Fluorocarbon Coatings Market Growth Driven by Architectural Durability, Renewable Energy Applications, and High-Performance Fluoropolymer Systems

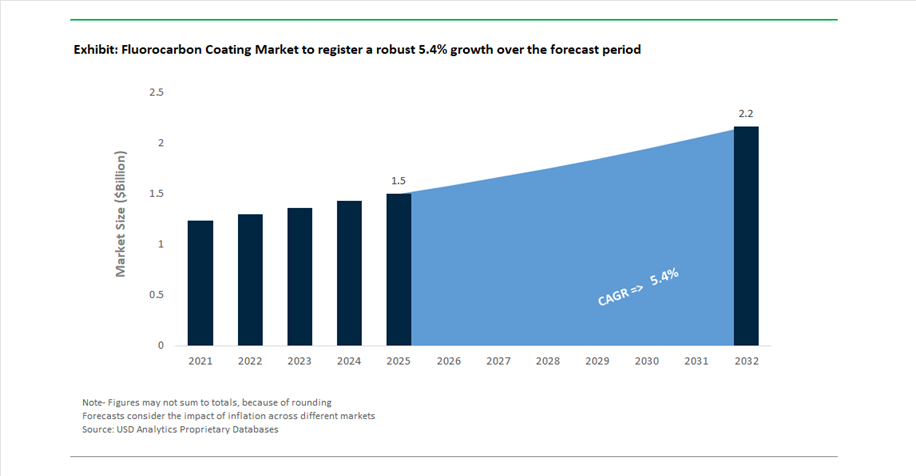

The global Fluorocarbon Coatings Market was valued at USD 1.5 billion in 2025 and is projected to grow at a CAGR of 5.4% between 2025 and 2032, reaching USD 2.2 billion by 2032. This growth is underpinned by increasing demand for ultra-durable, weather-resistant coatings across architectural, aerospace, automotive, and renewable energy applications.

Fluorocarbon coatings—primarily based on PVDF and FEVE chemistries—are widely recognized for their exceptional UV resistance, corrosion protection, color retention, and long service life, often exceeding 20–30 years. A key structural driver is the rising adoption of high-performance facade coatings in commercial real estate and infrastructure projects, where long-term durability and reduced maintenance costs are critical. These coatings are increasingly specified for high-rise buildings, curtain walls, and metal roofing systems, particularly in regions exposed to harsh environmental conditions.

Another major growth catalyst is the expansion of renewable energy infrastructure, especially solar power. Fluorocarbon coatings are used in solar panel backsheets and frames to enhance UV stability and maintain efficiency over extended lifecycles. Additionally, the growth of aerospace and automotive sectors is driving demand for coatings that can withstand extreme temperatures, chemical exposure, and mechanical stress.

Sustainability is also shaping market evolution. The development of solar-reflective, low-energy curing, and long-life coatings is enabling compliance with green building standards such as LEED. Furthermore, regulatory approvals for specialized fluorocarbon applications in refrigeration and energy systems are expanding the addressable market.

Laser-Curing Breakthroughs, and Renewable Energy Integration Reshape Market Dynamics

The fluorocarbon coatings market is undergoing significant transformation driven by industry consolidation, advanced curing technologies, and expansion into high-growth applications. In November 2025, AkzoNobel and Axalta Coating Systems announced a $25 billion all-stock merger, creating the world’s largest platform for fluorocarbon coatings. The combined entity integrates architectural powder coatings and mobility fluoropolymer technologies, supported by a substantial R&D budget aimed at accelerating next-generation weather-resistant solutions.

Technological innovation in curing processes is reshaping production efficiency. In March 2026, PPG Industries partnered with IPG Photonics to commercialize laser-cured powder coatings, significantly impacting fluorocarbon systems such as FEVE and PVDF. This technology enables near-instantaneous curing and reduces energy consumption by up to 90%, making it particularly valuable for heat-sensitive substrates and high-throughput manufacturing lines.

