Floor Coatings Market Growth Driven by Industrial Flooring Demand, Fast-Cure Technologies, and Infrastructure Modernization

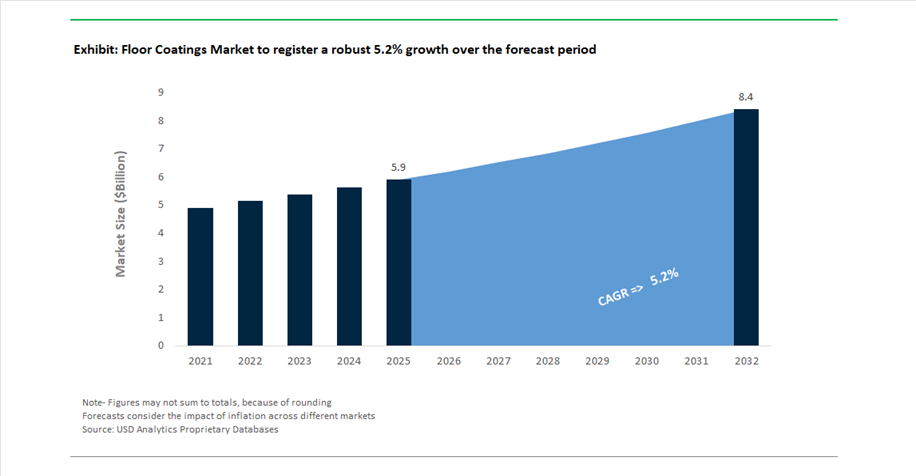

The global Floor Coatings Market was valued at USD 5.9 billion in 2025 and is projected to grow at a CAGR of 5.2% between 2025 and 2032, reaching USD 8.4 billion by 2032. This growth is driven by increasing demand for durable, hygienic, and high-performance flooring systems across industrial facilities, healthcare environments, commercial buildings, and logistics infrastructure.

Floor coatings—primarily based on epoxy, polyurethane, and methyl methacrylate (MMA) chemistries—are essential for providing chemical resistance, abrasion durability, anti-slip properties, and easy maintenance. A key structural driver is the expansion of high-specification environments such as pharmaceutical cleanrooms, food processing plants, semiconductor facilities, and data centers, where flooring must meet strict regulatory and operational standards.

Another major growth catalyst is the rise of cold-chain logistics and e-commerce warehousing, which is accelerating demand for coatings capable of curing in low-temperature environments with minimal downtime. Additionally, the growing emphasis on sustainability and decarbonization in construction is driving the adoption of low-VOC, high-solids, and cementitious flooring systems that reduce environmental impact while maintaining performance.

Fast-Cure Flooring Systems, and Cold-Storage Coating Innovation Reshape Market Dynamics

The floor coatings market is undergoing significant transformation driven by industry consolidation, technological innovation, and regional expansion strategies. In November 2025, AkzoNobel and Axalta Coating Systems announced a $25 billion merger, combining their industrial flooring portfolios to create a unified global platform for high-performance flooring systems, particularly targeting data centers and heavy industrial environments.

Product innovation is increasingly focused on speed and efficiency. In June 2025, Sherwin-Williams received a Top Product Award for its Accelera One system, a high-solids urethane grout and topcoat capable of curing for foot traffic in just two hours. This innovation addresses the critical need for rapid installation and minimal operational disruption in high-traffic environments such as hospitals and pharmaceutical facilities.

Technological advancements are also enabling new application environments. In April 2026, industry trends highlighted the rapid adoption of MMA-based floor coatings, which can cure at temperatures as low as -20°C, making them ideal for cold-storage warehouses and refrigerated logistics facilities. This shift reflects the growing importance of zero-downtime maintenance solutions in global supply chains.

Capacity expansion and regional manufacturing investments are strengthening supply chains. In October 2024, Stonhard opened a major automated manufacturing facility in Malaysia, significantly increasing production capacity for resinous flooring systems to meet demand from semiconductor and electronics sectors in Southeast Asia.

Strategic acquisitions and regional restructuring are also shaping competition. In June 2025, JSW Paints acquired a majority stake in AkzoNobel India, strengthening its position in the industrial flooring segment. Similarly, in October 2025, BirlaNu acquired Clean Coats to expand its presence in epoxy and polyurethane flooring systems for specialized applications such as cleanrooms and food processing facilities.

Material innovation is also advancing substrate preparation and system performance. In September 2025, BASF launched Acronal® primers designed for flowable hydraulic cement underlayments, improving adhesion and substrate control for modern self-leveling flooring systems.

