Gas Barrier Membranes Market Growth Driven by Emission Control Regulations, Data Center Infrastructure, and High-Performance Multilayer Technologies

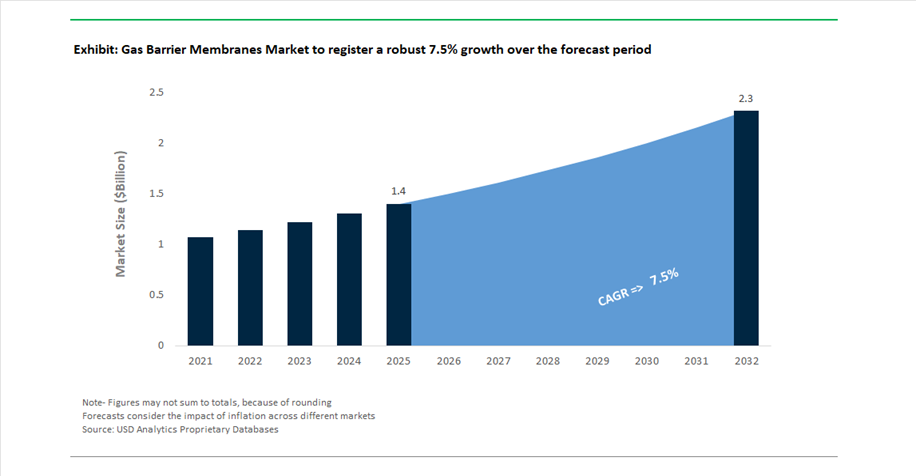

The global Gas Barrier Membranes Market was valued at USD 1.4 billion in 2025 and is projected to grow at a CAGR of 7.5% between 2025 and 2032, reaching USD 2.3 billion by 2032. This strong growth reflects increasing demand for advanced gas containment, environmental protection, and high-spec building envelope solutions across construction, energy, packaging, and industrial applications.

Gas barrier membranes are engineered to provide ultra-low permeability against gases such as methane, carbon dioxide, radon, and oxygen, making them critical in applications ranging from foundation protection and landfill containment to food packaging and semiconductor environments. A major structural driver is the tightening of environmental regulations, particularly those targeting greenhouse gas emissions and hazardous gas containment. The updated Global Warming Potential (GWP) standards introduced by regulatory authorities in 2025 have accelerated the adoption of high-performance membranes capable of meeting stricter emission reporting and containment requirements.

Another key growth driver is the expansion of data center infrastructure and high-spec commercial construction, where gas barrier membranes are increasingly used to protect sensitive equipment from moisture ingress and ground gases. Additionally, the rising focus on sustainable construction and green building certifications is pushing developers to adopt advanced membrane systems that reduce environmental impact while ensuring long-term structural integrity.

Technological advancements are also reshaping the market. The development of multilayer membranes with aluminum cores and high-purity polymer layers is enhancing barrier performance, while liquid-applied and thin-film barrier technologies are enabling greater flexibility in installation and integration with existing manufacturing processes.

Regulatory Push, AI-Driven Quality Control, and Multilayer Membrane Innovation Reshape Market Dynamics

The gas barrier membranes market is undergoing a structural transformation driven by regulatory enforcement, digitalization, and advanced material innovation. In February 2026, Sika AG launched its “Fast Forward” strategy, focusing on digitalization and automation of membrane production. This initiative aims to enhance efficiency while accelerating the development of high-spec membranes for data centers and sustainable infrastructure projects.

Product innovation is increasingly targeting multi-gas protection. In January 2026, Cordek introduced its Tri-Gas Membrane, a multilayer system with an aluminum core designed to provide simultaneous protection against methane, carbon dioxide, and radon, meeting stringent UK building codes.

Sustainability is becoming a competitive differentiator. In December 2024, A. Proctor Group achieved its carbon reduction targets ahead of schedule by transitioning toward solar-powered manufacturing and localized supply chains, reducing the embedded carbon footprint of its membrane products.

