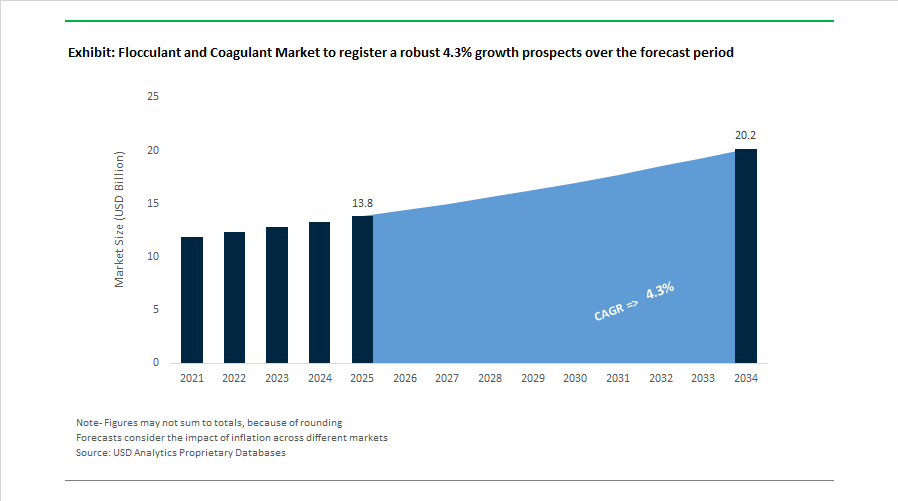

The Flocculant and Coagulant Market is projected to grow from $13.8 billion in 2025 to $20.2 billion by 2034, registering a CAGR of 4.3%. Market expansion is anchored in rising municipal wastewater treatment investments, tightening industrial discharge regulations, mining throughput growth, and sustained demand for enhanced oil recovery chemicals. Polyacrylamide-based flocculants, organic and inorganic coagulants, biomass-balanced polymers, and specialty monomers such as N-vinylformamide are central to solid-liquid separation, sludge dewatering, produced-water treatment, and ultrapure water systems. Supply chain resilience, sustainability credentials, and digital dosing integration have emerged as decisive procurement criteria across utilities and industrial clients.

In December 2025, Ecolab, through its Nalco Water division, completed the acquisition of Ovivo’s electronics ultrapure water business, integrating specialized flocculation technologies tailored for semiconductor fabrication facilities where ultra-low particulate and ionic contamination thresholds are mandatory. In October 2025, SNF Group finalized its €135 million acquisition of Syensqo’s Oil & Gas division, expanding its friction reducer and high-molecular-weight polyacrylamide production footprint for hydraulic fracturing and enhanced oil recovery operations. In June 2025, Solenis and NCH Corporation entered into a definitive merger agreement, combining Solenis’s global coagulant and polymer portfolio with NCH’s strong middle-market water treatment presence to scale digital dosing and monitoring platforms worldwide. In May 2025, Veolia secured full ownership of Water Technologies and Solutions, enabling deeper integration of coagulants and flocculants with its Hubgrade digital performance optimization systems. In April 2025, Derypol invested $1.08 million in a new reactor in Spain, adding more than 5,000 tons of annual flocculant output to support European municipal wastewater demand. During 2025, SNF also announced a $250 million expansion in Oman to establish a regional hub supplying high-volume polymers for Middle Eastern produced-water treatment and reinjection.

Throughout 2024, strategic divestments and sustainable polymer innovation reshaped the competitive landscape. In July 2024, BASF agreed to divest its mining-focused flocculants and coagulants business to Solenis, strengthening Solenis’s global position in mineral processing chemicals and tailings management solutions. In late 2024, SNF and Mitsubishi Chemical partnered to produce N-vinylformamide, a critical monomer for next-generation high-performance flocculants used in paper, textile, and specialty wastewater applications. Earlier in 2024, Solenis initiated a $193 million expansion of its Suffolk, Virginia manufacturing facility, adding significant capacity for organic coagulants serving North American drinking water and industrial effluent markets. In 2024, Kemira launched Superfloc® BioMB, the industry’s first large-scale biomass-balanced polyacrylamide line, delivering equivalent performance to conventional petroleum-based flocculants while lowering carbon footprint metrics sought by municipal utilities and sustainability-driven procurement frameworks.