Operational efficiency and sustainability initiatives are gaining traction. In February 2026, Sika AG reported growth in high-value flooring solutions while implementing its “Fast Forward” program to optimize supply chains and improve profitability. Additionally, Master Builders Solutions expanded manufacturing capacity with a focus on low-carbon flooring materials, supporting decarbonization efforts in large-scale construction projects.

Fast-Cure Polyaspartic Floor Coatings Gaining Traction in Cold-Chain Logistics Infrastructure

The floor coatings industry is witnessing a decisive shift toward polyaspartic coatings in cold-storage and logistics environments, driven by the need to minimize operational downtime and ensure performance in sub-zero conditions. Traditional epoxy coatings face critical limitations in cold-chain applications, particularly due to their inability to properly cure at low temperatures and their susceptibility to brittleness under thermal stress. In contrast, polyaspartic floor coatings offer rapid curing capabilities, achieving full traffic readiness within one to two hours compared to the 24 to 72 hours required for industrial epoxy systems. For large-scale cold storage facilities, this translates into the recovery of up to 70 hours of operational uptime during maintenance cycles, directly impacting revenue continuity. From a performance standpoint, polyaspartic resins maintain significantly higher flexibility, approximately 98% greater than standard epoxies, allowing them to withstand thermal expansion and contraction in environments reaching temperatures as low as minus 30 degrees Celsius. This flexibility reduces the risk of cracking and delamination, which are common failure modes in epoxy-coated floors under extreme conditions. Additionally, lifecycle performance data from 2026 indicates that polyaspartic systems can achieve service lifespans exceeding 20 years in high-traffic distribution centers, substantially outperforming epoxy coatings that typically require replacement within five to seven years. These advantages are positioning polyaspartic coatings as the preferred solution for high-performance industrial flooring in cold-chain logistics and food distribution facilities.

Slip-Resistant Floor Coatings Becoming Mandatory for Multifamily Balcony Safety Compliance

The increasing frequency of slip-and-fall litigation in residential real estate is driving a structural shift in the specification of exterior floor coatings, particularly for multifamily balconies and walkways. Property owners and developers are moving beyond basic waterproofing systems toward advanced slip-resistant coatings that integrate safety compliance into material design. Regulatory and legal pressures are prompting the adoption of coatings that meet minimum Dynamic Coefficient of Friction thresholds of 0.42 for wet surfaces, necessitating the use of aggregate-enhanced resinous systems that provide consistent traction under varying environmental conditions. This shift is being reinforced by the growing role of liability management in property operations, where failure to meet slip-resistance standards can result in substantial financial penalties, including multi-million-dollar lawsuits and insurance coverage limitations. As a result, property managers are implementing formalized safety programs that include documented coefficient of friction testing and third-party certification to establish compliance records. Maintenance practices are also evolving, with routine inspections now incorporating quantitative slip-resistance measurements rather than relying solely on visual assessments. This documentation serves as a critical legal safeguard in liability disputes. The integration of safety performance into floor coating specifications is transforming the market, driving demand for high-friction, durable exterior coatings tailored to residential and commercial building applications.

Antimicrobial Floor Coatings Driven by US VA Healthcare Modernization Initiatives

The modernization of healthcare infrastructure, particularly within the United States Department of Veterans Affairs system, is creating a significant opportunity for antimicrobial floor coatings designed to enhance infection control. Healthcare-associated infections remain a major concern in clinical environments, driving demand for floor systems that actively inhibit microbial growth. Current initiatives under the 2025 to 2026 research and infrastructure programs are prioritizing the deployment of seamless, non-porous resinous flooring systems that eliminate grout lines, which are known to harbor bacteria and pathogens. These advanced coatings are being engineered with integrated antimicrobial agents capable of suppressing organisms such as methicillin-resistant Staphylococcus aureus and Clostridioides difficile at critical junctions such as floor-to-wall coving. In addition to antimicrobial performance, there is a strong emphasis on low-VOC formulations to ensure indoor air quality compliance in sensitive healthcare environments. The broader antimicrobial coatings market in North America is projected to reach approximately 16.43 billion dollars in 2025, with hospital flooring representing a key growth segment driven by regulatory and institutional demand. The convergence of infection control priorities, regulatory compliance, and infrastructure investment is positioning antimicrobial floor coatings as a core component of next-generation healthcare facility design.

