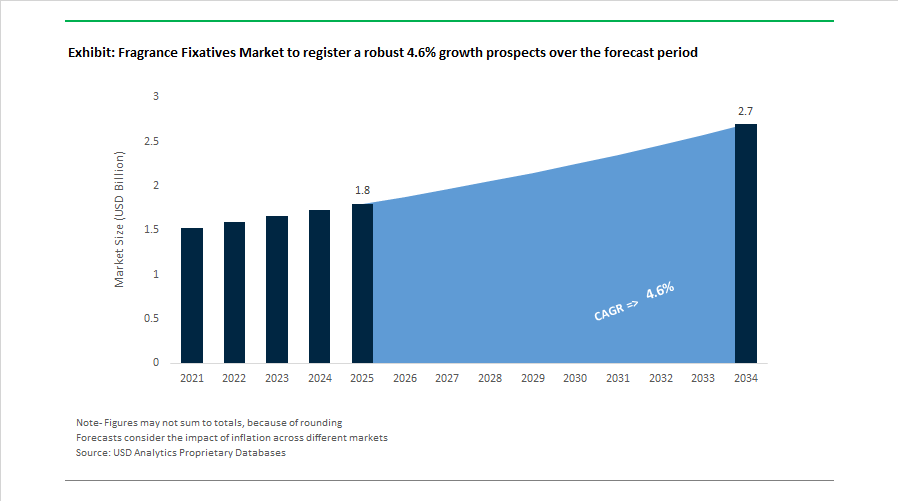

Fragrance Fixatives Market Size 2025–2034: $1.8 Billion to $2.7 Billion at 4.6% CAGR Driven by Sustainable Anchoring and Biotech-Derived Base Notes

The Fragrance Fixatives Market is projected to expand from $1.8 billion in 2025 to $2.7 billion by 2034, registering a CAGR of 4.6%. Market growth is anchored in rising demand for long-lasting perfumes, fabric care scent retention, air care systems, and premium personal care formulations that require stable base notes and controlled evaporation profiles. Natural fixatives, biotech-derived aroma anchors, plant-based esters, and microplastic-free encapsulation systems are increasingly replacing legacy synthetic musks and petroleum-derived stabilizers. Regulatory compliance with ECHA standards, carbon footprint transparency, and circular sourcing strategies are reshaping procurement criteria across global fragrance houses and FMCG brands.

In November 2025, IFF inaugurated an on-site green hydrogen facility in Benicarló, Spain, supporting low-carbon synthesis of aroma chemicals and fixatives. The same month, IFF introduced an AI-powered smart dosing robot across its production network to optimize the ratio of fixatives to volatile top notes, ensuring batch-to-batch consistency while reducing raw material waste. In December 2025, dsm-firmenich unveiled a fragrance collection inspired by “Cloud Dancer,” utilizing Clearwood Prisma, a biotech-derived base material functioning as a sustainable fixative that delivers extended longevity with a lightweight olfactory profile. During late 2025 and into 2026, Symrise evaluated strategic divestment of its terpene ingredients business as part of a transformation plan prioritizing high-margin, performance-driven fixatives and cosmetic actives.

In October 2025, Givaudan announced the acquisition of Belle Aire Creations, strengthening its mid-market presence in North America and expanding access to specialized fixative systems for air care and professional scent branding. In September 2025, Givaudan broke ground on a CHF 40 million facility in Guangzhou to localize fragrance fixative production for the rapidly expanding Asian cosmetics and personal care markets. In July 2025, IFF launched ENVIROCAP™, a biodegradable biopolymer encapsulation technology designed to anchor scent molecules in fabric care products while meeting EU restrictions on synthetic microplastics. Earlier in 2025, IFF completed acquisition of Aromtech Ltd, enhancing its portfolio of natural fixatives derived from supercritical CO2-extracted berry seeds and plant lipids. In April 2025, BASF introduced reduced product carbon footprint versions of L-Menthol FCC with plans for Citronellol and Geraniol variants, reinforcing the transition toward lower-carbon base and fixative ingredients.