Expansion into renewable energy applications is accelerating demand. In January 2024, DuPont launched Foralutex Xynergy, a fluorocarbon coating designed for solar panel components, enhancing UV resistance and ensuring performance over 25+ year lifecycles. This aligns with the global push for durable and efficient renewable energy infrastructure.

Regional expansion strategies are strengthening market penetration. In March 2026, Daikin Industries established a new fluorochemical sales unit in India, targeting high-growth sectors such as electronics, semiconductors, and battery manufacturing. Additionally, in January 2026, AkzoNobel announced the opening of a Dubai aerospace coatings hub, improving supply chain efficiency for high-performance fluorocarbon coatings in harsh desert environments.

Sustainability and regulatory developments are also influencing adoption. In October 2024, Sherwin-Williams showcased its Fluropon® solar-reflective coatings, enabling compliance with cool-roof and LEED standards. Furthermore, in February 2025, the European Commission approved the use of fluorocarbon nanocoatings in refrigeration systems, supporting energy efficiency improvements across the cold-chain logistics sector.

Industrial investment and supply chain development continue to expand capacity. In January 2024, AGC Inc. initiated construction of a new fluoropolymer production facility to support applications in green hydrogen production, while PPG Industries expanded its architectural fluorocarbon coating portfolio to target high-end commercial construction projects.

Commercial agreements are further strengthening market positioning. In January 2026, PPG Industries became the exclusive supplier for Quality Collision Group, consolidating the use of fluorocarbon-based automotive refinish coatings across its network.

Transition from Liquid PVDF to Powder-Based Fluorocarbon Coatings for Low-Emission Architectural Applications

The fluorocarbon coating industry is undergoing a fundamental shift as regulatory pressure on volatile organic compound emissions accelerates the transition from traditional liquid PVDF coatings to powder-based formulations. Conventional liquid PVDF systems rely heavily on solvent carriers such as N-Methyl-2-pyrrolidone, which are increasingly restricted under global environmental regulations. In response, PVDF powder coatings are emerging as a preferred alternative due to their near-zero VOC profile, aligning with sustainability frameworks such as LEED v4.1 and green building certifications. Powder coating systems offer substantial operational advantages, including material utilization rates of up to 98% through overspray recovery, compared to 50% to 70% efficiency in liquid systems where significant losses occur during application. This improvement directly reduces raw material waste and production costs. Additionally, PVDF powder coatings provide enhanced coating thickness integrity, with single-coat applications achieving film builds of 60 to 80 microns, delivering superior edge coverage and improved resistance to environmental stressors such as coastal salt exposure. From an energy perspective, the elimination of solvent flash-off zones and hazardous waste processing contributes to a 15% to 20% reduction in overall energy consumption per unit of coated substrate. These combined environmental and performance benefits are positioning PVDF powder coatings as the next-generation standard for architectural aluminum and facade applications in global construction markets.

Multi-Layer Ceramic-Reinforced PTFE Coatings Enhancing Durability in Consumer and Industrial Applications

The development of multi-layer fluorocarbon coating systems incorporating ceramic reinforcements is redefining durability standards in both consumer and industrial applications. Traditional PTFE coatings, while offering excellent non-stick properties, have historically faced limitations in abrasion resistance and mechanical durability. The integration of ceramic primers or intermediate layers addresses these challenges by providing a robust mechanical anchor for the fluorocarbon topcoat. Performance benchmarks from 2025 indicate that ceramic-reinforced PTFE systems deliver five to ten times greater scratch resistance compared to conventional two-layer coatings under standardized testing conditions. These hybrid systems also exhibit significantly enhanced surface hardness, with the ability to withstand over 50,000 cycles of metal utensil abrasion, making them suitable for high-use environments such as cookware and industrial processing equipment. Thermal performance is also improved, with ceramic components enhancing heat distribution by approximately 12%, reducing localized hot spots that can lead to coating degradation. Importantly, these advanced systems are being formulated to meet global food safety standards by eliminating PFOA and PFOS substances, ensuring compliance with evolving regulatory frameworks. The combination of durability, thermal efficiency, and regulatory compliance is driving the adoption of ceramic-fluorocarbon hybrid coatings across a wide range of applications.

