Fluoropolymer Coating Additives Market Growth Driven by PFAS-Free Transition, EV Applications, and High-Performance Surface Engineering

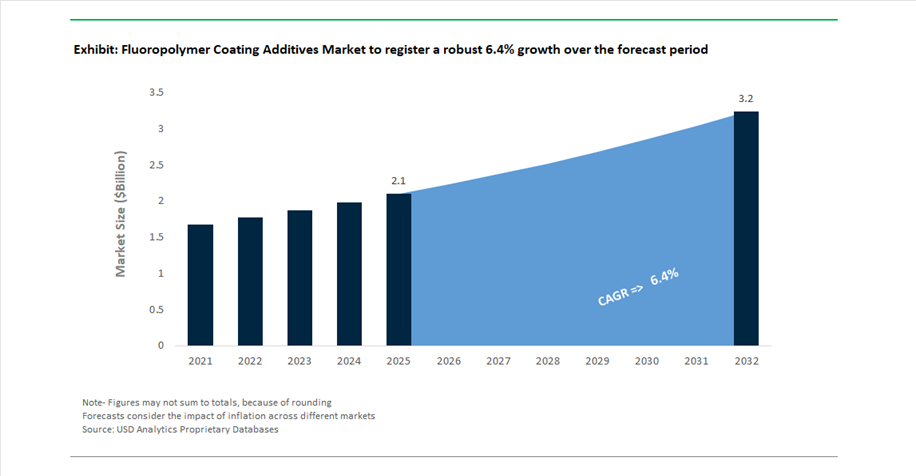

The global Fluoropolymer Coating Additives Market was valued at USD 2.1 billion in 2025 and is projected to grow at a CAGR of 6.4% between 2025 and 2032, reaching USD 3.2 billion by 2032. This above-average growth reflects the increasing demand for advanced surface modifiers, defoamers, wetting agents, and tribological additives used to enhance the performance of high-end coatings across automotive, electronics, aerospace, and industrial sectors.

Fluoropolymer additives play a critical role in imparting low surface energy, chemical resistance, anti-fouling behavior, and slip properties to coatings. A major structural driver is the expansion of electric vehicles (EVs), semiconductors, and hydrogen systems, where coatings must withstand extreme thermal, chemical, and electrical stress conditions. These applications require highly specialized additive systems that ensure coating integrity, durability, and performance consistency at micro and nano scales.

A defining trend reshaping the market is the global transition away from PFAS-containing chemistries, driven by regulatory pressure in Europe and North America. Manufacturers are rapidly developing PFAS-free, silicone-based, and bio-circular alternatives that replicate the performance of traditional fluorinated additives while meeting compliance standards. This shift is not only regulatory-driven but also aligned with corporate sustainability goals focused on reducing environmental impact and carbon footprint.

PFAS-Free Portfolio Transformation, Bio-Circular Additives, and EV-Driven Innovation Reshape Market Dynamics

The fluoropolymer coating additives market is undergoing a structural transformation driven by regulatory shifts, sustainability innovation, and advanced application requirements. In November 2024, Clariant completed its transition to a fully PFAS-free additive portfolio, introducing products such as Ceridust® 8170 M that deliver comparable performance to PTFE-based additives while ensuring regulatory compliance and reduced environmental impact.

Similarly, in August 2024, BYK-Chemie announced its plan to eliminate all PFAS-containing additives by the end of 2025, replacing them with silicone-based and bio-based alternatives. This move signals a permanent industry shift toward non-fluorinated chemistries in key applications such as automotive and architectural coatings.

Sustainability-driven innovation is accelerating through bio-circular materials. In March 2025, Evonik Industries launched its mass-balanced coating additives portfolio, incorporating renewable feedstocks into high-performance wetting agents and defoamers. These additives allow manufacturers to maintain coating performance while significantly reducing embedded carbon emissions.

