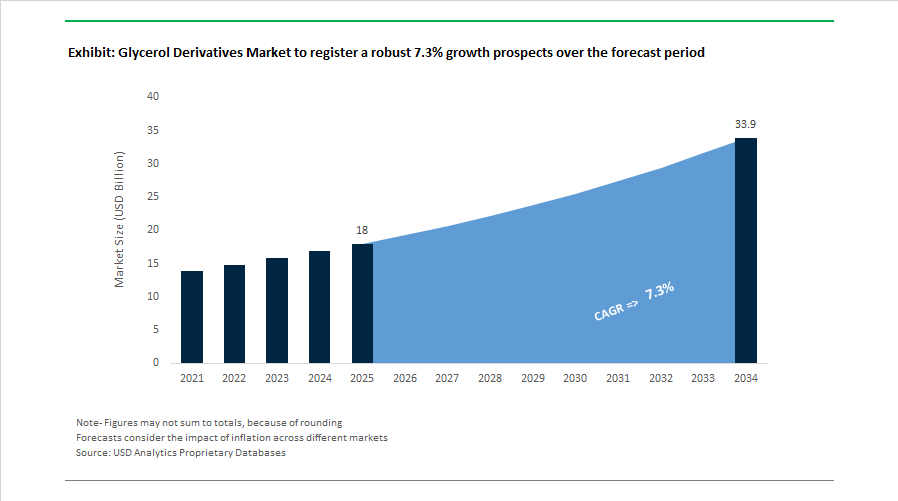

Glycerol Derivatives Market to Reach $33.9 Billion by 2034 at 7.3% CAGR Fueled by Bio-Refining, Traceability Mandates, and Green Polyol Chemistry

The Glycerol Derivatives Market is projected to grow from $18 billion in 2025 to $33.9 billion by 2034, registering a CAGR of 7.3%. Market expansion is driven by rising utilization of glycerol esters, glycerol ethers, propylene glycol derivatives, and bio-based polyols across personal care, pharmaceuticals, food emulsifiers, lubricants, and renewable polymers. The market is closely linked to biodiesel production volumes, crude glycerin upgrading capacity, and sustainability-driven reformulation across cosmetics, specialty chemicals, and performance materials. Increasing regulatory oversight on traceability, quality compliance, and carbon intensity is accelerating investment in refined glycerin and high-purity glycerol derivative platforms.

In January 2024, Xylome Corporation launched precision-fermentation palm oil substitutes targeting food and cosmetic manufacturers seeking sustainable alternatives to traditional glyceryl esters. In March 2024, ORLEN S.A. marked one year of operations at its BioPG facility, utilizing glycerol feedstock to produce renewable polypropylene glycol with a capacity of 30,000 metric tons annually under BASF technology. In May 2024, Fermbox Bio introduced EN3ZYME, a microbial blend aimed at optimizing ethanol synthesis, indirectly influencing crude glycerol quality and downstream glycerol derivative economics. In July 2024, India implemented mandatory BIS standards for petrochemicals, increasing demand for certified glycerol-based intermediates and reducing dependence on low-grade synthetic imports. In October 2024, Argent Energy commissioned Europe’s largest technical glycerine refinery at the Port of Amsterdam, upgrading biodiesel-derived crude glycerine into 99.7% pure technical-grade glycerine suitable for industrial ester and ether production. The same month, Oleon NV acquired a majority stake in A. Azevedo Óleos in Brazil, expanding its footprint in glycerol and castor oil derivatives for lubricants and personal care applications, while Evonik Industries partnered with Kolmar Wuxi to develop multifunctional glycerol esters for the Chinese beauty market.

Traceability and feedstock integration intensified through 2024–2025. In its late 2024 sustainability report, Wilmar International confirmed progress toward achieving 100% traceability to plantation by 2025, enhancing supply chain transparency for vegetable oil-derived glycerol used in pharmaceutical excipients and cosmetic emulsifiers. In March 2025, BASF SE announced price increases for diols and polyol derivatives in North America due to higher feedstock and regulatory compliance costs associated with bio-based production. In May 2025, Louis Dreyfus Company inaugurated a 55,000 metric ton per year glycerin refining plant in Lampung, Indonesia, focused on producing USP-grade glycerin and derivatives for food and pharmaceutical markets. In Q3 2025, Solvay S.A. reinvested proceeds from CO2 emission rights optimization into specialty bio-based bicarbonate and glycerol derivative development for electronics and renewable energy applications.

