-resistant materials for infrastructure and data centers. Additionally, in May 2025, SCHOTT AG secured approval for a €300 million advanced ceramics plant in Poland, targeting aerospace and defense applications.

Emerging applications in electronics are also reshaping demand. In November 2024, Corning partnered with Samsung Electronics to develop ceramic substrates for semiconductor packaging, leveraging the fireproof and thermal stability properties of ceramics to protect high-density chips.

Operational restructuring is improving efficiency across the industry. In January 2025, Morgan Advanced Materials consolidated its operations into three global segments, prioritizing investment in thermal products and technical ceramics, while RHI Magnesita optimized its production network to focus on high-margin fireproof ceramic products used in cement and steel industries.

Transition to Recrystallized Silicon Carbide (RSiC) in Lithium-Ion Battery Kiln Furniture

The fireproof ceramics industry is undergoing a major material shift as lithium-ion battery manufacturers replace conventional cordierite and alumina-based kiln furniture with recrystallized silicon carbide to support next-generation cathode production. This transition is primarily driven by the need for higher thermal efficiency, improved throughput, and contamination-free processing of high-nickel cathode materials such as NCM811 and LFP. RSiC ceramics offer a significant thermal conductivity advantage, delivering values approximately 10 to 15 times higher than traditional cordierite-mullite materials. This enables more uniform heat distribution during calcination, reducing localized hot spots and ensuring consistent particle morphology. Additionally, the superior thermal shock resistance of RSiC allows for rapid heating and cooling cycles, enabling battery manufacturers to increase kiln throughput by up to 20%, a critical factor in scaling gigafactory production. Durability improvements are equally significant, with RSiC kiln components engineered to last between 500 and 1,000 cycles compared to the 50 to 100 cycle lifespan of traditional saggers, substantially reducing operational downtime and cost per unit output. Furthermore, binder-free RSiC formulations minimize trace contamination from elements such as iron and sulfur, which can negatively impact battery performance and safety. These advantages are positioning RSiC as a cornerstone material in high-performance ceramic solutions for battery manufacturing infrastructure.

Adoption of Silicon Carbide-Coated Cathodes in Aluminum Smelting for Energy Efficiency and Longevity

The aluminum smelting industry is increasingly adopting silicon carbide-coated cathode technologies to enhance operational efficiency and extend potline service life under high-amperage conditions. Traditional carbon cathode blocks are prone to chemical degradation and typically require replacement every four to six years, resulting in significant maintenance costs and production downtime. The integration of silicon carbide coatings provides a protective barrier that significantly improves resistance to molten cryolite penetration and chemical attack, reducing structural degradation. This innovation is enabling smelters to extend cathode lifespan by approximately 30% to 50%, delivering substantial capital expenditure savings over time. Additionally, advanced TiB2-silicon carbide composite coatings enhance wettability between molten aluminum and the cathode surface, allowing for a reduction in the anode-cathode distance within the Hall-Héroult process. This optimization directly translates into energy savings of 10% to 15%, a critical advantage in an energy-intensive industry. Improved thermal management is another key benefit, with silicon carbide refractory linings contributing to a 20% reduction in thermal hotspots across potlines, ensuring more stable current distribution and consistent production output. These performance enhancements are driving the adoption of advanced ceramic coatings as a strategic solution for improving efficiency and sustainability in aluminum production.

US DOE Industrial Decarbonization Programs Driving Demand for High-Temperature Ceramic Membrane Reactors

The United States Department of Energy’s industrial decarbonization initiatives are creating a significant growth opportunity for advanced fireproof ceramics, particularly in the development of high-temperature ceramic membrane reactors for hydrogen production. Under funding frameworks associated with the PIPES Act of 2025, substantial investment is being directed toward the development of leak-proof ceramic membranes capable of operating under extreme pressure and temperature conditions. These ceramic systems are designed to enable hydrogen production with purity levels exceeding 90% in a single-stage process, offering a more energy-efficient alternative to conventional multi-step steam methane reforming. Advanced ceramic membranes are also being integrated into carbon capture technologies, with proton-conducting materials capable of operating between 600°C and 900°C to facilitate the direct separation of carbon dioxide from industrial emissions during hydrogen synthesis. These innovations are aligned with the DOE’s Hydrogen Shot initiative, which targets reducing hydrogen production costs to 2 dollars per kilogram, a goal heavily dependent on the scalability and durability of ceramic electrolyzer and membrane components. The convergence of hydrogen production, carbon capture, and high-temperature materials science is positioning fireproof ceramics as a critical enabler of industrial decarbonization strategies in the United States.