Germany’s AgBB and BImSchV Standards Driving Adoption of Low-Emission Floor Coatings in Public Buildings

Germany’s stringent indoor air quality regulations are setting a global benchmark for low-emission floor coatings, creating a strong opportunity for manufacturers capable of meeting advanced environmental compliance standards. Under the AgBB evaluation framework and the Federal Immission Control Ordinance, floor coatings used in indoor public spaces must undergo rigorous emission testing to ensure minimal release of volatile organic compounds and hazardous substances. Products are required to pass both short-term and long-term chamber tests, typically conducted over three-day and twenty-eight-day periods, to demonstrate compliance with strict exposure limits. Certification through recognized labels such as Blue Angel has become a prerequisite for use in schools, hospitals, and government buildings, effectively establishing low-emission coatings as the standard in public sector procurement. These requirements are driving innovation in waterborne, solvent-free, and ultra-low VOC coating technologies that balance environmental safety with performance durability. Furthermore, Germany’s regulatory framework is increasingly influencing broader European construction standards, positioning early-compliant manufacturers to gain a competitive advantage as similar requirements are adopted across the European Union. This regulatory alignment is expanding the addressable market for sustainable floor coatings and reinforcing the importance of emission-certified products in global construction and infrastructure projects.

Floor Coatings Market Share 2025: Self-Leveling Systems and Anti-Slip Performance Lead Demand

Application Method Insights: Self-Leveling Coatings Dominate for Seamless Industrial Flooring

The self-leveling segment leads the floor coatings market with a dominant 48% market share in 2025, driven by its critical role in delivering smooth, seamless, and hygienic flooring solutions across high-performance environments. Self-leveling epoxy and polyurethane floor coatings are extensively used in pharmaceutical cleanrooms, food processing facilities, and electronics manufacturing plants, where joint-free surfaces prevent bacterial growth, dust accumulation, and contamination risks. These coatings flow uniformly across substrates, creating flawless finishes essential for compliance with strict hygiene and safety standards. Additionally, self-leveling systems significantly reduce labor costs and application time, as they require fewer skilled workers and minimal surface preparation compared to traditional high-build or multi-coat systems. This efficiency makes them highly attractive for large-scale industrial and commercial flooring projects. As industries prioritize durability, cleanliness, and operational efficiency, self-leveling floor coatings will continue to dominate market adoption.

Functional Characteristic Insights: Anti-Slip Coatings Lead with Safety Compliance Requirements

The anti-slip segment holds the largest 28% share in the floor coatings market in 2025, driven by increasing emphasis on workplace safety regulations and accident prevention. Regulatory bodies such as OSHA and EU workplace safety directives mandate the use of slip-resistant flooring systems in high-risk environments including commercial kitchens, hospitals, car washes, and industrial wet areas. Anti-slip floor coatings enhance traction and reduce the risk of workplace injuries, making them a critical specification in both new construction and renovation projects. Technological advancements are further boosting this segment, with manufacturers incorporating aggregate additives such as aluminum oxide, silica, and polymer grit into epoxy and polyurethane coatings to achieve long-lasting slip resistance without compromising cleanability or aesthetics. As safety compliance becomes increasingly stringent across industries, anti-slip functional coatings will remain a key growth driver in the global floor coatings market.

Floor Coatings Market Competitive Landscape: Innovation, Sustainability, and High-Performance Systems Driving Market Leadership

The global floor coatings market is highly consolidated, led by multinational players leveraging advanced materials science, digital integration, and sustainability-driven innovations. Market leaders are focusing on high-performance industrial flooring, eco-friendly formulations, and strategic expansions to strengthen their position across construction, manufacturing, and infrastructure segments.

Sherwin-Williams accelerates high-margin industrial flooring growth through rapid innovation and global distribution

The Sherwin-Williams Company is strengthening its leadership in the floor coatings market by targeting high-margin commercial and industrial segments amid a softer demand environment. The company projects adjusted diluted EPS of $11.50 to $11.90 in 2026, supported by high-single-digit growth in its Protective & Marine segment and strong residential repaint demand. Its expansion of the global retail footprint by 10% enhances just-in-time distribution capabilities for professional floor contractors across North America and emerging Asian markets. Sherwin-Williams is scaling its high-performance flooring portfolio with systems enabling 30% faster return-to-service times, a critical differentiator in industrial manufacturing environments. The integration of the Suvinil acquisition is accelerating its dominance in South America’s decorative floor coatings market, the company continues to optimize its portfolio toward premium industrial solutions.

