Flame Retardant Thermoplastic Market Growth Driven by EV Safety, Halogen-Free Innovation, and Regulatory Compliance

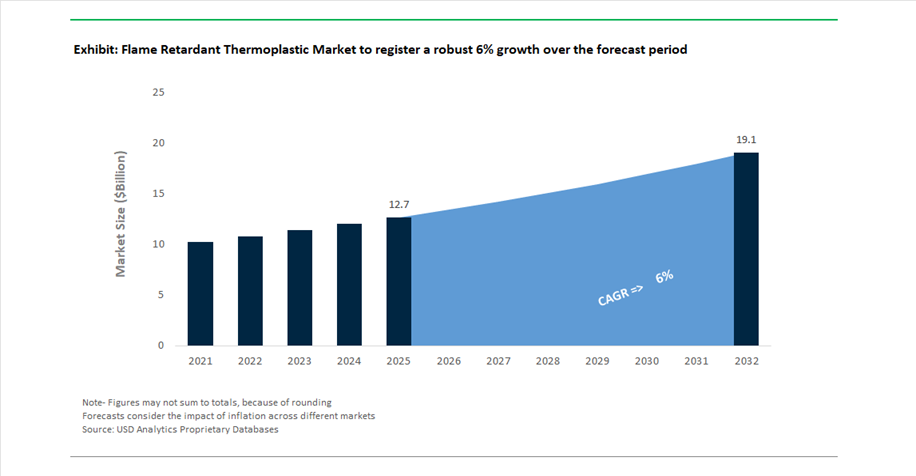

The global Flame Retardant Thermoplastic Market was valued at USD 12.7 billion in 2025 and is projected to grow at a CAGR of 6% between 2025 and 2032, reaching USD 19.1 billion by 2032. This growth is primarily driven by increasing demand for fire-safe, lightweight, and high-performance polymer materials across electric vehicles (EVs), electronics, construction, and industrial applications.

Flame retardant thermoplastics are essential in applications where thermal stability, electrical insulation, and fire resistance are critical. A major growth driver is the rapid expansion of the electric mobility ecosystem, where these materials are used in battery housings, connectors, charging infrastructure, and wire insulation. As EV architectures shift toward higher voltage systems (800V+), the need for materials capable of withstanding extreme thermal events while preventing fire propagation is intensifying.

Another key trend shaping the market is the transition toward halogen-free flame retardant (HFFR) materials, driven by tightening environmental and safety regulations. Traditional brominated flame retardants are increasingly being replaced with phosphorus-based, mineral-based, and bio-circular alternatives, which reduce toxic emissions during combustion. Additionally, stringent regulations such as EU restrictions on bisphenol compounds are pushing manufacturers to develop next-generation, compliant thermoplastics for sensitive applications like food-contact and consumer appliances.

Halogen-Free Material Expansion, EV Battery Safety Innovation, and Supply Chain Volatility Reshape Market Dynamics

The flame retardant thermoplastic market is undergoing rapid transformation driven by regulatory shifts, EV-driven material innovation, and upstream cost pressures. In March 2026, BASF expanded its Ultrason® P portfolio, introducing high-heat thermoplastics that are free from BPA and BPS, in response to evolving EU regulations. These materials enable manufacturers to comply with food-contact safety standards while maintaining flame retardant performance.

Localization and capacity expansion are also key strategic priorities. In March 2026, BASF began commercial production of Elastollan® flame-retardant TPU in Shanghai, strengthening supply for Asia-Pacific markets, particularly in industrial automation, robotics, and EV charging cables. This move reflects the broader industry trend toward regionalized supply chains to support high-growth sectors.

Electric vehicle safety is emerging as a critical innovation frontier. In May 2024, SABIC showcased phase-change thermoplastic barrier technology, capable of absorbing heat during thermal events and preventing fire propagation in battery modules. Additionally, SABIC’s BLUEHERO™ initiative successfully deployed non-halogenated flame-retardant polypropylene in EV battery enclosures, capable of withstanding temperatures up to 1,000°C for five minutes, significantly enhancing passenger safety.