China PFAS Regulatory Framework Creating Demand for Low-Toxic Fluorocarbon Coating Solutions

China’s Ministry of Ecology and Environment is significantly tightening control over fluorinated substances through its New Pollutants Management Action Plan, creating both compliance challenges and strategic opportunities for fluorocarbon coating manufacturers. The regulatory framework requires comprehensive inventory reporting for PFAS substances exceeding annual usage thresholds of 100 kilograms, compelling manufacturers to adopt advanced compliance tracking and reporting systems. This shift is driving demand for low-toxicity and non-toxic fluorocarbon resins that can meet regulatory approval while maintaining high-performance characteristics. Manufacturers that achieve certification under these frameworks are gaining a competitive advantage, with data indicating approximately 20% higher success rates in securing government and infrastructure contracts. Additionally, the Chinese government is actively incentivizing the development of short-chain fluorocarbon alternatives through targeted R&D tax credits, encouraging innovation in safer, next-generation coating chemistries. These regulatory dynamics are reshaping the competitive landscape, favoring companies that can deliver compliant, high-performance fluorocarbon coatings aligned with environmental and safety standards.

US Hydropower Infrastructure Investments Driving Adoption of ETFE Fluorocarbon Coatings

The modernization of hydropower infrastructure in the United States is creating a significant growth opportunity for ETFE-based fluorocarbon coatings, particularly in applications requiring long-term corrosion resistance and hydraulic efficiency. The U.S. Bureau of Reclamation is increasingly specifying ETFE coatings for critical components such as penstocks and trash racks due to their exceptional resistance to abrasion, corrosion, and bio-fouling. ETFE-coated surfaces are being engineered to deliver service lifespans of up to 50 years, significantly outperforming traditional coating systems that require periodic maintenance every 10 to 15 years. In addition to durability, ETFE coatings provide functional performance benefits by reducing friction at the interface between water and pipe surfaces, improving hydraulic efficiency by approximately 2% to 3%. This efficiency gain translates directly into increased power generation output over the lifecycle of hydropower facilities. Bio-fouling resistance is another critical advantage, with ETFE coatings demonstrating up to 90% reduction in the accumulation of organisms such as algae and zebra mussels, minimizing maintenance requirements and operational disruptions. With over 500 million dollars allocated to hydropower efficiency and safety upgrades in the 2025 to 2026 funding cycle, demand for high-performance fluorocarbon coatings is expected to increase significantly, positioning ETFE as a key material solution in renewable energy infrastructure.

Fluorocarbon Coating Market Share 2025: Metal Substrates and Project-Based Contracting Lead Growth

Substrate Insights: Metal Dominance Driven by PVDF-Coated Architectural Applications

The metal substrate segment leads the fluorocarbon coating market with a substantial 62% market share in 2025, fueled by its extensive use in architectural aluminum applications. Fluorocarbon coatings, particularly PVDF (polyvinylidene fluoride) coatings, are widely specified for curtain walls, roofing systems, window frames, and façade panels in high-rise buildings, airports, and stadiums due to their exceptional 30+ year weatherability, UV resistance, and chalk resistance. A major growth driver is the adoption of coil coating technology, where metal sheets are pre-coated in continuous processes to achieve uniform thickness, enhanced durability, and lower VOC emissions compared to field-applied coatings. This method also accelerates installation timelines and ensures consistent quality across large construction projects. As global urbanization and demand for long-lasting, low-maintenance exterior coatings increase, metal-based fluorocarbon coatings will continue to dominate the market landscape.

Distribution Channel Insights: Project-Based Contracting Drives Large-Scale Coating Applications

The project-based contracting segment accounts for the largest 48% share in the fluorocarbon coating market in 2025, reflecting the project-centric nature of large infrastructure and construction applications. Fluorocarbon coatings are primarily applied through contract-based projects such as bridges, stadium domes, commercial complexes, and high-rise façades, where customized coating solutions are specified and executed on-site or through factory-applied coil systems. This approach allows architects, engineers, and project owners to maintain strict specification control, including selection of FEVE vs. PVDF coatings, gloss levels, and custom color requirements, often backed by long-term performance warranties. Unlike distributor-led sales, project-based contracting ensures precise application standards and compliance with architectural design intent. As mega construction projects and infrastructure investments continue to rise globally, project-based contracting will remain a key channel driving growth in the fluorocarbon coatings market.

