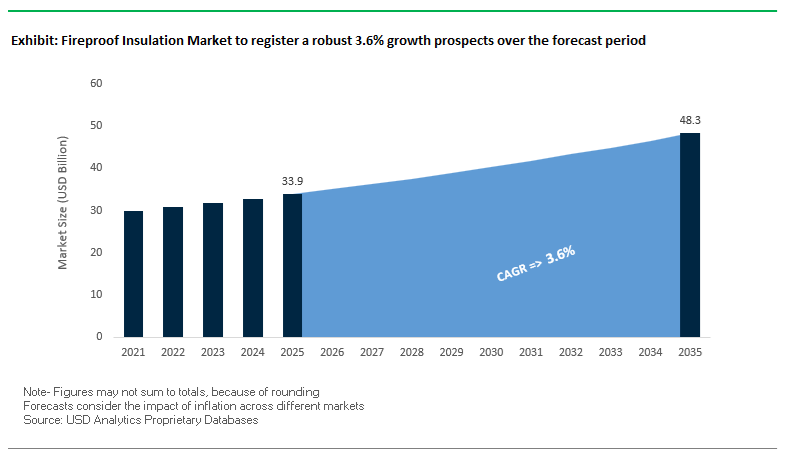

The Fireproof Insulation Market, valued at USD 33.9 billion in 2025, is projected to grow steadily to USD 48.3 billion by 2035, supported by a moderate but resilient CAGR of 3.6%. Industry stakeholders—including architects, façade engineers, MEP contractors, and building safety regulators—are increasingly prioritizing non-combustible insulation materials that meet Euroclass A1 criteria, provide exceptional thermal stability, and comply with stringent passive fire protection (PFP) codes. Demand is advancing in high-rise construction, technical insulation for HVAC systems, industrial environments, and energy-efficient building envelopes where fire performance, durability, sustainability, and regulatory certification are all mandatory purchasing criteria.

The Fireproof Insulation Market continues to experience structural transformation, driven by investments in capacity expansions, low-carbon mineral wool production, and heightened global regulatory emphasis on non-combustible insulation. In November 2025, Rockwool announced that its cumulative investments for the first nine months of 2025 reached 307 million EUR, reflecting aggressive expansion into North America, India, and Romania. The surge in capital deployment highlights soaring global demand for non-combustible stone wool insulation as governments and urban planners prioritize fire resilience in high-density cities. Complementing the, the industry’s sustainability shift accelerated in October 2025, when Saint-Gobain ISOVER introduced new Environmental Product Declarations (EPDs) documenting significant CO₂ reductions achieved through renewable energy usage and increased recycled content—an essential development as building material emissions become a major ESG metric.

The momentum toward green manufacturing intensified further in June 2025, when Saint-Gobain inaugurated the world's lowest-carbon glass wool insulation plant in Finland, achieving 80% lower CO₂ emissions than the industry average thanks to electrification and renewable energy inputs. Earlier, in January 2025, the company commissioned the first hybrid glass furnace in the Netherlands capable of operating on green electricity and biogas—demonstrating the pathway toward fossil-free mineral wool production. In Europe, regulatory pressure is rising: the European Commission announced in November 2024 its intent to propose new rules prioritizing non-flammable insulation following major fire events, reinforcing long-term demand for Euroclass A1/A2-rated mineral wool solutions.

Product innovation remains strong. In March 2025, Rockwool launched Fire Barrier EN, a stone wool system engineered to meet BS EN 1364-1:2015 standards for compartmentation—meeting growing market needs for certified fire partitions in complex building envelopes. Meanwhile, the integration of fireproof insulation with complementary life-safety systems is advancing, demonstrated by Specified Technologies Inc. (STI) introducing an upgraded SpecSeal Cast-In Firestop Device in March 2024, featuring adjustable height settings (8"–36") and W-rated water protection for through-floor penetrations.

Buyers evaluating fireproof insulation systems assess the ability of mineral wool and glass wool products to retain structural and thermal integrity under extreme temperatures, maintain long-term performance exceeding 65 years, and support perimeter fire containment (PFC) requirements imposed on modern curtain wall and façade assemblies. With global attention intensifying on building safety—especially after major global fire incidents—regulators in Europe and APAC are increasingly reinforcing mandates for A1/A2-rated façade insulation. Further, manufacturers are expanding capacity, transitioning to low-carbon production technologies, and integrating renewable energy sources into mineral wool furnaces to meet sustainability goals without compromising fire safety performance.