Material innovation is also expanding into advanced applications. In October 2025, Covestro introduced thermally conductive, flame-retardant polycarbonates designed for replaceable battery systems, improving both performance and safety in portable power and mobility applications. Similarly, Arkema advanced its bio-circular thermoplastic portfolio, promoting sustainable alternatives for electronics and automotive sectors.

Supply chain volatility is influencing pricing and market dynamics. In March 2026, Lanxess implemented price increases of up to 35% for flame retardants, reflecting rising raw material and energy costs. This highlights the ongoing pressure on manufacturers to balance cost efficiency with supply reliability and sustainability goals.

Advanced manufacturing technologies are also reshaping production models. Following the integration of Covestro’s additive materials business, Stratasys expanded its portfolio of flame-retardant thermoplastic filaments, enabling on-demand manufacturing of aerospace interiors and EV components through additive manufacturing.

Regional expansion continues to support demand growth. In December 2024, Asahi Kasei expanded its resin compounding capacity in China, targeting high-performance, halogen-free thermoplastics for electronics and automotive markets.

Organophosphorus-Based Flame Retardant Polyamides Gaining Traction in EV High-Voltage Applications

The flame retardant thermoplastics market is undergoing a structural shift as electric vehicle electrification accelerates demand for high-performance, halogen-free materials capable of meeting stringent electrical and thermal requirements. Organophosphorus-based flame retardant polyamides are increasingly replacing legacy halogenated systems due to their superior electrical insulation performance and mechanical stability in thin-wall geometries. As of 2025, phosphorus-based flame retardants account for approximately 42% of the non-halogenated additive segment, driven by their ability to achieve UL 94 V-0 flammability ratings at relatively low loadings of 10% to 18% in glass-fiber-reinforced polyamide systems. These materials are engineered to meet the highest Comparative Tracking Index classification of 600 volts, ensuring resistance to electrical tracking in compact, high-voltage EV connectors. Advanced formulations also deliver dielectric strengths exceeding 30 kV/mm at operating temperatures up to 140°C, supporting applications in EV charging infrastructure and high-density electronic systems. The integration of phosphorus-nitrogen synergistic systems has further enhanced material efficiency by reducing additive loading requirements by approximately 15% while maintaining impact strength and mechanical integrity. These innovations are positioning organophosphorus-modified thermoplastics as a critical enabler of safe, lightweight, and miniaturized electrical components in next-generation mobility platforms.

Bio-Based Flame Retardant Thermoplastics Emerging Under EU Circularity and Toxicity Regulations

European regulatory frameworks, including the Single-Use Plastics Directive and the Packaging and Packaging Waste Regulation, are accelerating the transition toward bio-based flame retardant thermoplastics in electronics, industrial, and packaging applications. These policies are driving a shift away from fossil-derived polymers toward renewable alternatives such as bio-based polyamides, including PA56 and PA610, which offer comparable performance with reduced environmental impact. The EU Bioeconomy Strategy is further reinforcing this transition by promoting non-toxic-by-design additives, encouraging the development of flame retardant systems derived from lignin, starch, and other bio-based carbon sources. These materials are achieving UL 94 V-0 performance while reducing the carbon footprint of structural thermoplastics by up to 35%. Technological advancements are also enabling bio-based flame retardant compounds to meet the stringent requirements of modern electronics, including maintaining V-0 ratings at wall thicknesses as low as 0.4 millimeters, supporting ongoing device miniaturization trends. The electronics and electrical sector now accounts for over 38% of halogen-free thermoplastic applications, reflecting strong alignment between regulatory compliance requirements such as REACH and RoHS and the adoption of sustainable material solutions. This convergence of environmental regulation and material innovation is positioning bio-based flame retardant thermoplastics as a key growth segment in the global market.