Fluorocarbon Coating Market Competitive Landscape: Sustainable Chemistry, Infrastructure Demand, and High-Performance Applications Shaping Competition

The fluorocarbon coating market is highly competitive, driven by sustainability mandates, infrastructure expansion, and innovation in high-durability fluoropolymer technologies. Leading companies are prioritizing PFAS-free formulations, advanced architectural coatings, and high-performance applications across automotive, aerospace, and semiconductor industries.

PPG drives sustainable fluorocarbon innovation and automotive color leadership in global markets

PPG Industries is reinforcing its leadership in the fluorocarbon coatings market through innovation, sustainability, and automotive OEM collaborations. In February 2026, the company launched its “Parallels” automotive color theme featuring Secret Safari, a fluorocarbon-based coating delivering a chameleon-like finish for premium vehicles. With $15.9 billion in 2025 net sales, PPG is intensifying its focus on China through partnerships with Xiaomi and BYD to introduce 100 new colors over three years. Following the $2 billion divestiture of its architectural retail business, the company has redirected fluorocarbon R&D toward high-margin industrial OEM and aerospace coatings. 44% of its 2026 revenue comes from sustainably advantaged products, including low-VOC fluoropolymer topcoats. This positions PPG at the forefront of clean chemistry and next-generation fluorocarbon coatings innovation.

AkzoNobel optimizes portfolio and advances low-carbon fluorocarbon coating ecosystems

AkzoNobel is sharpening its competitive edge in the fluorocarbon coatings market through portfolio optimization and sustainability-driven partnerships. In April 2026, the company agreed to divest its Pakistan unit for €50 million, continuing its strategy of exiting non-core markets following its India exit in 2025. It has formed a “Sustainability Trio” with Arkema and BASF to develop bio-based fluorocarbon powder coatings with reduced carbon footprints. AkzoNobel’s solar-absorbing wall technology integrates fluorocarbon binders capable of maintaining over 95% efficiency across a 30-year lifecycle in urban environments. The company reported a 14.2% adjusted EBITDA margin in early 2026, supported by its value-over-volume approach in marine and protective coatings. This strategic alignment enhances its leadership in sustainable architectural and industrial fluoropolymer coatings.

Sherwin-Williams captures infrastructure demand with next-generation fluorocarbon durability solutions

The Sherwin-Williams Company is capitalizing on the infrastructure boom to strengthen its fluorocarbon coatings market position. The company issued 2026 EPS guidance of $11.50 to $11.90, supported by strong growth in its Coil & Extrusion segment for architectural fluorocarbon coatings. Its Fluorokem™ and FIRETEX® product lines have been upgraded with next-generation fluorinated chemistries delivering superior bond strength and up to 50-year durability compared to conventional systems. Sherwin-Williams is also expanding its DesignHouse services with AI-driven color matching, reducing project lead times by 20% for large-scale facade applications. With a network of over 5,000 stores, the company offers unmatched technical support and just-in-time delivery capabilities. This integrated approach strengthens its dominance in large infrastructure and commercial construction projects.

Daikin advances semiconductor and PFAS-free fluorocarbon technologies for next-gen electronics

Daikin Industries is driving growth in the fluorocarbon coatings market through semiconductor-focused innovation and regulatory-aligned material development. In 2026, the company showcased high-purity FEP and PTFE coatings at SEMICON Korea and Southeast Asia, targeting sub-10 nm fabrication environments. Its February 2026 innovations include PTFE anti-dripping additives and advanced electrolyte design for lithium-ion batteries, enhancing flame retardancy through fluorocarbon fibrillation. Daikin is transitioning toward hydrocarbon-based polymer processing aids to develop PFAS-free alternatives while maintaining productivity. Its Neoflon™ FEP coating powder is widely recognized for corrosion-resistant applications in chemical processing, offering pinhole-free coatings at ultra-thin thicknesses. This positions Daikin as a leader in high-performance and next-generation electronics coatings.