Innovation capacity and R&D infrastructure expansion continued into 2026. In January 2026, Cargill Incorporated expanded its Vilvoorde Innovation Center in Belgium to accelerate development of glycerol-based texturizers and emulsifiers for plant-based and reduced-sugar food systems. This investment aligns with rising European demand for clean-label emulsifiers and multifunctional polyol-based stabilizers.

The Glycerol Derivatives Market landscape reflects integration of biodiesel side-stream valorization, renewable polypropylene glycol expansion, precision-fermentation lipid alternatives, mandatory quality standards in emerging markets, plantation-level traceability, and growing demand for USP-grade glycerin derivatives. Competitive differentiation is increasingly anchored in feedstock security, carbon footprint reduction, bio-based polyol innovation, regulatory-grade purity, and application-specific formulation expertise across personal care, pharmaceuticals, food processing, lubricants, and advanced materials sectors.

Glycerol Derivatives Market Trends and Strategic Growth Opportunities

Biodiesel Byproduct Upcycling Is Redefining Pharma-Grade Glycerol Supply Chains

The glycerol derivatives market is undergoing a structural transformation driven by the rapid expansion of global biodiesel mandates and the resulting oversupply of crude glycerol. For every 100 kilograms of biodiesel produced, approximately 10 kilograms of crude glycerol are generated, creating sustained surplus volumes as countries such as Brazil advance B15 blending and Indonesia targets B40 and B50 adoption. This structural glut is forcing producers to pivot away from disposal-oriented approaches toward value-driven refining strategies focused on high-purity glycerol derivatives for pharmaceutical, cosmetic, and specialty chemical applications.

Refining technologies are increasingly capable of upgrading 80 to 90% purity crude glycerol into 99.7% pharmaceutical-grade material, enabling entry into regulated end markets with significantly higher margins. Capital investment trends reflect this shift. Oleon recently commissioned a new production facility in Germany with an annual capacity of 15,000 metric tons, specifically designed to serve European demand for high-purity glycerol derivatives in cosmetics and coatings. Policy frameworks are reinforcing long-term feedstock availability. The European Union’s Renewable Energy Directive III mandates deeper greenhouse gas intensity reductions in transport fuels, ensuring a stable, low-cost supply of biodiesel-derived glycerol through at least 2030. Together, these factors are repositioning glycerol from a byproduct liability into a strategic bio-based platform chemical.

Bio-Based Polyols Accelerate Decarbonization of the Polyurethane Value Chain

Glycerol-derived polyols are emerging as a central lever in the decarbonization of polyurethane foams used across automotive, construction, and consumer goods sectors. Corporate ESG commitments, combined with tightening low-VOC material standards, are accelerating substitution of petroleum-based polyether and polyester polyols with bio-based alternatives. Industry benchmarks indicate that nearly 28% of current R&D investment in sustainable polymers is now focused on bio-based polyurethane systems.

Major industrial players are scaling capacity to meet this demand. Cargill has committed more than 35 million dollars toward expanding production of bio-based industrial polyols, citing accelerating demand from insulation, furniture, and automotive interior manufacturers. Commercial partnerships are translating innovation into market-ready products. Covestro and Selena have launched bio-attributed polyurethane foams for thermal insulation that deliver comparable R-value performance while materially lowering carbon footprint. Government data show that more than 35% of new polyurethane applications in North America now incorporate sustainable or bio-derived content, representing a roughly 40% increase in adoption over the past three years. This trend positions glycerol derivatives as foundational inputs in low-carbon materials strategies.

Pharmaceutical Expansion of Glycerol Ethers and Esters

High-value pharmaceutical pathways represent a major opportunity for glycerol derivatives, particularly glycerol ethers and esters with antiviral and immunological relevance. Glycerol monolaurate is gaining attention as a broad-spectrum antiviral mitigant, with studies demonstrating efficacy against complex viral pathogens such as African swine fever. These findings are opening commercial avenues across both human and veterinary pharmaceutical markets, where demand for biocompatible lipid-based actives is rising.

