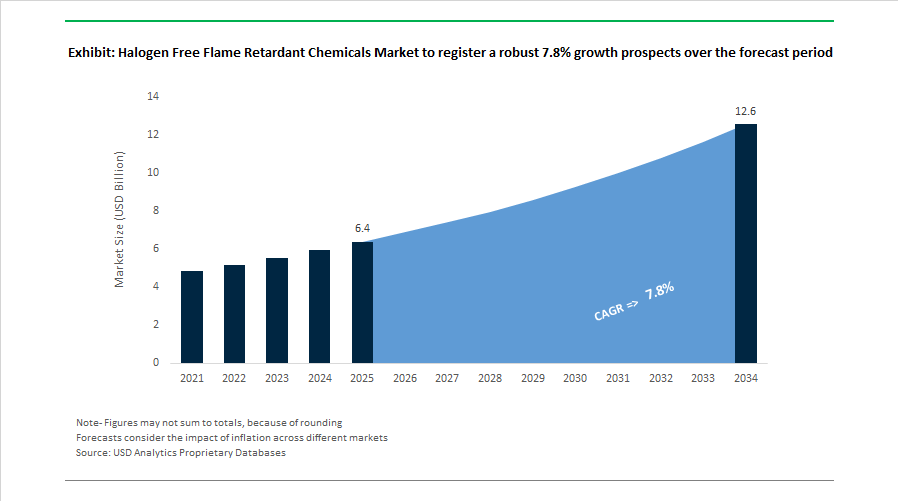

Halogen Free Flame-Retardant Chemicals Market to Reach $12.6 Billion by 2034 at 7.8% CAGR Driven by EV Electrification, Regulatory Bans, and Phosphorus-Based Innovation

The Halogen Free Flame Retardant (HFFR) Chemicals Market is projected to grow from $6.4 billion in 2025 to $12.6 billion by 2034, registering a CAGR of 7.8%. Market expansion is anchored in regulatory-driven substitution of brominated and chlorinated flame retardants, rapid electrification of vehicles, renewable energy infrastructure build-out, and stricter building safety standards across Asia-Pacific, North America, and Europe. Phosphorus-based flame retardants, aluminum trihydrate (ATH), magnesium hydroxide systems, polymeric reactive additives, and melamine-free ammonium polyphosphates are gaining traction as manufacturers respond to SVHC listings, Safer Consumer Products regulations, and ISO-aligned fire testing frameworks.

In August 2024, BlackRock, Inc. acquired Albemarle Corporation, strengthening investment exposure to both bromine and emerging halogen-free flame retardant technologies supporting green energy applications. In October 2024, BASF SE launched Ultramid® Advanced N3U41G6, a non-halogenated PPA compound engineered for insulated-gate bipolar transistor housings in renewable energy and power electronics. In November 2024, Clariant AG introduced Exolit AP 422 A, a melamine-free ammonium polyphosphate designed for intumescent coatings following melamine’s SVHC classification. In December 2024, South Korea aligned national building board regulations with ISO 5660-1 fire testing standards, effectively accelerating replacement of legacy halogenated additives with aluminum and magnesium hydroxide systems.

Regulatory and portfolio shifts intensified in 2025. In January 2025, LANXESS AG entered a global distribution agreement with FRX Polymers, Inc. for the Nofia® brand of polymeric halogen-free flame retardants, expanding penetration in construction and consumer electronics markets. In March 2025, California listed tetrabromobisphenol A as a Priority Product under its Safer Consumer Products program, accelerating migration toward phosphorus-based alternatives in electronic housings. In May 2025, J.M. Huber Corporation acquired alumina trihydrate and antimony-free flame retardant assets from The R.J. Marshall Company, reinforcing its North American ATH and smoke suppressant portfolio. In June 2025, BASF introduced Ultramid® Advanced N3U42G6, a non-halogenated PPA compound minimizing electro-corrosion in 800V+ EV connectors. In November 2025, Clariant completed a CHF 100 million expansion at its Daya Bay site in China, adding a second Exolit OP production line to support high-voltage e-mobility platforms. During late 2025, LANXESS promoted Levagard 2100, a reactive phosphonate flame retardant chemically bonded into PUR and PIR foam matrices to reduce migration and volatility compared to TCPP.

