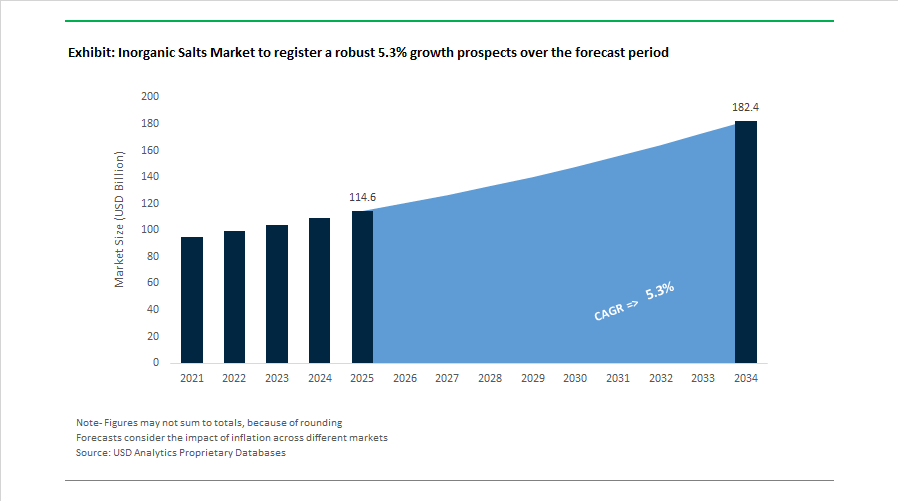

Inorganic Salts Market to Reach $182.4 Billion by 2034 at 5.3% CAGR as Battery-Grade and Electronic-Grade Segments Reshape Global Supply

The Inorganic Salts Market is projected to expand from $114.6 billion in 2025 to $182.4 billion by 2034, registering a CAGR of 5.3%. Growth is increasingly driven by lithium salts for battery electrolytes, ultra-high-purity electronic-grade salts for semiconductor manufacturing, and strategic investments in potash and industrial sodium chloride capacity. The market is undergoing a structural shift away from commodity salt applications toward high-margin specialty and energy-transition segments.

In December 2023 and throughout 2024, Sigma-Aldrich, part of Merck KGaA, launched a comprehensive portfolio of high-purity anhydrous and hydrated inorganic salts designed for pharmaceutical R&D, emphasizing precise moisture control for drug precursor stability. In 2024, Araltuz JSC in Kazakhstan commissioned a new production line for high-grade salt with NaCl purity of at least 98.5%, targeting industrial and food-processing markets in the EU and Central Asia. During the same period, K+S Group completed the transition following its $2.93 billion divestment of the Americas salt business, reinvesting capital into European potash and magnesium salt operations focused on pharmaceutical and chemical-grade purity.

Strategic energy-linked expansion accelerated in 2025. At the 2025 China Inorganic Salt Industry Development Conference, it was disclosed that China’s total sector output value is projected to exceed 680 billion yuan by year-end 2025, with lithium carbonate and lithium hydroxide capacities reaching 1.95 million and 700,000 tons annually. By late 2025, East China accounted for 70% of the nation’s electronic-grade inorganic salt capacity, supplying ultra-high-purity materials above 99.999% purity for semiconductor fabrication. During the Salt Forum 2024 and 2025 sessions, producers including HubSalt and Tata Chemicals highlighted sodium-ion batteries as a potential disruptor, increasing focus on chlor-alkali-grade salts suitable for next-generation sodium-based energy storage systems. In 2025, Neogen Chemicals leveraged U.S. 45X non-FEOC provisions to begin bulk lithium salt shipments to North America, positioning itself as a diversified alternative to Chinese supply chains. Concurrently, Vietnam met its 2025 industrial salt development target under Decision 1325/QD-TTg, maintaining 14,500 hectares and producing 1.5 million tons while transitioning to higher-value industrial output.