Municipal and industrial water treatment plants are accelerating the shift from conventional aluminum sulfate to Polyaluminum Chloride and other pre-polymerized inorganic coagulants to reduce sludge volumes and improve process stability. Field audits conducted during 2024–2025 indicate that high-basicity PACl formulations can cut residual sludge generation by up to 40%. This is economically significant as sludge handling and disposal now account for close to one-quarter of total operating costs in several North American and European treatment facilities.

Regulatory pressure is reinforcing this transition. The revised EU Urban Wastewater Treatment Directive finalized in late 2025 introduces stricter nutrient and phosphorus removal targets, favoring coagulants with wider pH tolerance and faster floc formation. High-basicity PACl reduces reliance on downstream pH correction chemicals, lowering chemical consumption and simplifying operations.

Supply-side capacity is expanding in response. In February 2025, Gujarat Alkalies and Chemicals Limited commissioned a 32,000 tonnes per annum liquid PAC facility alongside a 9,900 tonnes per annum spray-dried powder unit. This investment reflects strong demand growth across municipal water treatment, textiles, and heavy industry, particularly in Asia-Pacific and export markets requiring stable, high-performance coagulants.

Environmental scrutiny of petroleum-based polyacrylamides is accelerating the adoption of biomass-balanced and bio-derived organic flocculants, especially in food processing, mining, and environmentally sensitive watersheds. Rather than forcing operators to redesign treatment systems, suppliers are positioning these products as drop-in replacements with lower carbon footprints.

During 2024–2025, Kemira introduced its Superfloc BioMB portfolio, representing the first commercially available biomass-balanced flocculants certified under ISCC Plus. By partially replacing fossil-derived raw materials with bio-based feedstocks, utilities can reduce Scope 3 emissions without modifying dosing or mixing infrastructure.

Performance data supports broader adoption. An August 2024 study published in Scientific Reports showed that a bio-based cationic flocculant achieved a 61.3% reduction in chemical oxygen demand in food industry wastewater. This outperformed conventional surfactants at a lower unit cost, strengthening the business case for sustainable chemistries beyond regulatory compliance.

In mining, sustainability has moved from pilot projects to procurement criteria. By November 2025, around 43% of new product development in the mining flocculant segment focused on green or hybrid chemistries. In Europe, the use of traditional inorganic salts in sensitive catchments declined by 17% year over year as operators adopted bio-based alternatives to meet stricter permitting conditions.

Electrification is reshaping demand patterns for flocculants and coagulants, particularly in lithium, copper, and nickel extraction. With electric vehicle sales projected to exceed 20 million units in 2025, lithium demand increased by roughly 30% year on year. Solid-liquid separation chemicals have become essential enablers for Direct Lithium Extraction and tailings management, where water recovery rates approaching 90% are now required to achieve water-neutral mining certifications.

This has driven a shift toward tailored chemistries. SNF Group has expanded its portfolio to more than 1,100 organic coagulants and flocculants, enabling site-specific optimization based on ore mineralogy, pH, and brine salinity. By late 2025, 38% of mining operators preferred customized formulations over standardized products, reflecting the complexity and value-at-risk in critical mineral processing.

Strategic consolidation is reinforcing this opportunity. In September 2025, Kemira acquired Water Engineering Inc. for $150 million to strengthen its position in industrial water treatment services. The transaction targets mining and hydrometallurgical operations where integrated chemical solutions and on-site expertise command higher margins and longer-term contracts.

Emerging regulations on per- and polyfluoroalkyl substances are creating a premium market for coagulants used as pre-treatment agents ahead of advanced filtration. Rather than replacing existing systems, utilities are increasingly relying on enhanced coagulation to protect costly downstream technologies such as granular activated carbon and ion-exchange resins.

