Furniture Wood Coatings Market Growth Driven by Sustainable Finishes, High-Speed Manufacturing, and Premium Aesthetic Trends

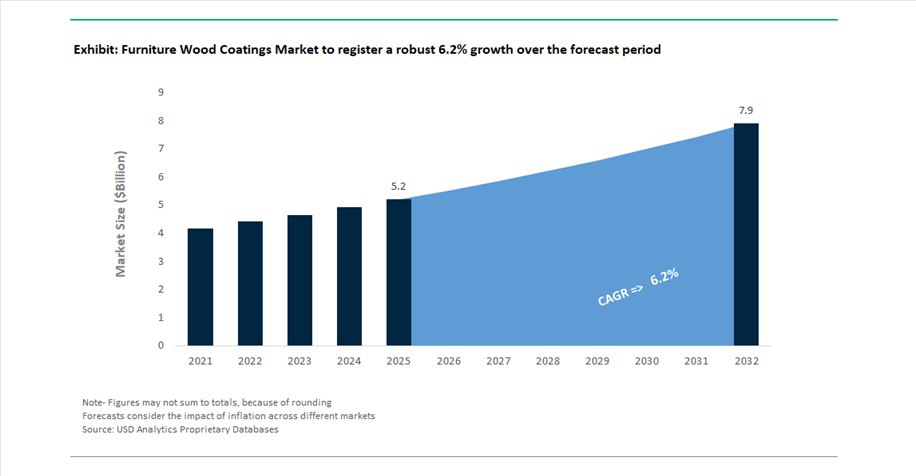

The global Furniture Wood Coatings Market was valued at USD 5.2 billion in 2025 and is projected to grow at a CAGR of 6.2% between 2025 and 2032, reaching USD 7.9 billion by 2032. This growth is fueled by rising demand for durable, sustainable, and design-oriented coatings across residential, commercial, and modular furniture segments.

Furniture wood coatings play a critical role in delivering surface protection, aesthetic enhancement, and longevity, with key properties including scratch resistance, chemical resistance, UV stability, and moisture protection. A major growth driver is the global expansion of ready-to-assemble (RTA) furniture and modular cabinetry, particularly in urban housing markets. These applications require coatings that can withstand high wear-and-tear, repeated cleaning, and transportation stress, while maintaining visual appeal.

Sustainability is a defining trend shaping the market. Manufacturers are rapidly transitioning toward waterborne, low-VOC, and high-solids coating systems, replacing traditional solvent-based finishes. This shift is driven by regulatory pressure, retailer requirements, and consumer preference for environmentally friendly products. Additionally, advancements in fast-curing and energy-efficient coating technologies are enabling furniture manufacturers to increase production throughput while reducing operational costs.

Another key trend is the rise of biophilic and natural design aesthetics, where coatings are engineered to enhance the natural grain and texture of wood rather than obscure it. This has led to increased demand for translucent finishes, matte coatings, and specialty pigments, particularly in premium and custom furniture segments.

Mega-Merger Consolidation, Waterborne System Innovation, and Color-Driven Design Trends Reshape Market Dynamics

The furniture wood coatings market is undergoing a structural transformation driven by industry consolidation, sustainable product innovation, and evolving design preferences. In November 2025, AkzoNobel and Axalta Coating Systems announced a $25 billion merger, combining their wood coating portfolios to create a major global platform focused on high-speed industrial furniture finishing systems. This consolidation is expected to accelerate R&D in coatings for modular and mass-produced furniture.

Sustainability-driven innovation is rapidly advancing. In May 2025, Teknos launched next-generation water-based interior coatings at Ligna 2025, designed to meet stringent emission standards while improving curing efficiency. These systems enable manufacturers to reduce energy consumption and comply with environmental regulations without sacrificing performance.

Product development is increasingly focused on manufacturing efficiency. In March 2026, PPG Industries introduced AQUACRON® WSP, a single-component, primer-and-topcoat-in-one system. This innovation streamlines production lines by reducing coating steps, improving throughput, and enhancing surface durability for high-volume furniture production.

Design-driven innovation is also shaping market demand. In September 2025, AkzoNobel launched its “Rhythm of Blues” color palette, featuring translucent finishes that enhance wood grain visibility, aligning with the growing biophilic design trend. Similarly, in August 2025, Sherwin-Williams introduced its Colormix® 2026 forecast, emphasizing durable, matte finishes for hospitality and healthcare furniture applications.

