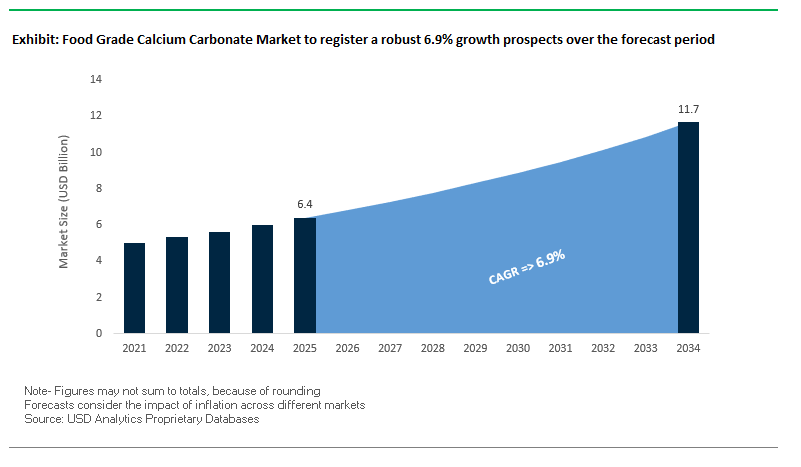

Market Overview: Food Grade Calcium Carbonate Market Valued at $6.4 Billion in 2025

The Global Food Grade Calcium Carbonate Market is valued at USD 6.4 billion in 2025 and projected to reach USD 11.7 billion by 2034, expanding at a CAGR of 6.9%. Food-grade calcium carbonate has emerged as an essential additive in fortified foods, beverages, and dietary supplements, addressing the global challenge of calcium deficiencies and bone health concerns. Beyond fortification, calcium carbonate plays multiple functional roles as a dough conditioner, processing aid, and anticaking agent, making it a versatile and indispensable ingredient in modern food systems.

The market is shaped by the balance between ground calcium carbonate (GCC) and precipitated calcium carbonate (PCC). While GCC dominates due to cost-effectiveness, PCC is gaining traction in applications requiring higher purity and smoother textures, particularly in bakery products, confectionery, and pharmaceuticals. Its particle uniformity enhances product performance and consumer appeal.

Food-grade calcium carbonate also supports cost optimization for manufacturers, functioning as both a nutritional and structural additive. Given its abundance, cost-effectiveness, and eco-friendliness, it is increasingly used in functional foods, fortified snacks, and confectionery. With consumers demanding BPA-free, high-purity, and eco-certified products, the industry is moving towards sustainable sourcing and advanced processing technologies.

Key Insights for Industry Professionals:

- Market Size 2025: USD 6.4 Billion | 2034: USD 11.7 Billion | CAGR: 6.9%

- Nutritional demand: Fortification in beverages, baked goods, and supplements.

- Material trend: GCC dominates, but PCC adoption is rising in high-purity applications.

- Functional roles: Used as anticaking agent, dough conditioner, and flow enhancer.

- Cost advantage: Reduces production costs while maintaining product quality.

- Sustainability: Circular economy initiatives influencing sourcing and processing.

Market Analysis: Recent Developments in the Food Grade Calcium Carbonate Market

The food grade calcium carbonate industry is witnessing strong investment momentum, sustainability-driven innovation, and cross-industry collaborations that reinforce its strategic importance across food, beverages, and supplements.

In August 2025, Beta Glass recorded a 63% revenue surge, highlighting robust performance in the packaging industry, which is interconnected with food-grade minerals through supply to food and beverage end-users. Similarly, in July 2025, Verallia introduced Vista, a new 100% post-consumer recycled (PCR) glass type, emphasizing sustainability trends that parallel calcium carbonate sourcing strategies.

Sustainability-focused innovation has been a major driver. In July 2024, Mineral Technologies Inc. signed an agreement with a global paper manufacturer in Brazil to implement NewYield LO PCC technology, converting paper mill waste into precipitated calcium carbonate. This development demonstrates the growing circular economy integration of PCC technology, which can be adapted for food-grade applications. Earlier, in April 2024, MTI further strengthened its foothold in China and India with three long-term PCC supply agreements, enabling it to better serve Asia’s fast-growing fortified food and supplement industries.

M&A activity has also reshaped competition. In January 2023, Holcim acquired Nicem, a leading Italian GCC producer, strategically enhancing its European footprint in high-purity calcium carbonate. Meanwhile, in February 2024, reports noted a recovery in the DACH construction markets, indirectly influencing calcium carbonate demand across multiple industries.