The vaccine ecosystem further strengthens this opportunity. The U.S. vaccine adjuvants market, which relies heavily on oil-in-water emulsions stabilized by glycerol derivatives, is projected to approach 1.4 billion dollars by 2034. Government-backed research initiatives supported by National Institutes of Health and Centers for Disease Control and Prevention are accelerating development of next-generation particulate adjuvants that use glycerol-based lipids to enhance antigen delivery. Pharmaceutical companies are increasingly collaborating with academic and biotech partners to optimize glycerol ether formulations that improve drug transport efficiency and immune cell targeting, positioning glycerol derivatives as critical enablers in advanced therapeutics.

Bio-Based De-Icing Fluids for Aviation and Infrastructure Resilience

Environmental regulation is catalyzing a significant shift toward glycerol-based de-icing and anti-icing fluids in aviation and transport infrastructure. Stricter oversight by the Environmental Protection Agency and the European Union Aviation Safety Agency is driving the phase-out of urea-based de-icers due to their high toxicity and wastewater impact. The EPA’s Airport Deicing Effluent Guidelines require major airports to eliminate urea-containing products, creating immediate demand for biodegradable glycerol-based Type I and Type IV fluids with lower chemical oxygen demand.

Operational data underscore market readiness. At Munich Airport, approximately 57% of de-icing fluids used during the 2024 to 2025 winter season were recycled or bio-based, highlighting the operational maturity of glycerol-derived solutions. In North America, where increasingly volatile winter weather events stress airport operations, authorities are prioritizing glycerol-based fluids for their superior holdover times and reduced environmental toxicity. The region currently accounts for more than 32% of global demand for advanced aircraft de-icing solutions, positioning glycerol derivatives as a long-term growth engine at the intersection of sustainability, safety, and infrastructure resilience.

Glycerol Derivatives Market Share and Segmentation Insights

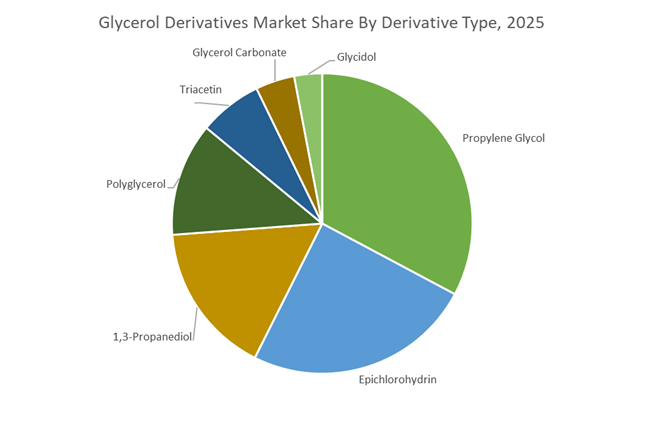

Propylene Glycol Leads the Glycerol Derivatives Market Through Bio-Based Chemical Production

Propylene Glycol accounted for 32.80% of the Glycerol Derivatives Market share in 2025, making it the largest derivative produced from glycerol feedstocks. Bio-based propylene glycol is typically produced through catalytic hydrogenolysis of glycerol, a process that converts surplus glycerin generated from biodiesel production into high-value chemical intermediates. This derivative is widely used across food processing, pharmaceutical formulations, personal care products, and industrial fluids, where it functions as a humectant, solvent, and stabilizing agent. Its chemical properties closely match those of petroleum-derived propylene glycol, allowing manufacturers to substitute bio-based material without altering formulation performance. In 2025, demand for glycerol-derived propylene glycol is expanding due to renewable content certification and sustainability commitments from global consumer brands. Companies in the food, cosmetics, and pharmaceutical sectors increasingly require bio-based chemical inputs to meet carbon reduction targets and product sustainability claims. Certified renewable propylene glycol produced from glycerol enables manufacturers to maintain performance standards while improving product environmental credentials, allowing suppliers to command premium pricing for verified renewable-grade material.