US PHMSA Regulations Driving Adoption of Fire-Resistant Thermoplastic Liners in Rail Tank Cars

The United States Department of Transportation’s Pipeline and Hazardous Materials Safety Administration is creating a significant opportunity for flame retardant thermoplastics through updated regulations targeting the safe transportation of hazardous liquids. Regulatory updates introduced in 2025 and effective January 2026 incorporate expanded industry standards that emphasize enhanced thermal protection and structural integrity for rail tank cars carrying flammable substances. These requirements are driving the adoption of advanced thermoplastic liner systems with integrated flame retardant properties capable of preventing catastrophic failure during fire incidents. Increased regulatory scrutiny on legacy liner materials is opening a substantial retrofit market, particularly for operators seeking compliance with updated safety standards under federal transport regulations. Additionally, research funding initiatives are supporting the development of next-generation composite thermoplastic liners that combine chemical resistance with high-performance fire retardancy. These innovations are aimed at improving crashworthiness and fire resistance in derailment scenarios, where thermal exposure can compromise structural integrity. The convergence of regulatory enforcement and technological advancement is positioning flame retardant thermoplastics as a critical component in modern hazardous material transport systems.

India’s Metro and Railway Fire Safety Regulations Driving Demand for LSZH Thermoplastics

India’s rapidly expanding urban transit infrastructure is creating a strong growth opportunity for flame retardant thermoplastics, particularly low smoke zero halogen materials used in electrical and interior applications. Updated regulations issued by the Central Electricity Authority and the Ministry of Railways in 2026 mandate the use of LSZH thermoplastics for electrical conduit systems, smart meters, and interface components in metro and high-speed rail networks. These materials are essential for minimizing smoke toxicity and corrosive gas emissions during fire events, ensuring passenger safety in confined transit environments. The requirement for compliance with European EN 45545-2 HL3 fire safety standards is further elevating performance expectations, driving demand for high-quality flame retardant compounds. With more than 20 metro projects currently under development, the scale of infrastructure expansion is creating a substantial market for specialized thermoplastic materials. Additionally, new guidelines require thermoplastic enclosures to maintain V-0 flammability ratings under voltage levels up to 650 volts, reinforcing the need for advanced material formulations with high dielectric strength and thermal stability. Government initiatives such as the Production Linked Incentive scheme are also supporting domestic manufacturing of flame retardant thermoplastics, reducing import dependence and strengthening local supply chains. These combined regulatory and industrial factors are positioning India as a high-growth market for advanced fire-safe thermoplastic materials.

Flame Retardant Thermoplastic Market Share 2025: Pellet Form and Direct Sales Channels Drive Growth

Form Insights: Pellet Segment Leads with Processing Efficiency and High-Volume Manufacturing Demand

The pellets segment dominates the flame retardant thermoplastic market with a 52% market share in 2025, driven by its ready-to-process convenience and superior consistency in manufacturing operations. Flame retardant (FR) thermoplastic pellets are widely used as direct drop-in materials for injection molding and extrusion, eliminating the need for additional compounding or mixing steps. This ensures uniform dispersion of flame retardant additives, which is critical for achieving consistent fire safety performance in automotive components, electrical & electronics (E&E) parts, and industrial applications. The segment’s leadership is further reinforced by its extensive use in high-volume applications such as wire and cable jacketing, appliance housings, and EV battery connectors, where compliance with UL 94 V-0 fire safety standards is mandatory. As demand for lightweight, fire-safe polymer solutions increases across industries, pellet-based thermoplastics will continue to be the preferred format for scalable and efficient production.

Distribution Channel Insights: Direct Sales Dominate with OEM-Centric Supply Models

The direct sales channel accounts for the largest 55% share in the flame retardant thermoplastic market in 2025, reflecting the importance of customization, technical support, and long-term supply reliability. Large OEMs in industries such as automotive, electronics, and electrical manufacturing prefer direct procurement from material producers to access tailored formulations, including halogen-free, brominated, and specialty flame retardant compounds with specific melt flow indices. Direct engagement also ensures compliance with stringent global regulations and provides access to detailed technical documentation and performance certifications. Additionally, long-term supply agreements enable OEMs to secure stable pricing and priority allocation, particularly during raw material shortages involving key inputs like phosphorus-based additives and magnesium hydroxide. As supply chain resilience and product customization become increasingly critical, direct sales channels will remain a dominant force in the flame retardant thermoplastic market.

Flame Retardant Thermoplastics Market Competitive Landscape Driven by Halogen-Free Innovation, EV Applications, and High-Performance Polymers

The flame retardant thermoplastics market is highly competitive, driven by halogen-free formulations, EV electrification, and stringent fire safety regulations. Key players are focusing on advanced polymers, PFAS-free chemistries, and integrated supply chains to address demand across electronics, automotive, robotics, and infrastructure applications.