Market restructuring and pricing dynamics shaped 2026 performance. In January 2026, Clariant formed a joint venture with FUHUA in Sichuan to develop next-generation phosphorus-based non-halogenated flame retardants tailored to automotive and electronics regulatory environments. Effective January 1, 2026, Huber Advanced Materials implemented a global 5% to 15% price increase across its fire retardant portfolio due to U.S. tariffs on imported ATH feedstock and elevated freight and compliance costs.

The Halogen Free Flame Retardant Chemicals Market outlook reflects accelerating EV battery system requirements, high-voltage connector safety upgrades, global building code harmonization, antimony-free and melamine-free reformulation, ATH and magnesium hydroxide substitution, and strategic joint ventures in Asia. Competitive differentiation increasingly depends on phosphorus chemistry innovation, feedstock security, compliance with SVHC and U.S. state regulations, reactive polymer integration, and high-performance thermal and dielectric properties for automotive, electronics, and construction applications.

Halogen-Free Flame Retardant (HFFR) Chemicals Market Trends and Strategic Opportunities

OEM-Led Mandates Accelerate Halogen-Free Adoption in Consumer Electronics

The halogen-free flame retardant chemicals market is increasingly shaped by binding sustainability standards set by global consumer electronics OEMs rather than by regulation alone. Leading brands have embedded strict halogen-free thresholds into supplier codes of conduct, effectively making HFFR materials the default choice for printed circuit boards, device housings, connectors, and internal wiring. By late 2025, OEM specifications defined halogen-free content as no more than 900 ppm of chlorine or bromine individually and 1,500 ppm in total, a benchmark that has become non-negotiable for suppliers serving premium smartphones, laptops, and network equipment.

This shift is also technology driven. High-frequency 5G and RF devices require low dielectric constants and minimal signal loss, pushing materials engineers toward phosphorus-nitrogen HFFR systems that deliver dielectric constants below 3.5 while eliminating halogen-related reliability risks. To support rising demand, Clariant commissioned a second production line at its Daya Bay site in November 2025 as part of a CHF 100 million investment, expanding output of Exolit OP solutions used to achieve UL 94 V-0 ratings in thin-walled electronic enclosures. At the same time, sustainability disclosures such as Apple’s 2025 Environmental Progress Report are amplifying supply chain pressure for recycled or renewable inputs, accelerating R&D into bio-based HFFR resins that combine flame retardancy with reduced lifecycle emissions.

Strategic M&A and Vertical Integration Redefine HFFR Formulation Models

Another defining trend is the transition from stand-alone additive sales to integrated HFFR systems delivered by vertically integrated providers. Chemical producers are consolidating specialized assets to offer complete, application-ready flame retardant packages that ensure compatibility with target polymers and simplify qualification for OEM customers. In May 2025, J.M. Huber Corporation acquired alumina trihydrate, antimony-free flame retardant, and molybdate-based smoke suppressant assets from The R.J. Marshall Company, strengthening its position as a full-spectrum supplier for wire, cable, and composite applications.

Localized innovation is also gaining importance. In November 2025, Clariant and FUHUA formed a joint venture in Sichuan to develop next-generation phosphorus-based HFFR solutions tailored to regional building and automotive standards. Portfolio refinement among majors underscores this focus on specialty value creation. LANXESS completed its exit from commodity polymer businesses in April 2025 and is reallocating capital toward its Specialty Additives segment, prioritizing high-efficiency, bromine-free systems that mitigate raw material volatility while meeting stringent regulatory and OEM requirements.

High-Voltage HFFR Solutions for Electric Vehicle Battery Architectures

Electrification of transport is unlocking a high-growth opportunity for halogen-free flame retardant chemicals capable of operating in 800-volt and higher battery systems. EV battery packs demand materials that simultaneously prevent thermal runaway propagation and provide reliable electrical insulation under sustained heat and humidity. HFFR-based tapes, encapsulants, and thermoplastics are increasingly specified to meet these dual requirements while supporting lightweight design.