Polymers and Chemicals Drive the Largest Demand for Glycerol-Derived Chemical Intermediates

Polymers and Chemicals represented 38.60% of the Glycerol Derivatives Market share in 2025, making this sector the largest consumer of glycerol-based chemical intermediates. Glycerol derivatives serve as critical building blocks for polymer production and specialty chemical synthesis, enabling manufacturers to develop renewable alternatives to traditional petroleum-derived monomers. Derivatives such as epichlorohydrin, propylene glycol, and 1,3-propanediol are widely used in the production of epoxy resins, polyurethanes, polyester fibers, coatings, adhesives, and engineered plastics. These materials are essential in industries including automotive manufacturing, packaging materials, consumer goods, and construction chemicals. In 2025, the polymer sector is experiencing increased adoption of bio-based monomers derived from glycerol, driven by sustainability initiatives across industrial supply chains. For example, 1,3-propanediol is widely used in PTT polyester fibers and Sorona® polymers, while bio-based epichlorohydrin is utilized in renewable epoxy resin systems. These materials allow manufacturers to produce high-performance polymers with renewable content, enabling companies to meet environmental targets while maintaining mechanical strength, durability, and chemical resistance required in advanced material applications.

Competitive Landscape in Glycerol Derivatives Market

BASF SE Expands High-Purity Glycerol Derivatives Through Green Transformation

BASF SE is reinforcing its position in bio-based glycerol derivatives under its Winning Ways strategy, prioritizing market-driven green transformation and high-margin specialty chemicals. The April 2025 launch of Lamesoft® OP Plus reflects BASF’s focus on glycerol-based wax dispersions that enhance sustainability profiles in rinse-off personal care formulations. Scaling of the Zhanjiang Verbund site strengthens BASF’s supply of pharmaceutical- and cosmetic-grade glycerol derivatives across Asia-Pacific. The company anticipates sustainable chemical demand to outpace supply by late 2026, prompting capital allocation toward low-emission, high-performance polyols and emulsifiers. Its integrated production infrastructure ensures consistent quality for high-purity glycerol derivatives used in dermatological and industrial applications.

Wilmar International Anchors Global Glycerol Feedstock and Derivative Supply

Wilmar International controls the upstream economics of crude glycerol through its dominance in palm and lauric oil processing across Indonesia and Malaysia. In 2025 and 2026, the company shifted focus from commodity glycerin sales toward higher-margin glycerol esters and functional derivatives for food, cosmetics, and oleochemical applications. The $70 million acquisition of PZ Cussons Plc’s remaining stake in PZ Wilmar consolidated downstream integration into consumer and personal care formulations. Wilmar’s Timebound Action Plan targets 100% traceability to plantation, aligning glycerol derivative exports with EUDR compliance requirements. As a primary global supplier, Wilmar acts as a price anchor in the glycerol market, stabilizing feedstock flows for derivative manufacturers worldwide.

Kao Corporation Advances Precision Surfactants Using Glycerol Chemistry

Kao Corporation continues expanding its high-value chemical portfolio under its K27 Mid-term Plan, emphasizing growth beyond Japan in Asia and the Americas. FY2025 results showed a 3.7% increase in consolidated net sales, supported by performance in information materials and chemical businesses. Kao’s precision selective cleansing technologies incorporate glycerol-derived surfactants engineered for superior skin compatibility and full biodegradability. These derivatives enhance sensory performance while meeting stringent environmental standards in personal care markets. The company’s focus on premium hair and skin care, reinforced by its planned July 2026 share split, reflects confidence in high-margin glycerol-based formulations within its Global Consumer Care segment.

Oleon NV Strengthens European Leadership in Bio-Circular Glycerol Esters

Oleon NV, part of the Avril Group, operates as a leading European supplier of pharmaceutical- and cosmetic-grade glycerol derivatives. Its upstream integration enables 100% vegetable-based sourcing for glycerol esters and specialty polyols. In 2026, Oleon is aligning production with the EU Green Claims Directive, positioning its derivatives as bio-circular alternatives to petroleum-derived solvents and stabilizers. Enhanced digital and physical traceability systems support audit readiness for multinational B2B customers in regulated markets. The company’s emphasis on excipient purity and compliance strengthens its competitive position in pharmaceutical, nutraceutical, and premium cosmetic formulations requiring validated glycerol ester specifications.