Premium performance coatings are bridging aesthetics and durability. In June 2025, Hempel launched Flat Eggshell finishes through its Farrow & Ball brand, offering washable, ultra-low-sheen coatings that replicate traditional finishes while providing modern durability.

Regional expansion is strengthening supply chains and market access. In September 2025, Hempel expanded its presence in India with a new technical office in Pune, targeting the rapidly growing domestic furniture manufacturing sector. Meanwhile, Sayerlack (a Sherwin-Williams brand) expanded its premium water-based coating portfolio in November 2025, focusing on professional-grade finishes for custom furniture makers.

Sustainability credentials are becoming a competitive differentiator. In June 2024, Teknos earned the EcoVadis Gold rating, placing it among the top 5% globally and strengthening its position with major furniture retailers requiring verified ESG compliance.

EUDR Compliance Driving Bio-Resin Traceability and Sustainable Formulation Strategies

The furniture wood coatings industry is undergoing a structural transformation as the EU Deforestation Regulation enforces strict traceability requirements for bio-based raw materials used in coating formulations. With a compliance deadline set for December 30, 2026, manufacturers must now demonstrate full supply chain transparency for wood-derived inputs such as tall oil fatty acids used in alkyd resins. This includes providing geolocation data for raw material sourcing, fundamentally altering procurement and supplier validation processes. Non-compliance carries significant financial risk, with penalties reaching up to 4% of annual EU turnover, elevating traceability from a sustainability initiative to a core compliance requirement. In response, coating manufacturers are accelerating the development of bio-based formulations that balance environmental compliance with performance durability. Waterborne wood coatings incorporating 20% to 24% plant-based content are emerging as a viable solution, enabling manufacturers to align with regulatory expectations while maintaining industrial-grade performance. Additionally, the industry is witnessing the widespread adoption of advanced supply chain monitoring systems, including satellite-based verification tools, with approximately 70% of major resin suppliers expected to implement traceability frameworks by 2026. This shift is embedding sustainability and transparency into product development, positioning traceable bio-resin coatings as a competitive differentiator in global furniture markets.

Transition from 2K Polyurethane to 1K Waterborne UV-Cured Systems Enhancing Efficiency and Reducing Emissions

Furniture manufacturers are increasingly transitioning from traditional two-component polyurethane coatings to one-component waterborne UV-cured systems, driven by the need to improve production efficiency and reduce environmental impact. Conventional 2K polyurethane systems are associated with operational inefficiencies, including limited pot life and material wastage of approximately 10% to 15% due to premature curing. In contrast, 1K UV-cured coatings eliminate these inefficiencies by offering ready-to-use formulations that do not require on-site mixing. From a production standpoint, UV-curable systems deliver significant cycle time advantages, achieving sandable cure within minutes compared to the several-hour curing window required for polyurethane coatings. This acceleration enables higher throughput in furniture manufacturing lines and reduces bottlenecks in finishing operations. Additionally, waterborne UV systems significantly lower solvent emissions, with industrial implementations demonstrating reductions exceeding 60% in volatile emissions compared to solvent-based alternatives. These coatings also maintain high durability standards required for commercial office furniture, including resistance to abrasion, chemicals, and daily wear. The convergence of operational efficiency, environmental compliance, and performance reliability is driving widespread adoption of 1K UV-cured coatings as the next-generation solution in wood finishing applications.

California SCAQMD Rule 1136 Driving Reformulation of Low-VOC Touch-Up and Repair Coatings

The amendment of SCAQMD Rule 1136 in April 2026 is creating a substantial opportunity for low-VOC wood coatings, particularly in the touch-up and repair segment. The regulation eliminates the use of historically exempt solvents such as para-chlorobenzotrifluoride and tert-butyl acetate, forcing manufacturers to redesign formulations that meet stricter environmental criteria. The introduction of Product Weighted Maximum Incremental Reactivity limits further shifts compliance from traditional VOC content metrics to ozone-forming potential, requiring advanced formulation strategies to achieve regulatory approval. This transition is impacting approximately 516 industrial facilities in Southern California, creating immediate demand for compliant alternatives that can replace legacy solvent-based coatings. Given that phased-out solvents currently contribute nearly 1.9 tons of daily VOC emissions, the regulatory shift represents both a compliance challenge and a significant market opportunity for innovative low-emission products. Manufacturers capable of developing high-performance coatings that meet these new reactivity-based standards are well-positioned to capture market share in one of the most tightly regulated coatings markets globally.