Electrification and high-tech applications are driving next-generation additive development. In October 2025, Syensqo (spun off from Solvay) showcased its Tecnoflon® and Solef® additive lines, targeting EV batteries and hydrogen fuel cells, where enhanced chemical resistance and stability are critical. Additionally, Arkema expanded its Kynar® PVDF capacity in September 2025, supporting the production of high-purity additives for wire, cable, and semiconductor applications.

Innovation is also focusing on replacing fluorinated performance characteristics. In June 2025, Evonik Industries introduced TEGO® Foamex 8051, a siloxane-based defoamer designed as a high-performance alternative to fluorinated defoamers in industrial coatings. Meanwhile, in November 2025, Shamrock Technologies advanced non-PFAS tribological additives, aiming to replicate the low-friction benefits of fluoropolymers in industrial and medical coatings.

Material innovation is extending into extreme-performance environments. In September 2025, Arkema launched its Zenimid™ polyimide range, used as additive modifiers to enhance the thermal stability of fluoropolymer coatings in aerospace and high-temperature industrial applications.

Regional expansion strategies are strengthening market penetration. In March 2026, Daikin Industries established a new technical hub in India, focusing on high-purity fluorochemical additives for electronics and EV manufacturing. Industry reports in January 2026 also highlight India as the fastest-growing market for fluoropolymer additives, driven by local manufacturing expansion and export-oriented compliance requirements.

PTFE Micropowder Additives Enhancing Stability and Throughput in EV Battery Coating Lines

The fluoropolymer coating additives industry is being significantly shaped by the rapid scale-up of electric vehicle battery manufacturing, particularly in high-speed electrode coating processes. Slot-die coating lines, operating at increasingly higher speeds, require precise control over slurry rheology and surface tension to maintain uniform coating quality. PTFE micropowder additives are emerging as a critical solution, enabling consistent wet film thickness with tolerance levels within ±1.5% across wide-format electrode foils. These additives reduce shear thinning at high flow rates, ensuring stable coating behavior even at elevated production speeds. As a result, manufacturers have been able to increase line speeds from approximately 50 meters per minute to over 85 meters per minute without introducing defects such as ribbing or edge-beading. Beyond coating stability, PTFE micropowders also enhance downstream mechanical performance by acting as dry lubricants during calendering, reducing internal stress within electrode structures by around 18% and minimizing micro-cracking during winding processes. Surface energy control is another key advantage, with PTFE additives enabling contact angles above 110 degrees in aqueous systems, effectively eliminating pinhole defects that can compromise battery performance. These capabilities are positioning PTFE-based additives as indispensable components in next-generation battery production lines focused on throughput, yield optimization, and product reliability.

Elimination of Fluorinated Surfactants in Food-Contact Coatings Reshaping Additive Formulation Strategies

Regulatory pressure from global food safety authorities is driving a fundamental reformulation shift in fluoropolymer coating additives, particularly in applications involving food-contact release coatings. Updated specifications require residual fluorinated surfactant levels to fall below 25 parts per billion, significantly tightening allowable limits for PFAS-related substances. This has accelerated the adoption of fluorine-free stabilizing agents in PTFE-based dispersions, with approximately 40% of European packaging converters transitioning to alternative chemistries by mid-2025. These next-generation formulations are achieving comparable non-stick performance while delivering a 90% reduction in extractable organic fluorine during migration testing, addressing both regulatory compliance and consumer safety concerns. Major global consumer goods companies are further reinforcing this trend by mandating the elimination of intentionally added fluorinated surfactants in greaseproof packaging by 2026. This convergence of regulatory enforcement and brand-driven sustainability commitments is reshaping additive demand toward high-purity, low-migration fluoropolymer systems. Manufacturers are increasingly focusing on developing advanced aqueous dispersions that balance performance, compliance, and environmental safety, positioning surfactant-free additive technologies as the new standard in food-grade coating applications.