Emerging Trends and Strategic Opportunities Driving the Food Grade Calcium Carbonate Market

Strategic Shift Towards Bioavailable and Highly Soluble Formulations

The food grade calcium carbonate (FGCC) market is experiencing a strategic transition from traditional ground limestone to engineered forms such as precipitated calcium carbonate (PCC) and amorphous calcium carbonate (ACC), driven by demand from functional foods and nutraceutical applications. Enhanced bioavailability is a critical factor, with ACC demonstrating 2 to 4.6 times higher absorption in humans compared to crystalline calcium carbonate (CCC), addressing fortification challenges in complex matrices like plant-based milk and high-fiber bakery products. Solubility improvements are particularly relevant for beverage applications, where standard calcium carbonate exhibits limited solubility. Innovative forms such as calcium lactate citrate and calcium lactate malate are emerging as competitive alternatives, enabling manufacturers to maintain product efficacy. Additionally, co-processed formulations designed to overcome absorption barriers enhanced by factors like Vitamin D are gaining traction, enabling FGCC to meet stringent nutritional labeling requirements and consumer expectations for functional fortification.

Rapid Adoption as a Cost-Effective Opacifier and pH Stabilizer in Plant-Based Beverages

FGCC is increasingly leveraged in plant-based milk alternatives, including almond, soy, and oat beverages, not only for calcium fortification but also for functional performance as a natural opacifier and pH stabilizer. Its multi-functional benefits whitening effect, acidity regulation, and fortification provide a single-ingredient, clean-label solution that enhances product stability and visual appeal. Calcium carbonate helps neutralize the natural acidity in plant-based substrates, preventing protein and fat separation and ensuring consistent texture throughout shelf life. This trend is supported by rising consumer demand for clean-label, plant-based alternatives and aligns with industry efforts to provide functional ingredients that deliver multiple benefits while reducing reliance on synthetic additives.

Development of Co-Processed FGCC for Enhanced Functionality

Significant opportunities exist for manufacturers to develop FGCC co-processed with natural minerals and vitamins, such as magnesium and Vitamin D3, to create synergistic blends with improved technical and health functionality. Co-processing enhances dispersion, reduces chalkiness, and allows for more uniform incorporation in food matrices. The nutraceutical industry demonstrates a successful precedent, with softgel formulations combining calcium carbonate, magnesium, and Vitamin D3 achieving improved absorption and bioactivity. Additionally, functionalized calcium carbonate (FCC) provides a blueprint for food applications, leveraging porous internal structures for better dispersion and texture, transforming FGCC from a commodity ingredient to a high-value specialty solution.

Positioning FGCC as a Natural Alternative to Phosphates in Meat and Seafood Analogues

With increasing consumer scrutiny of synthetic phosphates, FGCC offers a natural, label-friendly alternative for plant-based and cultured meat products. It functions as a pH regulator and moisture-retention agent, improving texture, yield, and sensory qualities while enabling “no phosphates” label claims. Academic and industry research highlights calcium powders derived from natural sources, such as eggshells or oyster shells, as effective replacements for inorganic phosphates. Companies have successfully developed natural phosphate replacement formulations that match the functional performance of synthetic ingredients, creating a clear market opportunity for FGCC in clean-label, next-generation protein products.

Competitive Landscape: Key Companies in Food Grade Calcium Carbonate Market

The Global Food Grade Calcium Carbonate Market is defined by a mix of long-established mineral producers and specialty solution providers that are leveraging R&D, global supply networks, and sustainability strategies to serve food, beverage, and dietary supplement industries.

Omya AG: Global Leader in High-Purity Calcium Carbonate

Omya is a dominant force in the calcium carbonate industry, offering high-purity food-grade solutions for fortified foods, beverages, and supplements. Its Omyadent innovation, highlighted in February 2023, combines calcium carbonate particles with hydroxyapatite for functional use in dental care, showcasing cross-industry potential. Omya’s vertical integration ensures stringent quality control from mining to distribution, providing customers with reliable, consistent supply aligned with food safety regulations.