BASF strengthens flame retardant thermoplastics portfolio with TPU innovation and China-based integration

BASF SE is advancing its position in the flame retardant thermoplastics market through localized production and high-performance TPU innovation. The company began commercial production of Elastollan® FR TPU at its Shanghai facility, targeting industrial automation and robotics applications in Asia-Pacific. Its Performance Materials division reported €6.8 billion in sales, with a strategic focus on EV charging cables and advanced polymer systems. BASF is scaling halogen-free flame-retardant TPU grades that meet stringent safety and durability requirements. Integration of the Zhanjiang Verbund site ensures cost efficiency and supply chain resilience for polyolefin and polyurethane compounds. This positions BASF as a leader in next-generation flame retardant thermoplastic materials.

SABIC drives PFAS-free thermoplastics innovation with SILTEM™ and ULTEM™ high-performance resins

SABIC is strengthening its leadership in the flame retardant thermoplastics market through PFAS-free material innovation and high-performance polymer solutions. The company introduced SILTEM™ HU resins, designed as non-fluorinated alternatives for medical devices and tubing applications. Its LNP™ ELCRES™ copolymers meet UL746G standards while addressing clean chemistry regulations in electronics manufacturing. SABIC’s ULTEM™ HU resins remain the benchmark for surgical robotics, offering high strength and sterilization compatibility. The launch of LNP™ LUBRILOY™ compounds eliminates PTFE while improving wear resistance in electronic components. These innovations reinforce SABIC’s position in sustainable and high-performance thermoplastic solutions.

Clariant accelerates halogen-free flame retardants with phosphorus-based additives and renewable materials

Clariant is expanding its presence in the flame retardant thermoplastics market through advanced additive technologies and regional manufacturing expansion. The company showcased Exolit™ OP 1266, a halogen-free flame retardant designed for 800V+ electric mobility systems requiring high CTI performance. Its Daya Bay facility and joint venture with Fuhua enhance supply chain efficiency in Asia. Clariant introduced Licocare™ RBW Vita, a renewable additive derived from rice bran wax that reduces carbon footprint while meeting food contact standards. Its AddWorks® PPA solutions provide PFAS-free processing aids, eliminating extrusion defects in flame-retardant films. These developments position Clariant as a leader in sustainable flame retardant additives.

Lanxess focuses on high-margin flame retardant thermoplastics with brominated and phosphorus-based solutions

Lanxess AG is reinforcing its competitive position in the flame retardant thermoplastics market through its FORWARD! strategy, targeting €150 million in annual savings while focusing on high-margin specialty additives. The company remains a leader in brominated flame retardants, including Emerald Innovation™ products, while expanding its Levagard® phosphorus-based portfolio. It is prioritizing R&D in low-smoke, halogen-free compounds to meet growing infrastructure demand in Europe. Lanxess benefits from strong vertical integration in bromine and phosphorus supply, mitigating raw material volatility. Operational restructuring initiatives are enhancing efficiency and profitability. These capabilities strengthen its position in engineering thermoplastics and industrial fire safety solutions.

DuPont integrates flame retardant thermoplastics into advanced materials for aerospace and energy applications

DuPont is leveraging its materials science expertise to integrate flame retardant properties into high-performance polymers used in aerospace, electronics, and energy systems. The company received Edison Awards recognition for its Tychem® 6000 SFR, highlighting innovation in multi-hazard protective materials. DuPont is advancing flame-retardant polyimides and aramids for high-density data centers and aerospace applications. Its FilmTec™ technologies support sustainable lithium-ion battery production by enabling water reuse in separator manufacturing. The company is also aligning with net-zero construction trends through fire-resistant building materials. These initiatives position DuPont as a key innovator in advanced thermoplastic and composite systems.

Albemarle strengthens flame retardant thermoplastics leadership with brominated solutions and mineral-based growth

Albemarle Corporation is reinforcing its role in the flame retardant thermoplastics market through its Saytex® brominated flame retardants, which account for 15% of global demand in engineering plastics and automotive applications. Following its acquisition by BlackRock, the company is focusing on energy transition markets with high-purity fire safety materials. Albemarle is investing in polymeric brominated solutions that minimize leaching and comply with REACH and RoHS standards. Its mineral flame retardant segment, including aluminum trihydroxide and magnesium hydroxide, driven by demand for low-toxicity cable materials. These strategies strengthen its position in both traditional and sustainable flame retardant solutions.