Product launches in 2025 highlight this shift. Clariant introduced Exolit OP 1266 TP in October 2025, delivering a comparative tracking index of 600 volts in polybutylene terephthalate even after prolonged moisture exposure. Weight reduction is another critical driver. Polymer solutions reinforced with HFFR additives can replace metal shields, improving vehicle range without compromising fire safety. SABIC and Dow are advancing HFFR composite concepts for battery covers that pass large-scale fire tests while significantly reducing mass. Regulatory momentum from standards such as UN R136 and China’s GB 38031 further reinforces demand by mandating improved thermal protection and containment performance in EV batteries worldwide.

Smoke-Suppressing HFFR Systems for Public Safety and Infrastructure

Public safety regulations are creating a parallel opportunity for HFFR systems optimized not only for flame resistance but also for smoke suppression. Building and transport codes increasingly emphasize low smoke and low toxicity materials, recognizing that smoke inhalation is the leading cause of fatalities in enclosed fires. Low Smoke Zero Halogen materials are now prioritized in rail, metro, commercial buildings, and airports.

Innovation in this area is accelerating. In March 2024, Clariant launched Exolit AP 422, a melamine-free, REACH-approved ammonium polyphosphate designed for PIR insulation panels and polyurethane foams used in high-occupancy buildings. Updates to International Building Code requirements during 2024 and 2025 have intensified focus on smoke migration and air leakage, driving demand for HFFR-enhanced curtains, gaskets, and compartmentation systems. Providers such as Smoke Guard are deploying these solutions in retrofits of open-plan commercial structures to improve evacuation safety.

Aerospace and defense applications add a high-margin dimension to this opportunity. The U.S. Environmental Protection Agency’s 2025 updates under the Toxic Substances Control Act, particularly around PFAS and legacy flame retardants, are forcing aircraft manufacturers to redesign wire and cable insulation. This recalibration favors advanced HFFR formulations that combine smoke suppression with extreme thermal and mechanical resilience, positioning specialty chemical suppliers with proven halogen-free technologies for sustained growth across safety-critical infrastructure markets.

Halogen Free Flame Retardant Chemicals Market Share and Segmentation Insights

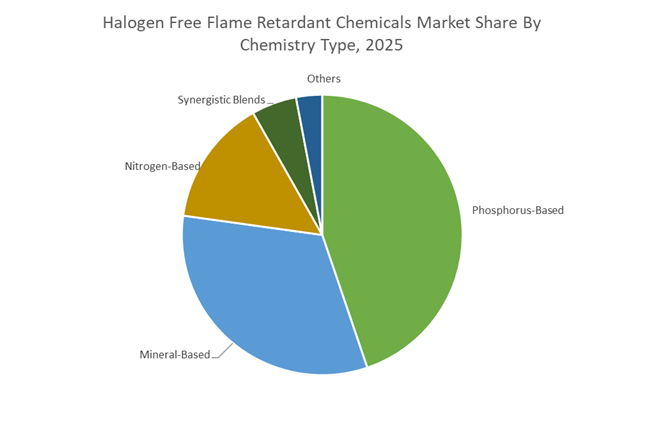

Phosphorus-Based Systems Lead the Halogen Free Flame Retardant Chemicals Market in Engineering Plastics and Electronics

Phosphorus-Based flame retardants accounted for 44.80% of the Halogen Free Flame Retardant Chemicals Market share in 2025, making them the dominant chemistry category across multiple polymer applications. Phosphorus-based systems including organophosphates, phosphinates, and red phosphorus formulations provide highly efficient flame retardancy through both gas-phase radical quenching and condensed-phase char formation mechanisms, allowing them to protect a wide range of polymer matrices. These chemistries are particularly effective in engineering plastics, epoxy resins, thermoplastics, and high-performance composite materials used in electrical, automotive, and industrial applications. Their ability to meet stringent fire safety standards while complying with environmental regulations restricting halogenated flame retardants has accelerated adoption across global manufacturing industries. In 2025, the segment is experiencing strong growth through the increasing use of phosphinate-based flame retardants, particularly aluminum diethylphosphinate, which demonstrates excellent thermal stability in high-temperature polymer systems such as polyamides and polyesters. These advanced materials maintain performance at processing temperatures approaching 350°C, making them highly suitable for miniaturized electronic components.