Innovation momentum intensified across 2025 through collaborative and botanical initiatives. Givaudan launched Fixalure Naturals following acquisition of a botanical chemistry startup, positioning plant-derived esters as replacements for traditional synthetic musks while maintaining 8-to-12-hour scent anchoring performance. During 2025, Symrise and Mane partnered to co-develop natural fixatives derived from upcycled wood and citrus side-streams, aligning with circular economy sourcing requirements demanded by European retailers and luxury fragrance brands.

Trends and Opportunities Shaping the Fragrance Fixatives Market

Accelerated Shift to Bio-Based Fixatives and White Biotechnology Captives

Retailer-driven clean beauty standards and tighter EU REACH Annex XVII scrutiny on synthetic musks are pushing fragrance houses toward bio-based and fermentation-derived fixatives. By late 2025, leading players such as Givaudan and Symrise had scaled white biotechnology platforms to industrialize sustainable alternatives to legacy petrochemical and animal-derived fixatives. Microbial fermentation now enables consistent, ethical production of Ambroxide and Sclareolide derived from clary sage, with bio-based variants accounting for more than 23% of the premium fixative segment.

Green chemistry is becoming a commercial differentiator rather than an R&D experiment. In June 2024, P2 Science expanded its Citropol F platform, a bioderived and biodegradable fixative engineered to enhance fragrance stamina without petrochemical solvents. These molecules deliver high hydrolytic stability, making them particularly valuable in liquid soaps and detergents where fixatives must withstand water exposure without scent breakdown.

Regulatory pressure is accelerating this transition. Commission Regulation (EU) 2025/1090, effective June 2025, tightened limits on volatile organic solvents, prompting a 15% year over year increase in R&D investment into botanical resinoids such as benzoin and labdanum. These high-molecular-weight materials function as true fixatives by anchoring volatile top notes, while aligning with low-VOC and natural-origin positioning demanded by European retailers.

Next-Generation Biodegradable Encapsulation for Time-Released Performance

Encapsulation technology is redefining how fixatives deliver longevity while complying with emerging microplastic bans. In November 2025, Givaudan expanded its PlanetCaps range, the first high-performing biodegradable fragrance encapsulation system compliant with ECHA microplastic regulations. These capsules provide friction-activated release in hair and body care, preserving scent integrity while eliminating persistent polymer residues.

Laundry care has become a key proving ground for encapsulated fixatives. The launch of IRRESISTIBLE Laundry Serum in Q4 2025 introduced a formulation carrying a 40% fragrance load within biodegradable microcapsules. This technology supports wash-to-wardrobe freshness lasting up to one year, responding directly to consumer demand for extreme longevity in fabric care products.

Beyond durability, fixatives are becoming responsive systems. Innovations showcased in 2025 include smart aromachology capsules designed to modulate fragrance diffusion based on biometric signals such as skin temperature. These systems transform fixatives from static stabilizers into active components that shape user experience across the product lifecycle.

Functional Fixatives for Premium Home and Fabric Care

Premiumization across household categories is expanding demand for fixatives that can withstand thermal and mechanical stress. In home fragrance, manufacturers increasingly specify fixatives that prevent olfactive drift in candles and reed diffusers exposed to temperatures above 50°C. By 2025, materials such as sucrose acetate isobutyrate and high-stability resins saw strong adoption in prestige home care lines where scent consistency defines brand equity.

Fabric care represents an even larger volume opportunity. Initiatives by Procter & Gamble and Unilever to elevate everyday products have accelerated development of substantive polymer fixatives that bind fragrance molecules to cotton and synthetic fibers. These systems ensure premium notes such as neo-gourmand coffee and spice profiles remain perceptible even after repeated washing and high-heat tumble drying.

While prestige fragrance grew approximately 6% in the first half of 2025, the mass market for fragranced household goods expanded by 17%. This divergence creates a substantial opportunity for cost-effective synthetic-alternative fixatives, including Iso E Super, which deliver strong sillage and diffusion at price points suitable for high-volume applications.

Performance Stability in Alcohol-Free and Water-Based Formats

The rise of halal-certified, sensitive skin, and alcohol-free fragrances is reshaping fixative requirements. Water-based perfumes lack the inherent preservative and fixative properties of ethanol, creating a technical challenge around longevity. In 2025, this drove increased use of water-soluble fixative polymers such as acrylate copolymers and natural solubilizers including ethoxylated sorbitan esters, designed to stabilize oil droplets and slow fragrance evaporation.