Arkema accelerates circular economy leadership with advanced fluorocarbon material innovations

Arkema S.A. is strengthening its position in the fluorocarbon coatings market through advanced material innovation and circular economy initiatives. At JEC World 2026, the company introduced Zenimid™ polyimide films and expanded Kynar® PVDF applications for aerospace and hydrogen storage, focusing on thermally stable fluorocarbon resins. Its collaboration with Composite Recycling and Veolia is enabling commercialization of Elium®, the first recyclable thermoplastic liquid resin used in hybrid fluorocarbon composite structures. Arkema has achieved breakthroughs in boat hull recycling using Elium®, reinforcing its leadership in sustainable high-performance materials. Additionally, its 100% bio-based Rilsan® Polyamide 11 is being integrated with fluorocarbon coatings to establish a “Green Safety” benchmark in automotive thermal management. This strategy enhances Arkema’s role in sustainable fluoropolymer ecosystems.

Beckers strengthens coil coating leadership with renewable chemistry and Asia-Pacific expansion

Beckers Group is consolidating its leadership in fluorocarbon coil coatings through innovation, sustainability, and regional expansion. The company opened a state-of-the-art R&D center in Shanghai, reinforcing its position as the global leader in coil coatings and targeting Asia-Pacific industrial growth. Its collaboration with Anodyne Chemistries aims to develop renewable chemical alternatives to petroleum-based fluorocarbon precursors, advancing sustainable industrial coatings. Beckers operates across 23 locations in 17 countries, specializing in high-performance coatings for metal building applications such as roofing and cladding. The company received SBTi net-zero approval in late 2025 and is targeting a 15% reduction in carbon intensity across its fluoropolymer portfolio by 2026 through renewable energy adoption. This positions Beckers as a sustainability-driven leader in architectural fluorocarbon coatings.

United States Fluorocarbon Coating Market: Semiconductor Reshoring and Aerospace-Grade Performance Coatings

The United States fluorocarbon coating market is undergoing a significant transformation, fueled by the rapid reshoring of semiconductor manufacturing, renewable energy infrastructure, and aerospace innovation. The implementation of the CHIPS and Science Act has unlocked over $150 billion in private investments, driving substantial demand for high-performance fluorocarbon coatings, particularly FEVE coatings used in cleanroom structural steel and chemical handling systems.

Product innovation remains a key growth pillar, with companies like Alfa Chemistry expanding advanced fluoropolymer portfolios to meet the high-temperature stability requirements of AI-driven data center cooling systems. Strategic collaborations, such as the partnership between 3M and H.B. Fuller, are further enhancing the adoption of self-cleaning, anti-fouling fluorocarbon coatings for coastal and industrial infrastructure.

Regulatory developments are reshaping the competitive landscape, especially following DuPont’s 2025 PFAS-related settlement, which is accelerating the shift toward PFAS-free fluorocarbon dispersions and low-emission coatings. In aerospace, the adoption of FEP-based coatings for liquid hydrogen systems highlights the increasing importance of fluoropolymers capable of operating under extreme cryogenic conditions. Additionally, the expansion of utility-scale solar projects is boosting demand for UV-resistant fluorocarbon coatings, improving the efficiency and durability of solar module backsheets.

China Fluorocarbon Coating Market: Water-Based Technologies and Smart Infrastructure Expansion

China continues to dominate the global fluorocarbon coatings market share, transitioning toward waterborne, eco-friendly coating technologies to comply with stringent environmental regulations. The Ministry of Ecology and Environment’s 2025 VOC standards have mandated a large-scale shift from solvent-based PVDF coatings to water-based FEVE fluorocarbon formulations, especially in architectural applications.

Massive investments in smart city infrastructure, particularly in the Pearl River Delta, are driving demand for nanotechnology-enhanced fluorocarbon coatings capable of delivering long-term durability and up to 25-year gloss retention on high-rise curtain walls. Additionally, the growth of the offshore wind energy sector has increased the adoption of anti-corrosive fluorocarbon coatings for turbine towers operating in harsh marine environments.