Technical support and compliance capabilities are expanding alongside regulatory complexity. In October 2025, Visqueen enhanced its technical services in Europe, supporting developers in meeting increasingly complex ground gas protection standards and certification requirements.

Advanced manufacturing and material innovation are also reshaping the market. In January 2026, Borealis invested in high-purity polypropylene production, ensuring a stable supply of critical materials used in multilayer gas barrier membranes.

Digital transformation is emerging as a key differentiator. In January 2026, leading manufacturers including Nitto and Sika AG implemented AI-driven “Digital Twin” quality control systems, enabling real-time detection of microscopic defects such as pinholes, ensuring zero-defect certification for critical applications.

Cross-industry innovation is also influencing the market. In September 2025, Fujifilm introduced the LuXtreme Pro LED curing system, enabling the development of thin-film, liquid-applied gas barrier coatings with significantly lower energy consumption.

Additionally, developments in adjacent industries are creating indirect growth opportunities. The March 2026 acquisition of Hi-Tech Inks by Siegwerk is strengthening the development of barrier coatings and inks for flexible packaging, contributing to the broader evolution of gas barrier technologies.

Finally, compliance with stringent safety standards is expanding application scope. In May 2025, Hollingsworth & Vose achieved KTW certification for its membrane materials, validating their use in drinking water and food-contact applications, one of the most demanding regulatory environments globally.

Membrane-Based CO₂ Removal Replacing Amine Scrubbing in Natural Gas Processing

The gas barrier membranes industry is experiencing a structural shift as membrane-based gas separation technologies increasingly replace conventional amine scrubbing systems in natural gas processing, particularly in offshore and remote environments. Traditional amine systems require large infrastructure footprints and energy-intensive solvent regeneration processes, making them less suitable for space-constrained installations such as floating production storage and offloading vessels. In contrast, membrane systems offer up to 50% reduction in equipment footprint, enabling more efficient utilization of platform space. From a performance perspective, modern cellulose acetate and polyimide membranes are achieving methane recovery rates exceeding 95% while reducing carbon dioxide concentrations from approximately 20% to below 2%, meeting pipeline-grade specifications. Energy efficiency is another critical advantage, with membrane systems reducing overall energy consumption by approximately 30% due to their reliance on pressure differentials rather than thermal regeneration. Additionally, maintenance requirements are significantly lower, with membrane modules designed for service lifespans of three to five years even in aggressive sour gas environments, eliminating issues related to corrosion and solvent degradation commonly associated with amine systems. These combined benefits are positioning gas separation membranes as the preferred technology for next-generation gas processing infrastructure focused on efficiency, modularity, and reduced operational complexity.

Palladium Alloy Membranes Enabling Ultra-High-Purity Hydrogen for Fuel Cell Applications

The rapid expansion of the hydrogen economy is driving demand for advanced gas barrier membranes capable of delivering ultra-high-purity hydrogen required for fuel cell technologies. Palladium alloy membranes are emerging as the industry benchmark for final-stage hydrogen purification due to their unique ability to selectively permeate hydrogen while blocking all other gases. These membranes achieve purity levels exceeding 99.999%, meeting stringent fuel cell standards and ensuring catalyst protection in hydrogen-powered vehicles and energy systems. Technological advancements have improved the operational efficiency of palladium-based membranes, with optimized thin-film designs enabling operation at temperatures between 300°C and 450°C, reducing energy input requirements compared to earlier systems. Durability has also improved through alloying with elements such as silver and copper, increasing resistance to sulfur and carbon poisoning by approximately 25%, which is critical for long-term performance in industrial environments. Additionally, modern palladium membrane systems are achieving high flux densities, allowing compact and modular purification units to be deployed at hydrogen refueling stations and decentralized production sites. These innovations are positioning palladium alloy membranes as a key enabling technology in the scaling of clean hydrogen infrastructure.