Capital reallocation and capacity expansion intensified into 2026. Throughout 2025 and finalized by January 2026, Arkema divested hydrogen peroxide, sodium chlorate, and related non-core salt assets, redirecting capital toward high-purity salts for electronics and energy-transition applications. In February 2026, BASF announced a new production line in Mangalore, India, dedicated to dispersions and high-performance resins utilizing inorganic salt catalysts for construction and coatings demand in South Asia. In February 2026, Neogen Chemicals reported its strategic pivot toward lithium salts and electrolytes despite temporary bottlenecks at its Dahej facility, targeting gigawatt-scale battery manufacturers and expecting global approvals by H1 FY27. By December 2025, Chinese and Indian enterprises including Asia Potash International established nearly 4.5 million tons of potash fertilizer capacity in Laos, reinforcing regional supply security for potassium-based inorganic salts across Asia’s agricultural and industrial value chains.

Inorganic Salts Market Trends and Opportunities

Multi-Billion-Dollar Scaling of High-Purity Metal Salt Precursors for EV Cathodes

The rapid global shift toward high-nickel and lithium-rich battery chemistries has structurally repositioned inorganic metal salts as mission-critical inputs for the electric vehicle value chain. Battery-grade nickel sulfate, lithium hydroxide, and cobalt sulfate are no longer treated as bulk intermediates; they are now strategic materials produced under near-semiconductor-grade discipline. By 2025, producers have moved decisively from pilot-scale purification toward industrial six-nines quality production to meet sub-ppm impurity thresholds demanded by next-generation cathode active materials.

In December 2025, industry data confirmed that more than 68% of global nickel sulfate output was being consumed by the EV sector, underscoring how deeply electrification has reshaped demand allocation. Newly commissioned hydrometallurgical hubs in the second half of 2025 tightened iron impurities to ≤100 ppm and copper to ≤50 ppm, directly translating into a 4–6% improvement in battery cell yields. For decision makers, this yield uplift materially alters the cost curve of gigafactory operations and reinforces long-term offtake agreements with salt producers capable of consistent ultra-high purity delivery.

Supply chain integration is accelerating in parallel. In July 2025, BASF Battery Materials signed a framework agreement with CATL, signaling a shift toward vertically coordinated supply models. In this structure, inorganic salt producers act as embedded partners rather than transactional vendors, leveraging geographically distributed production networks to supply localized gigafactories and reduce logistics risk.

Circularity is emerging as a second structural pillar. The commercial launch of BASF’s black mass recycling facility in Schwarzheide, Germany, in June 2025 with a capacity of 15,000 tons per year demonstrates the rise of “circular salts.” By recovering lithium, nickel, and cobalt via hydrometallurgy from end-of-life batteries, the industry is creating a domestic, lower-carbon stream of high-purity inorganic salts that reduces dependence on primary mining while strengthening supply security in Europe.

Supply Chain Volatility and Regulatory Realignment in High-Volume Industrial Salts

While battery materials are scaling up, the broader inorganic salts market is being reshaped by energy economics and regulatory intervention. High-volume salts such as sodium sulfate are experiencing pronounced geographic shifts in production as traditional hubs face rising energy costs and environmental constraints.

As of September 2025, intensified anti-dumping investigations by both the U.S. and the EU into Chinese chemical exports introduced potential duties ranging from 10% to 500%. These measures have materially altered the economics of importing commodity salts and upstream precursors, forcing downstream users to secure more expensive but politically resilient domestic supply. For procurement leaders, this has elevated supply continuity above short-term price optimization.

Energy costs are amplifying regional divergence. Pricing data from October 2025 shows sodium sulfate trading at approximately $0.27 per kilogram in Europe versus $0.24 per kilogram in North America. Elevated natural gas prices have made energy-intensive vacuum evaporation processes structurally less competitive in Europe, accelerating the shift toward solar evaporation and by-product recovery routes in energy-advantaged regions.