Technological advancements include the development of hydrophilic self-cleaning fluorocarbon resins, which are increasingly used in logistics hubs and industrial facilities. Furthermore, China’s strategic export quota adjustments on fluorspar-derived materials are strengthening domestic consumption, particularly in EV battery production and semiconductor-grade PVDF applications. The rollout of 6G infrastructure is also boosting demand for low-dielectric fluorocarbon coatings, ensuring minimal signal interference in densely populated urban regions.

India Fluorocarbon Coating Market: Infrastructure Expansion and “Make in India” Manufacturing Growth

India is emerging as a high-growth region in the global fluorocarbon coatings market, driven by rapid urbanization, infrastructure modernization, and government-backed initiatives like “Make in India” and PMAY-U 2.0. The approval of over 235,000 housing units in 2025 has significantly increased the consumption of fluorocarbon-based architectural coatings, particularly for exterior durability and weather resistance.

The country’s railway modernization projects, including the expansion of the Vande Bharat high-speed train network, have standardized the use of FEVE-based fluorocarbon coatings to ensure long-term resistance to UV radiation and harsh climatic conditions. Investments in Petroleum, Chemicals & Petrochemicals Investment Regions (PCPIRs) are further driving demand for specialty fluoropolymer coatings across industrial applications.

Product innovation is also gaining traction, with major consumer brands launching appliances featuring fluorocarbon conformal coatings on PCBs to enhance durability in coastal environments. Additionally, India’s expanding metro networks across 29 cities have widely adopted PVDF coatings for station infrastructure due to their corrosion resistance and aesthetic longevity.

Regulatory support through updated Eco-mark certification standards is encouraging the production of low-VOC fluorocarbon powder coatings, offering tax incentives and accelerating the transition toward environmentally sustainable coating solutions.

Japan Fluorocarbon Coating Market: Bio-Based Innovation and High-Purity Semiconductor Applications

Japan’s fluorocarbon coating market is defined by its focus on precision engineering, sustainability, and high-purity industrial applications. The country is leading innovation in bio-derived FEVE resins, targeting significant reductions in carbon footprint for architectural and industrial coatings by 2026.

Japan remains a global leader in high-purity FEP coatings used in semiconductor manufacturing, particularly for advanced nodes below 3nm, where contamination control is critical. Regulatory updates to JIS K 5970 standards have introduced stricter requirements for weather resistance, especially in marine and coastal environments, ensuring long-term coating performance.

Urban development initiatives in Tokyo are integrating photocatalytic fluorocarbon coatings, which actively reduce air pollutants such as NOx on building facades, aligning with sustainability goals. Additionally, innovations such as cool-roof fluorocarbon coatings with high Solar Reflectance Index (SRI) are improving building energy efficiency by reducing cooling loads during peak summer months.

A key application area is the expansion of FEP-coated optical fibers in medical devices, where the coating’s low refractive index enhances signal clarity in advanced diagnostic equipment.

South Korea Fluorocarbon Coating Market: EV Battery Safety and Marine Coating Innovations

South Korea is leveraging fluorocarbon coating technologies to strengthen its leadership in electric vehicle (EV) batteries, marine engineering, and advanced manufacturing. The development of low-friction fluorocarbon-silicone hybrid coatings for LNG carrier hulls has improved fuel efficiency by approximately 5%, highlighting the role of advanced coatings in maritime sustainability.

The country’s EV ecosystem is rapidly adopting PVDF-based fluorocarbon coatings in high-nickel cathode materials, enhancing thermal stability and extending battery life. Investments by industry leaders such as LG Chem and Samsung SDI are accelerating innovation in battery-grade fluoropolymer coatings, supporting next-generation energy storage technologies.

The Smart Factory initiative is driving the adoption of ESD fluorocarbon floor coatings in semiconductor manufacturing facilities, improving operational safety and efficiency. Technological advancements include the commercialization of multi-layer hydrophobic fluorocarbon coatings, which are gaining traction in industrial applications due to their superior moisture resistance.

