Greywater Recycling Systems Market Overview: Growth Outlook to 2034

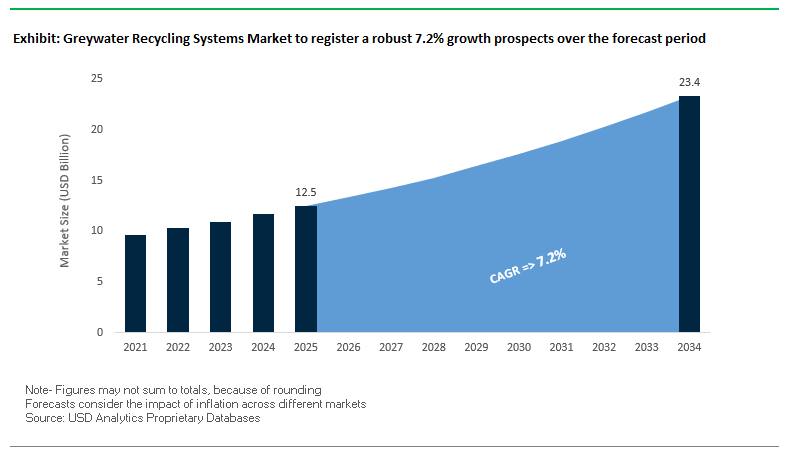

The global greywater recycling systems market is projected to expand from $12.5 billion in 2025 to $23.4 billion by 2034, reflecting a healthy CAGR of 7.2%. This steady growth underscores the rising urgency to address water scarcity, climate change, and sustainable urban development. Greywater, which comprises wastewater from showers, sinks, and laundry, makes up nearly 40% of household water use, and its effective treatment and reuse are becoming integral to green building practices and water conservation strategies worldwide. The adoption of greywater recycling systems is being accelerated by regulatory mandates, green building certifications, and increasing economic incentives for reducing water bills and sewage volumes.

Key Insights for Industry Stakeholders

- Household savings potential: Residential greywater systems can reduce freshwater consumption by an average of 35%, primarily by reusing water for irrigation and toilet flushing.

- EPA findings: The U.S. Environmental Protection Agency (EPA) reports that the average American uses over 80 gallons of water daily, with nearly 40% qualifying as greywater.

- Regional growth hotspots: The Asia-Pacific region is emerging as a fast-growth hub due to green building codes and rapid urbanization, alongside rising water stress.

- Policy-driven momentum: Growing awareness of state and federal water regulations in the U.S. and Europe is driving municipalities, real estate developers, and industries to adopt on-site greywater treatment solutions.

Market Analysis: Recent News and Strategic Developments in Greywater Recycling

The greywater recycling systems market is evolving rapidly, shaped by regulatory pressure, sustainability targets, and new technologies in decentralized water treatment. Over the past year, the industry has seen significant breakthroughs in nanotechnology membranes, microbial fuel cells, and mobile treatment units, reflecting a strong pipeline of innovations that enhance efficiency and reduce costs.

In August 2025, DuPont Water Solutions earned recognition as part of the BIG Sustainability Awards for its advancements in industrial wastewater reuse and minimal liquid discharge (MLD) technologies critical for greywater treatment. In July 2025, Veolia Water Technologies was chosen to equip France’s largest treated wastewater reuse project in Argelès-sur-Mer, which will provide irrigation water to agriculture, showcasing the scale at which greywater reclamation is being deployed. Just two months earlier, in May 2025, Veolia also announced its acquisition of full ownership of its Water Technologies & Solutions subsidiary, consolidating its position as a global leader in urban and industrial water reuse.

Innovation has also taken center stage. In April 2025, Kurita Water Industries demonstrated wastewater-powered microbial fuel cells, opening a path toward energy-positive water treatment. In May 2024, Nijhuis Saur Industries launched a mobile greywater treatment unit, offering decentralized and flexible solutions for real estate projects and disaster relief scenarios. Academic and research institutions are also driving breakthroughs: in January 2025, the Journal of Membrane Science published research on nanofiber membranes that efficiently remove arsenic and lead, while in December 2024, another study revealed successful use of engineered nanoparticles for cost-effective heavy metal removal. Additionally, in October 2024, a minimum liquid discharge (MLD) plant began operations in Foshan, China, treating 160,000 m³/day for the textile sector, highlighting replicable models for urban and industrial greywater management.