Huber Engineered Materials: Expanding Through Granulation Expertise

Huber specializes in granular calcium carbonate and blended formulations for food and supplements. Its 2021 acquisition of Nutri Granulations expanded its product capabilities in high-quality granulated calcium carbonate. The company’s strategic focus is on delivering innovative, functional mineral blends that improve fortification in dietary supplements, baked goods, and fortified snacks. Huber’s continuous investment in technology enhances its product performance and regulatory compliance.

Minerals Technologies Inc. (MTI): Driving PCC Innovation

MTI is a global leader in precipitated calcium carbonate (PCC), serving food, pharmaceutical, and paper sectors. In July 2024, MTI’s NewYield LO PCC technology in Brazil demonstrated its ability to convert waste into valuable PCC, reinforcing its sustainability leadership. MTI’s competitive strength lies in particle engineering and purity control, enabling its PCC to deliver superior performance in food formulations.

Imerys S.A.: Specialty Mineral Solutions with Regional Strength

Imerys provides a broad portfolio of calcium carbonate products, including its CalciLight series, which reduces plastic product weight while maintaining durability demonstrating cross-industry adaptability. In August 2022, Imerys divested its U.S. carbonates division to focus on high-growth specialty markets, while its 2019 acquisition of EDK in Brazil expanded its Latin American presence. Imerys positions itself as a sustainability-focused supplier offering versatile, high-performance food-grade mineral solutions.

Mississippi Lime Company: Trusted Supplier of High-Purity Calcium Carbonate

Mississippi Lime Company is recognized for its high-purity calcium-based products, widely used in food fortification, pharmaceuticals, and water treatment. Its Food Grade Calcium Carbonate line is central to its portfolio, offering reliable, safe, and consistent mineral solutions. The company emphasizes continuous process improvement and sustainability, ensuring compliance with stringent global food safety standards while expanding its footprint across diverse end-user industries.

Food Grade Calcium Carbonate Market Share Insights

Ground Calcium Carbonate Leads Market Share by Product Type in the Food Grade Calcium Carbonate Industry

Ground Calcium Carbonate (GCC) dominates with a 70% share, highlighting its role as the volume leader in food-grade calcium carbonate applications. Produced by mechanically grinding limestone or marble, GCC provides a cost-effective calcium source where ultra-high purity is not critical. Its broad adoption in animal feed, staple food fortification, and general food additive roles is driven by its abundance, low processing costs, and widespread availability across regions. While Precipitated Calcium Carbonate (PCC) has carved out a niche for high-purity, high-functionality applications such as excipients and premium dietary supplements, GCC’s sheer cost advantage secures its position as the default option for bulk applications. The market dynamic reflects a clear value-performance tradeoff: GCC dominates high-volume, cost-sensitive markets, while PCC thrives in segments where purity, controlled morphology, and performance outweigh price.

Animal Feed Holds the Largest Market Share by Application in the Food Grade Calcium Carbonate Industry

Animal feed commands approximately 40% of the food grade calcium carbonate industry, cementing its role as the largest end-use application. Calcium carbonate is indispensable for bone health, eggshell strength, and metabolic function in livestock, poultry, and aquaculture, making it a critical mineral additive for global animal agriculture. The scale of demand is immense, tied directly to the rising global consumption of meat, poultry, dairy, and eggs. Feed-grade calcium carbonate also benefits from its cost-efficiency relative to alternative calcium sources, ensuring its widespread adoption across industrial-scale feed mills. While food additives (25%) and dietary supplements drive significant consumer-facing demand, and pharmaceuticals provide a high-value niche, it is the animal feed industry that sustains the bulk of global GCC consumption, reflecting both volume intensity and the irreplaceable nutritional role of calcium carbonate in animal production systems.

United States: FDA Regulations and Functional Food Innovation Driving Market Growth

The United States food grade calcium carbonate market is strongly influenced by the regulatory oversight of the U.S. Food and Drug Administration (FDA). Under Title 21 of the Code of Federal Regulations, Section 73.70, calcium carbonate is approved for safe use as a food additive, particularly in dietary supplements, candies, and even inks on chewing gum. This regulatory clarity has built confidence among manufacturers and consumers, fueling its adoption across functional food and nutraceutical applications. Increasingly, companies are refining production to deliver specialized grades with specific particle sizes, higher purity, and advanced surface treatments to meet the stringent standards of pharmaceuticals and fortified foods.