Germany Flame Retardant Thermoplastics Market: Non-Halogenated Innovation and Circular Economy Leadership

Germany is the global benchmark for eco-friendly flame retardant (FR) thermoplastics, driven by stringent EU sustainability mandates. The market is rapidly transitioning toward non-halogenated systems, with innovations like melamine-free ammonium polyphosphate (APP) and phosphorus-based compounds achieving UL 94 V-0 ratings at ultra-thin wall thicknesses (≈0.75 mm).

Regulation is a major catalyst. The revised Construction Products Regulation (2025) mandates Digital Product Passports (DPP) and sets EN 13501-1 Class B-s1, d0 as the baseline for insulation materials. Additionally, Extended Producer Responsibility (EPR) laws are discouraging additives that hinder recycling, pushing adoption of mineral-based flame retardants (e.g., magnesium hydroxide). Demand is also rising in appliances and smart-home devices, with FR-ABS usage increasing ~24% YoY, reinforcing Germany’s leadership in sustainable, high-performance plastics.

United States Flame Retardant Thermoplastics Market: Automotive Standards and Aerospace Innovation Driving Growth

The U.S. market is defined by strict fire safety standards and EV supply chain localization. Regulations such as FMVSS 302 have led to ~38% of vehicle interiors using FR plastics, particularly ABS and PC/ABS blends.

Technological innovation is focused on performance and lightweighting. Manufacturers are adopting nitrogen-based synergistic flame retardants to reduce heavy mineral loading while maintaining mechanical strength—critical for aerospace components. Federal investments in data centers and EV infrastructure are driving demand for FR-PBT and polyamide (PA66) in connectors and switchgear. Additionally, regulatory pressure on brominated flame retardants is accelerating the shift toward phosphorus-based systems, while new high-flow FR grades are enabling advanced manufacturing such as 3D printing.

China Flame Retardant Thermoplastics Market: EV Expansion and Non-Halogenated Transition Driving Scale

China dominates the global supply of flame retardant thermoplastics, leveraging its manufacturing scale and raw material control. Government policies are accelerating a shift toward non-halogenated flame retardants (NHFRs), with demand increasing by ~27% in government-funded infrastructure projects.

The EV sector is a key growth driver. Expansion of FR-PC/ABS production lines is supporting battery enclosures and electronic components, while stricter regulations on brominated FRs have reduced domestic halogenated output by ~15%. China is also a major supplier of antimony trioxide, though export restrictions have driven global price volatility. Additionally, applications in 5G infrastructure and electronics are increasing demand for phosphorus-based FR materials, reinforcing China’s leadership in both scale and advanced applications.

India Flame Retardant Thermoplastics Market: EV Safety Regulations and Infrastructure Growth Driving Rapid Expansion

India is emerging as a high-growth market for FR thermoplastics, driven by urbanization, EV adoption, and regulatory enforcement. The implementation of AIS 156 (Amendment 3) has significantly increased demand for FR-polyamide (PA6) and PBT in EV battery systems.

Construction and infrastructure are also key drivers. Demand for FR-PVC and FR-polyolefins in wire and cable applications has risen by ~12%, following stricter fire safety codes for high-rise buildings. Policy initiatives such as Quality Control Orders (QCO) are standardizing fire-resistant materials across public infrastructure. Additionally, global players are expanding local capabilities—e.g., BASF’s Ultramid® Advanced PPA launch (2025)—while increasing alignment with ISO 3795 standards is phasing out untreated plastics in automotive interiors.

South Korea Flame Retardant Thermoplastics Market: EV Batteries and Semiconductor Leadership Driving Innovation

South Korea is a global leader in high-performance FR thermoplastics, particularly for EV batteries and semiconductors. Capacity expansions—such as LG Chem’s +35 kiloton FR-ABS facility (2024)—are supporting growing global demand.