US EPA PFAS Reporting Requirements Driving Demand for Analytically Certified Additive Supply Chains

The implementation of the United States Environmental Protection Agency’s TSCA Section 8(a)(7) reporting rule is creating a substantial opportunity for fluoropolymer additive suppliers capable of delivering high levels of chemical traceability and analytical certification. The regulation mandates comprehensive reporting of PFAS production and usage dating back to 2011, covering more than 1,400 individual compounds. This has created an urgent need for additive batches that are analytically verified as free from restricted substances such as PFOA and PFOS at detection limits below 1 part per billion. Suppliers offering such certified materials are commanding price premiums of approximately 22% over standard-grade products, reflecting the value of compliance assurance in regulated markets. Additionally, coating formulators are increasingly consolidating their supplier base, with approximately 65% of North American companies prioritizing vendors that can provide long-term historical data on chemical composition to support regulatory disclosures. Investments in high-resolution analytical technologies, including mass spectrometry, have increased significantly to enable accurate PFAS detection and reporting. These developments are positioning analytically certified fluoropolymer additives as a critical component in compliance-driven supply chains across coatings and materials industries.

China’s GB/T 39482-2025 Standard Driving Demand for High-Stability Fluoropolymer Additives in Coil Coatings

China’s implementation of the GB/T 39482-2025 standard is creating a strong opportunity for advanced fluoropolymer coating additives designed to enhance dispersion stability and long-term performance in coil coating applications. The updated regulation introduces mandatory testing requirements to ensure coatings maintain pigment and additive dispersion stability for over 12 months of simulated storage, necessitating the use of high-performance polymeric dispersants and leveling agents. These additives are critical in preventing phase separation, pigment flocculation, and surface defects in fluorocarbon systems such as PVDF and FEVE coatings used in infrastructure projects. The standard also imposes stringent performance benchmarks, including 3,000-hour accelerated weathering resistance without additive leaching or surface degradation, significantly raising the bar for coating durability. As a result, demand for specialized fluorosurfactant-free additives has increased by approximately 14% year-over-year among Chinese coil coating manufacturers. Additionally, tighter color consistency requirements, with reduced Delta E tolerances, are driving the adoption of additives that improve pigment wetting and batch-to-batch uniformity. These regulatory developments are positioning high-stability fluoropolymer additives as essential components in advanced coil coating formulations for infrastructure and architectural applications.

Fluoropolymer Coating Additives Market Share 2025: Slip Agents and Liquid Dispersions Lead Performance Enhancements

Function Insights: Slip and Levelling Agents Dominate with Surface Performance Optimization

The slip and levelling agents segment leads the fluoropolymer coating additives market with a 24% market share in 2025, driven by its critical role in enhancing surface smoothness, flow characteristics, and coating aesthetics. These additives, typically based on modified PTFE or silicone-based fluoropolymers, significantly reduce the coefficient of friction, eliminating surface defects such as orange peel in powder coatings and liquid paints. This makes them indispensable in high-performance applications including automotive clearcoats, coil coatings, and industrial finishes, where flawless appearance is essential. Additionally, slip agents improve mar and scratch resistance, creating a lubricious surface that protects coated materials during handling, transport, and installation. This durability is especially valuable in architectural panels, consumer appliances, and heavy equipment coatings, extending product lifespan. As industries increasingly demand high-quality finishes with enhanced durability, slip and levelling additives will remain a cornerstone of innovation in the fluoropolymer coating additives market.

Form Insights: Liquid Dispersions Lead with Ease of Use and Consistent Performance

The liquid dispersions segment dominates the fluoropolymer coating additives market with a 52% share in 2025, owing to its superior ease of incorporation and consistent performance in coating formulations. Liquid fluoropolymer additives can be directly blended into paints, varnishes, and UV-curable coatings without the need for high-shear mixing or elevated processing temperatures, making them highly efficient for manufacturers. This simplifies production workflows and reduces processing time, particularly in large-scale paint and coatings manufacturing. Moreover, liquid dispersions ensure uniform particle distribution, eliminating challenges such as dust generation, agglomeration, and inconsistent dispersion commonly associated with dry powder additives. This results in reproducible slip, wetting, and surface modification performance across batches, which is critical for maintaining quality standards. As demand for high-performance, easy-to-process coating additives grows, liquid dispersions will continue to dominate the fluoropolymer coating additives market.