A 2024 study in Environmental Science: Advances demonstrated that combining conventional alum dosing with a cationic surfactant aid achieved greater than 98% removal of both long-chain and short-chain PFAS compounds. This approach significantly reduces fouling and extends media life in adsorption systems, lowering total treatment costs.

Microplastics are also driving specification upgrades. Research completed in 2025 shows that high-basicity PAC grades exceeding 60% basicity can capture up to 90% of microplastic particles during primary flocculation. This capability is becoming a standard requirement for new municipal wastewater plants across North America and Asia-Pacific.

Compliance spending is set to rise. Following the U.S. Environmental Protection Agency’s 2024 mandate establishing enforceable parts-per-trillion limits for PFAS in drinking water, municipal investment in specialized adsorption-aid coagulants is expected to increase through 2026. Utilities are prioritizing chemical solutions that allow rapid upgrades of legacy infrastructure while maintaining operational continuity.

Flocculants accounted for 54.80% of the Flocculant and Coagulant Market share in 2025, making them the dominant chemical category used in modern water and wastewater treatment processes. Flocculants—primarily organic polymer-based compounds such as polyacrylamides and modified acrylamide copolymers—play a critical role in water purification systems by aggregating destabilized suspended particles into larger flocs, allowing them to settle rapidly or be removed through filtration. These chemicals are widely applied across municipal wastewater treatment plants, industrial effluent treatment systems, sludge dewatering facilities, and mining process water clarification, where efficient solid-liquid separation is essential for operational efficiency and regulatory compliance. In 2025, technological advancements in cationic polymer flocculants are significantly improving treatment performance. Manufacturers have developed next-generation polymers with optimized molecular weight distribution and tailored charge density, enabling stronger particle aggregation and improved sludge compaction. These innovations allow treatment facilities to achieve higher cake solids during sludge dewatering, reduced polymer dosage rates, and lower overall chemical consumption, which improves both operational efficiency and cost management. As regulatory discharge standards become more stringent worldwide, advanced polymer flocculants continue to strengthen their leadership position in the global flocculant and coagulant market.

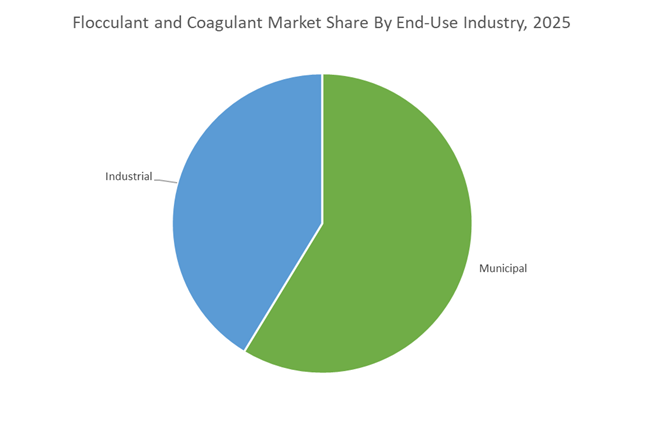

Municipal applications represented 58.70% of the Flocculant and Coagulant Market share in 2025, reflecting the critical role of chemical treatment in public water infrastructure. Municipal water and wastewater treatment facilities operate continuously to process drinking water supplies, sewage, and stormwater flows for large population centers, creating stable and recurring demand for coagulation and flocculation chemicals. These chemicals are essential for removing suspended solids, organic contaminants, phosphates, heavy metals, and microbial impurities, ensuring treated water meets regulatory discharge and potable water quality standards. A major driver shaping the municipal segment in 2025 is the growing wave of infrastructure modernization and capacity expansion projects. Many water treatment plants in North America and Europe are decades old, requiring upgrades to handle stricter environmental regulations, population growth, and climate-driven water stress. At the same time, rapid urbanization in Asia, Latin America, and parts of Africa is driving new investments in municipal wastewater treatment infrastructure. These modernization programs increasingly adopt advanced coagulation–flocculation technologies, automated dosing systems, and high-performance specialty treatment chemicals, which deliver improved removal efficiency compared with legacy systems. As a result, municipal water treatment remains the largest and most stable demand driver in the global flocculant and coagulant chemicals market.