Japan Food Sanitation Act Driving Demand for Certified Food-Safe Wood Coatings

Japan’s strengthened regulatory framework for food contact materials is opening a high-value opportunity for specialized wood coatings used in kitchenware and food-related applications. The enforcement of the Positive List system mandates that only approved substances can be used in coatings applied to wooden utensils such as bowls, trays, and chopsticks, effectively creating a highly controlled market environment. Compliance requirements extend beyond formulation to rigorous testing protocols, including advanced analytical methods such as inductively coupled plasma mass spectrometry to detect trace levels of harmful substances. Updated regulations also impose stricter limits on formaldehyde and heavy metal migration, increasing the demand for low-leaching, waterborne coating systems that ensure food safety. Non-compliant products face immediate removal from the market, reinforcing the importance of certification and regulatory adherence. These developments are driving innovation in food-safe coatings that combine durability with chemical inertness, positioning certified waterborne wood coatings as essential solutions in Japan’s kitchenware and food service sectors.

Furniture Wood Coatings Market Share 2025: Paints & Enamels and Distribution Networks Drive Growth

Product Type Insights: Paints and Enamels Lead with Color Versatility and Performance Benefits

The paints and enamels segment dominates the furniture wood coatings market with a 32% market share in 2025, driven by strong consumer preference for customizable color finishes and durable surface protection. These coatings offer unlimited color options, including matte, satin, and high-gloss finishes, making them highly popular in bedroom furniture, modular kitchens, children’s furniture, and ready-to-assemble (RTA) segments. The rise of fast-furniture and DIY home improvement trends is further accelerating demand for paints over traditional clear coatings. Additionally, modern water-based acrylic enamels deliver superior performance with excellent scratch resistance, stain blocking, and high opacity, enabling one-coat coverage on MDF, particleboard, and reclaimed wood substrates. This reduces labor time and improves production efficiency for manufacturers. As aesthetics and durability become key purchasing factors, paints and enamels will continue to lead innovation in the global furniture wood coatings market.

Sales Channel Insights: Distributors and Wholesalers Dominate with B2B Supply Chain Efficiency

The distributors and wholesalers segment holds the largest 52% share in the furniture wood coatings market in 2025, reflecting the critical role of bulk supply chains in furniture manufacturing ecosystems. Large-scale furniture producers rely on distributors for consistent, high-volume supply of coatings such as paints, stains, lacquers, and sealers, often delivered in industrial packaging formats like drums, totes, and 5-gallon pails. These partnerships enable volume-based pricing advantages and batch-to-batch consistency, which are essential for maintaining product quality across production lines. Additionally, distributors act as regional supply hubs, maintaining inventory of fast-moving coatings such as pre-catalyzed lacquers and sanding sealers, allowing for just-in-time delivery to cabinet makers and upholstery assembly units. This reduces on-site storage requirements and improves operational efficiency. As furniture manufacturing scales globally, distributor-led supply chains will remain pivotal in supporting market growth.

Furniture Wood Coatings Market Competitive Landscape: Sustainable Formulations, Digital Color Systems, and OEM Integration Driving Competition

The furniture wood coatings market is highly competitive, driven by waterborne technologies, bio-based coatings, and digital color integration. Leading companies are focusing on OEM partnerships, AI-driven customization, and low-VOC formulations to meet evolving sustainability regulations and growing demand in modular furniture and home renovation sectors.

Sherwin-Williams advances OEM wood coatings with AI-driven color systems and bio-based innovation

The Sherwin-Williams Company is strengthening its leadership in furniture wood coatings through advanced color technologies and premium product integration. In Q1 2026, the company introduced the Colormix® 2026 archive, an AI-enhanced palette enabling “Whole-Home Cohesion” for furniture OEMs and interior designers. The integration of its Sayerlack acquisition continues to anchor its premium Italian-designed wood coatings portfolio, reinforcing its dominance in high-end furniture finishes. Its Industrial Wood Coatings division produced over 1,850 custom color panels, offering just-in-time palette assessments and global color studio access. Sherwin-Williams’ R&D hubs feature fully integrated wood finishing operations, enabling real-time testing of clear topcoats and pigmented sealers on high-speed production lines. The company is also scaling bio-based coatings to reduce carbon footprint, particularly in kitchen cabinetry applications, which account for a 25.8% share.