Industry consolidation is also reshaping the competitive landscape. Cimbar Resources’ acquisition of Imerys Carbonates USA’s assets expanded production capacity and improved supply security across the country. Demand for food grade calcium carbonate is especially high in dietary supplements, processed foods, and beverages, where it serves as a calcium source, anti-caking agent, and leavening agent. With the clean-label movement gaining momentum, U.S. producers are prioritizing purity by eliminating heavy metals and other impurities in line with Food Chemicals Codex (FCC) standards. Meanwhile, e-commerce-driven demand for functional and fortified products continues to accelerate, ensuring strong growth momentum for the sector.

Germany: EU PPWR Compliance and Circular Economy Leadership Defining Market Trajectory

Germany’s food grade calcium carbonate market is deeply tied to the European Union’s stringent regulatory framework, particularly the new EU Packaging and Packaging Waste Regulation (PPWR) that took effect in February 2025. This regulation sets ambitious goals for recyclability and reuse, creating opportunities for calcium carbonate as a functional ingredient in sustainable packaging and food-grade applications. Germany’s Verpackungsgesetz (Packaging Act) further reinforces producer responsibility, making the market a global leader in circular economy practices.

Technological innovation is at the forefront, with companies developing high-purity calcium carbonate products designed for use in pharmaceuticals, confectionery, and specialized functional foods. The growing demand for eco-friendly packaging and food safety standards is pushing the industry toward cleaner, recyclable, and paper-based solutions that leverage calcium carbonate. Sustainability initiatives are particularly influential in Germany, where reducing plastic waste has become both a consumer expectation and a regulatory requirement. As a result, the country is driving Europe’s transition toward recyclable, high-performance additives and functional fillers.

China: Dual-Carbon Targets and AI-Driven Manufacturing Transforming Market Landscape

China’s food grade calcium carbonate market is undergoing a rapid shift, driven by the government’s “dual carbon” targets aimed at achieving carbon neutrality and peak emissions. These initiatives are encouraging the use of eco-friendly materials in food, beverage, and pharmaceutical packaging, directly influencing demand for calcium carbonate. Regulatory oversight through the National Food Safety Standard GB2760-2011 provides a clear framework for food additive use, ensuring safety and compliance across the sector.

On the technology front, manufacturers are embracing automation, AI, and “5G plus industrial internet” to enhance production efficiency and capacity flexibility. These smart manufacturing investments are enabling scalable, high-quality calcium carbonate production tailored for functional foods, dietary supplements, and pharmaceutical formulations. Additionally, stricter environmental policies are pushing smaller, inefficient mills out of the market, consolidating production among larger players. This has opened the door for global leaders like Minerals Technologies Inc., which recently expanded its presence in China by establishing an on-site precipitated calcium carbonate (PCC) plant under new supply agreements. E-commerce growth, coupled with rising consumer demand for fortified foods, further cements China as one of the most dynamic growth hubs for this market.

India: Make in India and Healthcare Demand Accelerating Market Adoption

India’s food grade calcium carbonate market is thriving under supportive governmental policies and a rapidly expanding consumer base. Initiatives like “Make in India” and “Zero Effect Zero Defect” are promoting high-quality domestic production, while the Production Linked Incentive (PLI) Scheme for the food processing sector is attracting new investments in manufacturing infrastructure. These efforts are boosting local capacity and ensuring standardized, high-quality calcium carbonate for food, beverage, and pharmaceutical applications.

The country’s growing middle class, rising disposable income, and urban lifestyle shifts are driving demand for fortified foods, single-serve products, and nutritional supplements enriched with calcium carbonate. At the same time, India’s fast-growing pharmaceutical and healthcare sectors driven by an aging population and higher chronic disease prevalence are increasing demand for high-purity calcium carbonate as an excipient and supplement ingredient. Environmental regulations, particularly the Plastic Waste Management (Amendment) Rules, are also influencing food and beverage packaging, indirectly boosting demand for eco-friendly additives like calcium carbonate. Combined, these drivers position India as one of the fastest-growing markets globally.

Brazil: Circular Economy Policies and Strategic Investments Fueling Market Growth

Brazil’s food grade calcium carbonate market is undergoing transformation through sustainability policies and advanced technology integration. The National Solid Waste Policy has been central in pushing industries toward circular economy models, promoting the adoption of reusable and recyclable alternatives. The government’s January 2025 ban on solid waste imports, including plastics, has further encouraged domestic innovations in packaging and food-grade applications.