SNF Group remains the world’s largest producer of polyacrylamide flocculants, controlling nearly 45% of the global water-soluble polymer market. Its FLOPAM™ and FLOCQUAT™ portfolios cover high-molecular-weight flocculants and cationic coagulants designed for sludge dewatering, mining tailings treatment, and municipal wastewater clarification. In 2025, SNF accelerated its Local-for-Local strategy by expanding manufacturing capacity in the United States and China to mitigate the impact of 145 percent tariff increases on chemical precursors. The company’s backward integration into acrylamide monomer production provides structural cost advantages and supply stability, reinforcing its dominance in bulk polymer chemistry. The introduction of a Bio-acrylamide enzymatic process operating at room temperature significantly lowers carbon intensity compared to conventional methods. This combination of scale, integration, and process innovation secures SNF’s leadership in high-performance flocculants for global water treatment markets.

Kemira Oyj holds the number one position in European water treatment chemicals and maintains global leadership in inorganic coagulants such as aluminum chlorohydrate. In July 2025, the company invested $23.3 million in Tarragona, Spain, to construct a new ACH production line supporting drinking water treatment demand. Kemira achieved a Leadership-level A- score in the 2025 CDP Water Security rankings, underscoring its sustainability credentials. The launch of the Superfloc BioMB line in 2025 introduced biomass-balanced flocculants with reduced carbon footprints while maintaining high flocculation efficiency in pulp, paper, and municipal wastewater applications. Under its Renewable Revenue strategy, Kemira aims to significantly increase feedstock sourcing from renewable and recyclable materials by 2030, including partnerships on alpha-glucan polymers. This transition toward low-carbon coagulants and specialty polymers reinforces Kemira’s positioning in sustainable water treatment chemistry.

Ecolab, through its Nalco Water division, differentiates itself by delivering integrated water management solutions rather than high-volume chemical supply alone. Its 3D TRASAR™ technology utilizes real-time monitoring sensors to automate coagulant and flocculant dosing, including ULTRION™ and NALKAT™ products, optimizing wastewater treatment efficiency. The company has strengthened its presence in data centers and semiconductor manufacturing, where ultrapure water and zero liquid discharge systems are mission critical. In 2025, Ecolab acquired Ovivo’s electronics ultrapure water business, reinforcing its foothold in high-tech water treatment. The 2025 Watermark™ Study highlighted rising industrial water demand driven by AI infrastructure growth, positioning digital dosing platforms as strategic water-saving tools. Through its eROI model, Ecolab quantifies measurable savings in water, energy, and operating costs, reinforcing its premium service-based model in advanced coagulant and flocculant applications.

Solenis has rapidly expanded its footprint in the flocculant and coagulant market through strategic acquisitions, including the $4.6 billion purchase of Diversey. Its portfolio includes high-performance polymers for pulp and paper processing and specialized coagulants for food and beverage wastewater treatment. In 2024 and 2025, Solenis announced a $193 million expansion in Suffolk, Virginia, increasing production capacity to meet surging North American demand for water treatment chemicals. Following integration with BASF’s paper and water business, Solenis now operates 71 manufacturing sites across 130 countries, enabling global supply continuity. The company emphasizes circular water reuse solutions for heavy industry, enabling customers to reclaim more than 90% of process water through advanced chemical separation and flocculation programs. This comprehensive service platform positions Solenis as a one-stop provider for industrial water and hygiene solutions.

BASF leverages its integrated Verbund production model to enhance efficiency in specialty flocculant and coagulant manufacturing. The startup of major facilities at the Zhanjiang Verbund site in late 2025 provides a benchmark for energy-efficient chemical production in the Asian market. Under its Winning Ways strategy for 2025 and 2026, BASF has restructured its water chemicals segment as a more agile standalone business unit to improve responsiveness in competitive municipal and industrial markets. The integration of digital monitoring with Zetag® and Magnafloc® flocculant lines enables smart dewatering, reducing sludge disposal costs by up to 15%. BASF is also transitioning toward zero-halogen and metal-free coagulants to comply with tightening European Union sludge toxicity regulations. This combination of digital integration, regulatory alignment, and production efficiency reinforces BASF’s technological relevance in advanced flocculation systems.