US DOE Carbon Capture Initiatives Driving Adoption of Polymeric Gas Barrier Membranes

The United States Department of Energy’s focus on decarbonizing hard-to-abate industrial sectors is creating a significant growth opportunity for polymeric gas barrier membranes in carbon capture applications. Through funding programs under the Office of Clean Energy Demonstrations, the DOE is supporting large-scale pilot projects aimed at capturing at least 95% of carbon dioxide emissions from industrial flue gas streams, particularly in cement and steel manufacturing. These initiatives are driving the development of high-performance membranes capable of operating under challenging conditions, including high particulate loads and exposure to sulfur and nitrogen oxides. In cement sector applications, facilitated transport membranes are being engineered to achieve carbon capture costs below 40 dollars per ton, improving the economic viability of decarbonization strategies. For steel manufacturing, membrane systems are being optimized to operate at low pressure differentials, targeting a 20% reduction in parasitic energy consumption compared to traditional carbon capture technologies. Pilot projects are rapidly scaling from laboratory units to integrated systems capable of processing over 500 tons of carbon dioxide per day, indicating strong progress toward commercial deployment within the 2027 to 2030 timeframe. These developments are positioning gas barrier membranes as a critical component in industrial carbon capture and emissions reduction strategies.

China’s Nitrogen Rejection Mandates Driving Membrane Adoption in Low-Calorific Gas Fields

China’s National Energy Administration is creating a strong growth opportunity for gas separation membranes through mandates requiring nitrogen rejection in natural gas fields with high nitrogen content. New regulations stipulate that fields with nitrogen concentrations exceeding 10% must implement on-site separation technologies to upgrade gas quality to meet national pipeline standards. Membrane-based nitrogen rejection units are emerging as the preferred solution due to their modular design and suitability for deployment in remote and geographically challenging regions. These systems enable operators to increase the calorific value of natural gas by up to 15%, ensuring compatibility with high-pressure transmission networks and urban distribution systems. In addition to performance benefits, membrane systems contribute to environmental sustainability by capturing methane from nitrogen-rich tail gas streams, reducing greenhouse gas emissions associated with venting. The Chinese government is also supporting domestic manufacturing of membrane technologies through tax incentives and industrial policies aimed at localizing production capacity. These combined regulatory and economic drivers are positioning gas barrier membranes as a key technology in the development of unconventional gas resources and energy infrastructure in China.

Gas Barrier Membranes Market Share 2025: CCS Applications and EPC Contracting Drive Expansion

Function Insights: Carbon Capture and Sequestration (CCS) Leads Amid Decarbonization Push

The carbon capture and sequestration (CCS) segment dominates the gas barrier membranes market with a 28% market share in 2025, fueled by the accelerating global transition toward decarbonization and carbon management technologies. Government incentives such as the US 45Q tax credit and the EU Innovation Fund are significantly boosting investments in membrane-based CO₂ separation systems across industries including power generation, cement, steel, and hydrogen production. Advanced polymer membranes and facilitated transport membranes are gaining traction due to their ability to efficiently separate CO₂ from flue gas, natural gas, and biogas streams. A key advantage of membrane-based CCS technology is its lower energy footprint compared to conventional amine scrubbing, reducing parasitic energy loads by 30–50% and improving overall process economics. As industries face increasing pressure to reduce carbon emissions, CCS applications will remain the primary growth engine in the gas separation membranes market.

Sales Channel Insights: Project-Based Contracting Dominates with Integrated System Delivery

The project-based contracting and engineering firms segment accounts for the largest 55% share in the gas barrier membranes market in 2025, reflecting the highly specialized and system-driven nature of membrane deployment. Gas separation membranes are typically delivered as part of fully engineered, turnkey solutions, including skid-mounted units, pressure vessels, and modular rack systems, designed and installed by EPC (Engineering, Procurement, and Construction) firms. These solutions are tailored for complex applications such as refineries, biogas upgrading facilities, and large-scale CCS hubs, where off-the-shelf components are insufficient. Additionally, project-based contracts include strict performance guarantees, covering parameters such as gas permeance, selectivity, and operational lifespan (typically 5–10 years), ensuring reliability under real-world feed gas conditions. This integrated approach reduces operational risk and enhances system efficiency, making EPC-led contracting the dominant channel in the global gas barrier membranes market.

Gas Barrier Membranes Market Competitive Landscape: Decarbonization, Hydrogen Economy, and High-Selectivity Membrane Technologies Driving Competition

The gas barrier membranes market is highly competitive, driven by rising demand for biogas upgrading, hydrogen purification, and carbon capture technologies. Key players are advancing high-selectivity polymer membranes, modular systems, and digital monitoring solutions to support industrial decarbonization and energy transition initiatives.

Air Liquide leads membrane-based gas purification with integrated service models and biomethane dominance

Air Liquide is a dominant force in the gas barrier membranes market, particularly in high-purity gas separation and biogas upgrading. The company operates over 500 membrane-based purification units globally, leading the biomethane conversion segment with methane recovery rates of up to 95% using its MEDAL™ membranes. Under its ADVANCE strategy, Air Liquide is targeting a 33% reduction in Scope 1 and 2 CO₂ emissions by 2035 through next-generation polyimide hollow-fiber membranes. The commissioning of a new high-capacity membrane manufacturing facility supports growing demand in China’s industrial decarbonization market. Its vertical integration across the gas value chain enables a “Membrane-as-a-Service” model with digital monitoring and predictive maintenance for remote operations. This combination of scale, innovation, and service integration reinforces its leadership in industrial gas membranes.

Evonik advances high-selectivity membranes and circular polymer innovation for energy transition

Evonik Industries is strengthening its position in the gas barrier membranes market through high-performance polyimide membrane technologies and sustainability initiatives. The company has commercialized SEPURAN® Green and SEPURAN® Noble membranes, achieving up to 99% purity in biomethane and helium recovery applications. Its SEPURAN® N₂ membranes have been optimized to operate at 20% lower pressure, significantly reducing energy consumption in offshore oil and gas platforms. Evonik is expanding into hydrogen mobility by supplying gas barrier membranes for fuel cell humidification and oxygen enrichment in automotive OEM applications. The company is also developing bio-based polymer precursors to reach a 20% bio-content target by 2027, aligning with circular economy goals. Its Schörfling R&D hub continues to pioneer advanced carbon molecular sieve membranes for complex chemical separations.

Honeywell UOP strengthens natural gas processing leadership with high-flux membrane systems

Honeywell UOP is a key player in the gas barrier membranes market, particularly in natural gas processing and acid gas removal applications. In April 2026, the company introduced Separex™ Flux+ membranes, delivering 25% higher flux compared to traditional cellulose acetate systems, improving efficiency in high-CO₂ gas streams. Its hollow-fiber membrane technology leads the construction segment with a strong market share due to superior packing density and scalability. Honeywell UOP membranes are deployed in 40% of global large-scale gas processing plants, highlighting its dominance in CO₂ and H₂S removal. The company integrates its membrane systems with UOP Russell modular plants, enabling plug-and-play installation and reducing on-site construction time by 30%. This integration capability enhances its competitiveness in large-scale energy infrastructure projects.

UBE Corporation expands high-temperature membrane applications for chemical and flue gas separation

UBE Corporation is enhancing its role in the gas barrier membranes market through capacity expansion and advanced polyimide membrane innovation. The company completed a twofold expansion of its hollow-fiber production capacity in Japan to meet growing demand for CO₂ separation. Its 2026 F-type membranes demonstrate exceptional thermal stability, maintaining selectivity at temperatures up to 150°C, making them ideal for flue gas and syngas purification. UBE leads in dehydration and solvent recovery applications, offering membrane solutions that replace energy-intensive distillation processes in chemical and pharmaceutical industries. The establishment of a technical support hub in Singapore strengthens its presence in the fast-growing Asia-Pacific market. This focus on high-temperature performance and process efficiency positions UBE as a key player in industrial gas separation technologies.

Air Products accelerates hydrogen economy adoption with modular membrane purification systems

Air Products and Chemicals is a leading provider of gas barrier membranes, particularly in hydrogen purification and industrial gas separation. Its PRISM® membrane systems have over 50 years of operational history, with extensive deployment across global industries. The company has scaled PRISM® GreenDry systems, enabling membrane-based gas dehydration and reducing maintenance costs by 40% compared to traditional desiccant systems. A significant portion of its $12.6 billion revenue in 2025 is linked to green hydrogen initiatives, where membrane separation plays a critical role in purification. In 2026, Air Products introduced modular hydrogen recovery systems for refinery off-gas, capable of handling variable flow conditions in decentralized energy networks. This innovation strengthens its leadership in hydrogen economy infrastructure and gas purification technologies.

MTR drives carbon capture innovation with advanced mixed-matrix membrane technologies

Membrane Technology and Research (MTR), Inc. is emerging as a disruptive innovator in the gas barrier membranes market, particularly in carbon capture and CCUS applications. In 2026, the company commissioned the world’s largest polymeric membrane carbon capture plant in Wyoming, capable of capturing over 150 tonnes of CO₂ per day using Polaris™ membranes. MTR specializes in mixed-matrix membranes that integrate metal-organic frameworks with polymer matrices, significantly enhancing permeability and selectivity beyond conventional limits. The company is targeting the CCUS market, due to global net-zero commitments. Its vapor-separation membranes enable recovery of valuable hydrocarbons from petrochemical vent streams, offering payback periods of less than 18 months. This strong innovation pipeline positions MTR at the forefront of next-generation membrane technologies.

India Gas Barrier Membranes Market: CCUS Acceleration and Industrial Gas Separation Expansion

India is emerging as the fastest-growing region in the global gas barrier membranes market, driven by aggressive investments in carbon capture, utilization, and storage (CCUS), industrial gas separation, and hydrogen production technologies. The Union Budget 2026–27 has introduced a major incentive scheme of ₹20,000 crore aimed at scaling CCUS adoption across heavy industries, positioning India as a critical hub for industrial decarbonization.

The country’s R&D roadmap for Net Zero, implemented in December 2025, is accelerating the transition of polyimide and polyamide gas separation membranes from pilot stages to large-scale refinery and industrial applications. Key industrial corridors such as Gujarat and Maharashtra are witnessing rapid deployment of membrane-based systems for nitrogen generation, natural gas conditioning, and blue hydrogen production.

Technological advancements include the integration of imported membrane modules with domestic engineering solutions, enabling cost-effective deployment in steel and cement sectors. The growing food processing and pharmaceutical industries are also driving demand for hollow fiber membranes, particularly in decentralized nitrogen generation systems. Additionally, global players are investing in localized training centers in Tamil Nadu, enhancing technical expertise and accelerating adoption among regional operators.

United States Gas Barrier Membranes Market: Bio-LNG Innovation and Hydrogen Recovery Systems

The U.S. gas barrier membranes market is advancing rapidly, supported by innovation in renewable natural gas (RNG), hydrogen recovery, and industrial decarbonization technologies. Companies such as Air Liquide and Air Products are leading innovation with advanced membrane solutions for biomethane production and LNG separation, significantly reducing reliance on energy-intensive processes.

Technological breakthroughs, including PRISM GreenSep LNG membrane separators, are enabling efficient Bio-LNG production by eliminating traditional amine scrubbing processes and lowering operational costs. The expansion of data centers is also driving demand for gas barrier membranes in fire suppression systems, where high-purity nitrogen is used to maintain inert atmospheres.

Regulatory pressures, particularly under the EPA’s PFAS Strategic Roadmap (2025), are encouraging the development of fluorine-free barrier coatings for packaging applications, accelerating innovation in bio-based and sustainable membrane materials. The U.S. market is dominated by polymeric membranes, widely used in natural gas sweetening and CO₂ removal processes, especially in energy hubs like the Permian Basin.

Significant investments in hydrogen recovery units across Gulf Coast refineries are further strengthening the adoption of membrane technologies as an energy-efficient alternative to cryogenic separation methods, reinforcing the country’s leadership in advanced gas separation systems.

Germany Gas Barrier Membranes Market: Hydrogen Backbone and Circular Packaging Innovation

Germany continues to lead the European gas barrier membranes market, driven by its strong focus on hydrogen infrastructure, circular economy solutions, and advanced material innovation. As a key contributor to the European Hydrogen Backbone project, Germany is deploying membrane technologies capable of achieving 99.9% hydrogen purity, enabling efficient integration with existing gas networks.

Sustainability remains a core focus, with innovations such as SEPURAN Green biogas membranes designed to maximize methane recovery in wastewater and agricultural applications. Regulatory frameworks under the EU Net Zero Industry Act are mandating increased CO₂ capture efficiency, accelerating the adoption of high-performance polyimide membranes across industrial sectors.

Germany is also pioneering mono-material barrier films for flexible packaging, aligning with circular economy goals by enabling recyclability without compromising barrier performance. Technological advancements include the development of ceramic-polymer hybrid membranes, offering superior thermal stability for chemical processing applications.

Key applications extend to vacuum insulation panels (VIPs) used in energy-efficient buildings, where gas barrier membranes play a critical role in maintaining insulation performance, reinforcing Germany’s position as a leader in sustainable building technologies.

China Gas Barrier Membranes Market: Industrial Scale Production and Petrochemical Integration

China dominates the global gas barrier membranes market share, driven by its massive industrial base and rapid expansion in petrochemical processing, biogas upgrading, and manufacturing-scale membrane production. The country is transitioning from a technology importer to a leader in integrated gas separation platforms, combining multiple functionalities such as CO₂ removal and H₂S treatment into single modular systems.

Government initiatives are supporting large-scale adoption, with incentives for installing membrane-based biogas upgrading units across hundreds of rural pilot projects. Coastal petrochemical hubs are driving demand for membranes in emission reduction and hydrocarbon recovery, supporting China’s environmental compliance goals.

Technological integration is enhancing efficiency, with modular membrane systems reducing operational footprints by up to 30%. The country also leads in the production of high-barrier films for food and beverage packaging, extending shelf life for exported goods.

Strict industrial emission regulations introduced in 2025 have made gas barrier membranes essential for VOC recovery in coating and paint manufacturing facilities. Additionally, expansion of membrane manufacturing clusters in Suzhou and Wuxi has significantly increased global supply capacity, particularly for hollow fiber polymeric membranes.

Japan Gas Barrier Membranes Market: High-Performance Materials and Electronics Integration

Japan’s gas barrier membranes market is defined by its leadership in high-performance materials, flexible electronics, and advanced medical applications. The country has achieved significant breakthroughs in transparent gas barrier membranes for foldable OLED displays, offering extremely low water vapor transmission rates, essential for next-generation electronics.

In the medical sector, innovations include breathable yet gas-impermeable membranes used in wound care and pharmaceutical packaging, ensuring product integrity while maintaining moisture balance. Government support through METI is driving R&D in inorganic and metallic membranes for high-temperature hydrogen production, aligning with Japan’s green growth strategy.

Technological advancements such as hybrid reverse osmosis and gas separation membranes are improving chemical resistance and reducing lifecycle environmental impact. Japan also plays a critical role in the lithium-ion battery sector, where gas barrier membranes are used in separators to prevent gas buildup and enhance safety.

Collaborations between industry and research institutes are accelerating the commercialization of graphene-based barrier materials, positioning Japan as a global leader in advanced membrane technologies.

South Korea Gas Barrier Membranes Market: Energy Storage and LNG Transport Innovation

South Korea is leveraging gas barrier membrane technologies to strengthen its position in energy storage systems (ESS), LNG transport, and semiconductor manufacturing. The shipbuilding sector is a major driver, with the adoption of FEP-coated gas barrier membranes in LNG carriers to ensure minimal boil-off rates during long-distance transportation.

In the battery sector, the development of gas-venting barrier membranes is enhancing safety in large-scale ESS installations by allowing controlled pressure release while preventing moisture ingress. Major investments by companies such as Samsung SDI and LG Energy Solution are accelerating innovation in solid-state battery materials, where high-performance gas barriers are critical for long-term durability.

Regulatory updates under K-REACH 2025 are enforcing stricter standards for barrier materials used in food-contact applications, encouraging the adoption of mineral-based and environmentally friendly coatings. Technological advancements include the commercialization of multi-layer co-extruded barrier films, combining multiple gas barrier properties into ultra-thin structures for electronics applications.

Additionally, semiconductor manufacturing facilities are utilizing specialized gas barrier curtains to maintain ultra-pure nitrogen environments, supporting advanced wafer processing technologies.

Gas Barrier Membranes Market Report Scope

Gas Barrier Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2032)

|

$2.3 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material Type (Polymeric Membranes, Inorganic and Metallic Membranes, Composite, Advanced Materials), By Module (Hollow Fiber, Spiral Wound, Plate and Frame, Tubular and Capillary), By Function (Gas Separation and Purification, Protection and Containment, Oxygen Enrichment and Nitrogen Generation, Acid Gas Removal, Hydrogen Recovery, Carbon Capture and Sequestration), By Substrate (Reinforced Membranes, Self-Adhesive Membranes, Liquid-Applied Barrier Membranes, Non-woven Fabric Backed), By End-Use Industry (Oil and Gas and Petrochemicals, Building and Construction, Chemical Processing, Food and Beverage, Healthcare and Pharmaceuticals, Energy and Power Generation, Environmental and Pollution Control), By Sales Channel (Direct Sales, Specialty Distributors and Wholesalers, Project-based Contracting and Engineering Firms)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Air Liquide S.A., Air Products and Chemicals, Inc., Linde plc, Honeywell International Inc., Evonik Industries AG, UBE Corporation, Parker Hannifin Corporation, Fujifilm Holdings Corporation, DIC Corporation, Toray Industries, Inc., Membrane Technology and Research, Inc., Generon IGS, Inc., Asahi Kasei Corporation, Pall Corporation, Atlas Copco AB

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Gas Barrier Membranes Market Segmentation

By Material Type

- Polymeric Membranes

- Polyimide and Polyamide

- Polysulfone

- Cellulose Acetate

- Polyethylene

- Polyvinyl Chloride

- Fluoropolymers

- Inorganic and Metallic Membranes

- Ceramic and Zeolite

- Silica

- Palladium and Silver Alloys

- Composite

- Advanced Materials

By Module

- Hollow Fiber

- Spiral Wound

- Plate and Frame

- Tubular and Capillary

By Function

- Gas Separation and Purification

- Protection and Containment

- Oxygen Enrichment and Nitrogen Generation

- Acid Gas Removal

- Hydrogen Recovery

- Carbon Capture and Sequestration

By Substrate

- Reinforced Membranes

- Self-Adhesive Membranes

- Liquid-Applied Barrier Membranes

- Non-woven Fabric Backed

By End-Use Industry

- Oil and Gas and Petrochemicals

- Building and Construction

- Chemical Processing

- Food and Beverage

- Healthcare and Pharmaceuticals

- Energy and Power Generation

- Environmental and Pollution Control

By Sales Channel

- Direct Sales

- Specialty Distributors and Wholesalers

- Project-based Contracting and Engineering Firms

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Gas Barrier Membranes Market

- Air Liquide S.A.

- Air Products and Chemicals, Inc.

- Linde plc

- Honeywell International Inc.

- Evonik Industries AG

- UBE Corporation

- Parker Hannifin Corporation

- Fujifilm Holdings Corporation

- DIC Corporation

- Toray Industries, Inc.

- Membrane Technology and Research, Inc.

- Generon IGS, Inc.

- Asahi Kasei Corporation

- Pall Corporation

- Atlas Copco AB

*- List not Exhaustive