- Mineral wool insulation withstands temperatures above 1,000°C, maintaining fiber structure and preventing flame spread—critical for PFP performance.

- Perimeter fire containment (PFC) systems must match the fire-resistance rating of the floor assembly, typically 2–3 hours, per IBC and ASTM E2307.

- Euroclass A1-rated insulation ensures zero contribution to fire, making it mandatory for high-rise façades and high-risk building envelopes.

- Fireproof insulation offers proven service life of 65+ years, maintaining thermal, acoustic, and fire resilience across the entire building lifespan.

- Leading manufacturers are targeting 15% embodied CO₂ reduction by 2025, aligning with sustainable construction and low-carbon building requirements.

Regulatory-Driven Material Transitions and High-Tech Innovation Shaping the Fireproof Insulation Market

Trend 1 - Global Mandate for A-Class Non-Combustible Insulation in High-Rise and Public Infrastructure

The regulatory landscape for façade and envelope insulation has fundamentally changed following high-profile building fires, particularly across the UK and Europe. The Euroclass fire classification (EN 13501-1) is now the defining benchmark for material approval in high-risk structures, compelling a widespread transition to A1 and A2-s1, d0 rated fireproof insulation.

Since December 2018, the UK has legally mandated that all “relevant buildings” over 18 meters-including residential, institutional, and healthcare facilities-use only materials rated A2-s1, d0 or A1 in external walls. This eliminates combustible insulation from high-rise applications and positions mineral wool and cellular glass as the industry’s default solutions. Mineral wool products, such as stone wool, achieve the highest Euroclass A1 rating and withstand temperatures approaching 1000°C, as verified in their Declarations of Performance (DoP). Their non-combustibility is non-negotiable for façade fire protection.

Regulations tightened further in December 2022, lowering the height threshold to 11 meters for many residential buildings. This expansion significantly widens the addressable market for fireproof insulation, driving rapid adoption in mid-rise buildings previously exempt from strict façade rules.

Smoke and toxicity performance-signified by the s1 (minimal smoke) and d0 (no flaming droplets) classifications-has become equally critical. As evacuation survivability is heavily influenced by smoke behavior, manufacturers must now optimize insulation chemistry to minimize toxic by-products during fire exposure. These combined requirements represent one of the most powerful regulatory drivers in the fireproof insulation market’s history.

Trend 2 - Ultra-High-Temperature Ceramic Insulation and Encapsulation Surge in BESS and EV Infrastructure

The rapid expansion of Battery Energy Storage Systems (BESS) and EV charging infrastructure has created an urgent demand for insulation materials that can withstand extreme thermal events-especially thermal runaway, where cell temperatures can exceed 1000°C. Regulatory frameworks now explicitly require fireproof insulation systems engineered to contain such events.

NFPA 855, the foundational standard for stationary ESS installations, requires system-level fire protection validated through UL 9540A large-scale thermal runaway testing. UL 9540A evaluates whether the failure of a single module induces propagation to adjacent modules. As a result, fireproof insulation materials-particularly ceramic fiber blankets and silica-based thermal barriers-must demonstrate the ability to contain heat long enough for suppression systems to activate.

Ceramic fiber blankets are gaining dominance due to their ultra-high-temperature resistance, low thermal conductivity, and structural stability under intense thermal stress. These materials protect enclosure walls, inter-module gaps, and cable routing channels, enabling installation layouts with reduced unit spacing while maintaining compliance through the Hazard Mitigation Analysis (HMA) required by NFPA 855.

With utility-scale BESS projects increasing in both capacity and density, and EV charging hubs expanding globally, demand for specialized fireproof encapsulation solutions is scaling rapidly. This trend positions ceramic thermal insulation as one of the fastest-growing segments in modern fire protection.

Opportunity 1 - Bio-Based, A-Class-Capable Fire-Resistant Insulation for Net-Zero Construction

Decarbonization targets across global construction markets are opening a high-growth innovation pathway for bio-based fireproof insulation that can meet the stringent combustibility limits of A2-s1, d0 classifications. This intersection of low embodied carbon and fire compliance represents one of the most commercially promising future segments.