Innovation is focused on next-generation materials. Development of low-smoke FR-ABS now accounts for ~45% of the office automation market, while nanotechnology-enhanced FR-PC (carbon nanotubes) improves both thermal conductivity and flame resistance. Regulatory shifts—such as the phase-out of PFAS-based additives—are pushing adoption of silicone-based flame retardants. Additionally, new safety standards for Energy Storage Systems (ESS) require UL 94 5VA-rated thermoplastics, reinforcing South Korea’s leadership in high-tech applications.

Japan Flame Retardant Thermoplastics Market: Precision Engineering and Bio-Based Innovation Driving Advanced Applications

Japan is at the forefront of high-precision and sustainable FR thermoplastics, particularly in electronics and advanced materials. Over 52% of new office automation devices now incorporate non-halogenated flame retardant components, reflecting strong regulatory and technological alignment.

Innovation is centered on bio-based and high-performance materials. Japanese researchers have developed lignin-derived flame retardants for transparent polycarbonate, achieving high fire resistance without compromising clarity. Additionally, advancements in FR-PPS compounds allow operation at temperatures exceeding 200°C, supporting next-generation power semiconductors. Updated regulations under the Fire Service Act (2025) are also enforcing stricter smoke density limits, while companies like Toray are expanding production of FR-PBT for EV charging systems. These factors position Japan as a leader in precision and sustainable flame-retardant technologies.

Flame Retardant Thermoplastic Market Report Scope

Flame Retardant Thermoplastic Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.7 Billion

|

|

Market Size (2032)

|

$19.1 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Resin (Polyolefins, Engineering Thermoplastics, Styrenics, Polyvinyl Chloride, High-Performance Thermoplastics), By Flame Retardant Chemistry (Non-Halogenated, Halogenated), By End-Use Industry (Electrical and Electronics, Automotive and Transportation, Building and Construction, Aerospace and Defense, Industrial Manufacturing), By Performance Grade (Standard Grade, High-Performance Grade, Low Smoke Zero Halogen, High-Heat Resistance Grade), By Form (Pellets, Masterbatches, Resins), By Distribution Channel (Direct Sales, Distributors and Compounders, Online)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, SABIC, DuPont de Nemours, Inc., Covestro AG, LG Chem, Ltd., LANXESS AG, Syensqo, Arkema S.A., Celanese Corporation, Asahi Kasei Corporation, Teijin Limited, Mitsubishi Engineering-Plastics Corporation, Avient Corporation, Trinseo S.A., RTP Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flame Retardant Thermoplastic Market Segmentation

By Resin

- Polyolefins

- Polypropylene

- Polyethylene

- Engineering Thermoplastics

- Polyamide

- Polycarbonate

- Polybutylene Terephthalate

- Polyethylene Terephthalate

- Styrenics

- Acrylonitrile Butadiene Styrene

- Polystyrene

- ABS Blends

- Polyvinyl Chloride

- High-Performance Thermoplastics

- Polyether Ether Ketone

- Polyphenylene Sulfide

- Polyethersulfone

By Flame Retardant Chemistry

- Non-Halogenated

- Aluminum Trihydroxide

- Magnesium Hydroxide

- Phosphorus-based

- Nitrogen-based

- Zinc

- Halogenated

- Brominated Flame Retardants

- Chlorinated Flame Retardants

By End-Use Industry

- Electrical and Electronics

- Automotive and Transportation

- Building and Construction

- Aerospace and Defense

- Industrial Manufacturing

By Performance Grade

- Standard Grade

- High-Performance Grade

- Low Smoke Zero Halogen

- High-Heat Resistance Grade

By Form

- Pellets

- Masterbatches

- Resins

By Distribution Channel

- Direct Sales

- Distributors and Compounders

- Online

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Flame Retardant Thermoplastic Market

- BASF SE

- SABIC

- DuPont de Nemours, Inc.

- Covestro AG

- LG Chem, Ltd.

- LANXESS AG

- Syensqo

- Arkema S.A.

- Celanese Corporation

- Asahi Kasei Corporation

- Teijin Limited

- Mitsubishi Engineering-Plastics Corporation

- Avient Corporation

- Trinseo S.A.

- RTP Company

*- List not Exhaustive