Key Market Trends Driving Greywater Recycling Adoption

Government Policy and Financial Incentives for Water Conservation

Government initiatives and financial support play a critical role in stimulating greywater system adoption. India’s Swachh Bharat Mission (Grameen) Phase-II, with an outlay exceeding ₹1,40,000 crore, emphasizes decentralized liquid waste management, including greywater treatment. Local programs, such as the $1,000 rebate offered by Guelph, Canada, make greywater systems more financially accessible for homeowners and small businesses. These policy measures and financial incentives directly accelerate market growth and encourage widespread adoption of sustainable water reuse solutions.

Technological Advancements in Filtration and Disinfection

Innovative treatment methods are improving efficiency, water quality, and safety of greywater recycling systems. Studies, such as a 2024 MDPI Water journal research, demonstrate that simple column-based filtration using gravel, sand, and activated carbon can reduce turbidity by 74% and biological oxygen demand by 64%. More advanced hybrid systems, integrating physical filtration (ceramic or quartz gravel) with disinfection technologies like UV, are highlighted in a 2025 IWA publication, reflecting the market trend toward multi-stage systems capable of providing higher-quality reclaimed water for non-potable uses, including irrigation and toilet flushing.

Corporate and Institutional Investment in On-Site Systems

Commercial and institutional buildings increasingly adopt on-site greywater recycling to reduce water footprint and operational costs. The Solaris building in New York City, for example, treats both greywater and blackwater using an MBR system to supply water for toilet flushing, irrigation, and cooling. Companies like Fluence Corporation offer modular, containerized systems, such as the Aspiral™, providing rapid deployment and up to 90% energy savings in aeration compared to conventional systems. This trend underscores a growing market for scalable, high-performance solutions in commercial and institutional settings.

Greywater Recycling Systems Market Share Insights

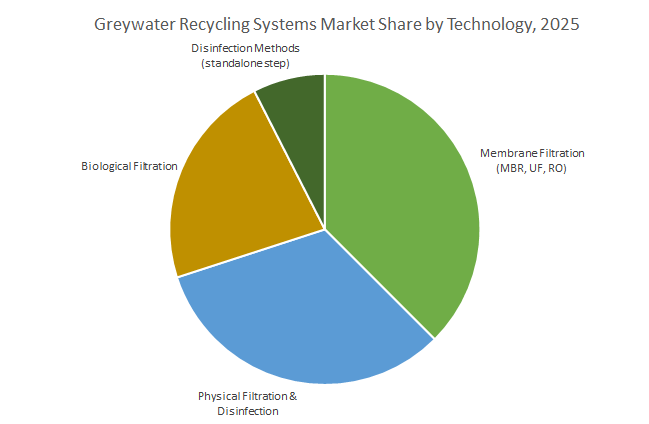

By Technology: Membrane Systems Lead Premium Segment

Membrane Filtration systems, including MBR, UF, and RO (38%), dominate the premium segment due to superior water quality suitable for multiple non-potable uses. Physical Filtration combined with Disinfection (32.8%) remains core for most residential and small commercial applications, offering reliability and cost-effectiveness. Biological Filtration (24.6%) leverages constructed wetlands, RBCs, and biofilters, valued for low energy use and eco-friendly design. Standalone Disinfection serves as a final polishing step, with UV disinfection preferred for chemical-free operation. Membrane technologies are expected to see the highest growth due to declining costs and increased adoption in high-quality water applications.

By Treatment Capacity: Small-Scale Systems Drive Volume Growth

Small-scale systems (up to 10 m³/day) (48.5%) dominate, serving single-family homes, multi-family residences, and small offices, driven by residential water mandates and sustainability awareness. Medium-scale systems (10–100 m³/day) (32.8%) cater to hotels, gyms, schools, and offices, providing significant ROI in water-intensive operations. Large-scale systems (100+ m³/day) (16.9%) serve universities, hospitals, and industrial facilities, representing high-value, custom-engineered projects that emphasize corporate sustainability objectives and operational cost savings.

By Application: Residential Leads, Commercial Offers Rapid ROI

Residential applications (52.9%) are the largest segment, fueled by mandatory green building codes, government rebates, and homeowner demand for utility cost reduction and self-sufficiency. Commercial applications (38%) offer rapid ROI in high water-use buildings, making them the most profitable growth segment. Industrial applications are niche, applied where greywater can serve process water, cooling towers, or landscape irrigation, often requiring advanced treatment for compliance and safety.