AkzoNobel strengthens global dominance through Axalta merger and waterborne coating leadership

AkzoNobel is reshaping the furniture wood coatings market through strategic consolidation and sustainability-driven innovation. In January 2026, the company finalized a $25 billion merger with Axalta, creating a global leader in industrial wood coatings and performance coatings. It achieved a 14.2% adjusted EBITDA margin in early 2026, supported by its “Sustainability Trio” initiative focused on carbon-neutral coatings for high-rise timber construction. The launch of the Rhythm of Blues™ furniture coatings line introduces anti-fingerprint and scratch-resistant properties tailored for luxury interiors. AkzoNobel’s leadership in waterborne coating technology aligns with stringent global emission regulations, positioning it in the fastest-growing segment. Through its Sikkens Wood Coatings brand, the company has also introduced bio-attributed resin systems, capturing demand from home renovation markets across North America and EMEA.

PPG drives digital wood coating ecosystems and sustainable OEM solutions for global furniture manufacturers

PPG Industries is enhancing its competitive position through digital innovation and sustainable industrial wood coatings. The company reported a 6% increase in adjusted EPS to $1.83 in Q1 2026, driven by demand for high-performance wood topcoats. Following the divestiture of its architectural retail business, PPG has shifted focus toward industrial OEM wood coatings, particularly for modular furniture and e-commerce-driven production models. Its PPG LINQ™ platform enables real-time color matching and viscosity monitoring across manufacturing sites, ensuring consistent finish quality globally. 44% of its sales now come from sustainably advantaged products, including low-emission and HAPs-free coatings. PPG has also secured long-term supply agreements with Asian furniture exporters, leveraging localized production in China to mitigate supply chain risks and logistics volatility.

Axalta accelerates high-speed furniture coatings with UV-curable systems and smart color innovation

Axalta Coating Systems is advancing its role in furniture wood coatings through high-efficiency curing technologies and smart color innovations. In April 2026, the company launched the Zencore™ Cabinet Coating System, a high-solids formulation designed for rapid-turnaround kitchen and bath cabinetry applications. Axalta’s UV-curable and radiation-cured coatings offer up to 50% faster curing times compared to traditional solvent-borne systems, improving manufacturing throughput. The company earned three 2026 Edison Awards™ for AI-powered color technologies, which are being integrated into its wood coatings portfolio for enhanced customization. Prior to its merger with AkzoNobel, Axalta reported $750 million in industrial segment revenue in 2025, driven by strong demand for trend-based color solutions. This focus on speed, efficiency, and innovation strengthens its position in high-performance furniture coatings.

Nippon Paint dominates Asia-Pacific with antimicrobial and zero-VOC wood coating innovations

Nippon Paint Holdings is a dominant force in the furniture wood coatings market. The company benefits from rapid urbanization and residential construction growth across China and Southeast Asia. Its integration of DuluxGroup and Betek Boya has created a robust global supply chain for polyurethane-based wood finishes. Nippon Paint is targeting green building trends with zero-VOC wood stains that meet stringent indoor air quality standards in the US and Europe. Additionally, it has developed antimicrobial coatings for healthcare furniture, achieving a 99.9% reduction in surface bacteria, addressing a segment growing at 5.5% in 2026. This combination of scale, innovation, and sustainability reinforces its leadership in emerging markets.

BASF shifts toward sustainable resins and circular feedstocks in furniture wood coatings value chain

BASF SE is repositioning its presence in the furniture wood coatings market by focusing on high-performance resins and sustainable raw materials. In March 2026, the company divested its coatings subsidiary in India for ₹230.16 crore as part of its “Winning Ways” strategy to streamline operations. BASF projects EBITDA of €6.2 billion to €7.0 billion in 2026, with a strategic emphasis on advanced resins and additives supporting wood coatings applications. It is collaborating with Anodyne Chemistries to develop renewable chemical feedstocks for industrial wood paints, reducing reliance on petroleum-based inputs. The company is also increasing its use of recycled and biomass-balanced materials to align with circular economy goals. This transition positions BASF as a key upstream innovator in sustainable furniture wood coating formulations.

Germany Furniture Wood Coatings Market: Leading VOC Compliance and Smart Manufacturing Innovation

Germany stands as the benchmark in the global furniture wood coatings market, driven by strict VOC compliance regulations, sustainability mandates, and advanced manufacturing technologies aligned with the EU Green Deal 2030 targets. The country’s leadership is reinforced by its strong adoption of waterborne wood coatings, UV-cured finishes, and bio-based coating systems, ensuring both environmental compliance and high-performance durability.