The EU’s Circular Economy Action Plan and national-level net-zero mandates encourage the adoption of renewable construction materials-provided they meet strict fire safety rules. Recent breakthroughs, such as Oak Ridge National Laboratory’s bio-based, halogen-free flame retardant, demonstrate the feasibility of next-generation insulation systems using renewable feedstocks while still meeting advanced fire standards.

Research published in 2023 provides a landmark proof point: a straw and waste-glass composite insulation board, treated with a modified binder, met the EN ISO 1182 combustion criteria, achieving an A2 classification. This marks a significant step in positioning bio-insulation as a viable alternative for high-rise applications long dominated by mineral wool.

Thermal performance is competitive. The straw-silicate insulation board achieved a thermal conductivity below 0.039 W/(m·K), comparable to conventional insulation. This demonstrates that sustainability goals and performance requirements can converge-a critical success factor for the future of fireproof insulation in green building projects.

Opportunity 2 - Smart Fireproof Insulation with Embedded Sensors for Predictive Safety and Asset Protection

A breakthrough opportunity lies in the emergence of smart fireproof insulation, where embedded sensors transform passive insulation layers into active safety systems capable of real-time monitoring and early-warning fire detection.

Moisture is one of the most common causes of insulation degradation and reduced fire resistance. Research into smart building materials demonstrates the value of integrating Temperature/Humidity (T/H) sensors with RF wireless communication chips directly into insulation layers. These sensors can detect moisture ingress well before it leads to mold, corrosion, or thermal performance reduction-enabling predictive maintenance instead of periodic manual inspection.

The integration of heat-sensing elements, including fiber-optic cables and thermistors, enhances fire detection capability. Because electrical faults and localized overheating frequently originate within wall cavities, smart insulation provides highly localized thermal monitoring that can alert facility managers to hazardous conditions before smoke detectors activate.

High-risk facilities-such as data centers, petrochemical infrastructure, archival storage, and high-value industrial plants-have the most to gain. By leveraging embedded sensor networks, operators can continuously monitor insulation integrity, eliminate blind spots in fire safety systems, and extend the service life of passive fire protection assets.

Smart insulation represents a next-generation evolution in fireproof materials, merging building intelligence, occupant safety, and asset protection into a unified high-value technology platform.

Fireproof Insulation Market Share Analysis

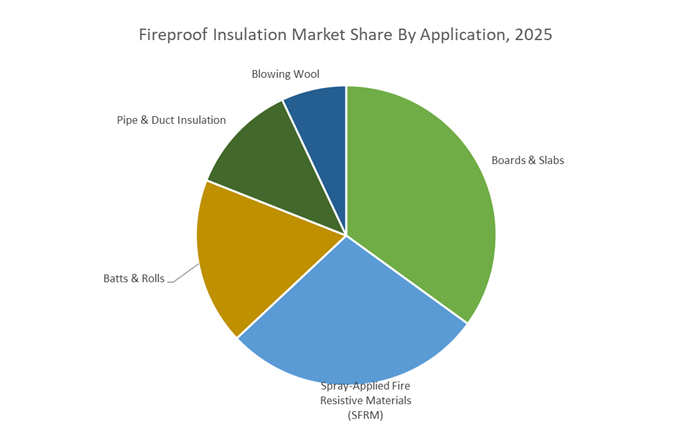

Market Share by Application Form: Boards & Slabs Lead Through Superior Fire Classification and Structural-Grade Durability

Boards & Slabs, commanding a 35% share, dominate the Fireproof Insulation Market because they deliver the highest levels of fire resistance, structural stability, and multi-functional performance required in critical building assemblies. High-density mineral wool, calcium silicate, and perlite-based boards consistently achieve Euroclass A1 non-combustibility, meaning they do not ignite, drip, or produce hazardous smoke—qualifications that make them indispensable in regulated fire-rated systems. Their ability to endure temperatures above 1,000°C without melting or structural failure enables them to protect steel beams, fire-rated walls, and other load-bearing components during fully developed fires. This performance profile aligns directly with stringent building codes that mandate long-duration structural fire protection, particularly in high-rise and institutional projects. Additionally, boards and slabs provide a robust thermal insulation advantage through low thermal conductivity values (λ), and their dense, fibrous architecture delivers effective acoustic dampening, supporting modern standards for occupant comfort in multi-unit residential and commercial spaces. Their rigidity, ease of installation, and compatibility with multi-layer fire-rated assemblies further strengthen their position as the most widely adopted fireproof insulation format across the construction sector. These combined benefits—fire resistance, thermal performance, acoustic control, and compliance assurance—explain their leading market share and their irreplaceable role in fire-safe building design.