India’s National Green Hydrogen Mission Driving Domestic Demand for Ceramic Electrolyzer Components

India’s National Green Hydrogen Mission is accelerating the development of a domestic supply chain for high-performance ceramic materials used in solid oxide electrolyzer cells, creating a substantial opportunity for the fireproof ceramics industry. The mission has allocated incentives to establish approximately 15,000 megawatts of electrolyzer manufacturing capacity by 2026, with a strong emphasis on localizing critical ceramic components such as yttria-stabilized zirconia electrolytes. Government funding of approximately 4,440 crore rupees is being directed toward the development of manufacturing capabilities that support high-temperature electrolysis technologies, which offer higher efficiency compared to conventional proton exchange membrane systems. Solid oxide electrolyzer cells operate at elevated temperatures and require advanced ceramic materials capable of maintaining structural and electrochemical stability under extreme conditions. As India targets the production of 5 million metric tonnes of green hydrogen by 2030, demand for durable, high-performance ceramic components is expected to rise significantly. Additionally, the localization mandate is positioning India as a competitive exporter of ceramic-based electrolyzer systems and green hydrogen derivatives, particularly for markets in Europe and Japan seeking zero-tariff imports.

Fireproof Ceramics Market Share 2025: Fiber Blankets and Thermal Stability Lead Industrial Demand

Product Insights: Ceramic Fiber Blankets Dominate High-Temperature Insulation Applications

The ceramic fiber blanket segment leads the fireproof ceramics market with a 35% market share in 2025, driven by its superior performance in high-temperature insulation environments. These blankets are widely used in petrochemical reformers, industrial kilns, and heat-treating furnaces, where low thermal conductivity and lightweight structure are critical for energy efficiency and operational safety. Their flexibility and adaptability make them highly suitable for complex industrial geometries, ensuring effective heat containment. A key advantage is their ease of installation and replacement, as needled ceramic fiber blankets can be cut, folded, and layered without specialized tools, significantly reducing maintenance downtime in industries such as steel production and glass manufacturing. This combination of thermal efficiency, cost savings, and operational convenience positions ceramic fiber blankets as the preferred solution in demanding thermal insulation applications, reinforcing their leading share in the global fireproof ceramics market.

Functional Property Insights: High Thermal Stability Drives Performance in Extreme Environments

The high thermal stability segment accounts for the largest 34% share in the fireproof ceramics market in 2025, reflecting strong demand for materials capable of withstanding extreme temperatures. Industries such as aerospace, cement, metallurgy, and power generation require ceramics that can operate continuously at temperatures exceeding 1200°C without sintering, cracking, or embrittlement. This makes high thermal stability a critical property for applications like aerospace heat shields, industrial chimneys, and incinerators. Additionally, increasing regulatory pressure for energy efficiency and carbon emission reduction is driving adoption, as thermally stable ceramics help minimize heat loss and optimize fuel consumption in high-temperature processes. By improving insulation performance and reducing energy waste, these materials support sustainability goals while lowering operational costs. As industries continue to prioritize durability and efficiency under extreme conditions, high thermal stability will remain a key driver in the fireproof ceramics market.

Fireproof Ceramics Market Competitive Landscape Driven by High-Temperature Insulation, Energy Transition, and Sustainable Refractories

The fireproof ceramics market is highly competitive, driven by demand for high-temperature insulation, passive fire protection (PFP), and low-carbon industrial processes. Key players focus on advanced ceramic fibers, refractory materials, and integrated solutions supporting LNG, hydrogen, steel, and semiconductor manufacturing applications.