Electrical and Electronics Industry Drives the Largest Demand for Halogen Free Flame Retardant Chemicals

Electrical and Electronics represented 42.60% of the Halogen Free Flame Retardant Chemicals Market share in 2025, establishing it as the leading end-use industry for halogen-free flame retardant systems. Modern electronic devices rely heavily on flame retardant polymers used in circuit boards, connectors, electrical housings, cable insulation, and electronic component casings, where strict fire safety standards must be met to prevent ignition and flame propagation. Regulations such as RoHS and WEEE in Europe, along with corporate sustainability commitments to eliminate halogenated additives, have significantly accelerated the adoption of halogen-free flame retardant formulations in electronic materials. In 2025, the electronics industry is experiencing increasing demand for advanced flame retardant solutions driven by 5G infrastructure expansion and the miniaturization of electronic components. As devices become smaller and more powerful, heat generation within compact electronic systems increases, requiring highly efficient flame retardant additives that can achieve UL 94 V-0 fire safety ratings at lower additive loadings. Phosphorus-based flame retardant systems designed for high-frequency electronic materials also help maintain electrical signal integrity while providing fire protection.

Competitive Landscape in Halogen Free Flame Retardant Chemicals Market

Clariant AG Expands Phosphorus-Based Exolit Portfolio for E-Mobility

Clariant AG remains a global leader in phosphorus-based halogen free flame retardants through its Exolit® brand, widely adopted in EV battery housings and engineering thermoplastics. In November 2025, Clariant signed a joint venture agreement with FUHUA to establish a new production facility in Sichuan, China, dedicated to next-generation phosphorus flame retardants. The expansion of its Daya Bay facility with a second Exolit® OP production line represents a CHF 100 million investment aimed at strengthening Asian supply security. Its Exolit® OP Terra line utilizes mass-balance certified renewable feedstocks and delivers approximately 20% lower carbon footprint while maintaining UL 94 V-0 performance even after multiple recycling cycles. In 2026, Clariant is also advancing titanium-based catalyst technology for polyesters as a sustainable alternative to antimony systems.

LANXESS AG Advances Reactive and Polymeric Flame Retardant Systems

LANXESS AG is prioritizing reactive and polymeric halogen free flame retardant systems to minimize additive migration and VOC emissions. In October 2025, the company introduced Levagard® 2100, a reactive phosphonate that chemically bonds into rigid PU and PIR foam matrices, eliminating leaching while improving fire classification performance. Under its FORWARD! optimization strategy, LANXESS is emphasizing Emerald Innovation® 5000 as a polymeric alternative to legacy brominated retardants such as DBDPE. The company is also expanding Pocan® BFN PBT compounds that achieve 600V CTI and enhanced glow-wire resistance for EV charging units and unattended appliances. In parallel, LANXESS reduced the carbon footprint of its Mesamoll® plasticizer line by approximately 20% through carbon-reduced raw materials.

ICL Group Scales Flame Retardant Solutions for EV Thermal Runaway Protection

ICL Group is intensifying its focus on flame retardant solutions engineered for lithium-ion battery thermal runaway protection. The company supplies over 50 specialized flame retardant formulations tailored for automotive powertrains, battery casings, and high-voltage charging systems. In 2026, ICL is transitioning from pilot-stage innovation to full commercial execution of polymeric and reactive phosphorus-based systems designed for New Energy Vehicle safety compliance. Leveraging its control over Dead Sea mineral resources, ICL ensures stable access to phosphorus and inorganic intermediates amid global supply volatility. The company is integrating AI-driven ROI analytics into manufacturing operations to enhance process efficiency and support carbon-neutral targets by 2030, reinforcing its competitive advantage in climate-aligned fire safety materials.