Kurita Water Industries remains a leading Asian provider of high-value on-site water treatment solutions, particularly in semiconductor and electronics manufacturing across Japan and China. The company differentiates through bio-based flocculants derived from natural materials such as chitosan and tannin, responding to growing ESG-driven procurement preferences. Under the Kurita Group Philosophy 2025, the firm prioritizes circular economy initiatives, including recovery of valuable minerals such as phosphorus during the flocculation process. Its 2025 and 2026 integrated reporting emphasizes expansion of Water as a Service models, where customers pay for water quality outcomes rather than chemical volumes. This shift toward performance-based contracts and resource recovery technologies positions Kurita strongly in high-tech industrial water management and sustainable flocculant chemistry.

The United States flocculant and coagulant market is being reshaped by a convergence of large-scale manufacturing investments and digitally enabled water management programs. In May 2025, Solenis announced an additional USD 76 million investment at its Suffolk, Virginia site, lifting total project capital to USD 269.4 million. The expansion includes a new 80,000-square-foot production unit and dedicated rail infrastructure, reinforcing domestic capacity for advanced polymeric flocculants used across municipal, pulp and paper, and industrial wastewater applications. This investment reflects a broader U.S. strategy of reshoring critical water treatment chemistries to ensure supply resilience as regulatory standards for nutrient removal and sludge minimization tighten nationwide.

Technology-driven water efficiency is emerging as a parallel growth lever. In October 2025, Ecolab through its Nalco Water division launched an AI-driven cooling and water management program tailored for hyperscale data centers. The platform integrates real-time monitoring of flocculation efficiency with predictive analytics to reduce cooling water consumption in AI-intensive infrastructure. The acquisition of Barclay Water Management in early 2025 further strengthened Ecolab’s digital water safety portfolio. On the public infrastructure side, accelerated disbursement from the Clean Water State Revolving Fund under the Bipartisan Infrastructure Law is enabling municipalities to upgrade coagulation systems, particularly to meet stricter phosphorus discharge limits. Collectively, these developments position the U.S. market at the intersection of polymer innovation, digital process control, and federally supported wastewater modernization.

India’s flocculant and coagulant market is undergoing structural strengthening through policy intervention and capacity investments. In March 2025, the Ministry of Finance imposed anti-dumping duties of up to USD 986 per tonne on Trichloro Isocyanuric Acid imports from China and Japan. While not a flocculant itself, this action protects upstream water treatment chemistry and incentivizes domestic production of coagulant precursors, improving supply security for municipal and industrial treatment operators. Simultaneously, SNF Flopam committed INR 800 crore in November 2025 to expand acrylamide monomer and polyacrylamide capacities at Gandhidham, Gujarat, directly addressing surging demand from industrial wastewater, mining, and textiles.

Sustainability credentials are becoming a key differentiator in India. In September 2025, BASF India achieved REDcert2 certification for its Dahej and Mangalore dispersion plants, enabling the supply of biomass-balanced, low-carbon water-based polymers to municipal utilities. In parallel, the BioE3 Policy has catalyzed the formation of biomanufacturing hubs that support the development of bio-based flocculants for food, beverage, and sensitive industrial effluents. These combined measures are accelerating India’s transition from import dependence toward a diversified portfolio of conventional and bio-derived flocculation solutions.

Spain is consolidating its role as a Southern European production hub for advanced water treatment chemicals. In July 2025, Kemira announced a nearly EUR 20 million investment to construct a new Aluminum Chloro Hydrate production line at Tarragona, scheduled for commissioning by early 2028. ACH is increasingly favored for drinking water treatment due to its high charge density and lower sludge generation. Complementing this, Derypol invested USD 1.08 million in April 2025 in a new flocculant reactor at Les Franqueses, adding 5,000 tons of annual capacity for water-synergy applications. These investments underscore Spain’s strategic focus on specialty coagulants and polymers aligned with EU drinking water quality directives.