Technological advancements are transforming production efficiency, with the introduction of AI-optimized color matching systems in 2025 that significantly reduce pigment waste in large-scale furniture manufacturing. Product innovation is also accelerating, highlighted by the commercialization of self-healing wood coatings using micro-encapsulated resins that repair minor surface scratches, particularly in high-use kitchen and cabinetry applications.

Strategic acquisitions, including SIC Holding (Oskar Nolte & Klumpp), have strengthened Germany’s capacity in radiation-cured (UV/EB) coatings for flat-pack furniture. Government initiatives such as Green Public Procurement mandates are requiring at least 20% bio-based content in coatings used for public furniture. Additionally, investments in UV-LED curing lines have reduced energy consumption by 35%, enhancing sustainability across woodworking hubs. Waterborne polyurethane (WPU) coatings dominate high-end cabinetry, ensuring compliance with stringent AgBB emission standards.

Vietnam Furniture Wood Coatings Market: Export-Led Growth and Industrial Coating Transformation

Vietnam has emerged as a high-volume export powerhouse in the furniture coatings market, benefiting from global supply chain shifts and increasing foreign direct investment. The rapid expansion of infrastructure, including the construction of over 100,000 housing units by 2025, has significantly increased demand for waterborne wood coatings and cost-effective alkyd topcoats.

Global coating leaders such as AkzoNobel and PPG have established innovation centers in Ho Chi Minh City, enabling just-in-time color customization for export-oriented furniture manufacturers. A major technological shift is underway, with the transition from traditional nitrocellulose (NC) lacquers to UV-curable coatings, driven by stringent zero-VOC import regulations in North America.

Regulatory compliance under the VPA/FLEGT agreement has standardized the use of non-toxic preservatives for furniture exports to the EU. Vietnam also continues to dominate in outdoor furniture, with extensive use of high-solids solvent-borne coatings optimized for tropical humidity resistance. Innovations such as anti-mold additives integrated into coatings are addressing challenges associated with long transit times in humid conditions.

United States Furniture Wood Coatings Market: Premiumization and E-Commerce-Driven Demand

The U.S. furniture wood coatings market is evolving rapidly, driven by the resurgence of domestic manufacturing and a growing preference for premium, low-emission furniture finishes. The expansion of e-commerce, now valued at over $90 billion in furniture sales, has created demand for “ship-safe” coatings that offer enhanced durability and resistance to abrasion during transportation.

Strategic investments, including IKEA’s omnichannel expansion, are accelerating the adoption of scratch-resistant powder coatings on MDF substrates. Technological innovation is evident in the development of Environmentally Adaptive (EA) Hydroplus waterborne coatings, which maintain consistent curing performance across varying climatic conditions.

Regulatory frameworks such as CARB Phase 2 and EPA TSCA Title VI have significantly increased the adoption of formalin-free wood coatings, particularly in residential applications. Product innovation is also focused on sustainability, with the introduction of bio-based coatings containing 20%–30% renewable content, especially in premium segments like nursery furniture.

Key applications include the dominance of conversion varnishes in custom kitchen cabinetry, offering superior resistance to chemicals and moisture, making them ideal for high-end residential projects.

India Furniture Wood Coatings Market: Housing Boom and Shift Toward Organized Retail

India is experiencing rapid growth in the furniture wood coatings market, driven by large-scale housing initiatives and the transition from unorganized carpentry to organized, branded furniture retail ecosystems. Government programs such as Pradhan Mantri Awas Yojana (PMAY) have sanctioned millions of homes, significantly increasing downstream demand for wood finishes and coatings.

Regulatory changes under the National Clean Air Programme (2025) are introducing stricter VOC limits for wood coatings, encouraging the adoption of water-based and low-emission wood finishes. The entry of global furniture brands and expansion of domestic players like Asian Paints have improved accessibility to eco-friendly wood coatings.

Infrastructure development, particularly the growth of co-working spaces in metro cities, is boosting demand for modular furniture coated with high-performance polyurethane (PU) finishes. Tax reforms, including GST reductions on bamboo flooring and joinery, are lowering costs for UV-coated bamboo panels, promoting their adoption in modern interiors.

The hospitality sector is another major driver, with increased use of high-build polyester and PU coatings for durable and aesthetically appealing hotel furniture. These trends collectively position India as a high-growth market with strong long-term potential.