Morgan Advanced Materials leads fireproof ceramics market with FireMaster® PFP solutions and low bio-persistent fibers

Morgan Advanced Materials holds a strong position in the fireproof ceramics market through its FireMaster® portfolio, widely adopted across petrochemical and shipbuilding sectors for passive fire protection applications. Its 2026 product range includes ceramic fiber blankets, rigid boards, and cable wraps designed for mission-critical fire safety compliance. The company is optimizing its supply chain to manage regional volatility while targeting growth in LNG and hydrogen infrastructure. A major innovation is the scaling of Superwool® low bio-persistent fibers, offering safer alternatives to traditional refractory ceramic fibers without compromising performance above 1200°C. This enhances occupational safety while maintaining thermal efficiency. Morgan’s focus on advanced insulation solutions strengthens its leadership in high-temperature fireproof ceramics.

Saint-Gobain expands fireproof ceramics portfolio with integrated facade systems and multi-local strategy

Saint-Gobain is reinforcing its position in the fireproof ceramics market through its "Lead & Grow" strategy, targeting infrastructure and non-residential construction, which now contribute nearly 33% of total sales. The company reported strong financial performance in 2025 with balanced global growth across key regions. Its EnveoVent system integrates fire resistance, thermal insulation, and acoustic performance into a single facade solution, reducing carbon emissions in building construction. Saint-Gobain’s multi-local approach enables customized solutions for regional market needs. Its leadership in construction chemicals supports the development of lightweight, energy-efficient ceramic systems. These capabilities position the company as a key innovator in integrated fireproof ceramic applications.

Vesuvius strengthens refractory ceramics capabilities through acquisitions and APAC expansion

Vesuvius plc is advancing its position in the fireproof ceramics market through strategic acquisitions and operational efficiency improvements. The integration of PiroMET and Molten Metal Systems added £22.5 million in revenue, enhancing capabilities in non-ferrous metal processing. Despite challenges in EMEA markets, the company maintained strong financial performance with revenues of £1,809.5 million in 2025. Its cost optimization initiatives delivered £17.8 million in savings, exceeding targets. Vesuvius has completed capacity expansion programs to capture significant growth in the Asia-Pacific refractory market, projected to rise sharply through 2030. Its focus on steel and foundry applications strengthens its industrial ceramics portfolio. These strategies position Vesuvius as a key supplier of high-performance refractory materials.

RHI Magnesita drives sustainable fireproof ceramics growth with green steel partnerships and recycling leadership

RHI Magnesita is a global leader in fireproof ceramics, reporting €3.4 billion in revenue and focusing on deleveraging and operational efficiency in 2026. The company is advancing its 4PRO business model, integrating circular economy principles and process optimization. It achieved a record recycling rate of 15.9%, reinforcing its position as a sustainability leader in refractory materials. RHI Magnesita has secured new contracts for green steel production, supplying ceramic linings for electric arc furnaces used in low-carbon steelmaking. Its integration of Resco synergies further enhances its product portfolio. These initiatives align with the growing demand for sustainable industrial ceramics. The company remains a critical player in decarbonizing heavy industries.

Imerys enhances fireproof ceramics portfolio with mineral-based solutions and sustainability-driven transformation

Imerys is strengthening its position in the fireproof ceramics market through its mineral-based solutions, including kaolin, ball clay, and feldspar for technical ceramics applications. The company is implementing Project Horizon to achieve €50–€60 million in cost savings, with significant benefits expected in 2026. Despite challenges in Europe, Imerys maintained strong EBITDA performance of €546 million in 2025. Its materials provide high electrical insulation and mechanical strength, supporting applications in 5G infrastructure and EV components. The company is transitioning toward a low-carbon portfolio, with 75% of its ceramics and building products evaluated against lifecycle sustainability criteria. This focus on performance and sustainability strengthens its competitive positioning in advanced ceramic materials.

Zircar Ceramics leads niche high-temperature applications with alumina-based innovations and precision engineering

Zircar Ceramics is a specialist leader in high-purity fireproof ceramics, focusing on alumina and zirconia fiber products for extreme temperature environments. Its high-alumina rigid boards maintain stability up to 1800°C, making them ideal for semiconductor manufacturing processes such as silicon carbide crystal growth. The company offers custom-machined ceramic components using AI-driven CNC technology, catering to aerospace and defense applications where precision and thermal performance are critical. Zircar’s low-mass insulation solutions enable faster heating cycles, reducing energy consumption in industrial kilns by up to 20%. Its niche expertise in high-temperature ceramics positions it as a key supplier in advanced industrial and semiconductor applications.