Market Share by End-Use Industry: Residential & Commercial Construction Dominates Through Code-Driven Demand and Dual Performance Requirements

Residential & Commercial Construction holds the largest 48% market share, driven by stringent global building codes that make fireproof insulation a mandatory component in nearly all new construction and major retrofits. Regulatory frameworks such as the International Building Code (IBC) and NFPA standards require assemblies—walls, floors, roofs, and structural elements—to achieve 1-hour to 2-hour fire ratings, elevating the demand for non-combustible, certified insulation materials like mineral wool. The sector’s dominance is reinforced by its focus on life-safety performance, as fireproof insulation is essential for protecting means of egress—corridors, stairwells, and exit enclosures—by maintaining low temperatures on the non-fire side to ensure safe evacuation and delay structural failure. The massive volume of construction activity in residential towers, commercial complexes, schools, hospitals, and mixed-use developments further multiplies the use of fireproof insulation across linear meters of walls, floors, ceilings, and mechanical penetrations. Importantly, fireproof insulation materials also deliver strong energy-efficiency benefits through high R-values, helping builders meet increasingly strict energy codes while simultaneously satisfying fire protection requirements. This dual compliance—energy and fire safety—makes mineral wool and other fireproof insulation materials the default choice for developers, architects, and builders worldwide, supporting the segment’s substantial share and reinforcing its long-term growth trajectory.

Country Analysis: Global Fireproof Insulation Development Hubs

United Kingdom: Post-Grenfell Regulatory Tightening Accelerates Demand for Non-Combustible Mineral Wool Facade Insulation

The United Kingdom remains one of the most tightly regulated fireproof insulation markets globally following the sweeping reforms enacted in the aftermath of the Grenfell Tower tragedy. The country’s strengthened fire safety framework has decisively shifted demand toward non-combustible fireproof insulation materials, particularly Euroclass A1 and A2-s1,d0-rated mineral wool and rock wool systems, which are now mandatory for use in external wall constructions on residential buildings over 18 meters. Updates to Approved Document B alongside broader enforcement under national Building Regulations have effectively removed combustible insulation materials—especially foam insulations—from high-rise building applications. This regulatory shift is having an immediate and profound impact on insulation material selection across remediation, renewal, and new-build projects.

The country is also experiencing a surge in domestic capacity investment to support this transition. Knauf Insulation’s €200 million mineral wool production facility, announced in late 2025, represents one of the largest U.K. insulation manufacturing investments in recent years and is directly aligned with rising demand for sustainable, non-combustible fireproof insulation. The plant will operate using low-carbon electric melting technology, demonstrating the U.K.’s dual push for fire safety and decarbonization. Additionally, nationwide remediation programs requiring the replacement of flammable External Wall Insulation (EWI) in thousands of high-rise residential properties guarantee multi-year demand for rock mineral wool systems. Compliance in the U.K. also involves rigorous assessment of both the insulation’s reaction-to-fire classification and the performance of the full cladding system under BS/EN fire testing, ensuring holistic fire performance in complex façade assemblies.

European Union / Germany: Euroclass A1 Standards and Decarbonization Strategies Shape Mineral Wool Innovation

The European Union—supported by strong leadership from Germany—remains at the forefront of fireproof insulation innovation due to its stringent Euroclass testing system, ambitious decarbonization goals, and harmonized construction safety regulations. Euroclass A1, the highest fire safety classification, sets the benchmark across EU member states for specifying rock wool, glass mineral wool, and other fully non-combustible insulation products, ensuring zero contribution to fire even under fully developed burning conditions. This standard is deeply embedded in the region’s construction codes, especially for high-rise and public-use buildings, and is a critical driver of consistent, high-volume demand for mineral wool solutions across Europe.

Sustainability and circularity further define the EU’s fireproof insulation market. Industry leaders such as Saint-Gobain emphasize “light and sustainable construction” in their long-term strategies, dedicating investment to lower-carbon manufacturing processes, enhanced recyclability, and reduced embodied carbon in mineral wool products. The region is also scaling production capacity to meet growing renovation and energy efficiency mandates. For example, the Knauf Group’s €135 million expansion in Târnăveni, Romania, completed in 2024, significantly increased the availability of mineral wool to support both fire safety upgrades and energy performance improvements across Central and Eastern Europe. EU-wide circular economy policies are also pushing manufacturers to incorporate higher recycled content and adopt advanced resource-efficiency practices, reinforcing Europe’s position as a global leader in sustainable, non-combustible fireproof insulation materials.