Fluoropolymer Coating Additives Market Competitive Landscape: PFAS-Free Innovation, High-Performance Additives, and Semiconductor Demand Shaping Growth

The fluoropolymer coating additives market is driven by PFAS-free innovation, high-performance surface modifiers, and rising demand from semiconductors, EV batteries, and advanced coatings. Leading players are focusing on sustainable chemistries, capacity expansion, and specialty additives to enhance adhesion, durability, dielectric performance, and regulatory compliance.

Daikin drives PFAS-free additive innovation and semiconductor-grade fluoropolymer leadership

Daikin Industries is strengthening its leadership in fluoropolymer coating additives through advanced PTFE additive innovation and PFAS-free processing technologies. In February 2026, the company launched PTFE anti-dripping additives with enhanced fibrillation properties, significantly improving flame retardancy in thin-wall electronics and office automation equipment. It also commercialized DAIKIN PPA DAHC-101, a hydrocarbon-based polymer processing aid offering a 100% PFAS-free alternative for polyolefin molding without compromising throughput. Collaborating with Osaka University, Daikin introduced fluoropolymer additive-enabled electrolyte designs to enhance thermal stability in high-energy-density lithium-ion batteries. The company is scaling its fluoro-materials portfolio for data centers, targeting low-dielectric additives for 6G infrastructure and AI-driven cooling systems. With a dominant presence in Southeast Asia and Korea semiconductor hubs, Daikin continues to lead in high-purity PTFE and FEP additive technologies.

Chemours leverages Teflon™ leadership and responsible manufacturing for high-margin applications

The Chemours Company remains the global benchmark in PTFE-based coating additives, leveraging its Teflon™ brand to command a significant share of the fluoropolymer market. The company has developed next-generation PTFE micro-powders using non-fluorinated surfactants, ensuring compliance with evolving PFAS and PFOA regulations in 2026. Its strategic focus on high-margin applications such as hydrogen economy membranes and EV battery safety underscores its role in enabling chemical resistance and dielectric performance. Chemours maintains a strong US-based manufacturing footprint, delivering supply chain resilience for aerospace and defense sectors transitioning from legacy suppliers. Its vertically integrated fluoropolymer capabilities further strengthen its leadership in non-stick coatings and industrial additive solutions. This combination of regulatory compliance and performance positions Chemours at the forefront of advanced fluoropolymer additives.

Syensqo accelerates fluorosurfactant replacement with next-generation sustainable coating additives

Syensqo is emerging as a key innovator in fluoropolymer coating additives by enabling the transition away from traditional fluorosurfactants. At the 2026 American Coatings Show, the company introduced a new generation of fluorosurfactant alternatives targeting full elimination of substances of concern in waterborne coatings. Its Rhodoline® HBR additive has become the industry standard for replacing fluorosurfactants, delivering superior hot-block resistance and foam control in architectural coatings. The commercialization of Addibond™ 106 enhances adhesion and corrosion protection (C3/C4) in direct-to-metal applications, strengthening performance in industrial environments. Syensqo is also scaling its Sipomer® monomer portfolio to improve water resistance and substrate adhesion in sustainable emulsion polymers. This integrated approach positions the company as a leader in eco-friendly, high-performance coating additive solutions.

Arkema expands PVDF additive capacity and circular material innovation for advanced coatings

Arkema S.A. is reinforcing its competitive position through capacity expansion and circular economy innovation in fluoropolymer additives. In March 2026, the company announced a 20% expansion of its Kynar® PVDF facility in China to support growing demand from lithium-ion battery and semiconductor markets. It also launched new PVDF additive capacity in Kentucky, targeting high-performance architectural coatings and water filtration membranes. At JEC World 2026, Arkema introduced Elium® resins with recycled content, integrating fluoropolymer additives to enhance UV resistance in wind energy and marine composites. Its global R&D ecosystem across France, Japan, and the US is focused on decarbonizing industrial materials through bio-attributed solutions such as Rilsan® PA11. This combination of scale, sustainability, and innovation strengthens Arkema’s leadership in advanced fluoropolymer additive technologies.