Croda International Expands APAC Capacity for Specialty Glycerol Polyols

Croda International is scaling its Singapore facility, operational during 2025 and 2026, to meet surging demand for glycerol-based emulsifiers and esters in Asia-Pacific. Its smart science platform focuses on developing glycerol derivatives that mimic the skin’s lipid barrier for advanced dermatological formulations. In 2026, Croda is accelerating functional substitution strategies, replacing petrochemical polyols with bio-based glycerol alternatives in coatings and polymer systems. The company’s Land Positive commitment by 2030 shapes sourcing decisions for raw glycerin, emphasizing regenerative agriculture and low-impact feedstocks. Croda’s strength lies in high-purity, performance-oriented glycerol derivatives tailored to life sciences and consumer care applications.

Stepan Company Expands Bio-Based Ester Capacity Through Strategic Acquisitions

Stepan Company has significantly expanded its glycerol ester and specialty oleochemical capacity following its acquisition of Ecogreen Oleochemicals’ fatty acid ester business. The company is a major supplier of high-purity glycerol esters used as carriers in medical nutrition and dietary supplements. In early 2026, Stepan emphasized bio-based polyols for construction, where glycerol-derived plasticizers enhance concrete workability and sustainability metrics. Leveraging strong North American manufacturing capabilities, Stepan is capitalizing on nearshoring trends to localize production of green chemicals. Its long-term strategy targets substantial regional market share expansion through reliable supply of pharmaceutical-grade and industrial glycerol derivatives.

China: Regulatory Acceleration and Biodiesel-to-Derivatives Integration

China’s glycerol derivatives industry is advancing through a tightly coordinated regulatory and manufacturing modernization agenda. In August 2025, the National Medical Products Administration approved multiple new cosmetic ingredient filings, including glycerol dioleate derived from camellia seed oil. This approval reflects a structural shift toward indigenous, bio-active lipid derivatives positioned for premium personal care formulations and reduced reliance on imported esters. In parallel, the Ministry of Industry and Information Technology is enforcing Smart Green Workshop standards across polyol production, mandating digital twin deployment for polyglycerol grades to lower energy intensity and improve batch consistency.

At the feedstock level, Shandong’s chemical clusters have operationalized integrated biodiesel-glycerol platforms that directly convert crude glycerol into glycerol carbonate using heterogeneous catalysis. This bypasses conventional purification, compresses processing steps, and improves carbon efficiency. Regulatory tightening by the State Administration for Market Regulation in 2025, particularly around illegal food additive derivatives, has further standardized analytical testing for glycerol-based digestive health ingredients, reinforcing quality-led export credibility.

India: Bio-Based Prioritization and Solvent Substitution

India has elevated glycerol derivatives to a strategic bio-based building block under its BioE3 policy framework, unlocking capital support for downstream expansion in refined polyglycerols and specialty esters. This policy signal is translating into capacity additions by domestic chemical groups and accelerating vertical integration across oleochemicals and biotechnology. Complementing this push, CSIR-CIMAP has piloted glycerol-derived green solvents for essential oil extraction, aiming to displace petroleum-derived hexane across fragrance and aroma value chains by the next regulatory cycle.

Industrial infrastructure investment has also gathered pace with the commissioning of a large bio-glycerine complex in western India, designed to support bio-based propylene glycol production for coatings and functional fluids. On the demand side, the rapid evolution of India’s cosmetics and personal care ecosystem is driving increased adoption of glycerol-based humectants and pearlizers, particularly for clean-label and sulfate-free formulations aligned with export market requirements.

United States: Onshoring Momentum and Renewable Pathway Innovation

In the United States, regulatory flexibility and energy policy alignment are shaping the glycerol derivatives landscape. The Environmental Protection Agency extended TSCA reporting timelines for selected polyol precursors into 2026, enabling manufacturers to complete safety validation for next-generation glycerol-derived plasticizers. This extension has provided operational certainty while companies recalibrate portfolios toward lower-toxicity alternatives.

Strategically, the Department of Energy has designated glycerol as a priority renewable building block, backing pilot projects that convert biodiesel byproducts into acrylic acid and superabsorbent polymer intermediates through chemo-enzymatic routes. Concurrently, tariff adjustments on refined glycerol imports have accelerated onshoring by agribusiness majors, expanding domestic production of acetins and triacetins to mitigate supply risk. Additional guidance from federal food safety programs in 2025 has tightened purity benchmarks for glycerol derivatives sourced from sustainable aviation fuel biomass, safeguarding food-grade emulsifier applications.