Huber Engineered Materials Strengthens Antimony-Free Mineral Portfolio

Huber Engineered Materials, a division of J.M. Huber Corporation, is a global leader in mineral-based halogen free flame retardants such as alumina trihydrate and magnesium hydroxide. In May 2025, Huber acquired the ATH and smoke suppressant assets of The R.J. Marshall Company, strengthening its North American position in antimony-free fire safety technologies. Through its Huber Advanced Materials unit, the company is expanding Hydral®, MAGNIFIN®, and molybdate-based Kemgard® systems that provide dual flame retardancy and smoke suppression in PVC and engineering plastics. With four production sites in North America and two in Europe, Huber acts as a strategic supplier for building and construction segments requiring low smoke, low toxicity performance. Its mineral-based fillers are increasingly specified for LSZH cable compounds and infrastructure applications.

Albemarle Corporation Balances Bromine Legacy with Polymeric Innovation

Albemarle Corporation continues to play a significant role in the global fire safety chemicals market while diversifying into halogen free polymeric systems. Following its August 2024 acquisition by BlackRock, institutional capital has accelerated Albemarle’s strategy to integrate lithium expertise with advanced fire protection technologies. The company markets SAYTEX ALERO®, a polymeric flame retardant engineered for recyclability and tailored mechanical performance in electronics and EV components. In 2026, Albemarle is aligning its SAYTEX® portfolio with e-mobility and digitalization trends, targeting thin-wall electronics and high-voltage modules requiring stringent fire resistance. Its global manufacturing footprint supports compliance with international fire safety standards designed to maximize life-saving escape time in residential and commercial infrastructure.

Nabaltec AG Expands Functional Fillers for LSZH and 5G Applications

Nabaltec AG is a specialized European producer of aluminum hydroxide and magnesium hydroxide functional fillers used in halogen free flame retardant systems. Its Functional Fillers segment generated EUR 114.1 million in revenue during the nine-month 2024 interim period, reflecting strong demand for sustainable compliance materials. The company is expanding into 5G telecommunications and miniaturized electronics, supplying ultra-fine surface-treated fillers with low dielectric constants. Through its APYRAL® and ETHAPOL® brands, Nabaltec plays a critical role in Low Smoke Zero Halogen cable insulation for global wire and cable markets. Its Lightweight Safety strategy focuses on enabling high filler loading in polyethylene compounds without compromising tensile strength, meeting evolving building code and EV infrastructure requirements.

China: Regulatory Acceleration and Phosphorus-Based Manufacturing Scale-Up

China remains the most structurally influential country within the halogen free flame retardant chemicals industry, driven by a combination of regulatory tightening, cost-driven material substitution, and deep integration with downstream automotive, electronics, and construction clusters. The enforcement of the GB 8624-2025 fire safety standard has materially reshaped demand patterns, mandating A-class flame resistance for fabrics used in public buildings. This regulation alone has triggered a documented 38% annual rise in domestic demand for halogen-free textile flame retardants, accelerating the displacement of brominated and antimony-based systems.

On the supply side, China’s transition toward phosphorus-based HFFRs is reinforced by large-scale capital investments. In November 2025, Clariant finalized a joint venture with Fuhua to construct a dedicated next-generation phosphorus flame retardant plant in Leshan, Sichuan. This development strengthens domestic supply resilience for automotive plastics and construction polymers. In parallel, Clariant operationalized its second production line at Daya Bay, a CHF 100 million expansion aimed squarely at Exolit OP phosphinate flame retardants for the Asian e-mobility value chain, particularly high-voltage electric drivetrains.

China’s industrial geography further reinforces this momentum. By 2025, the Yangtze River Delta accounted for 42% of national HFFR output, benefitting from proximity to global electronics assembly, EV battery manufacturing, and polymer compounding hubs. Cost volatility has also accelerated structural change. With antimony trioxide prices reaching USD 51,500 per ton in early 2025, manufacturers have rapidly shifted to ATO-free phosphorus systems to stabilize formulations and reduce exposure to geopolitical raw material risks. At the innovation frontier, researchers at Tsinghua University successfully commercialized a graphene oxide layered double hydroxide hybrid in late 2025, achieving UL 94 V-0 certification with only 8% additive loading, fundamentally improving efficiency metrics versus traditional inorganic hydroxides.