New mining and export hubs are emerging to address these imbalances. In May 2025, Minerals Development Oman partnered with Dev Salt to launch the Naqa Salt Project. Designed to be one of the largest facilities in the region, the project leverages solar evaporation to produce bromine-rich industrial salts targeted at export markets, offering a structurally lower-energy alternative to constrained European and North American production.

Salt Hydrates as Scalable Thermal Energy Storage Platforms

Inorganic salt hydrates are emerging as a compelling alternative to electrochemical batteries for long-duration thermal energy storage, particularly in building and district heating applications. Materials such as sodium sulfate decahydrate are being deployed as phase change materials that store and release heat at predictable temperatures, offering high safety and low cost relative to lithium-based systems.

Public funding is accelerating commercialization. In June 2025, the U.S. Department of Energy announced $15 million in funding for advanced energy storage projects, including multiple initiatives centered on iron- and sodium-based salt chemistries. These systems are being positioned for multi-day resilience in grid-stressed regions, with a clear advantage in non-flammability and material abundance.

Thermochemical salt hydrates highlighted under the DOE’s BENEFIT program demonstrated theoretical energy densities between 200 and 600 kWh per cubic meter, nearly an order of magnitude higher than paraffin-based phase change materials. This density enables compact storage modules that can be charged using excess solar energy and discharged for space heating, with projected payback periods of under five years for commercial buildings.

Commercial uptake has already begun. In early 2024, Armstrong World Industries launched its Ultima Templok ceiling system incorporating salt-hydrate PCMs, delivering up to 15% energy savings in commercial spaces. This deployment signals a scalable pathway for inorganic salts to participate directly in the decarbonization of the built environment.

High-Purity Inorganic Salts for Zero-Impurity Nutraceutical and Pharma Applications

The pharmaceutical and nutraceutical sectors are becoming a high-margin growth frontier for inorganic salts as formulations grow more sensitive and regulatory scrutiny intensifies. Excipient-grade salts meeting USP, EP, and JP standards are increasingly specified with near-zero heavy metal content to ensure patient safety and formulation stability.

In October 2025, Compass Minerals announced capital investment in a new production facility dedicated to specialty fertilizers and high-purity salts. The facility is explicitly designed to serve nutraceutical and wellness markets where trace contaminants can compromise product approvals and brand trust.

Demand for zinc sulfate and magnesium salts has accelerated sharply due to sustained post-pandemic focus on immune and metabolic health. Manufacturers are responding by investing in automated micronization and classification technologies to deliver consistent particle size distributions, a critical determinant of bioavailability in modern tablets and capsules.

Sustainability is becoming a procurement differentiator in parallel. In September 2025, Olin Corporation launched a new portfolio of eco-certified inorganic salts targeting pharma and personal care brands that require documented low-carbon footprints across their ingredient supply chains. For decision makers, this convergence of purity, performance, and sustainability is redefining competitive advantage in the inorganic salts market.

Inorganic Salts Market Share and Segmentation Insights

Sodium Salts Lead the Inorganic Salts Market Through Large-Scale Industrial and Chemical Applications

Sodium salts represented 42.80% of the Inorganic Salts Market share in 2025, making them the most widely consumed salt category across global industrial sectors. Sodium-based salts such as sodium chloride, sodium carbonate, sodium bicarbonate, sodium sulfate, and sodium phosphates are fundamental raw materials in numerous industrial and commercial applications including chemical manufacturing, water treatment, food processing, detergents, and agricultural inputs. Among these, sodium chloride holds the largest volume share due to its extensive use in chlor-alkali production, where it serves as the primary feedstock for manufacturing chlorine, caustic soda, and hydrogen. These products form the backbone of the global chemical industry, supporting downstream production of PVC plastics, solvents, disinfectants, and water treatment chemicals. In 2025, sodium salt demand continues to closely track the performance of the chlor-alkali industry, making sodium salts a critical indicator of overall chemical sector activity. Increasing global consumption of PVC, industrial cleaning chemicals, and water treatment agents continues to reinforce the strategic importance of sodium salts in industrial supply chains.