Growth in adjacent formats is amplifying this opportunity. Hair mists and body sprays recorded a 22% increase in consumer uptake during 2024–2025, driven largely by Gen Z and Gen Alpha preferences. These applications require non-drying fixatives that adhere closely to hair and skin, releasing aroma gradually through body heat without causing damage or irritation.

Longer term, bioeconomy commitments are reinforcing natural fixative pathways. At COP30 in November 2025, industry leaders emphasized the role of CO₂-extracted botanicals in future alcohol-free formulations. These extracts function as self-fixating systems due to their complex molecular profiles, aligning natural-origin claims with performance requirements in a global fragrance market exceeding USD 100 billion in value.

Fragrance Fixatives Market Share and Segmentation Insights

Synthetic Fixatives Dominate Fragrance Stability Technologies Across Modern Perfume Formulations

Synthetic Fixatives accounted for 64.80% of the Fragrance Fixatives Market share in 2025, making them the dominant category used to enhance fragrance longevity and stability in perfume and scented product formulations. Synthetic fixatives—including compounds such as musk ketone, ethylene brassylate, ambroxan, iso E super, and other synthetic macrocyclic musks—play a critical role in slowing the evaporation rate of volatile fragrance molecules. By stabilizing fragrance compositions, these ingredients allow perfumes and scented products to maintain consistent aroma profiles over extended periods, improving product performance and consumer satisfaction. Synthetic fixatives dominate the market because they offer consistent chemical purity, scalable production capacity, stable pricing, and customizable performance characteristics, advantages that natural fixatives often cannot provide due to supply limitations and variability. In 2025, the fragrance industry is undergoing a significant phthalate-free reformulation shift, driven by consumer concerns and regulatory scrutiny surrounding compounds such as diethyl phthalate (DEP) traditionally used as fragrance carriers and fixatives. Leading fragrance manufacturers have transitioned toward alternative synthetic fixative systems based on sebacates, citrates, and benzoates, which maintain fragrance longevity while complying with clean beauty standards and evolving regulatory frameworks. This shift is redefining product development strategies across the global fragrance fixatives market.

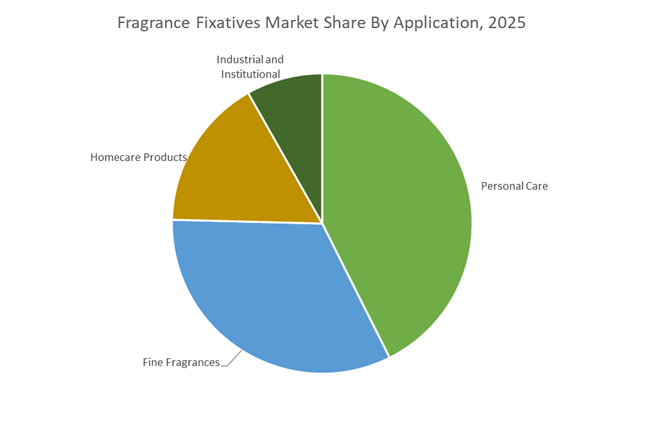

Personal Care Formulations Drive the Largest Demand for Advanced Fragrance Fixative Systems

Personal Care accounted for 42.60% of the Fragrance Fixatives Market share in 2025, making it the largest application segment for fragrance stabilization ingredients. Personal care products—including lotions, body creams, shampoos, deodorants, soaps, and shower gels—are used daily by billions of consumers worldwide, creating substantial demand for fragrance systems that deliver long-lasting scent performance and consistent sensory experiences. Because these products often contain complex formulation bases such as surfactants, emulsions, and active skincare ingredients, maintaining fragrance stability requires highly effective fixative technologies capable of preserving scent integrity throughout product storage and use. A key technical challenge influencing product development in 2025 is the rinse-off durability requirement in personal cleansing products. Consumers increasingly expect fragrances from products such as shampoos, body washes, and conditioners to remain perceptible even after rinsing. To address this challenge, fragrance houses and ingredient manufacturers are developing polymer-assisted fixative delivery systems, which allow fragrance molecules to adhere to skin and hair surfaces and release gradually over time.