United States: Policy-Led Adoption and High-Voltage Performance Engineering

The United States halogen free flame retardant chemicals market is increasingly shaped by regulatory incentives, aerospace safety standards, and advanced materials engineering for electric mobility and electronics. The expansion of the EPA Safer Choice program for 2026 has created a formal pull mechanism favoring mineral-based and bio-based HFFRs in consumer electronics and home furnishing applications. This policy alignment is prompting OEMs to specify halogen-free chemistries earlier in product design cycles, rather than as post-compliance substitutions.

Aerospace regulation has emerged as another decisive catalyst. The Federal Aviation Administration updated 14 CFR Part 25 in 2025, tightening vertical flame test requirements for aircraft interior textiles to a 12-second compliance window. This shift has materially increased adoption of phosphorus-nitrogen synergistic systems, which deliver faster char formation and lower smoke density compared to legacy solutions. Supply chain readiness is also improving. Huber Advanced Materials, a unit of J.M. Huber Corporation, strengthened its North American distribution infrastructure in 2025 through an expanded partnership with Nordmann, focusing on high-purity magnesium and aluminum hydroxides for rubber and elastomer compounds.

From an innovation standpoint, U.S. chemical producers are increasingly prioritizing hydrolysis-stable HFFRs to protect next-generation EV battery systems operating above 800 volts. The 2025 launch of Exolit OP 1242 exemplifies this shift, addressing long-term thermal stability and electrical insulation reliability in high-energy-density battery packs. Collectively, these developments position the United States as a performance-driven HFFR market where regulatory compliance, safety certification, and advanced electrical requirements converge.

Germany: Circular Economy Alignment and Reactive Flame Retardant Leadership

Germany’s halogen free flame retardant chemicals industry is defined by regulatory certainty, sustainability-driven reformulation, and leadership in reactive phosphorus technologies. The implementation of EU REACH Annex XVII restrictions in January 2025, which prohibit brominated flame retardants in textile applications, has effectively forced a full transition toward phosphorus-based intumescent and reactive systems among German suppliers. This regulatory clarity has reduced transitional ambiguity and accelerated capital deployment into compliant chemistries.

At the technology level, Lanxess showcased Levagard 2100 at the K 2025 trade fair, a next-generation reactive phosphorus flame retardant designed for rigid PUR and PIR foams. Unlike additive systems, Levagard 2100 chemically bonds into the polymer backbone, sharply reducing migration, VOC emissions, and long-term performance degradation. This characteristic is particularly relevant for insulation materials used in energy-efficient buildings, where durability and indoor air quality are tightly regulated.

Sustainability certification has become a competitive differentiator. In late 2025, leading German producers including Evonik and Lanxess achieved ISCC PLUS certification for mass-balanced bio-circular flame retardant portfolios. This aligns German HFFR production with the EU circular economy roadmap and provides downstream manufacturers with verifiable sustainability credentials. As a result, Germany increasingly functions as the EU’s reference market for low-emission, circular-compliant flame retardant systems.

India: Safety Regulation Formalization and Bio-Based Innovation Uptake

India’s halogen free flame retardant chemicals market is transitioning from voluntary adoption to mandatory compliance, driven by formal safety standards and infrastructure-led demand. In December 2025, the Bureau of Indian Standards implemented compulsory BIS certification for HFFR cables, requiring verified compliance on smoke density, halogen-free toxicity, and fire propagation performance. This mandate has materially increased demand for certified phosphorus-based cable compounds across power distribution, railways, and commercial construction.

Policy-driven innovation is also shaping market structure. Under the national BioE3 initiative, the Indian government has allocated R&D grants to accelerate development of lignin-chitosan composite flame retardants for the domestic cotton textile sector. These bio-based systems address both flame resistance and environmental compatibility, supporting India’s broader bioeconomy objectives. Infrastructure expansion provides additional pull. The Central Pollution Control Board issued 2025 guidelines encouraging halogen-free materials across metro rail and airport projects, explicitly linking low-smoke material performance to evacuation safety standards.