United States: AI-Enabled Greywater Systems and Regulatory Push Driving Market Expansion

The United States greywater recycling systems market is experiencing rapid growth due to stringent regulatory policies, technological innovations, and corporate adoption. The U.S. Environmental Protection Agency (EPA) is actively revising effluent guidelines to target specific contaminants, driving investment in advanced water reuse technologies. Municipal mandates, such as San Francisco’s requirement for new large constructions to integrate water reuse systems, are accelerating market adoption. Technological advancements include large-scale AI-enabled greywater recycling systems installed at major tech campuses in California, achieving a 40% reduction in water consumption. NSF-funded projects are further enhancing smart water management for households. Corporate initiatives, including hotel chains upgrading filtration systems and companies like Evoqua Water Technologies leading innovation, are expanding commercial and residential applications. Key applications focus on sustainable urban water management, reduction of potable water consumption, and integration of greywater systems in building designs.

China: Sponge City Program and Innovative Membrane Technologies Fuel Growth

China’s greywater recycling systems market is strongly influenced by government initiatives and technological advancement. The ambitious "Sponge City" program targets over 80% of urban areas to meet stormwater and greywater management standards by 2030, driving investment in both engineered and natural systems. Technological advancements, such as dual-functional reverse osmosis (RO) membranes developed by the Chinese Academy of Sciences, are enhancing greywater treatment efficiency. Corporate initiatives include projects by Danish company Aquaporin deploying advanced containerized forward osmosis (FO) systems, showcasing China’s openness to innovation. The market’s key applications involve urban flood management, sustainable rainwater reuse, and improvement of overall water quality in densely populated urban areas.

India: Government Mandates and Community-Level Implementation Boost Greywater Recycling

India’s market is propelled by regulatory mandates, government programs, and innovative technology deployment. The Bangalore Water Supply and Sewerage Board (BWSSB) requires all newly built independent houses to install greywater recycling systems, reducing stress on municipal water and sewage infrastructure. National initiatives such as the Swachh Bharat Mission (Grameen) Phase-II emphasize liquid waste management, promoting greywater systems at the Gram Panchayat level. Technological support includes IIT Madras’ deployment of advanced wastewater processing technologies, which are adaptable for greywater treatment. Corporate players, including VA Tech Wabag, are executing large-scale projects, driving the adoption of greywater recycling systems. Key applications focus on household and community-level water reuse, improved sanitation, and relief of pressure on freshwater resources.

Germany: Advanced Monitoring and ZLD Expertise Enhancing Greywater Management

Germany’s greywater recycling market benefits from regulatory frameworks, digital innovations, and corporate expertise in water management. The EU’s revised Urban Wastewater Treatment Directive (January 2025) mandates the "4th purification stage," incentivizing advanced oxidation and membrane filtration processes for greywater. The German Federal Environment Agency (UBA) notes that over 90% of major cities are developing climate adaptation strategies, which include AI-driven monitoring, digital twins, and optimized water management systems. Corporations such as H2O GmbH and GEA Group AG leverage their Zero Liquid Discharge (ZLD) expertise to provide sustainable greywater solutions. Market applications center on urban flood prevention, decentralized water management, and harvesting and reuse of greywater in residential and commercial infrastructure.

Australia: Infrastructure Investment and Innovative Water Technologies Supporting Market Growth

Australia’s greywater recycling systems market is shaped by strong environmental regulations, strategic infrastructure investment, and technological advancement. Sydney Water’s $34 billion investment plan through 2035, including projects like the Mamre Road Precinct Stormwater initiative, underscores the commitment to sustainable water infrastructure. Regulatory frameworks, including SEPP Waters of Victoria, guide water quality and environmental stewardship. CSIRO’s "Virtual Curtain" technology, which uses hydrotalcites to remove contaminants, demonstrates significant innovation in greywater treatment. The market is driven by water management needs for urban areas and mining activities, with a focus on long-term environmental stewardship and sustainable water reuse applications.