PPG Industries strengthens digital floor coating ecosystems and sustainable product dominance

PPG Industries is advancing its competitive position through digital innovation and sustainability leadership in industrial floor coatings. The company reported Q1 2026 adjusted EPS of $1.83, reflecting a 6% year-over-year increase driven by share gains in automotive OEM and industrial flooring applications. 43% of PPG’s sales now come from sustainably advantaged products, including low-VOC and bio-based floor coating systems. PPG dominates the concrete floor coatings segment, which accounts for 75.7% of total market revenue, through advanced moisture-vapor barriers and high-performance epoxy systems. Its PPG LINQ™ platform introduces real-time monitoring of coating wear using embedded sensors, enhancing predictive maintenance capabilities for facilities managers. Following a $2 billion divestiture of its architectural retail business, PPG is reallocating R&D investments toward high-growth segments such as electronics manufacturing and data center flooring.

AkzoNobel integrates design-driven coatings with eco-efficient production strategies

AkzoNobel N.V. is differentiating its floor coatings portfolio by merging aesthetic innovation with industrial-grade performance. The launch of its “Rhythm of Blues™” 2026 palette aligns with the growing “designer industrial” trend, enabling architects to combine visual appeal with durability in commercial flooring systems. Nearly 40% of its portfolio consists of eco-friendly, low-solvent coatings, contributing to a 10% improvement in global production efficiency. The company maintains strong market presence across Europe and Asia-Pacific, particularly in water-borne and powder-based floor coating technologies. Through partnerships with architects, AkzoNobel provides “Surface Genealogy” tracking to ensure full compliance with stringent EU green-building standards. This integration of sustainability, traceability, and design innovation positions AkzoNobel as a key player in premium architectural and industrial floor coatings.

Sika drives low-carbon industrial flooring leadership with digital transformation and ESD specialization

Sika AG is reinforcing its leadership in high-performance industrial flooring through sustainability and operational excellence. The company expects 1% to 4% sales growth in 2026 while aiming to outperform the broader market by 3% to 6% through targeted acquisitions in flooring and sealing solutions. Its digital transformation and plant optimization initiatives are projected to generate CHF 80 million in annual savings, improving cost efficiency and scalability. Sika has reduced Scope 1 and 2 emissions by 6.1%, positioning its Sikafloor® range as a low-carbon solution for large-scale industrial and pharmaceutical facilities. The company dominates the monolithic flooring segment and is a key provider of electrostatic discharge (ESD) flooring solutions critical for semiconductor gigafabs. This specialization enables Sika to capitalize on the rapid expansion of global semiconductor manufacturing infrastructure.

RPM International delivers seamless flooring dominance through vertically integrated solutions

RPM International Inc., through its Performance Coatings Group (PCG), is achieving strong growth in the global floor coatings market with a focus on turnkey solutions. The company reported record Q1 2026 sales of $2.11 billion, reflecting a 7.4% increase driven by demand for protective coatings and specialty OEM flooring systems. Organic growth of 6.7%, complemented by 2.5% acquisition-driven expansion, highlights RPM’s effective growth strategy. Its MAP 2025 program continues to enhance profitability, delivering record adjusted EBIT despite temporary inefficiencies from plant consolidations. The Stonhard brand leads the seamless flooring segment with a vertically integrated manufacture-to-installation model, reducing reliance on third-party contractors and ensuring quality control. This approach strengthens RPM’s position in high-performance buildings and industrial infrastructure projects.

Nippon Paint expands Asia-Pacific dominance with localized manufacturing and antimicrobial innovation

Nippon Paint Holdings is leveraging regional expansion and product innovation to capture significant share in the floor coatings market. The company achieved 6% revenue growth in 2026 by expanding operations in China and India, increasing production capacity by 12% to meet infrastructure demand. Its integration of the DuluxGroup acquisition has secured a dominant share in the Oceania high-performance floor coatings segment. Nippon Paint is prioritizing antiviral and antimicrobial flooring solutions, in healthcare and food-processing industries. The company’s “Local-for-Local” strategy ensures over 90% of floor resin sourcing is regionally aligned with manufacturing hubs, mitigating supply chain risks. This localized, innovation-driven model strengthens its competitive positioning across fast-growing emerging markets.

Germany Floor Coatings Market: Driving Europe’s Low-VOC, High-Performance Industrial Flooring Evolution

Germany continues to dominate the European floor coatings market, acting as a regulatory and technological benchmark for sustainable and high-performance coatings. The country’s strong alignment with the EU Green Deal has accelerated the shift toward low-VOC floor coatings, solvent-free epoxy systems, and eco-friendly polyurethane solutions, making Germany a critical innovation hub.