Japan: Precision Electronics and Semiconductor-Grade Flame Retardants

Japan’s role in the halogen free flame retardant chemicals industry is increasingly anchored in high-purity, electronics-grade applications rather than volume-driven markets. Tosoh Corporation expanded its bromine-free phosphorus derivative capacity under its 2024–2025 strategic plan, targeting advanced electronics manufacturers across the Asia-Pacific region. This expansion supports Japan’s competitive positioning in high-value polymer additives where consistency and trace impurity control are critical.

Looking ahead to 2026, Japanese firms are pioneering semiconductor-grade HFFRs with ultra-low ion content designed for advanced packaging and signal-sensitive applications. Traditional flame retardants often introduce ionic contamination that interferes with signal integrity and long-term reliability. By engineering ultra-clean phosphorus systems, Japanese suppliers are aligning HFFR innovation with next-generation semiconductor performance requirements, reinforcing Japan’s niche leadership in precision flame retardant chemistry.

Summary Table: Country-Level Strategic Signals in the HFFR Chemicals Industry

Halogen Free Flame Retardant Chemicals Market County Level Snapshot

|

Country

|

Regulatory Driver

|

Industrial Focus

|

Strategic Signal

|

|

China

|

GB 8624-2025 fire safety mandate

|

Phosphorus-based scale-up, ATO substitution

|

Cost stabilization and EV-led demand

|

|

United States

|

EPA Safer Choice, FAA Part 25

|

High-voltage EV systems, aerospace textiles

|

Performance-driven compliance

|

|

Germany

|

REACH Annex XVII, ISCC PLUS

|

Reactive and bio-circular HFFRs

|

Circular economy leadership

|

|

India

|

BIS certification, CPCB guidelines

|

Infrastructure cables, bio-based textiles

|

Formalized safety adoption

|

|

Japan

|

Electronics purity standards

|

Semiconductor-grade HFFRs

|

Precision chemistry leadership

|

Halogen Free Flame Retardant Chemicals Market Report Scope

Halogen Free Flame Retardant Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$12.6 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Chemistry Type (Phosphorus-Based, Mineral-Based, Nitrogen-Based, Synergistic Blends, Other Halogen-Free Systems), By Polymer Type (Polyolefins, Engineering Plastics, Epoxy and Polyurethane Systems, Vinyl and Elastomers), By End-Use Industry (Electrical and Electronics, Automotive and Transportation, Building and Construction, Aerospace and Defense, Textiles and Furnishings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Clariant AG, LANXESS AG, ICL Group, BASF SE, Huber Engineered Materials, Albemarle Corporation, ADEKA Corporation, Nabaltec AG, Kisuma Chemicals, Italmatch Chemicals S.p.A., Avient Corporation, Budenheim KG, Martin Marietta Magnesia Specialties, Thor Group, Hangzhou Lingrui Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Halogen Free Flame Retardant Chemicals Market Segmentation

By Chemistry Type

- Phosphorus-Based

- Mineral-Based

- Nitrogen-Based

- Synergistic Blends

- Other Halogen-Free Systems

By Polymer Type

- Polyolefins

- Engineering Plastics

- Epoxy and Polyurethane Systems

- Vinyl and Elastomers

By End-Use Industry

- Electrical and Electronics

- Automotive and Transportation

- Building and Construction

- Aerospace and Defense

- Textiles and Furnishings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Halogen Free Flame Retardant Chemicals Market

- Clariant AG

- LANXESS AG

- ICL Group

- BASF SE

- Huber Engineered Materials

- Albemarle Corporation

- ADEKA Corporation

- Nabaltec AG

- Kisuma Chemicals

- Italmatch Chemicals S.p.A.

- Avient Corporation

- Budenheim KG

- Martin Marietta Magnesia Specialties

- Thor Group

- Hangzhou Lingrui Chemical

*- List not Exhaustive