Shamrock Technologies leads micronized PTFE innovation for surface performance and regulatory compliance

Shamrock Technologies is a niche leader in micronized PTFE and specialty wax additives, focusing on surface enhancement and tactile performance. The company operates advanced laboratories across the US, Belgium, and China, enabling precise control over coating texture, gloss, slip, and abrasion resistance. In January 2026, Shamrock published breakthrough research on texture additives for powder coatings, offering formulators improved performance in heavy-duty industrial finishes. Its regulatory-ready PTFE micro-powders are designed to meet evolving global PFOA-free requirements, addressing increasing compliance challenges in coatings and ink additives. The company’s Performance Solutions portfolio is optimized for digital and flexographic inks, where low coefficient of friction additives are critical for high-speed e-commerce packaging. This specialization positions Shamrock as a key supplier in performance-driven additive markets.

Lubrizol advances hybrid additive systems and PFAS-free solutions for next-generation coatings

Lubrizol Corporation is enhancing its role in the fluoropolymer coating additives market through sustainable innovation and hybrid additive systems. The company is rapidly expanding its PTFE-free wax additive portfolio, delivering high-slip and scratch-resistant alternatives for coatings under increasing PFAS scrutiny. It has also developed EU-compliant PTFE grades that allow manufacturers to maintain performance while meeting “Essential Use” regulatory deadlines. Lubrizol’s Lanco™ surface modifiers have been re-engineered for universal compatibility across solvent-borne and water-borne resins, improving formulation flexibility. Through partnerships with Tier-1 automotive coaters, the company is advancing hybrid wax-fluoropolymer systems that reduce die build-up and melt fracture in high-throughput extrusion processes. This focus on performance, compliance, and integration strengthens Lubrizol’s competitive positioning in advanced coating additives.

United States Fluoropolymer Coating Additives Market: PFAS Compliance and EV Supply Chain Localization

The United States fluoropolymer coating additives market is at the forefront of innovation, driven by stringent PFAS regulations, semiconductor reshoring, and electric vehicle (EV) supply chain localization. The growing focus on sustainability and compliance with the EPA’s TSCA Section 6 risk evaluations is accelerating the shift toward low-emission, non-PFAS, and polymeric additive technologies, reshaping the competitive landscape for high-performance coating additives.

A major growth catalyst is the localization of EV manufacturing, with companies like General Motors investing heavily in domestic production. This has increased demand for PVDF binder additives and PTFE-based wire coating formulations, critical for battery efficiency and electrical insulation. Additionally, the ongoing execution of the CHIPS Act has significantly boosted demand for ultra-pure fluoropolymer additives, including ETFE and PFA, used in semiconductor fabrication facilities.

Product innovation is evolving rapidly, highlighted by PPG Industries’ ENVIROLUXE Plus series, which introduces fluoropolymer-free additives incorporating recycled plastics to maintain durability while reducing environmental impact. The expansion of hyperscale data centers is further driving the use of ETFE-jacketed cables with flame-retardant and low-toxicity additives, ensuring compliance with stringent fire safety standards. Strategic capacity expansions by companies like Chemours and Solvay in battery-grade PVDF production reinforce the U.S. leadership in next-generation coating additive technologies.

China Fluoropolymer Coating Additives Market: Renewable Energy Dominance and Industrial Scale Innovation

China continues to dominate the global fluoropolymer coating additives market share, transitioning toward high-value additive solutions for solar photovoltaics, EV batteries, and chemical processing industries. Government-backed initiatives under the Green Chemistry mandates of the 14th and 15th Five-Year Plans are promoting the adoption of water-based fluoropolymer dispersion additives, supported by tax incentives.

The country’s leadership in solar energy is driving demand for FEP and ETFE additives in bifacial photovoltaic module backsheets, designed to withstand extreme UV exposure. At the same time, large-scale chemical infrastructure investments along the Yangtze River are increasing the use of PTFE micropowder additives in anti-corrosive coatings for aggressive chemical environments.