China’s flocculant and coagulant landscape is shifting from volume-driven growth toward margin-focused specialization. Following the inauguration of its second dispersions line in 2024, BASF ramped up specialty water-based polymer dispersion output at Daya Bay in 2025, targeting high-efficiency flocculants for the pulp and paper sector. These formulations address stricter water reuse and discharge norms in industrial clusters. At the same time, Kemira initiated a profitability improvement program in Spring 2025, streamlining China operations and reducing headcount to prioritize advanced, higher-margin water treatment solutions. This recalibration reflects a maturing market where performance, not volume, defines competitive positioning.

Sweden is emerging as a center for integrated water treatment technologies. In 2025, Kemira received full investment approval for a new activated carbon reactivation plant at Helsingborg. The facility is designed to combine adsorption technologies with conventional flocculation and coagulation processes, supporting Kemira’s ambition to double its water treatment revenue. This hybrid approach addresses complex micropollutant removal challenges in European drinking water and wastewater systems, reinforcing Sweden’s role in advanced treatment innovation.

Oman is positioning itself as a regional production base for water-soluble polymers. During 2024–2025, SNF advanced its USD 250 million expansion project in the country, focused on polymers for Enhanced Oil Recovery and municipal water reuse. This investment leverages Oman’s strategic location to serve Gulf Cooperation Council markets, where desalination, produced water treatment, and reuse projects are accelerating. The development strengthens supply chains for high-performance flocculants in arid regions with acute water stress.

|

Country |

Strategic Driver |

Key Investment or Policy |

Market Impact |

|

United States |

Infrastructure funding and AI water management |

Solenis Suffolk expansion; Ecolab AI programs |

Higher polymer capacity and digital efficiency |

|

India |

Trade protection and localization |

SNF Flopam Gujarat expansion; REDcert2 polymers |

Import substitution and bio-based adoption |

|

Spain |

Drinking water quality upgrades |

Kemira ACH line; Derypol reactor |

Specialty coagulant growth |

|

China |

Margin optimization |

BASF Daya Bay ramp-up; Kemira rationalization |

Shift to high-performance solutions |

|

Sweden |

Advanced treatment integration |

Kemira Helsingborg reactivation plant |

Adsorption-flocculation convergence |

|

Oman |

Regional polymer hub |

SNF USD 250 million expansion |

GCC water reuse and EOR demand |

|

Parameter |

Details |

|

Market Size (2025) |

$13.8 Billion |

|

Market Size (2034) |

$20.2 Billion |

|

Market Growth Rate |

4.3% |

|

Segments |

By Type (Coagulants, Flocculants), By Form (Powder, Liquid, Solid), By Application (Raw Water Treatment, Municipal Wastewater Treatment, Industrial Process Water, Sludge Dewatering, Oil–Water Separation), By End-Use Industry (Municipal, Industrial) |

|

Study Period |

2019- 2025 and 2026-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Solenis, Kemira Oyj, Ecolab, SNF Group, BASF SE, Kurita Water Industries Ltd., SUEZ, Veolia Water Technologies, Feralco Group, Ixom, Gharda Chemicals Limited, Derypol S.A., Donau Chemie Group, Buckman Laboratories International, Inc., USALCO |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

*- List not Exhaustive

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Flocculant and Coagulant Market Landscape & Outlook (2026–2034)

2.1. Introduction to Flocculant and Coagulant Market

2.2. Market Valuation and Growth Projections (2026–2034)

2.3. Expansion of Municipal Water Infrastructure and Industrial Wastewater Regulations

2.4. Mining Throughput Growth and Chemical Demand for Solid-Liquid Separation

2.5. Oilfield Expansion and Polymer-Based Chemicals for Enhanced Oil Recovery

3. Innovations Reshaping the Flocculant and Coagulant Market

3.1. Trend: Transition to High-Basicity Pre-Polymerized Coagulants for Sludge Minimization

3.2. Trend: Commercialization of Biomass-Balanced and Bio-Based Organic Flocculants

3.3. Opportunity: Specialized Flocculants for Lithium and Critical Minerals Processing

3.4. Opportunity: Pre-Conditioning Coagulants for PFAS and Micropollutant Removal

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Flocculant and Coagulant Market