China Fireproof Ceramics Market: Semiconductor Scaling and Ultra-High Temperature Innovation Driving Global Leadership

China dominates the fireproof ceramics market, accounting for over 48% of Asia-Pacific demand, with a strategic shift toward high-purity and advanced applications. The surge in semiconductor manufacturing is a major catalyst, highlighted by a $1.8 billion investment in silicon carbide (SiC) ceramic consumables for wafer processing.

Policy and innovation are tightly linked. Under the 15th Five-Year Plan (2026), industries must improve furnace thermal efficiency by ~20%, accelerating adoption of bio-soluble ceramic fibers. Advanced aerospace programs are deploying ultra-high temperature ceramics (UHTCs) capable of operating above 2000°C, while EV battery facilities are integrating ceramic fiber fire barriers to prevent thermal runaway. Additionally, nuclear energy expansion is driving demand for radiation-resistant ceramics, reinforcing China’s leadership across high-tech and industrial applications.

United States Fireproof Ceramics Market: Aerospace Expansion and Infrastructure Resilience Driving High-Value Growth

The U.S. market is focused on high-performance ceramic systems for aerospace, infrastructure, and energy applications. A major development is the $450 million expansion of ceramic matrix composite (CMC) production, enabling next-generation jet engines to operate without active cooling.

Regulatory and technological trends are shaping demand. Updated EPA “Safer Choice” guidelines (2026) are phasing out traditional refractory ceramic fibers (RCFs), increasing adoption of alkaline earth silicate (AES) wool. The EV sector is driving demand for ceramic fire barriers in battery packs, while hydrogen infrastructure is advancing ceramic membranes for purification systems. Additionally, wildfire-prone regions are promoting ceramic-clad fireproof panels for residential construction, and data center growth is increasing demand for low-outgassing ceramic firewalls.

India Fireproof Ceramics Market: Infrastructure Boom and Industrial Modernization Driving Rapid Growth

India is one of the fastest-growing markets for fireproof ceramics, driven by infrastructure expansion and industrial policy support. Under the Gati Shakti master plan, fireproof ceramic linings are mandated for railway tunnels and large infrastructure projects, ensuring enhanced safety.

Industrial demand is also rising. The steel sector is commissioning 12 new blast furnaces (2025–2026), driving demand for high-alumina refractory bricks, while semiconductor investments (e.g., Dholera fab) are creating demand for high-purity ceramic components. Urban metro expansion is boosting use of ceramic fire-barrier blankets for tunnels, and the cement industry is adopting low-thermal-mass linings to improve energy efficiency. Additionally, innovations such as antimicrobial ceramic coatings for hospitals are expanding application scope.

Germany Fireproof Ceramics Market: Circular Economy and Hydrogen Infrastructure Driving Sustainability Leadership

Germany leads in sustainable fireproof ceramics, with a focus on circular materials and regulatory compliance. The commercialization of bio-attributed ceramic binders has reduced carbon footprints by ~15%, aligning with EU sustainability goals.

Hydrogen infrastructure is a major growth driver. Projects under the European Hydrogen Backbone are specifying ceramic-based hybrid coatings for valves and pipelines to resist high-temperature embrittlement. Regulatory frameworks such as REACH (2026 updates) are driving development of biocide-free ceramic slurries, while Digital Product Passports (DPP) ensure traceability and recyclability. Additionally, innovation in ceramic-aerogel composites is improving insulation performance for industrial applications, reinforcing Germany’s leadership in eco-friendly materials.

Japan Fireproof Ceramics Market: Ultra-Precision Materials and Seismic Resilience Driving Innovation

Japan is a global leader in high-purity and precision fireproof ceramics, particularly for electronics and advanced manufacturing. Breakthroughs include sub-micron coating precision for ceramic layers used in MLCC components, supporting high-density electronics.

Seismic resilience is a defining feature. The development of high-elongation ceramic fiber blankets (>800%) ensures fire integrity during structural movement in earthquake-prone regions. Additionally, innovations in high-refractive-index (HRI) ceramic coatings are enabling advanced AR/VR applications, while zirconia feedstock dominance (~70% global share) strengthens Japan’s position in thermal barrier coatings. Expanding use in elderly care infrastructure—such as warm-touch fireproof tiles—also reflects demographic-driven demand.