Competitive Landscape in Fragrance Fixatives Market

Givaudan Strengthens Bio-Based Fixatives and AI-Driven Scent Longevity

Givaudan S.A. is the dominant force in fragrance fixatives. The company’s captive molecules such as Ambrofix and Georgywood are widely used for long-lasting woody and amber profiles in fine fragrance and premium personal care. In February 2025, Givaudan expanded its portfolio with a new range of bio-based and renewable fixatives aligned with biodegradable standards emerging in the EU and North America. Late 2025 performance showed mass-market fragrance growth of 17%, reinforcing strong volume traction. Its 2025 to 2030 roadmap prioritizes Asia and the Middle East, markets known for demand for high tenacity fragrance compositions. Through AI integration and neurobiology research, Givaudan is engineering fixatives designed to enhance both scent persistence and targeted emotional responses, reinforcing its science-driven leadership in fragrance longevity chemistry.

dsm-firmenich Advances Fermentation-Derived and Multi-Sensory Fixatives

dsm-firmenich has strengthened its position in fragrance fixatives through biotechnology-derived ingredients following its merger transformation. In April 2025, the company introduced fermentation-based fixatives designed to lower environmental impact while preserving premium olfactory diffusion and stability. Clearwood Prisma remains a flagship biotech-derived material used as a sustainable fixative and scent amplifier in high-end formulations. The company’s Freezestorm™ cooling technology underpins multi-sensory fragrance systems, highlighted by the 2026 Frosted Star Anise launch. Through collaboration with Pantone, dsm-firmenich introduced the Cloud Dancer collection in 2026, reinforcing emotional balance and scent longevity themes across formats. By aligning fermentation chemistry with sensory science and premium branding initiatives, dsm-firmenich strengthens its competitive stance in sustainable fragrance fixative innovation.

IFF Reinvests in High-Margin Fixatives and Traceable Natural Ingredients

International Flavors & Fragrances is executing a portfolio reshaping strategy to prioritize high-margin specialty ingredients, including advanced fragrance fixatives. For 2026, the company issued sales guidance between $10.5 billion and $10.8 billion while launching a sale process for its Food Ingredients business to redirect capital toward scent and biosciences divisions. Between 2024 and 2026, IFF is reinvesting $150 million into innovation, with capital expenditure projected at 6% of sales to expand capacity and digital transformation. The company is targeting the Middle Eastern fine fragrance market, where demand for ultra-long-lasting perfume bases is strongest. Through LMR Naturals, IFF provides traceable, sustainable natural fixatives with high transparency in sourcing and extraction. This combination of capital reallocation, natural ingredient traceability, and premium scent development reinforces IFF’s position in high-value fragrance fixatives.

Symrise Expands Circular Economy and AI-Optimized Sustainable Fixatives

Symrise AG differentiates itself through circular economy strategies and AI-enabled fragrance optimization. Its Philyra 2.0 tool is being used to reformulate existing fragrances with biodegradable or renewable fixatives while preserving scent character and performance. The company is targeting average annual sales growth of 5 to 7% through 2028 with EBITDA margins between 21 and 23%, reflecting disciplined margin management in specialty aroma chemicals. Symrise markets molecules such as Sultanene and Filbertone, valued for diffusivity and long-lasting scent retention. The achievement of FSC Chain of Custody certification for forest-derived ingredients strengthens its leadership in sustainably sourced woody fixatives. Through upcycling side-stream raw materials into high-value aroma compounds, Symrise reinforces its commitment to sustainable fragrance chemistry.

Mane Expands Encapsulation Capacity for Timed-Release Fragrance Systems

Mane SA continues to advance timed-release fragrance longevity through encapsulation technologies and natural extraction platforms. The Phase II expansion of its Pinghu, China facility, initiated in late 2025 with a $70 million investment, is expected to add 17,000 tons of annual capacity focused on fragrance formats and encapsulated fixatives. Mane’s E-Pure technology supports high-purity natural fixatives used in prestige and niche perfume segments. The company opened a Fine Fragrance creation center in China in 2024 to address regional preferences for long-lasting scent profiles tailored to local consumer trends. Encapsulation innovation enables controlled fragrance release in laundry, home care, and personal care applications. By combining green chemistry principles with regional production expansion, Mane strengthens its foothold in high-performance fragrance fixatives.