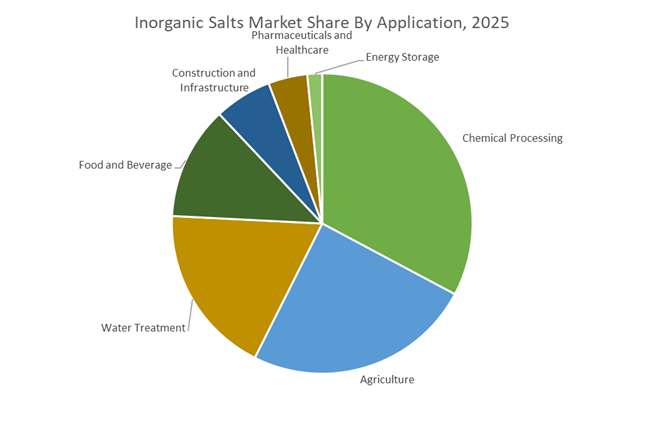

Chemical Processing Sector Generates the Largest Demand for Inorganic Salts

Chemical processing accounted for 32.80% of the Inorganic Salts Market share in 2025, positioning it as the leading end-use sector for inorganic salt consumption. The chemical industry relies heavily on inorganic salts as feedstocks, catalysts, intermediates, and processing agents in the production of a wide range of industrial chemicals including acids, pigments, fertilizers, detergents, polymers, and specialty chemicals. Sodium, potassium, calcium, and ammonium salts are routinely used in large-scale industrial reactions where they function as reactants, neutralizing agents, buffering compounds, and separation media. The scale of global basic chemical manufacturing ensures continuous demand for these salts across multiple processing stages. In 2025, sustainability initiatives within chemical manufacturing have also accelerated the adoption of industrial salt recovery and recycling technologies, enabling producers to recover valuable salts from process streams and reduce waste generation. Established examples include sodium sulfate recovery from viscose fiber production and ammonium sulfate recovery during caprolactam manufacturing, demonstrating how circular chemical processing strategies are reshaping inorganic salt supply chains.

Competitive Landscape in Inorganic Salts Market

K+S Aktiengesellschaft Expands Industrial Added Value and Mineral Security

K+S Aktiengesellschaft is a leading global supplier of potassium and magnesium salts, reinforcing its role across pharmaceutical-grade, industrial, and agricultural value chains. The company produces high-purity API-grade salts used in dialysis and infusion therapies, alongside industrial rock salt exceeding 99% NaCl purity and magnesium sulfate products. In late 2025, leadership emphasized Mining and Energy Resilience, advocating for strengthened European mineral sovereignty and diversified rare mineral extraction aligned with core potash operations. In December 2025, K+S expanded its Industrial Applications portfolio to deepen engagement with glass, plastics, and textile manufacturers. Through subsidiaries such as K+S North America and K+S Asia Pacific, the company operates a broad logistics network to ensure secure distribution of inorganic salts globally. Sustainable mining practices and long-term resource stewardship remain central to its strategy for industrial and food security.

Tata Chemicals Limited Accelerates Soda Ash and Specialty Salt Capacity

Tata Chemicals Limited, a flagship entity of the Tata Group, is expanding production capacity to meet growing demand for soda ash, iodized vacuum salt, and precipitated silica across Asia. In February 2026, the company approved a ₹515 crore investment to establish a greenfield IVSD manufacturing facility in Tamil Nadu with 210 KTPA capacity, strengthening its footprint in South India. Earlier in November 2025, the board sanctioned a ₹910 crore expansion at Mithapur and Cuddalore, adding 350 KTPA of dense soda ash and 50 KTPA of precipitated silica. By creating a second major manufacturing hub in southern India, Tata Chemicals aims to reduce logistics costs, shorten delivery cycles, and enhance supply chain resilience. Its flagship Mithapur complex maintains a global IVSD capacity of 1.6 million tonnes per annum, positioning the company as a dominant producer in industrial salt and alkali markets.