5.1. By Type

5.1.1. Coagulants

5.1.2. Flocculants

5.2. By Form

5.2.1. Powder

5.2.2. Liquid

5.2.3. Solid

5.3. By Application

5.3.1. Raw Water Treatment

5.3.2. Municipal Wastewater Treatment

5.3.3. Industrial Process Water

5.3.4. Sludge Dewatering

5.3.5. Oil–Water Separation

5.4. By End-Use Industry

5.4.1. Municipal

5.4.2. Industrial

5.5. By Region

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. South and Central America

5.5.5. Middle East and Africa

6. Country Analysis and Outlook of Flocculant and Coagulant Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Flocculant and Coagulant Market Size Outlook by Region (2026–2034)

7.1. North America Flocculant and Coagulant Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Form

7.1.3. By Application

7.1.4. By End-Use Industry

7.1.5. By Region

7.2. Europe Flocculant and Coagulant Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Form

7.2.3. By Application

7.2.4. By End-Use Industry

7.2.5. By Region

7.3. Asia Pacific Flocculant and Coagulant Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Form

7.3.3. By Application

7.3.4. By End-Use Industry

7.3.5. By Region

7.4. South America Flocculant and Coagulant Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Form

7.4.3. By Application

7.4.4. By End-Use Industry

7.4.5. By Region

7.5. Middle East and Africa Flocculant and Coagulant Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Form

7.5.3. By Application

7.5.4. By End-Use Industry

7.5.5. By Region

8. Company Profiles: Leading Players in the Flocculant and Coagulant Market

8.1. Solenis

8.2. Kemira Oyj

8.3. Ecolab

8.4. SNF Group

8.5. BASF SE

8.6. Kurita Water Industries Ltd.

8.7. SUEZ

8.8. Veolia Water Technologies

8.9. Feralco Group

8.10. Ixom

8.11. Gharda Chemicals Limited

8.12. Derypol S.A.

8.13. Donau Chemie Group

8.14. Buckman Laboratories International, Inc.

8.15. USALCO

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The Flocculant and Coagulant Market is expected to grow from $13.8 billion in 2025 to $20.2 billion by 2034, expanding at a CAGR of 4.3%. Market expansion is driven by increasing municipal wastewater treatment investments, industrial discharge regulations, mining throughput growth, and oilfield produced-water treatment demand. Advanced polymer flocculants and high-efficiency coagulants are becoming essential for improving solid–liquid separation efficiency and regulatory compliance across industries.

Municipal water and wastewater treatment dominates the market, accounting for approximately 58.7% of global demand in 2025. Aging water infrastructure in North America and Europe and new treatment plants in Asia-Pacific and Latin America are driving chemical consumption. These chemicals play a critical role in removing suspended solids, heavy metals, nutrients, and organic contaminants, ensuring treated water meets strict environmental discharge standards.

Sustainability initiatives are accelerating the development of biomass-balanced and bio-based flocculants, particularly for environmentally sensitive watersheds and food processing industries. Products such as biomass-balanced polyacrylamides allow utilities to reduce carbon footprint metrics while maintaining treatment performance. These innovations enable utilities to meet ESG procurement requirements without redesigning dosing infrastructure or treatment processes.

The critical minerals and lithium extraction sector is emerging as a major growth opportunity. Rapid expansion of electric vehicle production is increasing demand for lithium, copper, and nickel processing chemicals, where flocculants are essential for tailings management, brine clarification, and water recovery systems. Customized polymer formulations designed for complex mineral slurries are gaining strong adoption across mining operations.

Major industry participants include SNF Group, Kemira Oyj, Ecolab (Nalco Water), Solenis, BASF SE, Kurita Water Industries, Veolia Water Technologies, and SUEZ. These companies are investing in high-performance polymer flocculants, biomass-balanced water treatment chemicals, and AI-driven dosing technologies to improve water treatment efficiency across municipal and industrial applications.