Japan: Government-Supported MBR Projects and Advanced Residential Greywater Systems

Japan’s greywater recycling systems market is driven by government policies, academic R&D, and advanced technological adoption. The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) launched the A-JUMP project to promote membrane bioreactor (MBR) technology for sewage treatment, forming the basis for advanced greywater recycling. Toray Industries Inc. and other Japanese corporations are leaders in high-efficiency membrane technologies, facilitating industrial and residential applications. In 2025, new housing complexes in Tokyo implemented fully automated greywater treatment systems across all apartments, supported by government programs encouraging eco-friendly building practices. Key applications include water conservation, decentralized on-site greywater recycling, and integration into commercial and residential infrastructure.

Competitive Landscape: Leading Companies in Greywater Recycling Systems

The competitive landscape of the greywater recycling systems market features global water technology leaders, specialized solution providers, and disruptive startups. Competition is driven by portfolio integration, cost optimization, R&D intensity, and regulatory compliance expertise. Below are detailed company profiles reflecting the market’s strategic direction.

Xylem Inc.: Expanding Integrated Greywater Recycling Platforms

Xylem Inc. combines pumps, biological systems, and analytics to provide end-to-end water solutions, including greywater reuse. Its 2023 acquisition of Evoqua created one of the world’s most comprehensive portfolios for decentralized and municipal water treatment. Xylem’s solutions span advanced oxidation, membrane bioreactors, and IoT-enabled monitoring systems, enabling real-time optimization. By focusing on digital water technologies and predictive maintenance, Xylem helps municipalities and industries cut operational costs while strengthening resilience against water shortages.

Veolia Water Technologies: Large-Scale Water Reuse and ZLD Expertise

Veolia’s competitive strength lies in its integrated urban and industrial water treatment solutions, ranging from membrane technologies to thermal evaporators and ZLD systems. In May 2025, Veolia took full ownership of its Water Technologies & Solutions business, reinforcing its leadership in sustainable water reuse. Its expertise extends from engineering and plant design to long-term O&M contracts, enabling turnkey solutions for both cities and industries. Through its GreenUp strategy, Veolia aligns greywater recycling with climate action and circular resource use, positioning itself as a partner for sustainable urban infrastructure.

SUEZ – Water Technologies & Solutions: Customized Industrial Greywater Systems

SUEZ is recognized for delivering customized greywater recycling systems, particularly for industrial clients requiring high-efficiency water reuse and ZLD compliance. Recent project wins in Asia, including a 100% wastewater recycling plant in China, reinforce its expertise in complex water recovery. The company integrates biological processes, membranes, and predictive digital platforms that optimize system efficiency, minimize fouling, and cut chemical usage. By embedding AI-driven analytics, SUEZ delivers measurable savings in OPEX while ensuring compliance with tightening water regulations.

DuPont Water Solutions: Membrane-Driven Water Circularity

DuPont leverages its FilmTec™ RO and NF membranes, IntegraTec™ UF systems, and ion exchange resins as the backbone of advanced greywater recycling. Its FilmTec™ Fortilife™ XC160 Membrane, awarded in 2025, was designed for wastewater concentration and reuse efficiency. With a presence in 112 countries, DuPont’s technologies purify over 50 million gallons per minute, enabling municipal and industrial clients to achieve water circularity and reduced carbon footprints. Its strategic focus is on developing next-generation membranes that extend lifecycle, lower energy use, and minimize fouling critical for scaling greywater adoption globally.

JalSevak Solutions: Affordable Decentralized Greywater Recycling in India

JalSevak Solutions, a fast-growing Indian startup, specializes in compact, decentralized greywater systems designed for residential and commercial users. Its recognition in the Swachhata Startup Challenge, organized by India’s Ministry of Housing and Urban Development and AFD, reflects its innovation in addressing water scarcity. The company’s scalable systems (1–100 KLD) enable reuse for toilet flushing, gardening, and cleaning, cutting household freshwater demand by up to 35%. With 75% lower O&M costs compared to conventional sewage plants, JalSevak positions itself as a cost-effective and impact-driven player in emerging markets.