Compass Minerals Focuses on Sustainable Salt and Magnesium Solutions

Compass Minerals International is a key North American producer of sodium chloride and magnesium chloride, serving de-icing, water conditioning, and agricultural nutrient markets. In 2026, the company executed a binding agreement with the State of Utah to donate 201,000 acre-feet of water rights annually to support conservation of the Great Salt Lake, underscoring environmental stewardship commitments. The Sifto Industrial brand remains integral to industrial salt purity and water treatment segments. Fiscal 2026 Q1 results emphasized capital discipline and margin optimization within the salt segment amid volatile winter demand patterns. At its Ogden facility, Compass remitted 65,000 acres of leasehold land back to the state, reinforcing a Sustainable Production strategy that balances output with ecological preservation.

Solvay S.A. Repositions Toward High-Purity Electronic and Automotive Salts

Solvay has transitioned from commodity-heavy operations toward specialty inorganic salts targeting electronics, automotive, and advanced materials sectors. In early 2026, the company discontinued select inorganic product lines including hydrogen fluoride at its Bad Wimpfen site to convert the facility into a global innovation hub for Nocolok automotive brazing technologies. Recent product introductions include high-purity inorganic salts tailored for semiconductor fabrication and battery chemistries, reflecting strong growth in electronic-grade chemicals. Solvay allocated €25 million for restructuring and strategic investments to secure competitiveness in challenging European conditions. Consolidation of its Nocolok Tech Center at Bad Wimpfen strengthens its leadership in aluminum brazing flux technologies critical to automotive heat exchanger manufacturing.

Yara International ASA Advances Industrial Nitrogen and Clean Ammonia Strategy

Yara International is pivoting toward industrial nitrogen-based salts and low-emission ammonia as part of its broader industrial solutions transformation. At its January 2026 Capital Markets Day, the company outlined a roadmap to expand free cash flow by over $600 million through 2030, emphasizing premium nitrogen product portfolios. Yara is evaluating a potential $2 billion U.S. investment in low-emission ammonia in partnership with Air Products, with a final investment decision expected mid-2026. Since 2024, the company has delivered over $200 million in fixed cost reductions, improving competitiveness in industrial ammonium salts and specialty nitrate applications. Enhanced asset utilization and logistics optimization are targeted to generate an incremental $200 million EBITDA uplift by 2027, reinforcing its position in high-margin industrial nitrogen chemistry.

Nouryon Strengthens Innovation and Digitalized Production of Specialty Salts

Nouryon continues to expand its essential chemicals portfolio with a focus on inorganic salts, catalysts, and water treatment chemicals. Its new Customer Experience and Innovation Center in Brazil, expected to be fully operational by late 2026, will emphasize bio-based chelants and advanced salt formulations for home, personal care, and industrial sectors. The company recently doubled organic peroxide production capacity in Ningbo, China, supporting global polymer and coatings demand. Through a Digitalization and Industry 4.0 strategy, Nouryon integrates AI and advanced analytics across 15 innovation centers to optimize bulk chemical and inorganic salt production efficiency. Its portfolio includes salt-based catalysts, bleaching chemicals, and coagulants essential for municipal water treatment and pulp and paper manufacturing, strengthening its position in performance-driven specialty inorganics.