Takasago Integrates Bioscience and Neuroscience in Functional Fixatives

Takasago International Corporation leverages asymmetric synthesis expertise and bioscience research to enhance fragrance fixative performance. In February 2026, Takasago joined the Together for Sustainability initiative, reinforcing supply chain transparency and environmental compliance in aroma chemical production. The company is developing aroma ingredients derived from renewable and unused resources while incorporating catalytic manufacturing processes to lower environmental impact. Ongoing research into neuroscientific responses to scents aims to create functional fixatives that sustain stress-reduction and mood-enhancing effects over extended wear periods. Takasago maintains a strong position in Asian household and personal care markets, integrating advanced Japanese technology with global fragrance trends. This fusion of bioscience, sustainability, and functional scent engineering strengthens its competitive role in the evolving fragrance fixatives market.

United States: Regulatory Enforcement and Asset Realignment Reshaping Fixative Chemistry

The United States fragrance fixatives market is undergoing structural change driven by asset consolidation, state-level regulation, and federal oversight. In March 2025, Ashland Inc. finalized a USD 2.1 billion divestiture of its Avoca division to Mane. The transaction transferred key production assets in North Carolina and Wisconsin, positioning Mane as a primary domestic producer of sclareolide, a high-performance fragrance fixative widely used as a sustainable ambergris alternative. This shift has materially strengthened U.S.-based supply of bio-derived and long-lasting fixatives for fine fragrance and personal care formulations.

Regulatory pressure is accelerating reformulation. The enforcement of Washington State’s Toxic-Free Cosmetics Act from January 1, 2025 has restricted intentionally added phthalates and formaldehyde releasers, compelling national brands to pivot toward natural resins, aromatic ethers, and clean-label fixative systems. At the federal level, implementation of the Modernization of Cosmetics Regulation Act is intensifying facility registration and safety dossier requirements through 2025–2026. In parallel, U.S. fragrance houses are adopting AI-enabled “story-smelling” platforms that translate consumer data into real-time fixative tuning, optimizing scent longevity based on humidity and skin chemistry. These dynamics are redefining the U.S. market around compliant, data-driven, and sustainability-aligned fixative innovation.

France: Regulatory Leadership and Biotechnological Fixative Innovation

France remains the strategic nerve center of global fragrance fixatives, with regulatory leadership directly shaping product design. Following its U.S. acquisition, Mane expanded R&D activities in Grasse during 2025, focusing on biotechnological synthesis routes for next-generation fixatives. With 2024 revenues of EUR 1.77 billion and a dedicated innovation allocation for 2025–2026, the group is prioritizing sustainable ingredient platforms that balance olfactive performance with regulatory compliance.

France is also setting the pace on chemical restrictions. The national ban on PFAS in cosmetics, effective January 2026, is forcing a full redesign of long-wear fragrance systems that historically relied on fluorinated stabilizers. In addition, mandatory compliance with the 51st Amendment of the International Fragrance Association from October 30, 2025 has restricted or prohibited 59 substances, including several legacy fixatives flagged for genotoxicity risks. These measures are accelerating the shift toward biodegradable, non-persistent fixatives and reinforcing France’s role as the regulatory and innovation benchmark for global fragrance formulation.

China: Safety Dossiers and Localization Driving Synthetic Fixative Demand

China’s fragrance fixatives market is being reshaped by tighter regulatory oversight and accelerated localization of synthetic capacity. In July 2025, the National Medical Products Administration mandated full safety dossiers and enhanced adverse event reporting for all fragrance ingredients. This requirement has favored standardized, well-documented synthetic fixatives such as galaxolide and ambroxide sourced from verified global suppliers, raising compliance thresholds across the market.

Concurrently, consumer trends are influencing formulation strategy. The revival of “Chinese-style” fragrances in 2025 has combined traditional aromatic elements such as incense and regional resins with modern fixative technologies. Microencapsulation is being widely adopted to preserve delicate top notes while delivering extended wear in luxury offerings. On the supply side, capacity expansions in the Zhejiang Free Trade Zone during 2025–2026 are localizing production of synthetic musks, reducing dependence on European imports and supporting China’s vast personal care and home care sectors with domestically produced fixative intermediates.