Saudi Arabia Fireproof Ceramics Market: Vision 2030 Megaprojects and Extreme Climate Engineering Driving Demand

Saudi Arabia is a major growth market for fireproof ceramics, driven by Vision 2030 megaprojects and energy infrastructure expansion. Projects like NEOM and the Red Sea developments account for ~25% of regional demand, focusing on desert-resistant, solar-reflective ceramic insulation.

Energy and industrial sectors are key drivers. Aramco’s Master Gas System Phase 3 is specifying ceramic linings for hydrogen pipelines, while SABER regulations are enforcing use of certified fireproof materials (UL 1709). Localization efforts—such as new ceramic fiber plants in Dammam—are strengthening supply chains. Additionally, demand for aesthetic fireproof ceramics in commercial construction and intumescent-ready ceramic primers for steel structures is expanding applications, positioning Saudi Arabia as a high-value market.

Fireproof Ceramics Market Report Scope

Fireproof Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.2 Billion

|

|

Market Size (2032)

|

$12.6 Billion

|

|

Market Growth Rate

|

10.6%

|

|

Segments

|

By Product (Ceramic Fiber Blanket, Bulk and Feedstock, Ceramic Boards and Sheets, Ceramic Paper, Ceramic Modules and Blocks, Specialty Shapes and Engineered Components, Textiles), By Raw Material (Alumina-Silica, Polycrystalline Wool, Low Bio-Persistent Wool, Zirconia-based Ceramics, Silicon Carbide, Magnesia and Fireclay), By Temperature Grade (Low Temperature, Medium Temperature, High Temperature, Ultra-High Temperature), By End-Use Industry (Iron and Steel, Petrochemicals and Refineries, Power Generation, Ceramics and Glass Manufacturing, Aluminum and Non-Ferrous Metals, Aerospace and Defense, Automotive, Building and Construction), By Functional Property (High Thermal Stability, Low Thermal Conductivity, Thermal Shock Resistance, Chemical and Corrosion Resistance, Abrasive and Mechanical Wear Resistance)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain S.A., Morgan Advanced Materials plc, Alkegen, RHI Magnesita N.V., Vesuvius plc, Imerys S.A., Kyocera Corporation, Ibiden Co., Ltd., Shinagawa Refractories Co., Ltd., Luyang Energy-Saving Materials Co., Ltd., Isolite Insulating Products Co., Ltd., HarbisonWalker International, 3M Company, Rath Group, Zircar Ceramics, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fireproof Ceramics Market Segmentation

By Product

- Ceramic Fiber Blanket

- Bulk and Feedstock

- Ceramic Boards and Sheets

- Ceramic Paper

- Ceramic Modules and Blocks

- Specialty Shapes and Engineered Components

- Textiles

By Raw Material

- Alumina-Silica

- Polycrystalline Wool

- Low Bio-Persistent Wool

- Zirconia-based Ceramics

- Silicon Carbide

- Magnesia and Fireclay

By Temperature Grade

- Low Temperature

- Medium Temperature

- High Temperature

- Ultra-High Temperature

By End-Use Industry

- Iron and Steel

- Petrochemicals and Refineries

- Power Generation

- Ceramics and Glass Manufacturing

- Aluminum and Non-Ferrous Metals

- Aerospace and Defense

- Automotive

- Building and Construction

By Functional Property

- High Thermal Stability

- Low Thermal Conductivity

- Thermal Shock Resistance

- Chemical and Corrosion Resistance

- Abrasive and Mechanical Wear Resistance

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Fireproof Ceramics Market

- Saint-Gobain S.A.

- Morgan Advanced Materials plc

- Alkegen

- RHI Magnesita N.V.

- Vesuvius plc

- Imerys S.A.

- Kyocera Corporation

- Ibiden Co., Ltd.

- Shinagawa Refractories Co., Ltd.

- Luyang Energy-Saving Materials Co., Ltd.

- Isolite Insulating Products Co., Ltd.

- HarbisonWalker International

- 3M Company

- Rath Group

- Zircar Ceramics, Inc.

*- List not Exhaustive