Technological advancements include the development of nano-filler fluoropolymer additives, which enhance abrasion resistance while reducing polymer usage, improving cost efficiency. Capacity expansions by major players like Dongyue Group are strengthening the domestic supply of PVDF and PTFE additives for lithium-ion battery production.

Additionally, China’s rapid rollout of 5G and emerging 6G infrastructure is boosting demand for low-dielectric fluoropolymer additives, ensuring high-frequency signal integrity in telecommunications applications.

Germany Fluoropolymer Coating Additives Market: Hydrogen Economy and High-Voltage Safety Engineering

Germany is emerging as a key hub in the European fluoropolymer coating additives market, with strong emphasis on green hydrogen infrastructure, high-voltage EV systems, and regulatory compliance with EU PFAS restrictions. The country’s investments in hydrogen electrolyzers are driving demand for PVDF and PFA-based additives, which provide chemical stability under high-pressure and alkaline conditions.

German manufacturers are leading the development of “essential use” fluoropolymer additives, ensuring compliance with upcoming EU PFAS regulations while maintaining performance in critical sectors such as semiconductors and healthcare. The automotive sector is also a major growth driver, with Tier-1 suppliers integrating PTFE-based additives in high-voltage EV connectors to prevent electro-corrosion and enhance safety in advanced charging systems.

Strategic expansions by companies like Arkema and Daikin in the Rhine-Ruhr region are enabling the development of customized ETFE additives for architectural films used in climate-neutral building facades. Additionally, increasing alignment with EN 13501-1 fire safety standards is boosting the use of fluorocarbon-based smoke suppressant additives in public transportation infrastructure, reinforcing Germany’s leadership in safety-driven innovation.

Japan Fluoropolymer Coating Additives Market: High-Purity Semiconductor and Medical Innovation

Japan’s fluoropolymer coating additives market is defined by its leadership in precision engineering, semiconductor fabrication, and advanced medical applications. The country has successfully commercialized Grade-A fluoropolymer additives for chemical delivery systems, ensuring zero contamination in next-generation semiconductor manufacturing processes at the 2nm node.

In the medical sector, innovation is focused on ultra-low extractable FEP additives, used in tubing and drug delivery systems to ensure patient safety and product purity. A notable technological milestone is the development of laser-receptive PTFE additives, enabling high-precision marking of surgical tools without compromising their non-stick properties.

Government support through METI subsidies is accelerating the development of recycled fluoropolymer additives, promoting sustainability and circular economy initiatives. Japan also maintains a dominant position in the optical fiber industry, where specialized FEP additives are used as low-refractive-index cladding materials for high-speed medical imaging devices.

Strategic expansions by companies like AGC Inc. and Daikin are further advancing low-viscosity fluoropolymer grades, supporting additive manufacturing (3D printing) for aerospace and high-tech applications.

South Korea Fluoropolymer Coating Additives Market: Battery Safety and Energy Storage Innovation

South Korea is a global leader in the fluoropolymer coating additives market for energy storage systems (ESS), EV batteries, and advanced electronics manufacturing. The development of fire-retardant fluoropolymer additives capable of achieving UL 94-5VA ratings is enhancing safety in battery modules, preventing thermal runaway propagation.

The marine sector is also benefiting from FEP-based anti-fouling additives, which improve vessel efficiency by reducing hydrodynamic drag while protecting against bio-growth. Major corporations such as LG Chem and Lotte Chemical are expanding their engineering plastic additive portfolios, particularly for low-moisture PVDF grades suited for humid environments.

Significant investments in solid-state battery R&D are positioning fluoropolymer additives as critical components for electrolyte stabilization in next-generation batteries. Regulatory updates under K-REACH 2025 are enforcing strict migration testing standards, ensuring safe use in food-contact applications.

Additionally, the electronics sector is leveraging PTFE micropowder additives in OLED manufacturing equipment, ensuring smooth operation and minimizing particulate contamination in high-precision vacuum systems.