India: Bio-Based Fixatives and Export Professionalization

India’s fragrance fixatives market is advancing through a blend of biomanufacturing support and regulatory formalization. Growth in 2025 is being propelled by the BioE3 Policy, which is funding the development of ayurvedic-aligned fixatives derived from Indian sandalwood and indigenous essential oils. These bio-based materials are gaining traction in fine fragrance and wellness-oriented personal care products, aligning traditional aromatic heritage with modern formulation needs.

Export readiness is also improving. New 2025–2026 requirements from the Directorate General of Foreign Trade mandate exporter registration and GST-linked pollution control permits, raising compliance standards for domestic producers. This has strengthened the global competitiveness of Indian suppliers such as SVP Chemicals and Synthodor. At the same time, multinational brands including Oriflame have expanded localized luxury fragrance manufacturing in India, specifying high-solubility fixatives engineered for high-temperature and high-humidity climates. These trends position India as both an innovation and manufacturing hub for climate-adapted fixatives.

Japan: Precision Sustainability and Functional Fragrance Systems

Japan’s fragrance fixatives market is defined by precision chemistry and sustainability-led differentiation. In 2025, Takasago announced significant investment in green chemistry platforms, targeting carbon-neutral aromatic ethers and bio-based feedstocks. This initiative reflects the expectations of Japanese luxury consumers for traceable, low-impact fragrance ingredients without compromising scent longevity.

Looking ahead, Japanese chemical companies are leading research into advanced encapsulation technologies. Ongoing 2026 R&D programs are focused on nano-encapsulated fixatives that release scent in response to body temperature or motion. These innovations are tailored for premium active-wear fragrances and deodorants, where controlled release and durability are critical. Japan’s trajectory highlights a shift from traditional fixatives toward intelligent, function-driven systems integrated with lifestyle and performance attributes.

Summary of Country-Level Strategic Drivers in the Fragrance Fixatives Market

Fragrance Fixatives Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for Fragrance Fixatives

|

|

United States

|

TFCA and MoCRA enforcement

|

Rapid shift to clean-label, traceable fixatives

|

|

France

|

PFAS ban and IFRA compliance

|

Acceleration of biodegradable and bio-synthesized fixatives

|

|

China

|

NMPA safety dossier mandate

|

Rising demand for standardized synthetic fixatives

|

|

India

|

BioE3 policy and export regulation

|

Growth in bio-based and climate-adapted fixatives

|

|

Japan

|

Sustainability and smart encapsulation

|

Emergence of functional, responsive fixative systems

|

Fragrance Fixatives Market Report Scope

Fragrance Fixatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$2.7 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Fixative Type (Natural Fixatives, Synthetic Fixatives), By Form (Liquid, Solid, Emulsions and Microencapsulated), By Application (Fine Fragrances, Personal Care, Homecare Products, Industrial and Institutional), By Distribution Channel (Direct Sales, E-commerce Platforms, Specialty Chemical Distributors)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Givaudan SA, DSM-Firmenich AG, International Flavors & Fragrances Inc., Symrise AG, Mane SA, Takasago International Corporation, Robertet Group, Sensient Technologies Corporation, T. Hasegawa Co., Ltd., Ashland Inc., Eastman Chemical Company, SVP Chemicals Pvt. Ltd., Synthodor Company, PFW Aroma Chemicals, Kerry Group plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fragrance Fixatives Market Segmentation

By Fixative Type

- Natural Fixatives

- Synthetic Fixatives

By Form

- Liquid

- Solid

- Emulsions and Microencapsulated

By Application

- Fine Fragrances

- Personal Care

- Homecare Products

- Industrial and Institutional

By Distribution Channel

- Direct Sales

- E-commerce Platforms

- Specialty Chemical Distributors

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fragrance Fixatives Industry

- Givaudan SA

- DSM-Firmenich AG

- International Flavors & Fragrances Inc.

- Symrise AG

- Mane SA

- Takasago International Corporation

- Robertet Group

- Sensient Technologies Corporation

- T. Hasegawa Co., Ltd.

- Ashland Inc.

- Eastman Chemical Company

- SVP Chemicals Pvt. Ltd.

- Synthodor Company

- PFW Aroma Chemicals

- Kerry Group plc

*- List not Exhaustive