United States Inorganic Salts Market: Formulation Science, Agricultural Inputs, and Water Infrastructure Pull

The United States inorganic salts industry is evolving through formulation-led innovation, targeted agricultural investments, and structurally funded water infrastructure programs. Between February 2024 and 2025, Procter & Gamble secured two foundational patents, US 11,904,034 B2 and US 11,904,036 B2, covering clear personal cleanser systems engineered with stabilized ultra-low inorganic salt content. These patents reflect a material shift in surfactant formulation strategy, where precise salt control improves product clarity and skin mildness while preserving viscosity performance. In parallel, regulatory-driven reformulation is reshaping food-grade salt demand. In 2025, the U.S. Food and Drug Administration proposed expanded allowances for potassium chloride as a sodium-reduction substitute across more than forty standardized food categories, catalyzing accelerated adoption of potassium-based inorganic salts in dairy, canned vegetables, and processed foods.

Industrial and agricultural demand vectors are reinforcing this trajectory. In October 2025, Compass Minerals announced a capital investment to build a new specialty fertilizer facility focused on high-solubility inorganic salt nutrients for the 2026 crop cycle. Environmental compliance is also shaping portfolios. Olin Corporation launched a line of eco-friendly inorganic salts in September 2025 designed for lower environmental toxicity, aligning with EPA sustainability benchmarks effective in 2026. Public spending remains a stabilizing force, with California allocating $221 million during FY 2024–25 for water-quality projects that drive bulk procurement of inorganic salts for wastewater treatment and reverse osmosis pretreatment. On the healthcare front, U.S. manufacturers are optimizing pharmaceutical-grade sodium chloride for single-use ophthalmic and nasal products, with 2026 production lines emphasizing high-purity crystallization to meet tighter clinical specifications.

India Inorganic Salts Market: Policy Capital, Energy Efficiency Mandates, and Scale Expansion

India’s inorganic salts industry is being structurally reshaped by fiscal allocation, carbon accountability, and rapid capacity expansion across chemicals and fertilizers. The Union Budget 2025–26 allocated ₹1,61,965 crore to the Ministry of Chemicals and Fertilizers, channeling significant resources into the Production-Linked Incentive scheme for Advanced Chemistry Cell battery storage. This policy direction is materially increasing demand for lithium and sodium-based inorganic salts used in electrolyte systems and precursor materials. Carbon governance is becoming a defining operational constraint. The launch of the Carbon Credit Trading Scheme in mid-2026 will bind more than one thousand entities across energy-intensive sectors, including chlor-alkali and fertilizer producers, incentivizing the commercialization of low-emission Green Salts.

Corporate capital expenditure is aligning with these mandates. Tata Chemicals confirmed plans to invest ₹8,000 crore through 2027 to scale soda ash and industrial salt operations with a focus on lower-carbon manufacturing. At the regional level, Shivtek Spechemi Industries commissioned a new Hazira chemical facility in 2025 spanning more than one million square feet, targeting 250,000 MTPA capacity by 2027–28 for high-demand inorganic intermediates. Regulatory pressure is intensifying operational efficiency. Under the 2025 notification from the Ministry of Environment, Forest and Climate Change, chlor-alkali and fertilizer sectors must achieve emission intensity reductions ranging from 3.3% to 11% by 2025–26, accelerating adoption of energy-efficient electrolysis. Strategic consolidation is also altering global flows. In March 2025, Sudarshan Chemical completed the acquisition of Germany-based Heubach Group, integrating large-scale inorganic salt processing for pigments into an Indo-European supply chain.

China Inorganic Salts Market: Purity Upgrading and Agricultural Security

China’s inorganic salts industry is prioritizing quality upgrading and agricultural resilience to stabilize downstream sectors. In 2025, domestic producers accelerated the transition from traditional solar salt to high-purity vacuum salt to meet rising standards in food processing and chemical manufacturing. This shift is improving consistency and solubility for industrial-grade applications, including detergents, pharmaceuticals, and specialty chemicals.

Policy support remains central to agricultural inputs. During 2025, the Chinese government expanded credit programs to stabilize supplies of potassium chloride and ammonium sulfate, insulating nutrient availability from natural gas price volatility that could otherwise disrupt the 2026 harvest season. Industrial chemistry demand is also rising. Major clusters are scaling electrolysis of aqueous sodium chloride to increase sodium hypochlorite output, supporting projected 2026 demand in textile bleaching and municipal water chlorination. These developments collectively signal a pivot toward higher-purity salts with tighter process control across food, agriculture, and municipal infrastructure.