Technological advancement is also a defining trend. Robotics and artificial intelligence are being implemented across packaging and food additive industries to improve production efficiency and quality assurance. Notably, Minerals Technologies Inc. has invested in upgrading a PCC plant in Brazil with its NewYield LO PCC technology, which converts paper mill waste into functional filler pigments. This reduces raw material consumption, lowers disposal costs, and improves paper quality, supporting both food and packaging applications. As Brazil’s demand for sustainable food packaging and fortified products grows, calcium carbonate’s multifunctional properties are positioning it as a key additive in the region.

Japan: Regulatory Updates and Bio-Based Material Innovation Reshaping the Market

Japan’s food grade calcium carbonate market reflects the country’s advanced recycling systems and strong regulatory compliance culture. The Containers and Packaging Recycling Law ensures accountability across industries, creating a highly efficient recycling ecosystem. In May 2025, Japan’s Ministry of Health, Labour and Welfare (MHLW) introduced new standards for food-contact packaging under the Food Sanitation Act, including migration limits for synthetic resins, which is driving a stronger push for bio-based and safer materials.

Innovation in functionality and bio-material integration is a major driver of the Japanese market. Companies are investing in specialized calcium carbonate with enhanced dimensional stability and resistance to deformation for use in high-performance food and pharmaceutical applications. At the same time, the shift toward bio-based materials is evident, as seen in LyondellBasell’s collaboration with Shiseido to use bio-based polypropylene in packaging. This broader trend toward sustainable materials is creating opportunities for calcium carbonate as a functional, eco-friendly additive. The Japanese market, therefore, stands out for its blend of sustainability, regulatory compliance, and technological advancement in food grade applications.

Food Grade Calcium Carbonate Market Report Scope

Food Grade Calcium Carbonate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$11.7 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Product Type (Ground Calcium Carbonate, Precipitated Calcium Carbonate), By Form (Powder, Granules, Slurry), By Application (Dietary Supplements, Food Additives, Pharmaceuticals, Animal Feed, Other Applications), By End-Use Industry (Bakery, Dairy Products, Beverages, Pharmaceuticals & Nutraceuticals, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Omya AG, Imerys S.A., Minerals Technologies Inc., J.M. Huber Corporation, Mississippi Lime Company, Maruo Calcium Co., Ltd., Schaefer Kalk GmbH & Co. KG, Lhoist Group, Carmeuse, Shiraishi Calcium Kaisha, Ltd., Boral Limited, Calchem, CalciTech Ltd., GLC Minerals, LLC, ILC Resources

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Grade Calcium Carbonate Market Segmentation

By Product Type

- Ground Calcium Carbonate

- Precipitated Calcium Carbonate

By Form

By Application

- Dietary Supplements

- Food Additives

- Pharmaceuticals

- Animal Feed

- Other Applications

By End-Use Industry

- Bakery

- Dairy Products

- Beverages

- Pharmaceuticals & Nutraceuticals

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Grade Calcium Carbonate Market

- Omya AG

- Imerys S.A.

- Minerals Technologies Inc.

- J.M. Huber Corporation

- Mississippi Lime Company

- Maruo Calcium Co., Ltd.

- Schaefer Kalk GmbH & Co. KG

- Lhoist Group

- Carmeuse

- Shiraishi Calcium Kaisha, Ltd.

- Boral Limited

- Calchem

- CalciTech Ltd.

- GLC Minerals, LLC

- ILC Resources

* List Not Exhaustive

Methodology

The Food Grade Calcium Carbonate Market research conducted by USDAnalytics employs a comprehensive methodology integrating primary and secondary research to deliver actionable insights for industry professionals. Primary research involved interviews with leading manufacturers, suppliers, and distributors of ground and precipitated calcium carbonate across key regions including the U.S., Germany, China, India, Brazil, and Japan, gathering insights on production technologies, functional applications, bioavailability enhancements, and co-processed formulations. Secondary research included analysis of company annual reports, government regulations, patent filings, trade journals, and sustainability initiatives, validating trends in fortified foods, dietary supplements, plant-based beverages, and animal feed applications. Historical market data from 2015–2024 was combined with strategic developments such as M&A activities, regulatory shifts, and technological innovations to project market growth to 2034. Advanced modeling techniques and scenario analyses were employed to assess the impact of factors such as GCC vs. PCC adoption, cost-effective opacification, smart nutrient fortification, and circular economy initiatives, ensuring precise and reliable insights for decision-makers navigating the evolving global Food Grade Calcium Carbonate Market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.