Greywater Recycling Systems Market Report Scope

Greywater Recycling Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.5 Billion

|

|

Market Size (2034)

|

$23.4 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Technology (Membrane Filtration, Biological Filtration, Physical Filtration, Disinfection Methods), By Treatment Capacity (Small Scale, Medium Scale, Large Scale), By Application (Residential, Commercial, Industrial), By System Type (Gravity Systems, Pumped Systems, Package/All-in-One Systems, Custom-Designed Systems), By Sales Channel (Direct Sales, Distributors & Dealers, Online Retailers, System Integrators)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Pentair plc, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kingspan Group PLC, Kurita Water Industries Ltd., H2O GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Greywater Recycling Systems Market Segmentation

By Technology

- Membrane Filtration

- Biological Filtration

- Physical Filtration

- Disinfection Methods

By Treatment Capacity

- Small Scale (Up to 10 m³/day)

- Medium Scale (10 - 100 m³/day)

- Large Scale (Above 100 m³/day)

By Application

- Residential

- Single-Family Homes

- Multi-Story Apartments & Condominiums

- Commercial

- Office Buildings

- Shopping Malls & Retail Centers

- Hotels & Resorts

- Educational Institutions

- Hospitals & Healthcare Facilities

- Sports Facilities & Gyms

- Industrial

- Manufacturing Plants

- Food & Beverage Processing

- Municipal & Institutional

- Public Parks & Gardens

- Government Buildings

- Airports

By System Type

- Gravity Systems

- Pumped Systems

- Package/All-in-One Systems

- Custom-Designed Systems

By Sales Channel

- Direct Sales

- Distributors & Dealers

- Online Retailers

- System Integrators

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Greywater Recycling Systems Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Pentair plc

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kingspan Group PLC

- Kurita Water Industries Ltd.

- H2O GmbH

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Greywater Recycling Systems Market, mapping how policy drivers, building codes, and climate adaptation budgets translate into deployable solutions and bankable ROI. It highlights breakthroughs in modular MBR/UF packages, smart controls, and mobile units; the analysis reviews cost curves, maintenance intensities, and performance benchmarks across residential, commercial, and industrial settings, while profiling competitive strategies, partnerships, and channel dynamics. With scenario modeling through 2034, technology roadmaps, and regulatory heat-maps, this report is an essential resource for developers, utilities, EPCs, OEMs, and asset owners seeking resilient, code-compliant, and scalable greywater reuse programs. Scope Includes-

- By Technology: Membrane Filtration; Biological Filtration; Physical Filtration; Disinfection Methods

- By Treatment Capacity: Small (≤10 m³/day); Medium (10–100 m³/day); Large (>100 m³/day)

- By Application: Residential (single-family; multi-story); Commercial (offices, retail, hotels, education, healthcare, sports); Industrial (manufacturing; F&B); Municipal & Institutional (parks, government buildings, airports)

- By System Type: Gravity; Pumped; Package/All-in-One; Custom-Designed

- By Sales Channel: Direct; Distributors & Dealers; Online Retailers; System Integrators

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data 2021–2024; forecast data 2025–2034.

- Companies (analysis/profiles of 15+): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Pentair plc; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kingspan Group PLC; Kurita Water Industries Ltd.; H2O GmbH.

Methodology

USDAnalytics applies a triangulated approach: (1) bottom-up sizing from project databases, permits, and builder specifications for greywater systems across capacity bands; (2) top-down calibration using plumbing codes, rebate adoption rates, green-building certifications, and water-tariff structures; and (3) primary interviews with utilities, facility managers, OEMs, and integrators to validate CAPEX/OPEX, recovery factors, and lifecycle maintenance. We benchmark treatment trains via meta-analysis of peer-reviewed removal efficiencies, normalize for influent variability (BOD/TSS/surfactants/microbials), and run policy-led scenarios (mandates, incentives) to 2034. Competitive shares blend shipment tracking, channel checks, and disclosed backlogs, with sensitivity tests on membrane pricing, energy intensity, and retrofit density.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Greywater Recycling Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $12.5 Billion

1.3.2. Projected Market Valuation (2034): $23.4 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 7.2%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth, Drivers, and Key Challenges

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Market Trends Driving Greywater Recycling Adoption

