Gamma Linolenic Acid Market to Reach $4.6 Billion by 2034 at 9.1% CAGR Fueled by Molecular Farming and High-Potency Nutraceutical Demand

The Gamma Linolenic Acid (GLA) Market is projected to expand from $2.1 billion in 2025 to $4.6 billion by 2034, registering a robust CAGR of 9.1%. Market acceleration is driven by rising demand for plant-based anti-inflammatory nutraceuticals, high-potency borage and evening primrose oils, functional pet nutrition, and dermatology-focused formulations. Increasing consumer preference for clean-label, non-GMO specialty oils and clinically validated omega fatty acid blends is reshaping competitive dynamics across the dietary supplements and functional ingredients industry.

In May 2025, Bioriginal Food & Science Corp. introduced an industry-first cold-pressed, non-GMO borage oil containing 25% naturally occurring GLA. Developed through a proprietary selective breeding program, the product positions Bioriginal at the premium end of the high-potency GLA segment. In early 2025, the company filed global patents protecting its non-GMO high-yield borage cultivars, strengthening intellectual property control over clean-label GLA sources. In November 2025, Bioriginal restructured operations under the Bioriginal Group of Companies, consolidating six international entities to streamline global distribution of specialty oils into food, nutraceutical, and animal nutrition markets. These developments underscore consolidation and premiumization within the plant-derived GLA supply chain.

Biotechnology-driven molecular farming is introducing structural shifts in raw material sourcing. In late 2025, Moolec Science completed its U.S. cultivation campaign across 1,100 acres of engineered safflower, reporting a 57% year-over-year yield increase compared to 2024. In February 2026, Moolec announced that commercial-scale crushing of its GLASO1 safflower achieved a 45% GLA concentration, nearly doubling the concentration typically found in conventional borage oil while maintaining compatibility with standard agricultural infrastructure. In January 2026, the company secured Nasdaq compliance through a financial restructuring plan, stabilizing its commercialization roadmap. These milestones indicate a transition from pilot-stage molecular agriculture to scalable, high-concentration GLA production platforms.

Application expansion into new verticals is reinforcing long-term demand. In 2025, research findings highlighted by the New Hope Network confirmed that GLA supplementation bypasses delta-6-desaturase metabolic bottlenecks, enhancing anti-inflammatory hormone production when combined with Omega-3 fatty acids. This clinical validation accelerated launches of dual GLA-Omega-3 formulations targeting skin health, hormonal balance, and chronic inflammation management. The same year, manufacturers expanded into pet nutrition, introducing high-concentration GLA blends for allergy management and joint support in companion animals, opening a fast-growing adjacent revenue stream within veterinary nutraceuticals.

Regional manufacturing diversification is strengthening supply resilience. Throughout 2024 and 2025, Indian producers such as Aromex Industry and AOS Products Pvt. Ltd. scaled exports of refined and organic borage seed oil to Europe and North America, particularly for anti-aging and dermaceutical formulations. In 2024, Veramaris received Canadian regulatory approval for its algal oil platform, reinforcing confidence in single-cell lipid production technologies that may serve as future high-purity GLA production models.

Regulatory scrutiny intensified in 2025 when the European Food Safety Authority reported that only 12% of nutraceutical health claim applications were approved. This environment is compelling GLA producers to invest in controlled clinical studies to substantiate efficacy claims related to dermatology, inflammatory disorders, and women’s health.

The Gamma Linolenic Acid Market outlook reflects convergence of selective breeding innovation, molecular farming breakthroughs, intellectual property consolidation, clinical validation of omega synergies, and expansion into pet nutrition and cosmetic formulations. Competitive differentiation is increasingly defined by GLA concentration levels, non-GMO positioning, regulatory compliance in health claims, and scalable agricultural biotechnology platforms.

Market Size Outlook, 2021-2034.png)

Gamma Linolenic Acid (GLA) Market Trends and High-Impact Growth Opportunities

Precision Fermentation and Controlled Agriculture Are Redefining GLA Supply Economics

The global Gamma Linolenic Acid market is undergoing a structural sourcing transition as producers seek to mitigate agricultural volatility, yield inconsistency, and purity constraints associated with conventional botanical oils. Traditional feedstocks such as borage oil, with typical GLA concentrations of 20 to 25%, and evening primrose oil, averaging 8 to 10%, remain vulnerable to climate variability, crop disease, and regional farming economics. As a result, precision fermentation and bio-engineered oilseed platforms are emerging as strategically superior alternatives for year-round, high-purity GLA production.

By early 2025, advances in genome editing and metabolic pathway optimization had enabled oleaginous microorganisms to produce GLA-rich triglycerides at commercially viable yields. These developments are shifting GLA from an agriculturally constrained specialty lipid into a scalable bio-manufactured ingredient suitable for pharmaceutical, medical nutrition, and premium nutraceutical applications. Parallel to microbial innovation, plant-based sourcing is also evolving toward higher concentration and identity-preserved models. In May 2025, Bioriginal Food & Science Corp. introduced a non-GMO borage oil standardized at 25% GLA, targeting clean-label formulations that prioritize minimal processing over chemical concentration.

Supply chain control is becoming a decisive competitive advantage. In July 2024, Moolec Science SA secured a multi-year offtake agreement for its high-GLA safflower oil, establishing a closed-loop, traceable production system for the U.S. market. These models address long-standing supply fragility in the GLA market and are increasingly favored by multinational consumer health and nutrition brands seeking consistency, regulatory transparency, and ESG-aligned sourcing.

Clinical Research Is Expanding GLA from Anti-Inflammatory Use to Systemic Therapeutics

Clinical positioning of Gamma Linolenic Acid is expanding rapidly beyond dermatological and joint health applications into systemic inflammation, metabolic dysfunction, and cellular protection pathways. By late 2025, research focus had shifted toward inflammation resolution rather than simple suppression, with multiple studies demonstrating GLA’s ability to restore desaturase enzyme activity and rebalance inflammatory cytokine signaling. These mechanisms are particularly relevant in the management of metabolic dysfunction-associated steatotic liver disease and broader metabolic syndrome indications, where chronic low-grade inflammation is a primary driver of disease progression.

At the same time, pharmaceutical-grade GLA is attracting attention for its radioprotective potential. Preclinical data updated in 2024 demonstrated a substantial improvement in survival outcomes in radiation-exposed models, driven by immune modulation and intestinal barrier recovery. This body of evidence is positioning high-purity GLA as a potential adjunct ingredient in oncology support therapies and nuclear medicine recovery protocols. As regulatory agencies increasingly favor bioactive lipids with strong mechanistic validation, GLA’s expanding clinical evidence base is strengthening its credibility within both pharmaceutical development pipelines and regulated medical nutrition.

Advanced Skincare Formulations Are Unlocking Premium GLA Demand

The global shift toward barrier repair and skin microbiome health is creating a high-value opportunity for Gamma Linolenic Acid in advanced topical skincare. Conventional GLA oils face challenges related to oxidative instability and greasy sensory profiles, limiting formulation flexibility. In response, cosmetic and dermatological brands are increasingly adopting engineered delivery systems such as liposomal encapsulation to improve stability, skin penetration, and controlled release.

By January 2025, liposomal actives had become one of the most widely adopted formulation technologies in premium cosmeceuticals, enabling GLA to be incorporated into lightweight serums and barrier-repair creams with clinically measurable outcomes. Digital-first beauty platforms now account for approximately 43% of GLA-containing product sales, with brands leveraging instrumental metrics such as transepidermal water loss reduction to substantiate efficacy claims. GLA-enriched ceramide-support formulations are gaining strong traction within the global skincare industry, particularly across Asia-Pacific markets where consumer sophistication and demand for science-backed actives are highest.

Clinical Nutrition and Critical Care Applications Represent a High-Margin Growth Frontier

Gamma Linolenic Acid’s metabolic conversion into dihomo-gamma-linolenic acid and anti-inflammatory prostaglandins positions it as a strategic bioactive lipid for clinical nutrition. The enteral and parenteral nutrition segment is increasingly shifting toward omega-fortified and condition-specific formulations, particularly in intensive care and post-surgical recovery settings. Global clinical nutrition demand continues to expand, with hospitals prioritizing formulations that can reduce inflammation-related complications and shorten recovery timelines.

Leading medical nutrition players such as Nestlé and Abbott are actively evaluating GLA integration into specialized feeding protocols aimed at reducing ventilator-associated infections, sepsis risk, and systemic inflammatory burden in ICU patients. Clinical observations from mid-2025 indicate that GLA-containing modular nutrition solutions can reduce average hospital stays by approximately 30% in post-operative cohorts. This disease-specific positioning creates a compelling opportunity for suppliers of pharmaceutical-grade Gamma Linolenic Acid to move beyond commodity nutraceutical markets and embed GLA into high-value, regulated clinical care pathways.

Gamma Linolenic Acid Market Share and Segmentation Insights

Evening Primrose Oil Leads Gamma Linolenic Acid Supply Through Established Nutraceutical Recognition

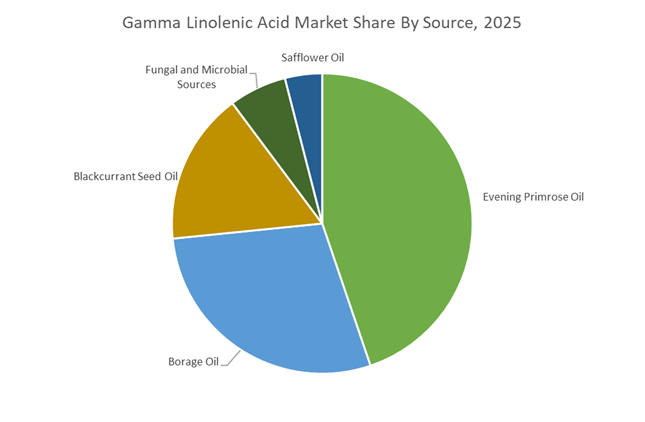

Evening Primrose Oil accounted for 44.80% of the Gamma Linolenic Acid Market share in 2025, positioning it as the most widely used natural source of GLA in global nutraceutical and wellness markets. Evening primrose oil has maintained its leadership due to decades of consumer awareness, extensive clinical research, and well-developed extraction supply chains across North America and Europe. The oil is widely recognized for its naturally high gamma linolenic acid concentration, which supports applications in women’s health supplements, skin health formulations, and anti-inflammatory nutraceutical products. Health practitioners and supplement manufacturers continue to favor evening primrose oil because of its established role in supporting premenstrual syndrome (PMS) management, menopause symptom relief, and dermatological wellness. In 2025, the supply chain for evening primrose oil is increasingly influenced by certified sustainable cultivation initiatives. Since evening primrose is frequently grown by smallholder farmers or harvested from semi-wild cultivation environments, major nutraceutical brands are implementing traceability systems, fair labor certifications, and biodiversity protection programs. These sustainability certifications allow manufacturers to position ethically sourced evening primrose oil at premium price points within the competitive gamma linolenic acid supplement market.

Dietary Supplements Drive the Largest Consumption of Gamma Linolenic Acid in Global Wellness Markets

Dietary Supplements represented 58.70% of the Gamma Linolenic Acid Market share in 2025, making it the dominant application segment within the global GLA industry. Gamma linolenic acid is widely consumed as a nutritional supplement ingredient, valued for its ability to support skin health, hormonal balance, immune function, and inflammation management. Consumers commonly obtain GLA through softgel capsules and oil-based supplements derived from evening primrose, borage oil, and blackcurrant seed oil, which are incorporated into daily wellness routines. The popularity of GLA supplements continues to grow alongside increasing consumer interest in preventive healthcare, natural anti-inflammatory compounds, and plant-derived omega fatty acids. In 2025, the dietary supplement segment is experiencing transformation through the rise of personalized nutrition platforms and data-driven wellness programs. Supplement companies are introducing customized GLA formulations tailored to individual health objectives, lifestyle factors, and genetic predispositions, supported by AI-driven nutritional assessments. These platforms recommend specific GLA sources, optimized dosage levels, and complementary nutrients, creating a high-value personalized segment within the broader gamma linolenic acid supplement market.

Competitive Landscape in Gamma Linolenic Acid Market

Bioriginal Strengthens Seed-to-Shelf Integration in High GLA Oils

Bioriginal Food & Science Corp., a subsidiary of Cooke Inc., is the most vertically integrated supplier in the global gamma linolenic acid market, controlling sourcing, extraction, refinement, and distribution. In November 2025, the company consolidated its North American, EMEA, and Asian operations under the Bioriginal Group of Companies structure to streamline global GLA supply chains. Its High GLA Borage Oil series uses specialized extraction methods to achieve naturally concentrated GLA levels optimized for skin and joint health applications. Late 2025 acquisitions of European oilseed processors secured proprietary access to borage and evening primrose seed supply amid evolving agricultural trade policies. This seed-to-shelf model enables batch-to-batch consistency, improved oxidative stability, and reliable supply for global nutraceutical and functional food manufacturers.

dsm-firmenich Focuses on Clinically Backed Medical Nutrition Applications

dsm-firmenich remains a benchmark supplier of high-purity, science-backed GLA solutions for medical nutrition and clean beauty formulations. Its life’s™ GLA 10 and 25 N-6 oils are stabilized with targeted antioxidant systems to preserve fatty acid integrity in complex formulations. In February 2026, the company confirmed divestment of its Animal Nutrition & Health business, reinforcing its strategic concentration on Human Nutrition & Care. Achieving EcoVadis Platinum and CDP Double A ratings in early 2026 strengthens its appeal among ESG-focused nutraceutical and skincare brands. The company’s purpose-led science framework emphasizes clinical efficacy in menopause management, PMS support, and anti-aging dermatology, positioning GLA as a premium bioactive lipid rather than a commodity oil.

BASF Expands Specialty Lipid Capacity Through Integrated Verbund Strategy

BASF SE leverages its global Nutrition & Care infrastructure to supply pharmaceutical-grade and nutraceutical-grade gamma linolenic acid ingredients. In February 2026, BASF projected earnings growth within its Nutrition & Care segment, supported by specialty fatty acids and bioactive lipid demand. The ramp-up of its Zhanjiang Verbund site in early 2026 strengthens access to the rapidly expanding Asian nutraceutical and functional food markets. A cost optimization program launched in 2026 raised annual savings targets to €2.3 billion, reinforcing price competitiveness in the global specialty lipids market. Under its Winning Ways strategy, BASF continues investing in research and formulation science to enhance bioavailability, stability, and performance of GLA in dietary supplements and fortified products.

Croda Advances Beauty Actives with Carbon Transparency Tools

Croda International Plc remains a leading innovator in beauty actives and dermatological lipid delivery systems incorporating gamma linolenic acid. In April 2026, the company is set to introduce a major Beauty Actives innovation platform that includes advanced encapsulation and delivery technologies for sensitive polyunsaturated lipids. Croda reported a 6.6% sales increase in 2025 and targets an operating margin exceeding 20% by 2028 through growth in Life Sciences and Consumer Care. Its Measure It to Master It carbon footprinting tool, launched in late 2025, allows customers to quantify CO2 impact at the ingredient level. The company prioritizes PEG-free, bio-based, and sustainable formulations that align with clean beauty and next-generation skincare demands.

ConnOils Expands Traceable and Powdered GLA Solutions for Functional Foods

ConnOils LLC is a leading North American supplier of traceable botanical oils rich in gamma linolenic acid, including borage, evening primrose, blackcurrant seed, and hemp seed oils. The company serves health and wellness brands requiring USDA Organic, Non-GMO, and identity-preserved sourcing certifications. In late 2025, ConnOils expanded strategic alliances to broaden its distribution network across Asia-Pacific markets experiencing rising nutraceutical consumption. During 2025 and 2026, the company introduced powdered GLA formulations tailored for fortified functional foods and beverage applications, improving formulation flexibility and oxidative stability. Positioned as a purpose-led partner, ConnOils offers customized oil blending and private label capabilities, supporting boutique supplement and skincare brands seeking high-quality, traceable GLA ingredients.

Canada: Clean-Label Leadership and Export-Grade Standardization

Canada has consolidated its position as a premium origin market for gamma linolenic acid through clean-label innovation and vertically integrated processing. In May 2025, Bioriginal Food & Science Corp. launched a non-GMO borage oil with 25% naturally occurring GLA, the highest concentration currently available in a clean-label format. This product is explicitly positioned for high-end human nutrition, clinical dietary supplements, and premium pet nutrition, where traceability and natural potency increasingly influence procurement decisions. The launch reflects a broader shift among North American buyers toward minimally processed, solvent-free specialty lipids with documented fatty acid profiles.

Infrastructure investments have reinforced this positioning. Following the late-2024 acquisition of The Factory and Cana Corporation, Bioriginal integrated advanced extraction, blending, and encapsulation capabilities across North America in 2025, shortening lead times for evening primrose and borage oil derivatives. At the policy level, the Canadian government updated its phytosanitary export support framework to align specialty oilseed shipments with European Food Safety Authority transparency requirements. This regulatory alignment has materially reduced friction for EU-bound GLA oils, strengthening Canada’s role as a compliant, export-oriented supply base.

United States: Identity-Preserved Supply and Women’s Health Demand

The United States GLA market is being shaped by controlled agricultural sourcing and expanding clinical adoption in women’s health. In 2025–2026, Moolec Science SA executed a three-year offtake agreement with a global consumer packaged goods company for GLASO™, its high-concentration GLA safflower oil. Commercial deliveries are underway, supported by a fully identity-preserved crop and processing system that addresses traceability, allergen control, and formulation consistency requirements for large-scale nutrition brands.

Regulatory and healthcare dynamics are reinforcing demand. U.S. manufacturers have increased sourcing of specialty lipids from India and Switzerland in response to shifting trade patterns and evolving environmental oversight, driving a 10–12% increase in the use of pharmaceutical-grade borage oil in dermatological formulations. In parallel, the 2025 National Wellness Initiative has driven wider clinical recommendations for GLA-rich supplements to support menopausal symptom management and hormonal balance. This has translated into a marked acceleration in softgel and encapsulated oil production pipelines planned for 2026.

China: Domestic Value Chain Localization and Pharmaceutical R&D

China’s gamma linolenic acid industry is undergoing rapid localization under a broader self-reliance strategy. The government’s 2025–2026 petrochemical and agricultural work plans incentivize the full domestic GLA value chain, from crop cultivation in northern provinces to high-purity extraction and refining. This policy direction is reducing dependence on North American imports while building domestic capacity tailored to pharmaceutical and cosmeceutical standards.

R&D activity is a critical differentiator. In late 2025, Chinese pharmaceutical agencies reported increased investment in lipid nano-carrier technologies that utilize GLA as a functional excipient to enhance bioavailability in anti-inflammatory and arthritis therapies. On the agricultural side, commercial-scale cultivation of Borago officinalis in high-altitude regions has achieved stable oil profiles averaging 22% GLA, meeting the quality thresholds demanded by China’s fast-growing premium skincare and cosmeceutical manufacturers.

India: Policy-Driven Extraction Capacity and Ayurvedic Standardization

India is emerging as a cost-competitive and innovation-oriented node in the global GLA landscape. Under the Union Budget 2025–26, the government extended the Production Linked Incentive scheme to specialty lipids, catalyzing an estimated INR 500 crore in private investment for high-purity GLA extraction facilities, particularly in Maharashtra. These projects are designed to serve both export nutraceutical markets and domestic pharmaceutical applications.

Market differentiation is also occurring at the product level. Indian Ayurvedic manufacturers increasingly standardized formulations with GLA-rich borage oil during 2025 to appeal to Western buyers seeking evidence-backed “Modern Ayurveda.” This convergence of traditional medicine with quantified lipid profiles is expanding India’s relevance beyond commodity oils into branded, standardized wellness ingredients with global reach.

Germany: Premium Cosmetics Integration and Carbon-Neutral Positioning

Germany’s GLA industry footprint is defined by downstream integration into premium cosmetics and strict sustainability compliance. In 2025, leading German personal care players incorporated GLA into approximately 28% of new high-end skincare launches, highlighting barrier-repair and anti-pollution benefits for urban consumers. This level of formulation penetration reflects strong confidence in GLA as a multifunctional active lipid rather than a niche supplement ingredient.

Operational sustainability is reinforcing market access. By January 2026, major German lipid processors completed transitions to 100% renewable electricity, enabling the commercialization of carbon-neutral GLA aligned with EU Scope 3 reporting expectations. Concurrently, Germany implemented the Critical Medicines Act guidelines, requiring full supply-chain mapping for GLA derivatives used in clinical nutrition. This transparency mandate favors suppliers with documented agricultural origins and controlled processing, further elevating entry barriers for lower-compliance imports.

Comparative Snapshot: Country-Level Positioning in the Gamma Linolenic Acid Industry

Gamma Linolenic Acid (GLA) Market County Level Snapshot

|

Country

|

Strategic Focus

|

Implications for GLA Supply

|

|

Canada

|

Clean-label potency and export compliance

|

Premium, EU-aligned borage and primrose oils

|

|

United States

|

Identity-preserved crops and women’s health

|

Scalable, traceable GLA for nutraceuticals

|

|

China

|

Value chain localization and pharma R&D

|

Domestic substitution and drug-delivery applications

|

|

India

|

PLI-backed extraction and Ayurvedic exports

|

Cost-efficient, standardized GLA for global markets

|

|

Germany

|

Premium cosmetics and carbon neutrality

|

High-compliance, sustainability-led GLA demand

|

Gamma Linolenic Acid (GLA) Market Report Scope

Gamma Linolenic Acid (GLA) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.1 Billion

|

|

Market Size (2034)

|

$4.6 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Source (Evening Primrose Oil, Borage Oil, Blackcurrant Seed Oil, Fungal and Microbial Sources, Safflower Oil), By Form (Liquid Oil, Powdered Form, Softgels and Capsules), By Concentration (Standard Concentration, High Concentration, Pharmaceutical Grade), By Application (Dietary Supplements, Cosmeceuticals, Pharmaceuticals, Functional Foods, Animal Nutrition)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bioriginal Food and Science Corp., BASF SE, Moolec Science SA, DSM-Firmenich, Cargill, Incorporated, Sudarshan Chemical Industries Limited, ConnOils LLC, AOS Products Pvt. Ltd., Jinan Shengquan Group, Sanmark Corp., Hebron S.A., Polaris Nutritional Lipids, ExtractionTek Solutions, Aromex Industry, K.K. Enterprise

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Gamma Linolenic Acid Market Segmentation

By Source

- Evening Primrose Oil

- Borage Oil

- Blackcurrant Seed Oil

- Fungal and Microbial Sources

- Safflower Oil

By Form

- Liquid Oil

- Powdered Form

- Softgels and Capsules

By Concentration

- Standard Concentration

- High Concentration

- Pharmaceutical Grade

By Application

- Dietary Supplements

- Cosmeceuticals

- Pharmaceuticals

- Functional Foods

- Animal Nutrition

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Gamma Linolenic Acid Industry

- Bioriginal Food and Science Corp.

- BASF SE

- Moolec Science SA

- DSM-Firmenich

- Cargill, Incorporated

- Sudarshan Chemical Industries Limited

- ConnOils LLC

- AOS Products Pvt. Ltd.

- Jinan Shengquan Group

- Sanmark Corp.

- Hebron S.A.

- Polaris Nutritional Lipids

- ExtractionTek Solutions

- Aromex Industry

- K.K. Enterprise

*- List not Exhaustive