Germany Inorganic Salts Market: Energy Storage Integration and Pigment Precursor Realignment

Germany’s inorganic salts industry is increasingly linked to energy transition technologies and high-performance materials. In early 2025, K+S Aktiengesellschaft announced collaborations with Sulzer and Arla Foods to deploy inorganic salt-based thermal energy storage systems. These projects position salts as functional materials within the EU Green Deal framework, supporting 2026 targets for renewable integration and industrial decarbonization.

Industrial restructuring is also underway. Following its acquisition by Sudarshan Chemical, Heubach’s German production sites are being retooled to manufacture high-performance inorganic metal salts used as precursors for automotive pigments. This reconfiguration reflects Germany’s shift toward higher-value, application-specific salt derivatives that serve advanced coatings and mobility markets rather than bulk commodity supply.

Inorganic Salts Industry: Country-Level Strategic Snapshot

Inorganic Salts Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Direction

|

|

United States

|

Formulation patents, food reformulation, water infrastructure

|

Personal care, fertilizers, wastewater treatment

|

High-purity and application-specific salts

|

|

India

|

Budgetary support, carbon trading, capacity build-out

|

Batteries, chlor-alkali, pigments

|

Scale with low-carbon manufacturing

|

|

China

|

Purity upgrading and agricultural security

|

Food processing, fertilizers, municipal chemicals

|

Transition from volume to quality

|

|

Germany

|

Energy transition and pigment precursors

|

Thermal energy storage, automotive pigments

|

High-value functional salt derivatives

|

Inorganic Salts Market Report Scope

Inorganic Salts Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$114.6 Billion

|

|

Market Size (2034)

|

$182.4 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Salt Type (Sodium Salts, Magnesium Salts, Calcium Salts, Potassium Salts, Ammonium Salts, Specialty Inorganic Salts), By Grade (Pharmaceutical Grade, Food Grade, Agricultural Grade, Industrial Grade), By Form (Powder, Granular, Crystal, Solution), By Application (Agriculture, Pharmaceuticals and Healthcare, Food and Beverage, Chemical Processing, Water Treatment, Energy Storage, Construction and Infrastructure)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cargill, Incorporated, K+S Aktiengesellschaft, Compass Minerals International, Inc., Tata Chemicals Limited, China National Salt Industry Corporation, Akzo Nobel N.V., INEOS Enterprises, Nutrien Ltd., Olin Corporation, Loba Chemie Pvt. Ltd., BASF SE, LANXESS AG, Thermo Fisher Scientific Inc., Otsuka Chemical Co., Ltd., Rio Tinto Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Inorganic Salts Market Segmentation

By Salt Type

- Sodium Salts

- Magnesium Salts

- Calcium Salts

- Potassium Salts

- Ammonium Salts

- Specialty Inorganic Salts

By Grade

- Pharmaceutical Grade

- Food Grade

- Agricultural Grade

- Industrial Grade

By Form

- Powder

- Granular

- Crystal

- Solution

By Application

- Agriculture

- Pharmaceuticals and Healthcare

- Food and Beverage

- Chemical Processing

- Water Treatment

- Energy Storage

- Construction and Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Inorganic Salts Industry

- Cargill, Incorporated

- K+S Aktiengesellschaft

- Compass Minerals International, Inc.

- Tata Chemicals Limited

- China National Salt Industry Corporation

- Akzo Nobel N.V.

- INEOS Enterprises

- Nutrien Ltd.

- Olin Corporation

- Loba Chemie Pvt. Ltd.

- BASF SE

- LANXESS AG

- Thermo Fisher Scientific Inc.

- Otsuka Chemical Co., Ltd.

- Rio Tinto Group

*- List not Exhaustive