2.3.1. Government Policy and Financial Incentives for Water Conservation

2.3.2. Technological Advancements in Filtration and Disinfection

2.3.3. Corporate and Institutional Investment in On-Site Systems

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments and Strategic Shifts

3.1.1. Veolia's Acquisitions and Reinforcement of Water Reuse Leadership (May-July 2025)

3.1.2. DuPont Water Solutions Recognized for Sustainability in Water Reuse (August 2025)

3.1.3. Goldman Sachs Acquires Liquid Environmental Solutions (July 2025)

3.1.4. Kurita Water Industries Pioneers Energy-Positive Treatment (April 2025)

3.1.5. Nijhuis Saur Launches Mobile Greywater Treatment Unit (May 2024)

3.1.6. Academic and Research Breakthroughs in Nanotechnology and Filtration (2024-2025)

3.1.7. On-site Greywater Projects in China and India (2024-2025)

4. Competitive Landscape: Leading Companies

4.1. Market Overview: Global Leaders and Innovative Specialists

4.2. Strategic Profiles of Key Companies

4.2.1. Xylem Inc.: Expanding Integrated Greywater Recycling Platforms

4.2.2. Veolia Water Technologies: Large-Scale Water Reuse and ZLD Expertise

4.2.3. SUEZ – Water Technologies & Solutions: Customized Industrial Systems

4.2.4. DuPont Water Solutions: Membrane-Driven Water Circularity

4.2.5. JalSevak Solutions: Affordable Decentralized Systems for Emerging Markets

4.2.6. Hydraloop: Low-Maintenance, IoT-Enabled Residential Systems

4.2.7. Kurita Water Industries Ltd.

5. Greywater Recycling Systems Market Segmentation Insights

5.1. By Technology

5.1.1. Membrane Filtration

5.1.2. Physical Filtration

5.1.3. Biological Filtration

5.1.4. Disinfection Methods

5.2. By Treatment Capacity

5.2.1. Small Scale (Up to 10 m³/day)

5.2.2. Medium Scale (10 - 100 m³/day)

5.2.3. Large Scale (Above 100 m³/day)

5.3. By Application

5.3.1. Residential (Single-Family Homes, Multi-Story Apartments)

5.3.2. Commercial (Office Buildings, Hotels, Educational Institutions)

5.3.3. Industrial (Manufacturing Plants, Food & Beverage Processing)

5.3.4. Municipal & Institutional (Public Parks, Government Buildings, Airports)

5.4. By System Type

5.4.1. Gravity Systems

5.4.2. Pumped Systems

5.4.3. Package/All-in-One Systems

5.4.4. Custom-Designed Systems

5.5. By Sales Channel

5.5.1. Direct Sales

5.5.2. Distributors & Dealers

5.5.3. Online Retailers

5.5.4. System Integrators

6. Country Analysis and Outlook

6.1. United States: AI-Enabled Systems and Regulatory Push

6.2. China: Sponge City Program and Innovative Membrane Technologies

6.3. India: Government Mandates and Community-Level Implementation

6.4. Germany: Advanced Monitoring and ZLD Expertise

6.5. Australia: Infrastructure Investment and Innovative Water Technologies

6.6. Japan: Government-Supported MBR Projects and Advanced Residential Systems

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Greywater Recycling Systems Market Size Outlook to 2034

7.1.1. By Technology

7.1.2. By Application

7.1.3. By Treatment Capacity

7.2. Europe Greywater Recycling Systems Market Size Outlook to 2034

7.2.1. By Technology

7.2.2. By Application

7.2.3. By Treatment Capacity

7.3. Asia Pacific Greywater Recycling Systems Market Size Outlook to 2034

7.3.1. By Technology

7.3.2. By Application

7.3.3. By Treatment Capacity

7.4. South America Greywater Recycling Systems Market Size Outlook to 2034

7.4.1. By Technology

7.4.2. By Application

7.4.3. By Treatment Capacity

7.5. Middle East and Africa Greywater Recycling Systems Market Size Outlook to 2034

7.5.1. By Technology

7.5.2. By Application

7.5.3. By Treatment Capacity

8. Company Profiles: Leading Players

8.1. Xylem Inc.

8.2. DuPont de Nemours, Inc.

8.3. Veolia Water Technologies

8.4. SUEZ

8.5. Pentair plc

8.6. Kingspan Group PLC

8.7. Toray Industries, Inc.

8.8. Kurita Water Industries Ltd.

8.9. H2O GmbH

8.10. V.A. TECH WABAG Ltd.

8.11. Aquatech International

8.12. Mitsubishi Chemical Corporation

8.13. Fluid Technology Solutions, Inc.

8.14. Hydraloop

8.15. JalSevak Solutions

8.16. Other Prominent Players

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures