Glass Flake Coatings Market Growth Driven by Offshore Energy Expansion, Heavy-Duty Corrosion Protection, and High-Build Epoxy Systems

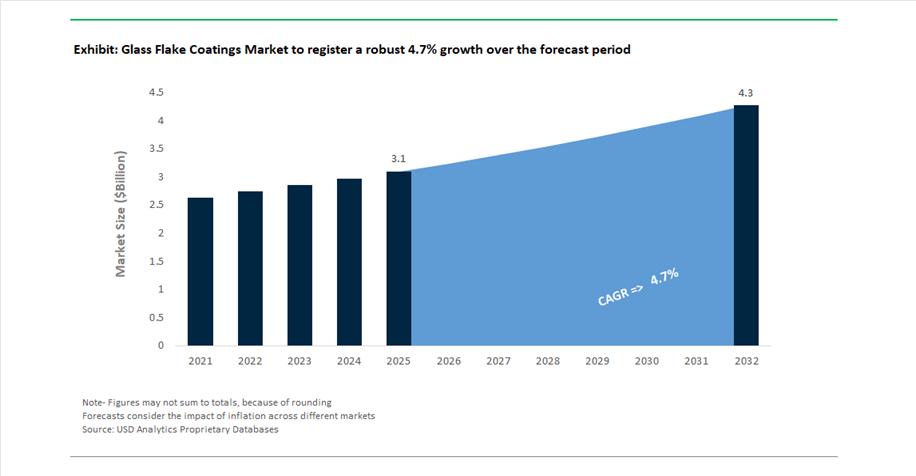

The global Glass Flake Coatings Market was valued at USD 3.1 billion in 2025 and is projected to grow at a CAGR of 4.7% between 2025 and 2032, reaching USD 4.3 billion by 2032. This growth is primarily driven by increasing demand for ultra-durable, high-barrier coatings in marine, oil & gas, offshore wind, and industrial infrastructure applications.

Glass flake coatings are engineered with microscopic glass platelets embedded in epoxy or polyester matrices, creating a tortuous path that significantly reduces permeability to water, oxygen, and corrosive chemicals. This makes them highly effective in extending the service life of assets exposed to harsh environments such as saltwater, chemicals, and extreme weather conditions. A key structural driver is the global expansion of offshore wind farms and LNG infrastructure, where long-term corrosion resistance and minimal maintenance are critical for economic viability.

Another major growth catalyst is the increasing adoption of multi-layer protective coating systems, including FBE/Glass Flake/Polypropylene (3LPP) stacks used in pipelines and energy infrastructure. These systems provide enhanced adhesion, mechanical strength, and corrosion protection, aligning with the industry’s shift toward lifecycle cost optimization and asset durability.

LNG-Specific Coatings, and AI-Driven Inspection Technologies Reshape Market Dynamics

The glass flake coatings market is undergoing a significant transformation driven by industry consolidation, application-specific innovation, and digital quality control advancements. In November 2025, AkzoNobel and Axalta Coating Systems announced a $25 billion merger, combining AkzoNobel’s International® marine coatings portfolio with Axalta’s industrial resin capabilities. This unified platform is focused on developing next-generation high-build glass flake epoxies for offshore wind and oil & gas sectors.

Product innovation is increasingly targeting specialized industrial environments. In September 2025, Hempel launched Hempadur Glass Flake 35470, specifically designed for LNG storage tanks. The formulation delivers an impermeable chemical barrier, addressing the need for contamination-free storage in the rapidly expanding LNG infrastructure market.

Capacity expansion is strengthening regional supply chains. In September 2024, Jotun increased its glass flake production capacity in Singapore by 40%, targeting rising demand from shipbuilding and coastal infrastructure projects across Southeast Asia.

Technological advancements are improving coating performance benchmarks. In September 2025, Chugoku Marine Paints introduced ceramic-modified glass flake coatings, achieving corrosion resistance exceeding 10,000 hours in salt spray tests, setting new standards for marine and naval applications.

Digital transformation is enhancing inspection and maintenance strategies. In January 2025, PPG Industries launched an AI-driven coating inspection platform, enabling operators to detect microscopic defects and shift toward risk-based maintenance schedules, extending the typical 15–20 year lifespan of glass flake systems.

Regional players are also gaining competitive traction. In September 2025, Shalimar Paints achieved ISO 12944-C5 certification for its glass flake coatings, enabling participation in high-value infrastructure projects under India’s Gati Shakti initiative.

Material innovation is addressing application challenges. In January 2025, the introduction of nano-modified hardeners improved the dispersion and alignment of glass flakes during application, reducing coating defects and enhancing barrier performance.

Upstream investments are reinforcing system performance. In January 2026, Borealis invested in high-purity polypropylene production, supporting 3LPP coating systems where glass flake layers act as a critical intermediate barrier.

Strategic focus on high-value segments is also evident. In February 2026, Sika AG launched its “Fast Forward” strategy, prioritizing high-margin glass flake coatings for applications such as data centers and semiconductor facility flooring.

Glass Flake Epoxy Coatings Enhancing Durability in Offshore FPSO Cargo Tanks

The glass flake coatings industry is witnessing increased adoption in offshore energy infrastructure, particularly in floating production storage and offloading vessels where corrosion and abrasion resistance are critical. Glass flake epoxy coatings are being specified for internal cargo tank linings due to their ability to create a multi-layered barrier structure that significantly enhances protection against harsh operating conditions. The incorporation of micrometer-scale glass flakes reduces water vapor transmission rates by up to 80%, effectively minimizing the risk of pitting corrosion in humid and chemically aggressive environments. This barrier performance is particularly important in the presence of sour gases and produced water, which accelerate corrosion in conventional coatings. In addition to corrosion resistance, glass flake systems provide approximately 25% improvement in abrasion resistance, protecting steel substrates from mechanical wear caused by fluid movement and particulate matter. These coatings also contribute to extended maintenance cycles, with operators targeting service lives of 15 to 20 years without major recoating, aligning with the long-term deployment strategies of modern FPSO vessels. Although initial application costs are higher, lifecycle cost analysis indicates a reduction in total ownership costs of around 30% due to decreased maintenance and repair requirements. These performance advantages are positioning glass flake epoxy coatings as a preferred solution for high-value offshore assets requiring long-term reliability.

Glass Flake Vinyl Ester Coatings Replacing Traditional Linings in Aggressive Chemical Storage Applications

Industrial facilities handling highly corrosive chemicals are increasingly transitioning to glass flake vinyl ester coatings as a superior alternative to traditional rubber and polyester linings. These advanced coatings provide exceptional permeation resistance, with values below 0.001 perm-inches, preventing chemical ingress and reducing the risk of osmotic blistering in high-temperature environments. The reinforcement provided by glass flakes enhances thermal shock resistance, allowing coatings to withstand temperature fluctuations up to 160°C without structural degradation. This makes them suitable for demanding applications such as sulfuric acid storage, chlorinated solvent handling, and flue gas desulfurization systems. In modern industrial specifications, glass flake vinyl ester coatings are being used for chemical concentrations up to 98%, replacing expensive alloy-based containment systems while delivering comparable performance. Another key advantage is rapid return-to-service capability, with full chemical resistance achieved within 24 hours, reducing downtime by approximately 40% compared to traditional lining systems. These characteristics are driving widespread adoption of glass flake coatings in industrial processing environments where durability, chemical resistance, and operational efficiency are critical.

India’s NMCG Phase III Driving Adoption of Glass Flake Coatings in Sewage Infrastructure

India’s National Mission for Clean Ganga Phase III is creating a significant opportunity for glass flake coatings in wastewater infrastructure, particularly for protecting concrete structures from biogenic sulfuric acid corrosion. Sewage treatment plants and pumping stations are increasingly exposed to microbial-induced corrosion caused by the formation of sulfuric acid in anaerobic conditions. Glass flake reinforced coatings are being specified to provide a durable barrier that prevents acid penetration and structural degradation. Under current infrastructure plans, treatment capacity expansions exceeding 7,000 million liters per day are being supported by coating technologies designed to extend asset life by more than 25 years, particularly in high-salinity regions such as the Ganga delta. Government funding allocations exceeding INR 692 crore are supporting the deployment of advanced coating systems that enhance durability and reduce maintenance requirements. Additionally, modern formulations are being developed with ultra-low VOC content below 100 grams per liter, aligning infrastructure development with environmental sustainability goals. These factors are positioning glass flake coatings as a key material solution in large-scale wastewater management and environmental protection initiatives in India.

USACE Standards Driving Adoption of Glass Flake Coatings for Hydraulic Steel Structures

The United States Army Corps of Engineers is creating a strong demand for glass flake coatings through updated standards for hydraulic infrastructure, including navigation lock gates and steel structures exposed to high mechanical stress. Glass flake coatings provide superior resistance to impact and abrasion, outperforming traditional coating systems by up to three times in mechanical durability tests. This performance is critical in environments where structures are subjected to repeated contact with commercial vessels and abrasive materials. Updated specifications favor high-build coating systems, allowing single applications of 500 to 750 microns to replace multiple layers of conventional coatings, reducing labor costs by approximately 15%. These coatings also contribute to extended maintenance intervals, increasing repainting cycles from approximately 12 years to over 25 years, minimizing operational disruptions in critical transportation infrastructure. Ongoing research efforts are further enhancing coating performance through the development of nano-modified glass flake systems that improve dielectric properties and reduce reliance on cathodic protection systems. These advancements are positioning glass flake coatings as a critical solution for long-term corrosion protection and operational efficiency in hydraulic engineering applications.

Glass Flake Coatings Market Share 2025: Topcoat Layer and Professional Applicators Lead Demand

Coating Layer Insights: Topcoat Segment Dominates with Superior Barrier Protection

The topcoat segment leads the glass flake coatings market with a 48% market share in 2025, driven by its critical role in delivering primary corrosion barrier performance and surface durability. Topcoats typically contain 30–50% glass flakes by weight, creating a tortuous path structure that significantly reduces moisture ingress, chemical permeation, and corrosive attack in aggressive environments such as chemical storage tanks, pipelines, and marine vessels. This high flake loading enhances long-term protection, making topcoats the most specified layer in multi-coat protective systems. In addition to functional performance, topcoats also provide aesthetic and finishing properties, including color uniformity, gloss retention, UV resistance, and weatherability, which are essential for industrial and offshore applications. As industries increasingly prioritize high-performance anti-corrosion coatings, the topcoat layer will continue to dominate due to its combined protective and visual benefits.

Sales Channel Insights: Professional Applicators Drive Market with Specialized Expertise

The professional applicators segment dominates the glass flake coatings market with a 52% share in 2025, reflecting the high level of technical expertise required for proper coating application. Glass flake coatings demand precise surface preparation standards such as near-white metal blasting (SSPC-SP10), along with controlled mixing ratios and multi-layer application techniques to ensure optimal flake alignment and barrier performance. As a result, industrial asset owners—including chemical processing plants, offshore oil platforms, and marine operators—rely heavily on certified applicators with specialized equipment and trained personnel. Additionally, professional applicators provide long-term performance warranties, typically ranging from 10 to 20 years, covering risks such as corrosion undercutting, blistering, and coating failure. These guarantees offer assurance that cannot be matched by distributor-led sales. As demand for durable, high-integrity protective coatings grows, professional applicators will remain the preferred channel in the glass flake coatings market.

Glass Flake Coatings Market Competitive Landscape: High-Barrier Epoxy Systems, Marine Protection, and Sustainable Industrial Coatings Driving Competition

The glass flake coatings market is highly competitive, driven by demand for high-build corrosion protection, marine coatings, and chemical-resistant linings. Leading players are focusing on low-VOC epoxy systems, lifecycle cost optimization, and advanced barrier technologies to support oil & gas, offshore, and infrastructure applications.

PPG advances AI-driven inspection and sustainable glass flake coatings for industrial and automotive sectors

PPG Industries is strengthening its leadership in the glass flake coatings market through digital innovation and sustainable product development. The company launched an AI-driven coating inspection platform in 2025, enabling predictive maintenance and automated quality assurance for glass flake systems in industrial and automotive applications. With $15.9 billion in 2025 net sales, PPG continues to drive growth through high-performance finishes and advanced coating technologies. 44% of its 2026 sales are derived from sustainably advantaged products, including low-VOC glass flake epoxy coatings that reduce environmental impact. Strategic collaborations with Xiaomi and BYD are enabling the development of over 100 new coating formulations combining aesthetic and functional performance. This integration of AI, sustainability, and innovation reinforces PPG’s competitive edge in high-performance coatings.

AkzoNobel dominates marine glass flake coatings with high-margin offshore and sustainable barrier solutions

AkzoNobel N.V. is a leading player in the glass flake coatings market, particularly in marine and offshore applications. Through its International® brand, the company holds a dominant share in the marine segment, supplying specialized coatings for ballast tanks and splash zones. Its value-over-volume strategy has driven a 14.2% adjusted EBITDA margin in 2026, focusing on high-margin protective coatings for energy infrastructure. AkzoNobel has achieved top-tier EcoVadis ratings, supported by its transition toward biomass-balanced resins that deliver equivalent barrier performance to traditional epoxy systems. The company is expanding its presence in Asia-Pacific by strengthening decentralized manufacturing to mitigate logistics and tariff challenges. This strategic alignment enhances its leadership in sustainable and high-performance glass flake coatings.

Jotun enhances barrier performance with advanced glass flake systems for high-temperature pipelines

Jotun A/S is advancing its position in the glass flake coatings market through high-performance pipeline coatings and barrier optimization. The company has commercialized next-generation glass flake aspect ratio control, improving barrier efficiency by 15% at reduced material loadings. Its protective coatings division is experiencing steady growth, supported by expanding Middle Eastern gas infrastructure projects requiring advanced FBE and epoxy hybrid systems. Jotun is a global leader in high-operating temperature coatings, with glass flake systems capable of maintaining integrity at temperatures up to 150°C. The company emphasizes lifecycle cost optimization, demonstrating that its coatings can extend maintenance intervals by 30–50% compared to conventional systems. This focus on durability and efficiency strengthens its competitiveness in energy and pipeline applications.

Hempel expands offshore and fire protection coatings with advanced glass flake reinforcement technologies

Hempel A/S is strengthening its position in the glass flake coatings market through innovation in offshore and industrial protection systems. Following record profitability in 2025, the company is expanding into offshore wind and energy storage sectors with its Hempaline Defend 430 solvent-free tank lining. Its Hempaguard NB coating integrates silicone technology with glass flake reinforcement to enhance impact resistance and durability in marine newbuilds. Hempel has also set a benchmark in passive fire protection with its Hempafire Extreme 550 system, offering up to 4-hour fire resistance for industrial applications.

Sherwin-Williams strengthens marine and wastewater coatings with high-solid glass flake epoxy systems

The Sherwin-Williams Company is expanding its footprint in the glass flake coatings market through high-performance marine and infrastructure solutions. Its SeaGuard® flake-filled epoxy coatings dominate the marine vessel segment, offering 87% volume solids and rapid drying times of 4 hours at 20°C. The company’s early water resistance formulations enable application in high-humidity and tidal environments, delivering impact resistance exceeding 126 inch-pounds. Sherwin-Williams is leveraging its Sewer Collection Certified Applicator Program to integrate glass flake coatings into wastewater infrastructure upgrades. Its vertically integrated supply chain helps mitigate raw material price volatility, including the 15–20% increase in epoxy resin costs in 2026. This operational efficiency enhances its competitiveness in large-scale infrastructure projects.

Grauer & Weil strengthens regional leadership with eco-friendly glass flake coatings for chemical infrastructure

Grauer & Weil (India) Ltd. is a key regional player in the glass flake coatings market, particularly in South Asia’s rapidly expanding industrial sector. The company is developing fluoroborate-free and non-cyanide coating systems aligned with global green chemistry standards while maintaining the mechanical strength of traditional glass flake resins. It leads the chemical and petrochemical lining segment in India, providing high-performance coatings that protect against aggressive acids and alkalis. Participation in SurfaceTechnology Germany 2026 highlights its growing global presence and technological capabilities. Its Kandivali manufacturing hub supports localized production and supply of barrier coatings for infrastructure rehabilitation projects. This regional focus and sustainable innovation position Grauer & Weil as a strong player in emerging markets.

United States Glass Flake Coatings Market: Infrastructure Rehabilitation and Hydrogen-Ready Coating Technologies

The United States glass flake coatings market is experiencing strong momentum, driven by large-scale infrastructure rehabilitation, energy grid modernization, and hydrogen pipeline readiness. Federal initiatives such as the Infrastructure Investment and Jobs Act and the Inflation Reduction Act are accelerating demand for dual-layer glass flake epoxy coatings, particularly across millions of miles of pipeline networks requiring corrosion protection.

Technological innovation is reshaping the market, with companies like PPG Industries introducing AI-driven coating inspection platforms capable of detecting micro-fissures in glass flake matrices, enhancing maintenance efficiency. Product development is also advancing with the introduction of hydrogen-ready glass flake coatings, specifically engineered to withstand high-pressure hydrogen-natural gas blends in repurposed pipelines.

Regulatory updates under the EPA’s VOC standards (2025) are pushing manufacturers toward solvent-free, high-solids glass flake systems, reducing hazardous air pollutant emissions in marine and industrial applications. Key applications include wastewater treatment plants, where glass flake coatings are widely used to combat biogenic sulfuric acid corrosion. Additionally, strategic expansions in the Gulf Coast region are improving the production of ultra-thin glass flake pigments, enhancing coating performance and application efficiency.

China Glass Flake Coatings Market: Mega Infrastructure and Water-Based Coating Transition

China continues to dominate the global glass flake coatings market share, with a strategic transition toward water-based glass flake dispersions and environmentally compliant coating systems. Government initiatives under the 14th Five-Year Plan and the “Blue Sky” program are mandating a shift from conventional epoxy coatings to glass flake-reinforced vinyl ester systems, improving emission control and long-term durability.

Large-scale infrastructure projects, including the South-to-North Water Diversion Project, are driving demand for NSF-certified glass flake coatings used in pumps, valves, and large-diameter pipelines to prevent erosion and corrosion. Regulatory developments such as GB 4806.10-2025 standards are expanding the scope of glass flake coatings in food-contact applications, increasing their versatility across industries.

Technological advancements include the commercialization of nano-modified glass flake hardeners, enhancing coating barrier properties for chemical storage tanks. Additionally, domestic manufacturing clusters in Jiangsu and Guangdong are scaling the production of E-glass flakes, reducing dependency on imports and strengthening the local supply chain.

Key applications include flue gas desulfurization (FGD) systems in coal-to-clean energy plants, where glass flake coatings provide resistance to abrasive and corrosive slurry environments, supporting China’s industrial decarbonization goals.

Saudi Arabia Glass Flake Coatings Market: Desalination Growth and Vision 2030 Infrastructure

Saudi Arabia is a leading market in the Middle East glass flake coatings industry, driven by ambitious investments under Vision 2030, including renewable energy, desalination, and mega infrastructure projects. The country’s growing focus on offshore wind and clean energy has increased demand for glass flake coatings in splash zones, providing long-term corrosion resistance in harsh marine environments.

Strategic expansions, including the establishment of specialized coating hubs in Dammam, are enabling localized production of abrasion-resistant glass flake linings tailored for desert and offshore conditions. The expansion of desalination projects led by the Saline Water Conversion Corporation (SWCC) is significantly boosting demand for high-build glass flake epoxy coatings used in intake systems and pipelines.

Regulatory frameworks by Saudi Aramco now mandate the use of glass flake coatings with silane coupling agents, ensuring enhanced adhesion and durability for subsea equipment. Key applications include the use of glass flake-coated rebar in NEOM infrastructure, designed to withstand aggressive saline groundwater conditions.

Additionally, investments in green ammonia export terminals are driving the adoption of glass flake linings in cryogenic storage tanks, protecting against chemical degradation and ensuring long-term operational reliability.

Norway Glass Flake Coatings Market: Offshore Engineering and Carbon Capture Applications

Norway remains a global leader in the glass flake coatings market, particularly in offshore engineering, carbon capture and storage (CCS), and marine asset protection. The deployment of specialized glass flake coatings for CO₂ transport pipelines is critical for handling supercritical carbon dioxide under high pressure without coating failure.

Technological advancements include the development of hybrid glass flake-polyolefin coating systems, offering enhanced adhesion and durability for ultra-deepwater pipelines operating under extreme thermal and pressure conditions. Regulatory requirements from the Norwegian Offshore Directorate are driving increased demand for corrosion-resistant coatings, particularly for aging North Sea assets.

Innovations such as intelligent glass flake coatings embedded with micro-sensors are enabling real-time monitoring of coating performance, improving maintenance and lifecycle management. Key applications include vinyl ester glass flake linings in offshore ballast tanks, ensuring compliance with international marine coating standards.

Sustainability initiatives are also gaining traction, with the development of glass flake materials derived from recycled solar panel glass, aligning with circular economy goals and reducing environmental impact.

India Glass Flake Coatings Market: Maritime Infrastructure and Industrial Corridor Expansion

India is witnessing rapid growth in the glass flake coatings market, driven by expansion in maritime infrastructure, industrial corridors, and chemical processing industries. Government initiatives such as the National Industrial Corridor Development Programme (NICDP) are increasing demand for glass flake-lined piping and valves across newly developed smart cities.

The Maritime India Vision 2030 is accelerating the use of glass flake epoxy coatings in port infrastructure, including jetty piling and structural steel in major ports like Tuticorin and Visakhapatnam. Regulatory developments by the Bureau of Indian Standards (BIS) are focusing on establishing safety codes for glass flake coatings in pipeline applications, ensuring quality and durability.

Key applications include the adoption of microphenolic glass flake coatings in pharmaceutical and chemical reactors, where high purity and corrosion resistance are critical. Additionally, increased government tender activity—over 137 projects in early 2026—highlights strong demand across sectors such as power generation and water treatment.

Investments in localized blending and testing facilities, particularly in Gujarat, are improving supply chain efficiency and enabling the customization of glass flake architectural coatings, supporting the growth of both industrial and commercial applications.

Japan Glass Flake Coatings Market: High-Purity Innovation and Marine Durability

Japan’s glass flake coatings market is defined by its leadership in high-purity applications, semiconductor manufacturing, and marine engineering. The development of ultra-low extractable glass flake coatings is supporting advanced semiconductor processes by ensuring zero contamination in chemical delivery systems.

Technological advancements include the production of ultra-thin glass flake pigments (below 2 microns), which improve coating barrier density and performance in thin-film applications. Government initiatives led by METI are supporting the development of bio-based resins compatible with glass flake coatings, enhancing sustainability in marine applications.

Key applications include the widespread use of glass flake coatings in chemical tanker linings, enabling safe transport of aggressive cargoes. Regulatory frameworks are ensuring strict compliance with product safety standards, particularly in eliminating heavy metal contaminants.

Industrial expansion is also driving innovation, with the introduction of low-viscosity glass flake coatings designed for airless spray applications, improving efficiency in confined industrial environments. These advancements reinforce Japan’s position as a leader in high-performance, precision-engineered coating technologies.

Glass Flake Coatings Market Report Scope

Glass Flake Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2032)

|

$4.3 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Resin Type (Epoxy Glass Flake, Vinyl Ester Glass Flake, Polyester Glass Flake, Acrylic Glass Flake, Polyurethane), By Technology (Solvent-borne Coatings, Water-borne Coatings, 100% Solids, Multi-component Systems), By Substrate (Steel, Concrete and Masonry, Non-Ferrous Metals, Fiberglass), By Coating Layer (Primer, Intermediate, Topcoat), By End-Use Industry (Oil and Gas, Marine, Chemical Processing, Power Generation, Infrastructure and Construction, Automotive and Transportation), By Functional Property (Corrosion and Chemical Resistance, Abrasion and Impact Resistance, Impermeability, High-Temperature Stability), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Professional Applicators)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., PPG Industries, Inc., Jotun A/S, The Sherwin-Williams Company, Hempel A/S, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., RPM International Inc., Chugoku Marine Paints, Ltd., Sika AG, KCC Corporation, Berger Paints India Limited, Chemco International Ltd., Tnemec Company, Inc., Shalimar Paints Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Flake Coatings Market Segmentation

By Resin Type

- Epoxy Glass Flake

- Vinyl Ester Glass Flake

- Polyester Glass Flake

- Acrylic Glass Flake

- Polyurethane

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- 100% Solids

- Multi-component Systems

By Substrate

- Steel

- Concrete and Masonry

- Non-Ferrous Metals

- Fiberglass

By Coating Layer

- Primer

- Intermediate

- Topcoat

By End-Use Industry

- Oil and Gas

- Marine

- Chemical Processing

- Power Generation

- Infrastructure and Construction

- Automotive and Transportation

By Functional Property

- Corrosion and Chemical Resistance

- Abrasion and Impact Resistance

- Impermeability

- High-Temperature Stability

By Sales Channel

- Direct Sales

- Specialty Industrial Distributors

- Professional Applicators

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Glass Flake Coatings Market

- AkzoNobel N.V.

- PPG Industries, Inc.

- Jotun A/S

- The Sherwin-Williams Company

- Hempel A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Chugoku Marine Paints, Ltd.

- Sika AG

- KCC Corporation

- Berger Paints India Limited

- Chemco International Ltd.

- Tnemec Company, Inc.

- Shalimar Paints Limited

*- List not Exhaustive