Italy Furniture Wood Coatings Market: Design Innovation and Circular Economy Leadership

Italy continues to lead the premium furniture wood coatings market, driven by its global reputation for design excellence, aesthetic innovation, and sustainable coating solutions. The development of “deep matte” coatings with zero-glare and high fingerprint resistance has become a defining trend in luxury furniture design.

Sustainability is a core focus, with Italian manufacturers pioneering de-inkable and de-coatable coatings, enabling the full recyclability of engineered wood products. Strategic acquisitions, such as Industria Chimica Adriatica (ICA), have centralized R&D efforts in Italy’s renowned furniture districts, strengthening innovation capabilities.

Product advancements include self-leveling wood coatings, which eliminate the need for inter-coat sanding, reducing production time and labor costs. Regulatory initiatives such as the “Made in Italy” Green Certificate ensure strict compliance with chemical safety standards for export furniture.

Key applications include UV-curable clear coats for exotic wood veneers, designed to prevent yellowing and maintain aesthetic integrity under prolonged sunlight exposure in high-end residential projects.

China Furniture Wood Coatings Market: Transition to Water-Based and High-Performance Coatings

China remains the largest producer in the global furniture wood coatings market, undergoing a significant transformation toward water-based and environmentally compliant coating systems. The enforcement of the National Aerosol and VOC Rule (2025/2026) has effectively phased out high-solvent coatings in urban manufacturing clusters, accelerating the shift to waterborne acrylics and UV-curable dispersions.

The country’s massive manufacturing scale continues to drive consumption, supported by the production of over a million furniture units annually. Technological advancements, including the deployment of UV-LED curing systems, have reduced energy consumption by up to 40%, improving operational efficiency and sustainability.

Investments by domestic players such as Carpoly and Bauhinia are focusing on bio-based resin development, reducing reliance on petrochemical-derived materials. The market is also witnessing increased demand for flame-retardant wood coatings, particularly in public infrastructure and commercial spaces, driven by stricter fire safety regulations.

Innovations such as “warm-touch” coatings are gaining popularity, enabling engineered wood panels to replicate the tactile feel of natural wood, enhancing consumer appeal while maintaining cost efficiency.

Furniture Wood Coatings Market Report Scope

Furniture Wood Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2032)

|

$7.9 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Technology (Solvent-borne, Water-borne, Radiation-Cured, Powder Coatings), By Resin Type (Polyurethane, 1K Polyurethane, 2K Polyurethane, Nitrocellulose, Acrylics, Polyester, Acid-Curing, Epoxy, Bio-based), By Product Type (Stains and Dyes, Varnishes and Lacquers, Shellacs, Paints and Enamels, Primers, Fillers and Sealers, Waxes and Oils), By Furniture Application (Residential Furniture, Commercial and Office Furniture, Outdoor and Garden Furniture, Institutional Furniture, Luxury and High-end Custom Furniture), By Substrate Type (Solid Wood, Wood Composites), By Sales Channel (Distributors and Wholesalers, Retail Sales, Online)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, AkzoNobel N.V., PPG Industries, Inc., RPM International Inc., Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun A/S, Asian Paints Limited, Hempel A/S, Sika AG, Teknos Group, Sirca S.p.A., Benjamin Moore & Co., IVM Chemicals s.r.l.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Furniture Wood Coatings Market Segmentation

By Technology

- Solvent-borne

- Water-borne

- Radiation-Cured

- Powder Coatings

By Resin Type

- Polyurethane

- 1K Polyurethane

- 2K Polyurethane

- Nitrocellulose

- Acrylics

- Polyester

- Acid-Curing

- Epoxy

- Bio-based

By Product Type

- Stains and Dyes

- Varnishes and Lacquers

- Shellacs

- Paints and Enamels

- Primers, Fillers and Sealers

- Waxes and Oils

By Furniture Application

- Residential Furniture

- Commercial and Office Furniture

- Outdoor and Garden Furniture

- Institutional Furniture

- Luxury and High-end Custom Furniture

By Substrate Type

- Solid Wood

- Wood Composites

By Sales Channel

- Distributors and Wholesalers

- Retail Sales

- Online

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Furniture Wood Coatings Market

- The Sherwin-Williams Company

- AkzoNobel N.V.

- PPG Industries, Inc.

- RPM International Inc.

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun A/S

- Asian Paints Limited

- Hempel A/S

- Sika AG

- Teknos Group

- Sirca S.p.A.

- Benjamin Moore & Co.

- IVM Chemicals s.r.l.

*- List not Exhaustive