A major breakthrough in the German market is the development of fast-cure polyaspartic floor coatings, which can achieve full mechanical load capacity within just two hours. These coatings are particularly optimized for high-traffic logistics hubs and industrial warehouses, significantly reducing downtime. Additionally, Germany is advancing bio-based epoxy resins, incorporating up to 45% renewable biomass while maintaining industrial-grade durability, such as high Shore D hardness.

Regulatory frameworks such as the AgBB 2025 updates are reshaping the market by enforcing strict emission limits for cleanroom coatings, particularly in pharmaceutical manufacturing. This has led to increased adoption of low-emission, antimicrobial polyurethane (PU) floor coatings in industries like food processing, where HACCP compliance is mandatory. Furthermore, investments in renewable energy infrastructure, especially wind turbine manufacturing, are driving demand for anti-static and non-slip industrial floor coatings.

United States Floor Coatings Market: Smart Warehousing and Next-Gen Industrial Flooring Systems

The U.S. floor coatings market is undergoing a transformation driven by e-commerce expansion, manufacturing reshoring, and infrastructure modernization. The surge in automated warehouses and logistics centers has significantly increased demand for high-build epoxy floor coatings and durable acrylic coatings.

A defining trend in the U.S. is the rapid adoption of smart floor coatings integrated with RFID and conductive sensors, enabling seamless navigation for automated guided vehicles (AGVs) in data centers and fulfillment hubs. These intelligent coatings are redefining operational efficiency in industrial flooring applications.

Government initiatives, including the Infrastructure Investment and Jobs Act, are fueling large-scale demand for industrial-grade coatings in transport infrastructure, such as bridge decks and transit systems. Simultaneously, environmental regulations under the EPA’s TSCA Section 6 are accelerating the transition toward NMP-free polyurethane coatings, promoting safer and eco-friendly solutions in residential and commercial flooring.

Innovation is also evident in the commercialization of ultra-thin UV-curable floor coatings, which reduce application downtime by up to 80%, making them ideal for retail showrooms. Additionally, the rise of lithium-ion battery gigafactories has created strong demand for chemical-resistant floor coatings, capable of withstanding harsh electrolyte exposure. Increasing compliance with SCAQMD Rule 1113 further ensures the adoption of low-emission coatings across the country.

China Floor Coatings Market: Transition to Waterborne Epoxy and Anti-Corrosive Systems

China leads the global floor coatings industry in volume, with a strategic shift toward high-performance waterborne epoxy coatings driven by stringent environmental regulations. Policies such as GB/T 35602-2017 Green Product Assessment have effectively restricted high-solvent coatings in urban construction, accelerating the adoption of sustainable alternatives.

Large-scale infrastructure projects, including free trade zones and urban developments, have boosted demand for high-solids polyurethane floor systems, particularly in commercial and industrial applications. China is also pioneering self-cleaning photocatalytic coatings, widely used in hospitals and airports to actively neutralize airborne pollutants and enhance indoor air quality.

The country’s manufacturing evolution is evident in the Pearl River Delta, where demand for electrostatic dissipative (ESD) floor coatings is surging due to the growth of semiconductor and electronics assembly industries. Domestic companies are investing heavily in R&D, focusing on moisture-tolerant epoxy primers designed for humid climates.

In addition, China’s booming retail sector in cities like Shanghai and Shenzhen is driving demand for decorative 3D epoxy flooring, blending aesthetics with durability in luxury commercial spaces.

India Floor Coatings Market: Infrastructure Boom and Industrial Coating Innovation

India is emerging as the fastest-growing floor coatings market in Asia-Pacific, supported by rapid urbanization and government-led initiatives such as Atmanirbhar Bharat and the National Infrastructure Pipeline (NIP). The development of smart cities, airports, and industrial corridors is significantly boosting demand for heavy-duty concrete floor coatings and industrial sealers.

Local manufacturers are innovating with hybrid polyurea-polyurethane coatings, combining flexibility with chemical resistance to withstand India’s extreme temperature variations. This innovation is particularly beneficial for industrial warehouses, automotive plants, and logistics centers.

Major industry players like Asian Paints and Kansai Nerolac are expanding their production capabilities through automated manufacturing units dedicated to industrial floor coatings and protective coatings. At the same time, increased foreign direct investment (FDI) in electronics manufacturing is driving demand for ESD-safe resinous flooring systems.