India Fluoropolymer Coating Additives Market: Industrial Expansion and Infrastructure-Led Demand

India is rapidly emerging as a high-potential market in the global fluoropolymer coating additives industry, driven by growth in pharmaceutical manufacturing, infrastructure modernization, and telecommunications expansion. The PLI scheme has accelerated the development of API manufacturing facilities, increasing demand for FEP-lined reactor additives in over 50 new plants commissioned during 2024–2025.

Infrastructure modernization, particularly in the railway sector, is driving the adoption of ETFE-based wire insulation additives for high-speed train networks like Vande Bharat, ensuring fire safety and durability under extreme climatic conditions. Regulatory initiatives by the Bureau of Indian Standards (BIS), including new Quality Control Orders, are mandating strict purity standards for fluoropolymer additives, improving product quality across domestic markets.

Investments by global companies in Gujarat are establishing localized blending and compounding centers, enabling just-in-time supply of PTFE micropowder additives for automotive and textile industries. The rapid growth of e-commerce logistics is also increasing the use of low-friction fluoropolymer additives in conveyor systems to enhance operational efficiency.

Furthermore, the expansion of the telecommunications sector is driving demand for FEP additives in 5G infrastructure, supporting the production of low-loss, high-performance networking hardware across the country.

Fluoropolymer Coating Additives Market Report Scope

Fluoropolymer Coating Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.1 Billion

|

|

Market Size (2032)

|

$3.2 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Additive (Polytetrafluoroethylene, Fluorosurfactants, Fluorinated Polyols, Fluoroelastomer Processing Aids, Perfluoroalkoxy, Fluorinated Silanes, Nano-fluoropolymer Additives), By Function (Slip and Levelling Agents, Wetting and Dispersing Agents, Surface Modifiers, Defoamers and Deaerators, Rheology Modifiers, Anti-fouling, UV and Weathering Stabilizers, Flame Retardant Synergists), By Technology (Water-borne Additives, Solvent-borne Additives, Powder-based Additives, 100% Solids), By End-Use Industry (Automotive and Aerospace, Building and Construction, Electrical and Electronics, Chemical Processing and Oil and Gas, Food and Beverage, Healthcare and Medical Devices, Renewable Energy), By Form (Liquid Dispersions, Dry Powders, Masterbatches)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Chemours Company, Daikin Industries, Ltd., 3M Company, Solvay S.A., AGC Inc., Arkema S.A., Shamrock Technologies, Inc., Micro Powders, Inc., BYK-Chemie GmbH, Evonik Industries AG, Gujarat Fluorochemicals Limited, Maflon S.p.A., Kitamura Limited, Laurel Products, LLC, Fluorogistx LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fluoropolymer Coating Additives Market Segmentation

By Additive

- Polytetrafluoroethylene

- Fluorosurfactants

- Fluorinated Polyols

- Fluoroelastomer Processing Aids

- Perfluoroalkoxy

- Fluorinated Silanes

- Nano-fluoropolymer Additives

By Function

- Slip and Levelling Agents

- Wetting and Dispersing Agents

- Surface Modifiers

- Defoamers and Deaerators

- Rheology Modifiers

- Anti-fouling

- UV and Weathering Stabilizers

- Flame Retardant Synergists

By Technology

- Water-borne Additives

- Solvent-borne Additives

- Powder-based Additives

- 100% Solids

By End-Use Industry

- Automotive and Aerospace

- Building and Construction

- Electrical and Electronics

- Chemical Processing and Oil and Gas

- Food and Beverage

- Healthcare and Medical Devices

- Renewable Energy

By Form

- Liquid Dispersions

- Dry Powders

- Masterbatches

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Fluoropolymer Coating Additives Market

- The Chemours Company

- Daikin Industries, Ltd.

- 3M Company

- Solvay S.A.

- AGC Inc.

- Arkema S.A.

- Shamrock Technologies, Inc.

- Micro Powders, Inc.

- BYK-Chemie GmbH

- Evonik Industries AG

- Gujarat Fluorochemicals Limited

- Maflon S.p.A.

- Kitamura Limited

- Laurel Products, LLC

- Fluorogistx LLC

*- List not Exhaustive