Government incentives are promoting the shift toward solvent-free fluorocarbon powder coatings, aligning with South Korea’s net-zero goals. Additionally, the consumer electronics sector is increasingly integrating oleophobic fluorocarbon coatings in foldable smartphones, ensuring durability and protection against dust and wear.

Brazil Fluorocarbon Coating Market: Aerospace Expansion and Renewable Energy Applications

Brazil is emerging as a strategic growth market in the Latin American fluorocarbon coatings industry, driven by advancements in aerospace manufacturing, renewable energy, and green mobility initiatives. Investments by Embraer, including a $3.5 billion commitment toward sustainable aircraft development, are boosting demand for high-performance fluorocarbon aerospace coatings.

Government initiatives such as the Nova Indústria Brasil (NIB) program are encouraging the adoption of anti-corrosive fluorocarbon coatings in hybrid and electric vehicles, particularly for lightweight aluminum structures. The country’s renewable energy sector is also expanding, with offshore wind projects driving demand for fluorocarbon-coated turbine components capable of withstanding high-salinity marine environments.

Industrial modernization efforts are strengthening Brazil’s position as a regional leader, with solvent-borne fluorocarbon coatings still widely used in mining equipment and heavy industrial machinery. Global players like AkzoNobel and PPG are expanding their presence through localized blending centers, enabling just-in-time customization for architectural projects.

A key application area is the growing use of fluorocarbon-lined storage tanks in the ethanol and biofuel industries, ensuring chemical resistance and maintaining product purity in demanding processing environments.

Fluorocarbon Coating Market Report Scope

Fluorocarbon Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2032)

|

$2.2 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Resin Type (Polyvinylidene Fluoride, Fluoroethylene Vinyl Ether, Polytetrafluoroethylene, Fluorinated Ethylene Propylene, Ethylene Tetrafluoroethylene, Others), By Technology (Liquid Coatings, Powder Coatings, Film Coatings), By Substrate (Metal, Concrete and Masonry, Plastics and Composites, Glass), By Application Environment (Outdoor, Indoor, Marine), By End-Use Sector (Building and Construction, Chemical Processing, Electrical and Electronics, Automotive and Transportation, Food and Beverage, Energy and Power, Healthcare), By Functional Performance (Weather and UV Resistance, Corrosion and Chemical Resistance, Anti-Fouling, Non-Stick, Thermal Stability), By Distribution Channel (Direct Sales, Specialty Distributors and Wholesalers, Project-based Contracting)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Daikin Industries, Ltd., AGC Inc., Arkema S.A., Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Jotun A/S, Kansai Paint Co., Ltd., Beckers Group, KCC Corporation, Tnemec Company, Inc., Solvay S.A., Shanghai Sinyang Semiconductor Materials Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fluorocarbon Coating Market Segmentation

By Resin Type

- Polyvinylidene Fluoride

- Fluoroethylene Vinyl Ether

- Polytetrafluoroethylene

- Fluorinated Ethylene Propylene

- Ethylene Tetrafluoroethylene

- Others

By Technology

- Liquid Coatings

- Powder Coatings

- Film Coatings

By Substrate

- Metal

- Concrete and Masonry

- Plastics and Composites

- Glass

By Application Environment

By End-Use Sector

- Building and Construction

- Chemical Processing

- Electrical and Electronics

- Automotive and Transportation

- Food and Beverage

- Energy and Power

- Healthcare

By Functional Performance

- Weather and UV Resistance

- Corrosion and Chemical Resistance

- Anti-Fouling

- Non-Stick

- Thermal Stability

By Distribution Channel

- Direct Sales

- Specialty Distributors and Wholesalers

- Project-based Contracting

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Fluorocarbon Coating Market

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- Daikin Industries, Ltd.

- AGC Inc.

- Arkema S.A.

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Jotun A/S

- Kansai Paint Co., Ltd.

- Beckers Group

- KCC Corporation

- Tnemec Company, Inc.

- Solvay S.A.

- Shanghai Sinyang Semiconductor Materials Co., Ltd.

*- List not Exhaustive