European Union: Re-Standardization and Circular Recovery

Across the European Union, regulatory recalibration is redefining glycerol derivative utilization. Commission Regulation (EU) 2025/651 has reauthorized mono- and diglycerides of fatty acids as glazing agents for fresh produce, forcing agricultural suppliers to re-standardize glycerol-based coatings and documentation. Simultaneously, REACH audits under the Zero Pollution objective are steering detergent and homecare producers toward polyglycerol esters, valued for superior biodegradability and aquatic safety compared with conventional surfactants.

Circularity is emerging as a differentiator. In late 2025, Lenzing confirmed successful recovery of glycerol derivatives from textile processing streams, repurposing these materials into industrial lubricants for automotive applications. This closed-loop model reinforces the EU’s emphasis on waste valorization while creating secondary supply streams for performance polyols.

Brazil: Decarbonization Incentives and Domestic Substitution

Brazil’s glycerol derivatives industry is being reshaped by decarbonization-linked incentives and trade protection. Under the Presiq green investment framework, chemical producers investing in low-carbon processes and bio-based feedstocks are receiving fiscal advantages, channeling capital toward glycerol value chains tied to biodiesel and renewable chemicals. This policy environment has strengthened Brazil’s position as a hub for bio-based polyols and carbonate intermediates.

At the same time, renewed import protection measures through 2026 are encouraging local production of glycerol-derived glycidol and polyols. Domestic leaders such as Braskem are leveraging these measures to deepen integration between bio-feedstocks and specialty derivatives, reducing exposure to external petrochemical volatility and reinforcing regional supply security.

Snapshot of Country-Level Strategic Drivers

Glycerol Derivatives Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Structural Impact on Glycerol Derivatives

|

|

China

|

Regulatory approvals and smart manufacturing

|

Higher-value cosmetic lipids and energy-efficient polyglycerols

|

|

India

|

BioE3 prioritization and solvent substitution

|

Rapid scale-up of bio-based polyols and green extraction

|

|

United States

|

Onshoring and renewable pathway funding

|

Domestic acetins, acrylics, and SAF-linked derivatives

|

|

European Union

|

REACH audits and circular economy

|

Shift to biodegradable PGEs and recovered polyols

|

|

Brazil

|

Decarbonization incentives and tariffs

|

Localization of glycerol-derived intermediates

|

Glycerol Derivatives Market Report Scope

Glycerol Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18 Billion

|

|

Market Size (2034)

|

$33.9 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Derivative Type (Polyglycerol, Glycerol Carbonate, Propylene Glycol, 1,3-Propanediol, Triacetin, Epichlorohydrin, Glycidol), By Grade (Pharmaceutical Grade, Food Grade, Technical Grade, Cosmetic Grade), By Source (Biodiesel Byproduct, Fatty Acid and Fatty Alcohol Processing, Soap Manufacturing, Synthetic Sources), By Application (Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Polymers and Chemicals, Energy Storage, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Wilmar International Limited, BASF SE, Cargill, Incorporated, KLK OLEO, Archer Daniels Midland Company, Oleon NV, Emery Oleochemicals, Godrej Industries Limited, Kao Corporation, IOI Group, Croda International Plc, Vantage Specialty Chemicals, Louis Dreyfus Company, Solvay S.A., Musim Mas Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glycerol Derivatives Market Segmentation

By Derivative Type

- Polyglycerol

- Glycerol Carbonate

- Propylene Glycol

- 1,3-Propanediol

- Triacetin

- Epichlorohydrin

- Glycidol

By Grade

- Pharmaceutical Grade

- Food Grade

- Technical Grade

- Cosmetic Grade

By Source

- Biodiesel Byproduct

- Fatty Acid and Fatty Alcohol Processing

- Soap Manufacturing

- Synthetic Sources

By Application

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Polymers and Chemicals

- Energy Storage

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Glycerol Derivatives Industry

- Wilmar International Limited

- BASF SE

- Cargill, Incorporated

- KLK OLEO

- Archer Daniels Midland Company

- Oleon NV

- Emery Oleochemicals

- Godrej Industries Limited

- Kao Corporation

- IOI Group

- Croda International Plc

- Vantage Specialty Chemicals

- Louis Dreyfus Company

- Solvay S.A.

- Musim Mas Group

*- List not Exhaustive