China: Nationwide High-Rise Inspection Campaign Driving Reform of External Wall Insulation (EWI)

China’s fireproof insulation market is experiencing unprecedented transformation as government authorities intensify nationwide enforcement of fire safety regulations across the country’s enormous inventory of high-rise buildings. In late 2025, the Ministry of Emergency Management and the State Council Work Safety Committee launched a sweeping inspection and rectification campaign focused on high-rise fire hazards, marking one of the most aggressive national interventions in building fire safety to date. A major focus of this campaign is the identification and removal of flammable external wall insulation (EWI), including numerous foam-based systems that fail to meet newly tightened fire safety thresholds. This enforcement surge is accelerating adoption of non-combustible mineral wool insulation for both façade refurbishment and new high-rise construction.

Beyond regulatory enforcement, China’s fireproof insulation demand is also shaped by evolving building energy codes. The General Code for Building Energy Efficiency and Renewable Energy Utilization (GB 55015-2021) mandates improved thermal performance for building envelopes while simultaneously requiring insulation materials to meet strict non-combustibility standards, fundamentally aligning energy efficiency with fire protection. A rapidly expanding category driving additional demand is data center construction, newly classified as a key energy-consuming product under China’s 2024 energy efficiency requirements. These facilities require high-performance, non-combustible insulation for fire compartmentation, environmental control, and thermal stabilization in large-scale server environments. As urban densification continues, China remains one of the world’s largest and fastest-growing markets for fireproof insulation.

United States: Integration of Mineral Wool with Mass Timber and WUI Fire Regulations Expands Fireproof Insulation Demand

In the United States, fireproof insulation demand is strongly driven by the increasing adoption of mass timber construction, continuous modernization of model codes, and intensifying fire safety requirements in Wildland-Urban Interface (WUI) zones. The 2024 Fire Design Specification for Wood Construction published by the American Wood Council (AWC) details how mineral wool insulation enhances the fire resistance of mass timber assemblies—providing essential protection for achieving 1-hour and 2-hour fire ratings in structural systems. This linkage between fireproof insulation and mass timber specification is introducing new structural applications for mineral wool as a fire-resisting thermal barrier, especially in mid-rise and tall timber buildings.

Enhanced code adoption also fuels market growth. The widespread enforcement of the International Building Code (IBC) and NFPA 101 requires tested and listed fire-rated insulation assemblies for structural components, floor-ceiling systems, and rated walls—sustaining high, steady demand for non-combustible mineral wool solutions. Meanwhile, the escalating risks associated with WUI fires—particularly in states like California, Oregon, and Colorado—are driving broader use of non-combustible exterior wall insulation in both residential and commercial construction. Compliance with ASTM E108 Class A/B/C roof covering requirements and enhanced exterior wall fire resistance is shifting builders away from foam insulations toward mineral wool systems capable of withstanding external flame exposure and ember attack. As climate-driven wildfire risks intensify, the U.S. is becoming a global leader in performance-based, code-integrated fireproof insulation adoption across new and existing buildings.

Competitive Landscape: Global Leaders Drive Decarbonized Mineral Wool, High-Temperature Performance, and System-Level Fire Protection

The competitive environment of the Fireproof Insulation Market is shaped by major manufacturers specializing in mineral wool, glass wool, PIR/phenolic boards, and integrated fire barrier systems. Leading companies are investing in decarbonized production, expanding their global footprint, and integrating advanced fireproofing solutions into broader building envelope technologies. Their strategies are grounded in enhancing fire resilience, meeting evolving code compliance, and supplying long-life insulation materials suitable for high-rise, industrial, and HVAC applications.

Rockwool remains the global benchmark for non-combustible stone wool insulation, providing solutions for buildings, industrial systems, and technical applications. Stone wool’s proven performance above 1,000°C positions Rockwool as a leading supplier for high-risk applications requiring EI-rated protection. In November 2025, the company reported 307 million EUR in investments across the first nine months of 2025, supporting new manufacturing facilities in North America and India, along with expanded capacity in Romania. Rockwool’s strategic emphasis on fire resilience, energy efficiency, and circularity continues to drive its leadership position in the global PFP market.

Saint-Gobain ISOVER is a major player in both glass wool and stone wool insulation, serving building, HVAC, and industrial markets with its ISOVER® and ULTIMATE™ product lines. The company is a global leader in decarbonized insulation manufacturing, having inaugurated the first hybrid glass furnace in the Netherlands in January 2025, followed by commissioning the world's lowest-carbon glass wool plant in Finland in June 2025. ISOVER’s U PROTECT® systems provide fire resistance up to EI 120 for HVAC ducts, supporting safe, compliant technical insulation across complex building infrastructure.

Knauf Insulation produces both glass mineral wool and rock mineral wool, emphasizing sustainability and circularity. Through its “For A Better World” strategy, the company aims to reduce product embodied CO₂ by 15% by 2025, supported by increased use of recycled content and energy-efficient manufacturing. A key differentiator is Knauf’s ECOSE® Technology, a bio-based binder free from formaldehyde and phenols, delivering enhanced indoor air quality while maintaining Euroclass A1/A2 fire performance. Knauf continues to expand its global foothold as demand increases for sustainable, non-combustible insulation solutions.

Owens Corning is recognized globally for fiberglass and mineral wool insulation, including its FOAMGLAS® cellular glass products that are inherently non-combustible, moisture-resistant, and suitable for industrial tanks, piping, and high-risk environments. The company prioritizes sustainable insulation solutions, offering glass wool products with 65%+ recycled content and focusing on healthy building compliance metrics. Its diverse portfolio enables Owens Corning to serve both residential building envelope markets and heavy industrial fireproofing needs.

Kingspan is a global leader in PIR and phenolic insulation boards, increasingly integrating fire-resistant core technologies including QuadCore® to meet stringent façade safety regulations. The company has invested significantly in large-scale fire testing facilities, ensuring that its composite panels meet system-level fire performance requirements. Kingspan continues to expand its building envelope portfolio through strategic acquisitions, emphasizing the integration of passive fire protection into high-performance insulated panels for commercial and industrial buildings.

Fireproof Insulation Market Report Scope

Fireproof Insulation Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$33.9 Billion

|

|

Market Size (2035)

|

$48.3 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material Type (Mineral Wool, Ceramic Fiber, Calcium Silicate, Aerogels, Foam Glass, Perlite), By Application Form (Boards & Slabs, Batts & Rolls, Loose Fill, Spray-Applied Fire Resistive Materials, Pipe & Duct Insulation), By End-Use Industry (Residential & Commercial Construction, Industrial & Infrastructure, Marine & Offshore, Transportation, HVAC Systems), By Fire Performance (Non-Combustible, Limited Combustibility, Firestop/Fire Block, High-Temperature Insulation, Fire-Resistance Rated Assemblies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain S.A., Knauf Group, Kingspan Group Plc, Owens Corning, Rockwool International A/S, Unifrax (Alkegen), Trelleborg AB, Aspen Aerogels Inc., Morgan Advanced Materials, 3M Company, Armacell International S.A., Luyang Energy-Saving Materials Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fireproof Insulation Market Segmentation

By Material Type

- Mineral Wool (Rock Wool, Slag Wool, Glass Wool/Fiberglass)

- Ceramic Fiber

- Calcium Silicate

- Aerogels (Silica Aerogel)

- Foam Glass

- Perlite

By Application Form

- Boards & Slabs

- Batts & Rolls

- Loose Fill / Blowing Wool

- Spray-Applied Fire Resistive Materials (SFRM)

- Pipe & Duct Insulation

By End-Use Industry

- Residential & Commercial Construction

- Industrial & Infrastructure

- Marine & Offshore

- Transportation

- HVAC Systems

By Fire Performance

- Non-Combustible (Euroclass A1)

- Limited Combustibility (Euroclass A2)

- Firestop / Fire Block

- High-Temperature Insulation (>1000°C)

- Fire-Resistance Rated Assemblies

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Fireproof Insulation Market

- Saint-Gobain S.A.

- Knauf Group (Knauf Insulation)

- Kingspan Group Plc

- Owens Corning

- Rockwool International A/S

- Unifrax (Alkegen)

- Trelleborg AB

- Aspen Aerogels, Inc.

- Morgan Advanced Materials

- 3M Company

- Armacell International S.A.

- Luyang Energy-Saving Materials Co., Ltd.

*- List not Exhaustive