Key industries such as pharmaceuticals and textiles are adopting high-gloss, dust-proof epoxy floor coatings to meet stringent export standards. Additionally, the Bureau of Indian Standards (BIS) is working on new regulations for slip-resistant floor coatings, enhancing safety in public infrastructure projects.

South Korea Floor Coatings Market: Smart Factory Integration and Nanotechnology Advancements

South Korea stands out in the advanced floor coatings market due to its leadership in precision engineering, electronics manufacturing, and smart factory systems. The integration of nanotechnology-enhanced coatings has significantly improved surface durability, offering scratch resistance and hardness levels exceeding 9H, ideal for cleanroom environments.

The country is also pioneering AI-integrated smart factory flooring, with color-coded and zoning-specific coatings designed to work seamlessly with machine vision systems in automated “lights-out” manufacturing facilities. This trend is transforming industrial floor design and operational efficiency.

Significant investments by companies like LG Chem and Samsung SDI in energy storage systems are driving demand for fire-retardant floor coatings, ensuring safety in high-risk industrial environments. Additionally, South Korea is promoting sustainability through incentives for carbon-negative floor coatings derived from captured CO₂ emissions.

Innovations such as low-odor, solvent-free MMA coatings allow for rapid overnight renovations in retail and healthcare settings, while specialized coatings for automotive test tracks provide thermal stability and simulate real-world driving conditions for EV testing.

Japan Floor Coatings Market: Bio-Based Innovation and Long-Life Industrial Flooring Solutions

Japan’s floor coatings industry is characterized by a strong focus on durability, lifecycle cost optimization, and sustainability. The country is at the forefront of bio-based floor coating innovations, including lignin-derived coatings, which offer high UV stability and mechanical strength while aligning with long-term environmental goals.

Technological advancements include the development of silicate floor hardeners that penetrate concrete deeply, creating a permanent crystalline barrier against oil and chemical ingress. These solutions are widely used in industrial facilities and logistics hubs where durability is critical.

Infrastructure initiatives under the “Resilient Japan” program have increased demand for seismic-resistant flexible floor coatings, ensuring structural safety in critical facilities. Regulatory updates to JIS K 5970 standards have further tightened emission limits, promoting the adoption of low-formaldehyde and low-TVOC coatings.

Strategic collaborations, such as partnerships between Toray Industries and Sika Japan, are advancing carbon fiber-reinforced floor overlays for high-load applications like bridges and ramps. Additionally, Japan leads in specialized solutions such as cold-storage floor coatings, capable of curing at temperatures as low as -25°C, catering to the growing food logistics sector.

Floor Coatings Market Report Scope

Floor Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.9 Billion

|

|

Market Size (2032)

|

$8.4 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Technology (Water-borne, Solvent-borne, 100% Solids, UV-Curable, Powder Coatings), By Component Type (One-Component, Two-Component, Three-Component), By Flooring Material (Concrete, Wood, Mortar, Terrazzo, Others), By Application Method (Self-Leveling, Thin-Film, High-Build, Broadcast), By End-Use Sector (Industrial, Commercial, Residential), By Functional Characteristic (Anti-Corrosion and Chemical Resistant, Anti-static, Anti-microbial, Anti-slip, Thermal Shock Resistant, Decorative)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., RPM International Inc., Sika AG, BASF SE, Jotun A/S, Asian Paints Limited, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., MAPEI S.p.A., Hempel A/S, Axalta Coating Systems Ltd., Tennant Coatings, Behr Process Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Floor Coatings Market Segmentation

By Technology

- Water-borne

- Solvent-borne

- 100% Solids

- UV-Curable

- Powder Coatings

By Component Type

- One-Component

- Two-Component

- Three-Component

By Flooring Material

- Concrete

- Wood

- Mortar

- Terrazzo

- Others

By Application Method

- Self-Leveling

- Thin-Film

- High-Build

- Broadcast

By End-Use Sector

- Industrial

- Commercial

- Residential

By Functional Characteristic

- Anti-Corrosion and Chemical Resistant

- Anti-static

- Anti-microbial

- Anti-slip

- Thermal Shock Resistant

- Decorative

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Floor Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- RPM International Inc.

- Sika AG

- BASF SE

- Jotun A/S

- Asian Paints Limited

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- MAPEI S.p.A.

- Hempel A/S

- Axalta Coating Systems Ltd.

- Tennant Coatings

- Behr Process Corporation

*- List not Exhaustive